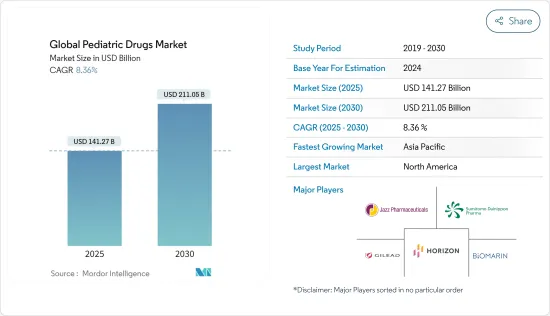

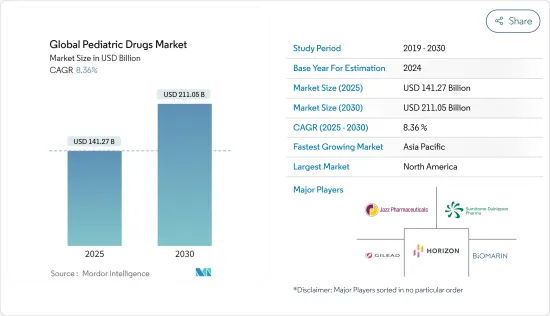

세계의 소아용 의약품 시장 규모는 2025년 1,412억 7,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 8.36%로 확대되어, 2030년에는 2,110억 5,000만 달러에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 세계 소아용 의약품 시장에 영향을 미쳤습니다. 비즈니스 세계에서 COVID-19 팬데믹은 전례없는 경제적 불확실성을 가져왔습니다. 일부 기업은 피해량이 적기 때문에 비교적 영향을 받지 않고 끝나고 있지만, 다른 많은 기업들은 유행의 영향을 회피할 수 없어 재정난에 휩쓸리고 있습니다. COVID-19의 대유행과 후속 감염 확대를 억제하기 위한 공중보건지도는 아이들의 건강과 복지에 광범위한 영향을 미치고 있습니다. 소아과 구급부문(ED)은 유행에 대응하기 위해, 케어의 제공을 급속하게 적응시켜 왔습니다.

소아용 의약품 시장의 성장을 가져오고 있는 주요 요인은 이전에 비해 출생율이 상승하고 있는 것과 소아의 치사적 증례가 증가하고 있는 것이며, 다양한 질환, 바이러스 감염증, 소화기 질환, 폐암, 영양 불량으로 인해 사망하는 것도 있습니다. UNICEF의 2020년 보고서에 따르면 2020년까지 5세 미만 어린이 500만 명이 사망할 것으로 예상됐습다. 2020년에는 매일 13,800명의 5세 미만 어린이가 사망하게 됩니다. 폐렴, 설사, 말라리아 등의 감염, 조산 및 분만 내 합병증은 여전히 세계 5세 미만 아동의 주요 사망 원인이 되었습니다. 따라서 5세 미만의 어린이 사망은 효율적인 치료가 필요합니다. 면역 결핍과 면역저하로 인한 조혈 줄기세포 이식(HSCT) 후 신장장애 및 폐기능장애 유병률의 상승은 세계 소아용 의약품 시장의 성장을 가져오고 있습니다.

면역력의 감소, 공해 증가, 다양한 알레르겐에 대한 노출은 만성 폐색성 폐질환(COPD)과 같은 만성 호흡기 질환을 유발하여 호흡기 질환 치료제 부문이 소아용 의약품 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. COPD는 세계 소아 건강 부담의 주요 원인이며, 질병의 효율적인 치료에 대한 수요가 증가하고 시장의 활성화로 이어지고 있습니다. WHO 2021에 따르면 만성폐쇄성 폐질환(COPD)은 세계 3위의 사인으로 2019년에는 323만명의 사망을 일으켰습니다. 따라서 소아의 COPD 유병률 증가는 예측 기간 동안 시장 성장을 밀어올릴 것으로 예상됩니다.

한편, 희귀 자가면역 질환 치료제 부문은 예측 기간 동안 가장 빠른 CAGR을 기록하고 시장을 독점할 것으로 예측됩니다. 이 분야의 우위성은 다양한 암, 유전성 질환, 기타 자가면역질환 환자 간의 일치율의 상승에 기인하는 이들 질환의 유병률의 상승에 기인하는 것으로 생각되며, 희귀질환 치료제의 개발을 지원 및 장려하는 인센티브를 제공합니다. 예를 들어, 2019년 5월, Jacobus pharmaceutical company은 RUZURGI(아미판프리딘) 정제에 대해 미국 식품의약국(FDA)으로부터 우선심사 및 패스트트랙 지정에 의한 승인을 취득했습니다. RUZURGI는 또한 소아에서 램버트 이튼 근무력 증후군(LEMS)의 치료제로서 희귀의약품의 지정도 받고 있습니다. 이러한 처방약은 고비용인 것도 급성장의 요인이 되고 있으며, 예측 기간 동안 세계의 소아용 의약품 시장을 견인하고 있습니다.

다양한 자가면역질환, 호흡기질환, 뇌성마비, 근위축증 등을 앓는 소아환자 증가와 더불어 미국에서 첨단기술의 채용이 급증하고 있기 때문에 북미가 소아용 의약품 시장을 독점할 것으로 예상되며 북미 시장의 주요 수익 점유율을 차지하고 있습니다.

예를 들어 Luyu Xie가 2020년 JAMA Network에 발표한 논문에 따르면 천식은 세계에서 가장 흔한 소아의 만성 질환 중 하나입니다. 미국에서는 600만 명의 어린이(인구의 약 8%)가 천식으로 진단되고 있으며 연간 의료비는 819억 달러에 이르고, 소아용 의약품에 대한 수요가 높습니다.

이 지역의 주요 기업이 소아 환자용으로 신제품을 발매하고 있는 것, 소아용 의약품에 대한 사람들의 의식을 높이기 위한 정부의 대처가 증가하고 있는 것, 희귀질환 치료제의 개발을 장려하고, 소아 의료 부담 증가를 경감하기 위해서 미국 식품의약국(USFDA)이 의약품 승인 가속화 이니셔티브를 도입해 조기 승인이 시장에서 더 많은 기회를 창출할 것으로 예상됩니다. 예를 들어, 2020년에는 항바이러스제인 Vekury(렘데시비르)가 미국 식품의약국에서 성인 및 12세 이상의 어린이에게 사용을 허가했습니다.

또한 가처분 소득 증가와 건강 관리 인프라 개선도 예측 기간 동안 세계 소아 건강 관리 시장의 성장을 뒷받침할 것으로 보입니다.

소아용 의약품 시장의 경쟁은 중간 정도이며, 여러 대기업이 참가하고 있습니다. 현재 여러 회사의 대기업이 시장 점유율로 시장을 독점하고 있습니다. 시장이 충족되지 않는 과제를 해결하기 위해 신제품을 출시하는 유력 기업도 있고 제품을 유통시키는 기업도 있습니다. 예를 들어, 2019년 4월, GSK는 미국 식품의약국(FDA)으로부터 5세부터 전신성 홍반성 루푸스(SLE) 소아의 두개 결손에 대한 미국 최초의 의약품으로 승인된 정맥 주사용(IV) Benlysta(벤리스타주)의 승인을 받았습니다.

The Global Pediatric Drugs Market size is estimated at USD 141.27 billion in 2025, and is expected to reach USD 211.05 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

The COVID-19 pandemic impacted the global pediatric drug market. In the business world, the COVID-19 pandemic has created unprecedented economic uncertainty. While some businesses are relatively insulated due to low exposure, many others have been unable to avoid the pandemic's effects and are experiencing financial hardship. The COVID-19 pandemic and subsequent public health guidance to reduce the spread of the disease have wide-reaching implications for children's health and wellbeing. Pediatric emergency departments (EDs) have rapidly adapted the provision of care in response to the pandemic.

The major factors attributing to the growth of the pediatric drugs market are a rise in the birth rate compared to previous years and the increased volume of fatal pediatric cases, which are leading to even deaths due to various diseases, viral infections, GI disorders, lung cancers, and malnutrition. According to the United Nations International Children's Emergency Fund (UNICEF) 2020 Report, 5.0 million children under five were expected to die by 2020. In 2020, this translated to 13,800 children under five dying each day. Infectious diseases such as pneumonia, diarrhea, and malaria, and preterm birth and intrapartum complications continue to be the leading causes of death among children under the age of five worldwide. Hence, deaths among children under age five demand efficient treatment. The rise in prevalence of renal or pulmonary dysfunctions following hematopoietic stem-cell transplantations (HSCT) due to defective or low immunity results in the growth of the global pediatric drugs market.

The respiratory disorder drugs segment is expected to account for the largest share of the pediatric drugs market due to lower immunity, increased pollution, and exposure to various allergens, resulting in chronic respiratory disorders such as Chronic obstructive pulmonary disease (COPD). COPD is a major cause of the global pediatric healthcare burden, leading to an increased demand for the efficient treatment of the diseases, in turn fueling the market. According to the World Health Organization 2021, Chronic Obstructive Pulmonary Disease (COPD) was the third leading cause of death worldwide, causing 3.23 million deaths in 2019. Thus, the increasing prevalence of COPD among children is expected to boost the market growth over the forecast period.

On the other hand, the rare autoimmune disorders drugs segment is anticipated to witness the fastest CAGR and dominate the market during the forecast period. The segment's dominance can be attributed to the increased prevalence of these disorders due to rising coincidences among the patients with various cancers, genetic disorders, and other autoimmune disorders, which provides incentives to assist and encourage the development of drugs for rare diseases. For instance, in May 2019, the Jacobus pharmaceutical company received approval from the US Food and Drug Administration (FDA) under Priority Review and Fast Track designations for its RUZURGI (amifampridine) tablets. Ruzurgi also received orphan drug designation for the treatment of Lambert-Eaton myasthenic syndrome (LEMS) in pediatric patients. These prescription drugs' high cost may also attribute to the fastest growth, propelling the global pediatric drugs market during the forecast period.

North America is expected to dominate the pediatric drugs market due to the rise in the volume of pediatric patient cases with kids suffering from various autoimmune disorders, respiratory disorders, cerebral palsy, and muscular atrophy, along with a steep rise in the adoption of advanced technologies in the US, which holds the major revenue share of the market in North America.

For instance, according to the article published in the JAMA Network in 2020 by Luyu Xie, asthma was one of the world's most common chronic diseases in children. In the United States, 6 million children (roughly 8% of the population) have been diagnosed with asthma, costing USD 81.9 billion in annual health care costs and resulting in high demand for pediatric drugs.

The launch of new products by key players in the region for pediatric patients, rise in government initiatives to create awareness in people for pediatric medicines, and early approvals with accelerated drug approval initiative by the USFDA to encourage the development of drugs for rare diseases and to decrease the rising pediatric burden are likely to create more opportunities in the market. For instance, in 2020, Veklury (remdesivir), an antiviral medication, was licensed by the US Food and Drug Administration for use in adults and children aged 12 and above.

Also, the rise in disposable income and improvements in healthcare infrastructure are likely to help the global pediatric healthcare market's growth over the forecast period.

The pediatric drugs market is moderately competitive and consists of several major players. A few major players are currently dominating the market in terms of market share. Some prominent players are launching new products to address the unmet challenges in the market, while others are distributing the products. For instance, in April 2019, GSK received approval from the US Food and Drug Administration (FDA) for its intravenous (IV) Benlysta (belimumab), the first medicine approved in the US for children with systemic lupus erythematosus (SLE) from as young as five years of age cranial defects. Some companies currently dominating the market include BioMarin Pharmaceutical Inc., Horizon Therapeutics PLC, Sumitomo Dainippon Pharma Co. Ltd, Gilead Sciences Inc., and Jazz Pharmaceuticals Inc.