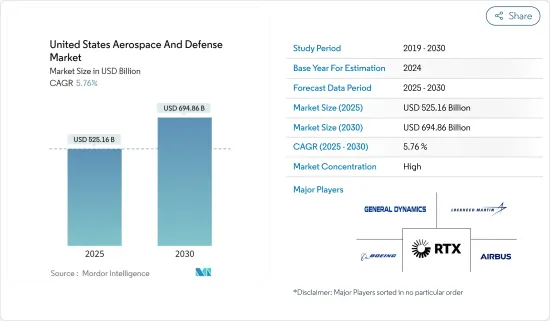

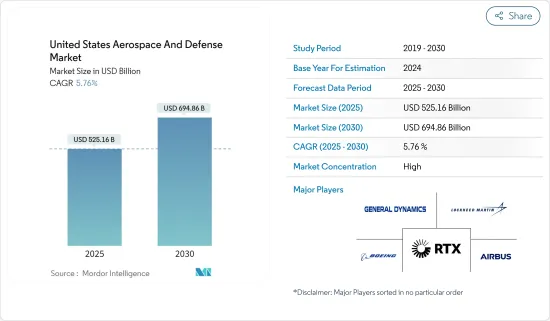

미국의 항공우주 및 방위시장 규모는 2025년 5,251억 6,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 5.76%로 확대되어, 2030년에는 6,948억 6,000만 달러에 달할 것으로 예측됩니다.

미국의 항공우주 및 방위 부문은 인프라와 제조활동 면에서 최대급 규모를 자랑합니다.

미국군은 공군과 해군의 항공기를 여러 개 사용하고 있습니다. 잠재적인 문제를 해결할 준비가되어있어 기존 함대를 업그레이드하고 효율적인 기술을 갖춘 새로운 함대를 구입하기 위한 대규모 투자가 지난 1년동안 확인되었습니다.

항공 및 방위 장비의 개발에 있어서, 3D 프린팅, 인공지능, 빅데이터 분석 등의 첨단 기술의 채용이 진행됨으로써, 향후 몇 년간은 보다 좋은 기회가 생길 것으로 예상됩니다. 그러나, 공급 체인이나 진화하는 사이버 보안 리스크에 관한 문제는 시장의 성장을 방해할 가능성이 있습니다.

우주기능은 미국과 그 동맹국에 국가 의사결정, 군사작전, 국토안전보장에 있어서 전례없는 우위성을 부여하고 있습니다.

미국의 위성제조 및 발사 산업은 급속히 발전하고 있는 산업이며, 미국의 우주개발과 국가안보보장의 대처에 있어 중요한 역할을 하고 있습니다. 새로운 위성 발사 수요는 우주로부터의 저지연 인터넷 액세스의 제공등, 다양한 위성 서비스의 필요성에 의해 초래되고 있습니다. 2022년 4월, Amazon의 자회사인 Kuiper Systems LLC는 2026년까지 1,500기의 위성을 발사하는 승인을 연방통신위원회에서 얻었습니다고 발표했습니다.

미국 우주 사령부는 아마도 미국 국방부(DoD)와 미국의 항공우주 및 방위 산업에 이익을 가져올 것으로 예상됩니다. 따라서 우주 연구 개발에 대한 지출 증가와 위성 발사 증가는 국가 전체 시장 성장을 가속합니다.

미국 공군은 육해군에 항공 지원을 제공하고 전장과 그 주변에 있는 부대를 지원하는 최신 기술을 갖추고 있습니다. 미 공군은 1만 3,247대의 운용기, 예비기, 운용종료기로 구성되어 있습니다.

중동에서의 군사 분쟁에 대한 미국의 참여는 공격기와 수송기 조달을 크게 뒷받침했습니다. 중국의 군사기술의 급속한 진보에 대항해 우위성을 유지하기 위해, 6세대 전투기의 계약을 2024년에 체결할 의향인 것이 발표되었습니다.

공군은 러시아의 위협에 대처하기 위해 여러 조달 계획을 성공시켰습니다. 미 공군의 미래 준비 계획과 함께 중요한 조달 이니셔티브 덕분에 공군 수요는 예측 기간 동안 상당한 성장률을 나타낼 것으로 예상됩니다.

미국의 항공우주 및 방위 시장은 그 특성상 통합되어 있습니다. 시장 주요 기업에는 General Dynamics Corporation, Airbus SE, Lockheed Martin Corporation, The Boeing Company, and RTXCorporation 등이 있습니다. 규제의 변화에 따라 기업은 최종 사용자의 진화하는 요구에 제품 포트폴리오를 맞추어야 합니다.

장기 계약을 획득하고 시장 점유율을 높이기 위해 참가 기업은 정교한 제품의 연구 개발에 많은 투자를 실시하고 있으며, 계속적인 연구 개발에 의해 미국의 항공우주 및 방위 시장의 플랫폼과 관련 제품 솔루션의 기술적 진보가 촉진되고 있습니다.

The United States Aerospace And Defense Market size is estimated at USD 525.16 billion in 2025, and is expected to reach USD 694.86 billion by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The US aerospace and defense sector is one of the largest in terms of infrastructure and manufacturing activities. The market is expected to grow primarily due to the armed forces' procurement and upgrade activities to counter emerging threats. Several contracts from the military, air force, and naval force are currently underway, and many new contracts are anticipated to be dispersed during the forecast period, creating a parallel demand for defense equipment.

The US military uses multiple aircraft across the air force and naval aircraft. Owing to the increasing international conflict with China over its aggression in the South China Sea, the US is gearing up to tackle any potential issues China might create for countries with close ties with the US, like Taiwan and Japan. As a result, significant investments in upgrading the existing fleet and purchasing a new fleet equipped with efficient technologies have been witnessed over the past year.

The growing adoption of advanced technologies such as 3D printing, artificial intelligence, and big data analytics in developing aviation and defense equipment will create better opportunities in the coming years. However, issues related to the supply chain and evolving cybersecurity risks may hinder market growth.

Space capabilities give the US and its allies unprecedented advantages in national decision-making, military operations, and homeland security. While a handful of private companies have driven the most recent space exploration efforts, there are ongoing discussions for establishing the Space Force as the sixth US military branch.

The US satellite manufacturing and launch industry is a rapidly evolving industry that plays a critical role in the country's space exploration and national security efforts. In recent years, this industry has undergone significant changes due to technological advancements, increasing demand for satellite services, and the presence of various prominent players. The demand for new satellite launches is driven by the need for various satellite services, such as providing low-latency internet access from space. In April 2022, Kuiper Systems LLC, a subsidiary of Amazon, announced that it had received approval from the Federal Communications Commission to launch 1,500 satellites by 2026. The company plans to reach 3,236 satellites by 2029, offering broadband internet services worldwide. The company secured around 83 launch services from Blue Origin, Arianespace, and United Launch Alliance (ULA) to launch these satellites.

The US Space Command will likely benefit the US Department of Defense (DoD) and the US aerospace and defense industry. The US Space Command, which oversees space operations using personnel and assets managed by the Space Force, will likely support A&D companies in accelerating investments in innovative technologies and capabilities. Thus, growing spending on space research and development and an increasing number of satellite launches drive market growth across the country.

The US Air Force is equipped with the most modern technology that provides air support for land and naval forces and aids the troops on and around a battlefield. The Air Force continues developing and procuring next-generation aircraft to meet the demands of significant power conflicts with Russia and China. The US Air Force comprises 13,247 operational, reserve, and out-of-service aircraft. The country's diplomatic and military relations with nations such as Japan and Taiwan have compelled it to drive significant investments into increasing the fleet of aircraft to counter any provocative military action from China successfully.

The US involvement in the military conflict in the Middle East majorly drove its procurement of attack aircraft and transport aircraft. The Department of Air Force proposed a budget request of USD 194 billion for FY 2023, an increase of USD 20.2 billion or 11.7% from the FY 2022 budget request. For instance, in May 2023, it was announced that the US Air Force intends to award a contract in 2024 for its sixth-generation fighter jet as it races to retain its edge against rapid advances in Chinese military technology. The country's defense agencies have been on a spree of procurements given the Russia-Ukraine War that drove significant US weapon supply to Ukraine.

The Air Force has successfully implemented several procurement plans to tackle any Russian threat. Owing to significant procurement initiatives, together with the future-ready plans of the USAF, the demand in the Air Force is expected to register a substantial growth rate during the forecast period.

The US aerospace and defense market is consolidated in nature. Some prominent players in the market are General Dynamics Corporation, Airbus SE, Lockheed Martin Corporation, The Boeing Company, and RTX Corporation. With the changing regulations, companies must align their product portfolio to the evolving requirements of end users. The market is also significantly influenced by the dispersion of upgrade contracts to enhance the capabilities of the current fleet of active aerial assets. The active role of the US in the global political front has resulted in the growth of the demand for advanced aircraft, UAVs, and satellites.

In order to gain long-term contracts and enhance market share, players are investing significantly in the R&D of sophisticated product offerings. Furthermore, continuous R&D has fostered technological advancements in platforms and associated products and solutions of the US aerospace and defense market.