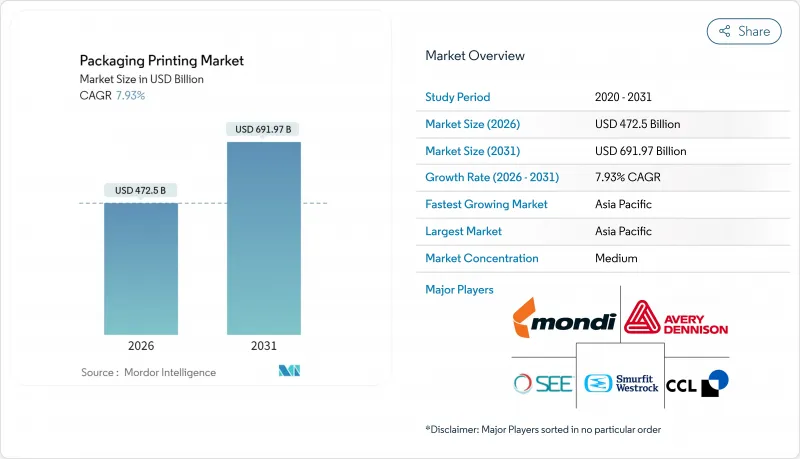

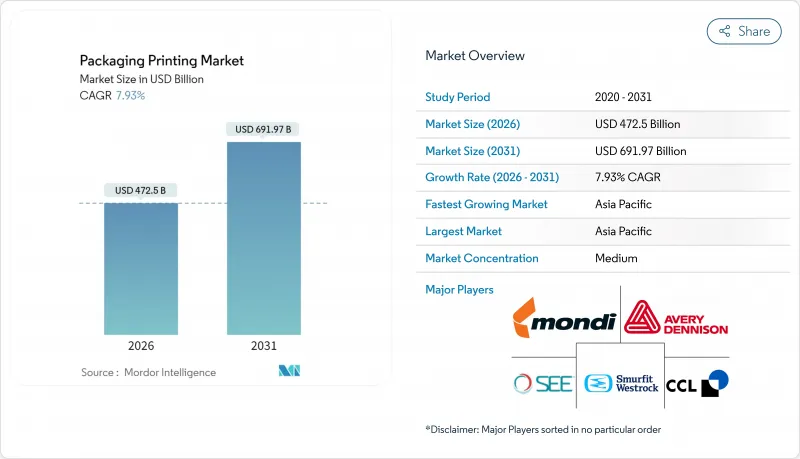

세계의 포장 인쇄 시장 규모는 2026년 4,725억 달러로 추정되고 있습니다. 이는 2025년 4,377억 8,000만 달러에서 성장한 수치이며, 2031년에는 6,919억 7,000만 달러에 달할 것으로 예측되고 있습니다. 2026년부터 2031년까지는 CAGR 7.93%로 성장할 전망입니다.

급속한 디지털 변혁, 급증하는 전자상거래 활동, 엄격한 지속가능성 정책은 기술선정, 기재선택, 지역별 투자 우선순위를 재구성하고 있습니다. 플렉소 인쇄는 긴 인쇄에 있어서 생산성에 의해 양산 면에서 우위성을 유지하고 있지만, 브랜드 오너는 현재, SKU의 다양화, 가변 데이터, 스마트 패키지 기능을 서포트하는 소량 로트 생산에 있어서 디지털 플랫폼을 선호하고 있습니다. 컨버터가 저에너지 소비와 고속 처리를 요구하는 가운데, UV 경화형 잉크 기술이 보급을 추진하고 있어 RFID 대응 패키지는 공급 체인의 가시성을 강화하고 있습니다. 전략 수준에서 컨버터는 하이브리드 인쇄 라인, 지역 밀착형 마이크로팩토리, 클로즈드 루프 소재 프로그램을 조합하여 인쇄 품질, 속도, 환경 부하가 브랜드 충성도를 좌우하는 시장에서 이익률을 지키고 있습니다.

IoT 연결의 보급으로 각 패키지가 데이터 노드로 변모하고 있습니다. 고부가가치 의약품에는 RFID를 포함한 점착 라벨이 표준 장비되고 있습니다. 디지털 인쇄기는 교체 없이 시리얼 코드를 통합하여 단가를 줄이고 실시간 인증을 가능하게 합니다. 소비자 앱이 이러한 식별자를 읽고 원산지 정보 및 충성도 혜택을 표시하여 참여도를 높이면서 리콜 관리를 지원합니다. 플렉소 인쇄 효율성과 인라인 잉크젯 모듈을 결합한 컨버터는 추적성 요구 사항을 충족하고 신속한 대응이 평가되는 계약을 획득했습니다.

소비자 직송 물류는 제품을 보호하고 그래픽을 돋보이게 하고 신속하게 도착하는 경량 형식이 우선합니다. Gelato와 같은 온디맨드 인쇄 네트워크는 배송 거리를 90% 줄이고 아날로그 설정에서 디지털 워크플로우로 전환하여 지역 생산 규모를 확대할 수 있음을 입증했습니다. 소량 생산(많은 경우 1만 단위 미만)은 기존 오프셋 인쇄의 경쟁력을 저하시켜 다음날 납품 가능한 매장 품질을 실현하는 고속 잉크젯 토너 인쇄기에 투자를 촉진하고 있습니다. 개봉 동영상이 무료 광고가 됨으로써 포장 인쇄 시장은 혜택을 받고 브랜드는 보다 자주 디자인 갱신을 실시하도록 촉구되고 있습니다.

고속 8색 플렉소 인쇄 라인은 최대 294만 달러의 비용이 소요되며 보조 슬리터, 플레이트 마운터, 용제 회수 장치도 필요합니다. 동남아시아의 중소 컨버터는 갱신을 늦추고 브랜드 소유자가 보다 엄격한 공차를 요구하는 가운데 진부화의 위험이 있습니다. 임대 프로그램은 존재하지만 금리는 총 소유 비용을 밀어 올립니다. 이 때문에 자금력 있는 그룹에 의한 가족 경영의 공장 인수가 가속화되고, 규모의 확대와 보다 유리한 기재 계약의 협상이 가능해집니다.

플렉소 인쇄는 2025년 시점에서 포장 인쇄 시장 규모의 34.78%를 차지하고 있어 필름이나 종이 웹에 있어서 비교할 수 없는 고속성을 지지하고 있습니다. 하이브리드 인쇄 플랫폼에서는 현재 플렉소 유닛에 잉크젯 스테이션을 적층함으로써 연속 코드나 지역별 그래픽을 인쇄 공정을 지체시키지 않고 실현하고 있습니다. 디지털 기기는 컨버터가 단기화와 SKU의 다양화를 추구하는 가운데 2031년까지 10.15%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 그라비아 인쇄는 이미지 충실도가 실린더 조각 비용을 정당화하는 고급 담배와 화장품 분야에서 틈새 시장을 유지합니다. 오프셋 인쇄는 접힌 판지에 집중되며 스크린 인쇄 및 기타 틈새 기술은 촉감성 니스와 금속 효과를 지원합니다.

투자 데이터는 이러한 추세를 뒷받침합니다. 2025년에 도입되는 포장 라인에는 예지 보전 센서가 탑재되어 예기치 않은 다운타임을 18% 삭감했습니다. 클라우드 기반 컬러 서버는 공장간에 아트워크를 실시간으로 조정합니다. 하이브리드 모델을 채택한 컨버터 기업에서는 준비 폐기물을 28% 줄이고 프로모션 패키지 시장 투입까지의 시간(TTM)이 반감한 것으로 보고되었습니다. 이러한 상황에 따라 설비 공급업체는 인쇄기와 워크플로우 소프트웨어를 번들로 제공하여 서비스 수익을 확보하고 포장 인쇄 시장에서 애프터마켓 이익률을 강화하고 있습니다.

2025년 현재 솔벤트 시스템은 포장 인쇄 시장에서 39.62% 점유율을 유지했습니다. 그러나 LED 램프가 전력 소비를 1제곱미터당 0.3-0.5kWh로 억제(열풍 건조기의 1.2-1.8kWh에 대해)함으로써 UV 경화 잉크의 출하량은 CAGR 9.52%로 증가하고 있습니다. 수성 잉크는 식품 접촉 규제로 VOC가 제한되는 종이 제품 중심 분야에서 가장 빠르게 성장하고 있습니다. 라텍스 및 LED-UV 기술은 기존에 수은 램프 경화가 불가능했던 수축 라벨과 열 감응 필름에 대응할 수 있습니다.

총 비용 모델에서는 다품종 생산 환경에서 UV가 유리합니다. 판 세정 스테이션이 불필요해져, 용제 재고가 삭감되어, 온 디맨드 경화에 의해 장치품이 감소합니다. 수지의 휘발성은 여전히 리스크이지만, 복수 조달과 사내 배합에 의해 가격 급등을 일부 상쇄할 수 있습니다. 잉크 공급업체는 퇴비화 시험을 통과한 바이오 단량체 및 광개시제에 대한 투자를 추진하고 있으며 화학 기술의 진보를 포장 인쇄 시장에 침투하는 지속가능성 과제와 일치시킵니다.

아시아태평양은 세계 생산량을 선도하고 2024년 신규 인쇄기 도입의 절반 이상을 차지합니다. 중국의 컨버터는 국내 스낵 수요에 대응하기 위해 다층 파우치 라인을 증설. 인도에서는 생산 연동형 인센티브 제도 아래 설비 투자 우대 조치를 실시. 베트남 태국의 연포장 제조업체는 니어 쇼어링의 혜택을 받아 신속한 스윙 태그 폴리 가방을 필요로 하는 의류 수출업체에게 공급합니다. 크로스 보더 투자에 의한 지역 노하우의 향상과 일본 잉크 제조업체와의 합작 사업이 품질 안정성을 높이고 있습니다.

북미 사업자의 기술과 규정 준수에 대한 노력이 잇스빈다. 디지털 골판지 인쇄기에 투자하여 당일 배송용 EC 박스의 생산 능력이 3배로 확대됩니다. 주 의회에서는 재활용 가능한 인쇄물을 평가하는 확대 생산자 책임 제도(EPR) 수수료가 도입되었습니다. 미국 컨버터는 UV-LED 개조를 선도하고 25%의 에너지 절약 효과를 주장하고 있습니다. 캐나다는 식품 접촉 제한을 FDA와 조화시켜 크로스 보더 조달을 용이하게 했습니다. 한편 멕시코는 USMCA 하에서 무관세 액세스를 요구하는 Tier 1 브랜드를 유치했습니다.

유럽은 규제 속도를 설정합니다. 이 지역의 포장재 재활용률 88% 목표는 특수 잉크가 필요한 단일 소재 라미네이트로 브랜드 가이드라인 전환을 촉진하고 있습니다. 독일의 기계 수출은 실시간 점도 제어 등 Industry 4.0 기능을 활용하고 이탈리아 인쇄 기계 제조 업체는 고급 브랜드 획득을 위한 인라인 냉박 가공을 표준 장비하고 있습니다. 동유럽, 특히 폴란드는 서유럽 국가보다 낮은 인건비로 잉여 생산을 흡수하면서 높은 기능 수준을 유지하고 있습니다. 네덜란드의 혁신 보조금은 종이 장벽 포장의 파일럿 라인을 지원하고 포장 인쇄 시장의 기세를 유지합니다.

packaging printing market size in 2026 is estimated at USD 472.5 billion, growing from 2025 value of USD 437.78 billion with 2031 projections showing USD 691.97 billion, growing at 7.93% CAGR over 2026-2031.

Rapid digital transformation, soaring e-commerce activity, and stringent sustainability policies are reshaping technology selection, substrate choice, and regional investment priorities. Flexography keeps its volume edge thanks to productivity on long runs, yet brand owners now favor digital platforms for short batches that support SKU proliferation, variable data, and smart-pack functionality. UV-curable ink chemistry gains ground as converters look for lower energy use and faster throughput, while RFID-enabled packs strengthen supply-chain visibility. At a strategic level, converters combine hybrid press lines, localized micro-factories, and closed-loop material programs to defend margins in a market where brand loyalty depends on print quality, speed, and environmental footprint.

Widespread IoT connectivity is turning each package into a data node, and pressure-sensitive labels embedded with RFID are now common on high-value pharmaceuticals. Digital presses integrate serialized codes without plate changes, cutting unit costs and enabling real-time authentication. Consumer-facing apps read these identifiers to reveal provenance or loyalty offers, deepening engagement while assisting recall management. Converters that combine flexo efficiency with inline inkjet modules meet traceability mandates and win contracts that reward responsiveness.

Direct-to-consumer logistics prioritize lightweight formats that protect goods, showcase graphics, and arrive swiftly. Print-on-demand networks such as Gelato's cut shipping distance by 90%, proving localized production scales once digital workflows replace analog set-up. Shorter run lengths - often below 10,000 units - push traditional offset out of contention, encouraging investment in high-speed inkjet and toner machines that deliver shelf-ready quality overnight. The packaging printing market benefits as every unboxing video becomes free advertising, pushing brands to refresh artwork more often.

A high-speed eight-color flexo line costs up to USD 2.94 million and demands auxiliary slitters, plate mounters, and solvent-recovery units. Smaller converters in Southeast Asia delay upgrades, risking obsolescence as brand owners insist on tighter tolerances. Leasing programs exist, but interest rates elevate the total cost of ownership. Consolidation, therefore, accelerates deep-pocketed groups buying family-run shops to unlock scale and negotiate better substrate contracts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flexography held a 34.78% share of the packaging printing market size in 2025, supported by unrivaled speed on film and paper webs. Hybrid press platforms now layer inkjet stations onto flexo units, enabling serial codes and regional graphics without slowing the run. Digital equipment records a 10.15% CAGR through 2031 as converters chase shorter cycles and SKU proliferation. Rotogravure retains a niche status in premium tobacco and cosmetics, where image fidelity justifies cylinder engraving costs. Offset lithography concentrates on folding cartons, while screen printing and other niche methods address tactile varnishes and metallic effects.

Investment data confirms the trajectory. Pack lines installed in 2025 feature predictive-maintenance sensors that cut unplanned downtime by 18%, and cloud-based color servers align artwork across plants in real time. Converters adopting the hybrid model report making ready waste down by 28% and TTM (time to market) halved for promotional packs. As such, equipment suppliers bundle workflow software with presses, locking in service revenue and strengthening aftermarket margins within the packaging printing market.

Solvent systems maintained a 39.62% share of the packaging printing market size in 2025. Yet UV-curable ink volumes rise at 9.52% CAGR as LED lamps curb power draw to 0.3-0.5 kWh per square meter versus 1.2-1.8 kWh for thermal ovens. Aqueous formulations grow fastest in paper-heavy segments where food contact regulations restrict VOCs. Latex and LED-UV chemistries address shrink labels and heat-sensitive films once off-limits to mercury-lamp curing.

Total-cost models favor UV in high-mix environments: plate washout stations disappear, inventory of solvents shrinks, and cure-on-demand lowers WIP. Resin volatility remains a risk, but multi-sourcing and in-house blending partly offset spikes. Ink suppliers invest in bio-based monomers and photoinitiators that pass compostability tests, aligning chemistry advances with the sustainability agenda permeating the packaging printing market.

The Packaging Printing Market Report is Segmented by Printing Technology (Offset Lithography, Rotogravure, and More), Ink Type (Solvent-Based Ink and More), Packaging Material (Labels, Plastic Containers and Films, Glass Containers, Metal Cans and Foils, and More), End-Use Industry (Food and Beverage, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific leads global output, housing more than half of new press installations in 2024. China's converters add multi-layer pouch lines to feed domestic snack demand, while India offers incentives for capital purchases under its Production-Linked Incentive scheme. Flexible packaging makers in Vietnam and Thailand gain from near-shoring, serving apparel exporters that need rapid swing tags and polybags. Cross-border investments elevate regional know-how, and joint ventures with Japanese ink suppliers improve quality consistency.

North American operators' position on technology and compliance. Investments in digital corrugated presses triple capacity for same-day e-commerce boxes, and state legislatures adopt extended producer responsibility fees that reward recyclable prints. U.S. converters also pioneer UV-LED retrofits, claiming 25% energy savings. Canada harmonizes food-contact limits with the FDA, easing cross-border sourcing, while Mexico attracts Tier-1 brands searching for tariff-free access under USMCA.the

Europe sets the regulatory tempo. The bloc's 88% packaging recycling target nudges brand guidelines toward mono-material laminates that rely on specialized inks. German machinery exports leverage Industrie 4.0 features such as real-time viscosity control, and Italian press builders bundle in-line cold-foil to court luxury houses. Eastern Europe, notably Poland, captures overflow work as labor rates undercut Western peers, yet workforce skills remain high. Innovation grants in the Netherlands fund pilot lines for paper-based barrier packs, sustaining momentum in the packaging printing market.