옥상 태양광 발전 설비 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Rooftop Solar Photovoltaic Installation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1689783

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

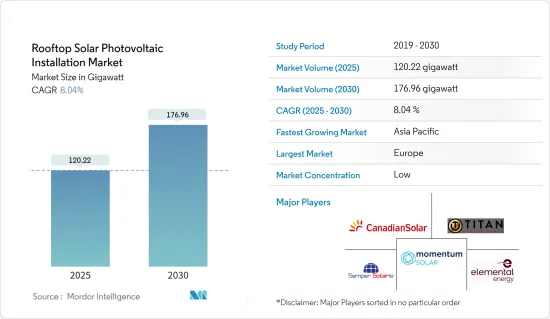

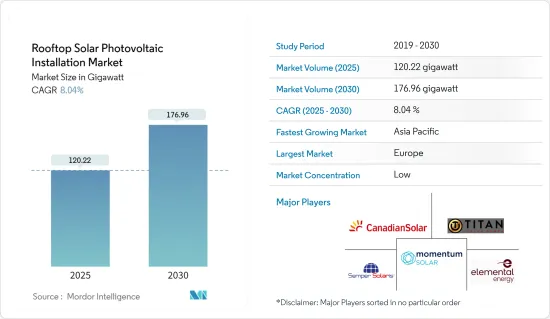

세계의 옥상 태양광 발전 설비 시장 규모는 2025년 120.22기가와트로 추정되며, 예측 기간 중(2025-2030년) CAGR 8.04%로 확대되어, 2030년에는 176.96기가와트에 달할 것으로 예측됩니다.

시장은 2020년 COVID-19에 의해 부정적인 영향을 받았습니다.

장기적으로는 태양광 패널 설비에 대한 우대조치나 세제우대조치 등의 형태로 정부의 지원시책이 뒷받침되고, PV 설비 비용의 저하나 패널 효율의 상승이 예측기간 중 시장을 견인할 것으로 보입니다.

한편, 초기설비투자가 고액인 것이 예측기간 중 시장성장을 방해할 것으로 예상됩니다.

신기술의 진보와 페로브스카이트 태양전지 시장 개척은 향후 옥상 태양광 발전 설비 시장에 몇 가지 기회를 가져올 것으로 예상됩니다.

2022년에는 아시아태평양이 옥상설비형 태양광발전의 최대 시장이 되었습니다.

옥상 태양광 발전 설비 시장 동향

주택용 옥상 설비가 시장을 독점할 전망

주택 부문에는 개인 주택이나 집합 주택이 포함됩니다.주택의 옥상 설비형 시스템은 업무용이나 산업용의 옥상 설비형 시스템에 비해 소규모입니다.

주택용 옥상 태양광 발전 시스템의 도입은 비용의 저하와 정부의 지원 시책에 의해 최근 세계에서 대폭 증가하고 있습니다. 합리적인 가격으로 신뢰할 수 있는 전력 옵션을 주민이 필요로 하는 다양한 나라로부터, 주택용 옥상 시스템 수요가 높아지고 있습니다. 많은 나라에서는 태양광 발전으로 발전된 전력은 송전망으로부터 전력을 구입하는 것보다 경제적으로 매력적입니다.

예를 들어 미국에서는 최근 몇 년간 주택용 지붕상 태양광 발전의 설비 용량이 급속히 증가하고 있습니다.

게다가 2022년, 미국의 주택용 태양광 발전 시스템의 평균 비용은 1 와트당 3.21 달러였습니다.

유럽연합(EU)은 태양광 패널의 국내 생산을 적극적으로 추진하고 있으며, 에넬 그린파워사가 유럽연합(EU)과 협력하여 이탈리아에 있는 태양광 패널의 기가팩토리를 확대한 것 등이 그 예입니다. 자금 지원을 받고, 엔넬 그린 파워사는 생산 능력을 기존의 20만 킬로와트에서 15배 증가한 300만 킬로와트로 확대하는 것을 목표로 하고 있습니다. 중국, 인도, 호주 등의 국가에서는 주택 부문에서의 태양에너지 프로젝트를 촉진하고 설비 비용을 삭감하기 위한 정부의 대처에 의해 주택용 지붕의 요구가 최근 몇 년 동안 높아지고 있습니다.

예를 들어 인도 정부는 신재생에너지부(MNRE)의 계통연계 지붕상 태양광발전 프로그램의 제2단계를 시작했습니다.

이상으로부터, 주택용 지붕 설비형 태양광 발전 시장은 예측 기간 중에 우위에 선다고 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양 국가에서는 급속한 도시화, 인구 증가, 공업화가 진행되어 전력 소비량이 대폭 증가하고 있습니다.

게다가 아시아태평양은 태양광량이 풍부하고 태양광 발전에 매우 적합합니다.

중국에는 세계 최대의 태양광 발전(PV) 제조 기업과 시설이 거의 모두 있으며, 세계의 태양광 발전 제조 능력의 70% 가까이가 중국에 있습니다.

게다가 정부의 적극적인 시책과 인센티브는 아시아태평양을 옥상용 태양광 발전 시장의 최전선으로 밀어 올리는데 있어 매우 중요한 역할을 하고 있습니다. 지붕상 태양광 발전 시스템의 도입을 장려하는 규제 틀 등, 강력한 지원 메커니즘을 도입하고 있습니다. 이러한 인센티브는 소비자나 기업의 경제적 부담을 경감해, 시장의 급성장을 가속하고 있습니다.

2022년 6월 호주 정부는 새로운 지붕상 태양광 발전 규제를 발표했습니다.

설비업체, 태양광소매업체, 제조업자에 대한 보고요건을 합리화합니다.

이상의 사실들로부터, 예측 기간중, 아시아태평양이 옥상 태양광 발전 설비 시장을 독점할 것으로 예상됩니다.

옥상 태양광 발전 설비 산업 개요

옥상 태양광 발전 설비 시장은 그 특성상 통합되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위: 달러)

2029년까지의 옥상 설비형 태양광 발전(PV) 시장(GW 베이스)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

태양전지판의 비용 저하

정부의 지원 시책

억제요인

초기 비용의 높이

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

도입 장소

주택용

상업 및 산업

지역(지역 시장 분석(2029년까지 시장 규모 및 수요 예측(지역만)))

북미

미국

캐나다

기타 북미

아시아태평양

중국

인도

호주

일본

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

유럽

독일

영국

스페인

이탈리아

프랑스

북유럽 국가

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

카타르

남아프리카

이집트

나이지리아

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Titan Solar Power NV Inc.

Momentum Solar

Canadian Solar Inc.

Elemental Energy Inc.

Semper Solaris Construction Inc.

Pink Energy

ReVision Energy LLC

ADT Solar

Baker Electric Home Energy

Infinity Energy Inc.

시장 랭킹/점유율 분석

제7장 시장 기회와 앞으로의 동향

신기술의 진보와 페로브스카이트 태양전지의 개발

JHS

영문 목차

영문목차

The Rooftop Solar Photovoltaic Installation Market size is estimated at 120.22 gigawatt in 2025, and is expected to reach 176.96 gigawatt by 2030, at a CAGR of 8.04% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Over the long term, supportive government policies in the form of incentives and tax benefits for solar panel installation, declining PV installation costs, and rising panel efficiencies are expected to drive the market during the forecast period.

On the other hand, high initial capital investment are expected to hinder the growth of the market during the forecasted period.

Nevertheless, new technological advancements and the development of perovskite solar cells are expected to create several opportunities for the rooftop solar PV installation market in the future.

Asia-Pacific was the largest market for rooftop solar PV installation in 2022. The region is also likely to be the fastest-growing market during the forecast period due to the presence of several developing economies, such as China and India.

Rooftop Solar Photovoltaic Installation Market Trends

Residential Rooftop Installation Expected to Dominate the Market

The residential segment includes individual houses and residential building complexes. Residential rooftop-mounted systems are small compared to commercial and industrial rooftop systems. The residential rooftop solar PV system typically has a capacity range of up to 50 kW.

The deployment of residential rooftop solar PV systems has increased significantly in recent years worldwide, owing to the declining costs and the government's supportive policies. Residential rooftop solar PV installations can be arranged in smaller configurations for mini-grids or personal use. There is a rise in demand for residential rooftop systems from various countries where residents need accessible, affordable, and reliable electricity options. In many countries, the electricity generated from solar PV is more economically attractive than buying electricity from the grid.

For instance, in the past couple of years, the United States experienced rapid growth in residential rooftop solar installed capacity; according to the Solar Energy Industries Association, the residential rooftop solar PV installed capacity grew by around 40% between 2021 and 2022. In 2022, the annual installed capacity was 5.9 GW compared to 4.2 GW in 2021.

Further, In 2022, the average cost of residential solar systems in the United States stood at USD 3.21 per watt. Although the price of residential solar has slightly increased in the last three years, it is still less than half the average cost registered in 2010. The decrease in the cost of residential solar systems has contributed to the significant increase in the solar capacity installed in United States households across the country.

The European Union is actively promoting the domestic production of solar panels, exemplified by initiatives such as Enel Green Power's collaboration with the European Union to expand a solar panel Gigafactory located in Italy. Supported by European Union funding, Enel Green Power aims to increase its production capacity by a significant factor, specifically fifteen-fold, from the existing 200 MW to a substantial 3 GW. Anticipated to be operational by July 2024, this production facility represents a considerable investment totaling approximately USD 630 million, with an expected contribution from the European Union of around USD 124 million. This concerted effort is poised to drive down the cost of rooftop solar panels in the near term and to stimulate heightened demand for residential rooftop solar systems throughout Europe. The need for residential rooftops has increased in countries such as China, India, and Australia in the past couple of years due to government initiatives to promote solar energy projects in the residential sector and reduce installation costs.

For instance, the Government of India initiated phase II of the Ministry of New and Renewable Energy's (MNRE) grid-connected rooftop solar program. Under this program, in April 2022, the Tamil Nandu Energy Development Agency issued a tender to install 12 MW of grid-connected residential rooftop solar systems in Tamil Nandu. Similarly, Telangana state's Renewable Energy Department Corporation invited bids to appoint suppliers to build 50 MW of grid-connected residential rooftop solar projects.

Therefore, owing to the above points, the residential rooftop solar PV installation market is expected to dominate during the forecast period.

Asia-Pacific Expected to Dominate the Market

Rapid urbanization, population growth, and industrialization across Asia-Pacific countries have fueled a substantial rise in electricity consumption. In response, governments and businesses are increasingly turning to rooftop solar PV installations as a viable means to augment energy supply while addressing environmental concerns.

Moreover, the Asia-Pacific region offers an abundance of sunlight, making it exceptionally conducive to solar energy generation. The favorable climatic conditions and technological advancements in solar panel efficiency ensure optimal energy yield from rooftop installations. This natural advantage bolsters the region's attractiveness and viability of solar PV installations.

China is home to nearly all the largest solar photovoltaic (PV) manufacturing companies and facilities globally, with almost 70% of the global solar PV manufacturing capacity in China. These companies also dominate other businesses, such as polysilicon, ingot, and wafer-making, which are integral to the solar panel supply chain. This extraordinary control of the global solar PV supply chain puts Chinese manufacturers at a more significant advantage when compared to solar equipment manufacturers from other countries.

Furthermore, proactive government policies and incentives play a pivotal role in propelling Asia-Pacific to the forefront of the rooftop solar PV market. Governments across the region have implemented robust support mechanisms, including feed-in tariffs, tax credits, and regulatory frameworks that encourage the adoption of rooftop solar PV systems. These incentives reduce the financial burden on consumers and businesses, stimulating rapid market growth.

In June 2022, the Australian government released new rooftop solar PV regulations. The government committed USD 19.2 million in the 2021-22 budget to reform the SRES (Small-scale Renewable Energy Scheme). The amendment regulations aim to protect consumers better and improve integrity in the rooftop solar sector. The amendments are as follows:

Streamline reporting requirements for installers, solar retailers, and manufacturers. Allow the Regulator to take a more direct role in setting the conditions for solar PV components eligible for small-scale technology certificates. Such mandates are expected to see a massive rise in rooftop solar PV adoption during the forecast period.

Therefore, owing to the above points, Asia-Pacific is expected to dominate the rooftop solar PV installation market during the forecast period.

Rooftop Solar Photovoltaic Installation Industry Overview

The rooftop solar installations market is consolidated in nature. Some of the key players in the market (in no particular order) include Titan Solar Power NV Inc, Momentum Solar, Canadian Solar Inc., Elemental Energy Inc., and Semper Solaris Construction Inc, and among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Rooftop Solar Photovoltaic (PV) Installed Market in GW, till 2029

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.1.1 Declining Solar Panel Costs

4.6.1.2 Supportive Government Policies

4.6.2 Restraints

4.6.2.1 High Upfront Cost

4.7 Supply Chain Analysis

4.8 Porter's Five Forces Analysis

4.8.1 Bargaining Power of Suppliers

4.8.2 Bargaining Power of Consumers

4.8.3 Threat of New Entrants

4.8.4 Threat of Substitute Products and Services

4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Location of Deployment

5.1.1 Residential

5.1.2 Commercial and Industrial

5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Asia-Pacific

5.2.2.1 China

5.2.2.2 India

5.2.2.3 Australia

5.2.2.4 Japan

5.2.2.5 Malaysia

5.2.2.6 Thailand

5.2.2.7 Indonesia

5.2.2.8 Vietnam

5.2.2.9 Rest of Asia-Pacific

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Spain

5.2.3.4 Italy

5.2.3.5 France

5.2.3.6 Nordic Countries

5.2.3.7 Turkey

5.2.3.8 Russia

5.2.3.9 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 United Arab Emirates

5.2.5.3 Qatar

5.2.5.4 South Africa

5.2.5.5 Egypt

5.2.5.6 Nigeria

5.2.5.7 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Titan Solar Power NV Inc.

6.3.2 Momentum Solar

6.3.3 Canadian Solar Inc.

6.3.4 Elemental Energy Inc.

6.3.5 Semper Solaris Construction Inc.

6.3.6 Pink Energy

6.3.7 ReVision Energy LLC

6.3.8 ADT Solar

6.3.9 Baker Electric Home Energy

6.3.10 Infinity Energy Inc.

6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 New Technological Advancements and the Development of Perovskite Solar Cells