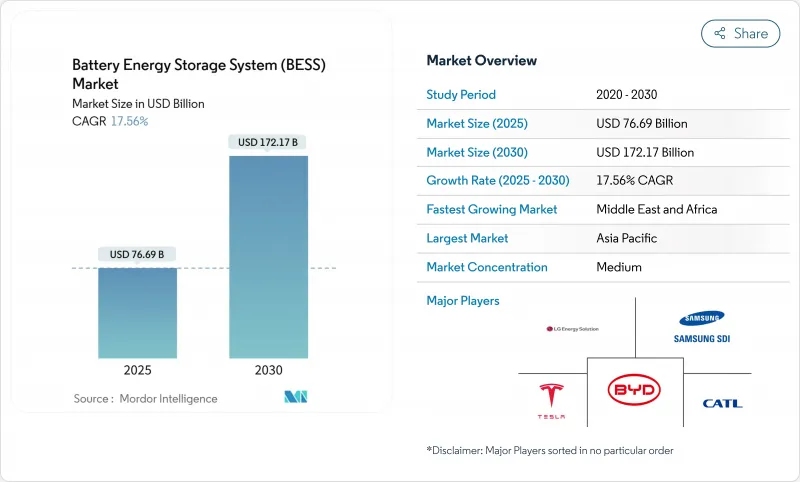

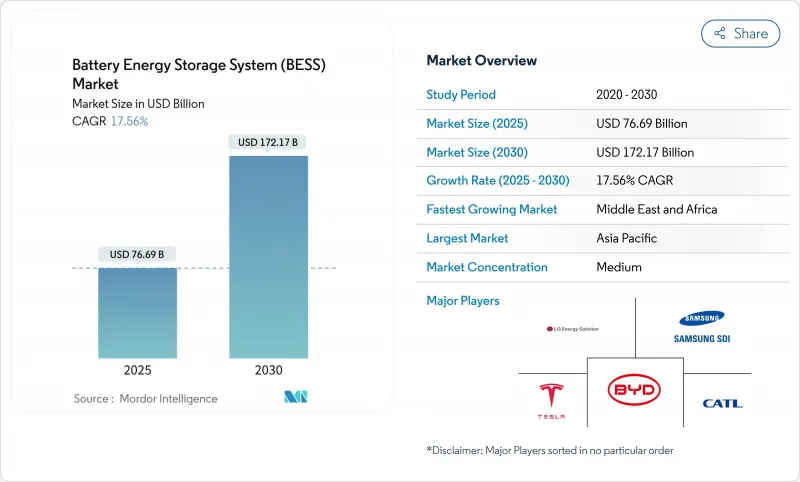

배터리 에너지 저장 시스템(BESS) 시장 규모는 2025년에 766억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 17.56%로, 2030년에는 1,721억 7,000만 달러에 달할 것으로 예상됩니다.

리튬 이온 배터리의 급속한 비용 절감, 지원 조달 의무, 그리드 현대화 지출 증가는 대규모 스토리지를 틈새 신뢰성 도구에서 주류 인프라로 바꾸고 있습니다. 미국의 인플레이션 삭감법이나 EU의 넷·제로 산업법 등의 정책적 추풍이, 몇 기가와트 규모의 프로젝트·파이프라인을 지지하고 있습니다. 한편, 계통형성 인버터 요건은 에너지재정거래 이외의 수익원을 확대하고 있습니다. 동시에 호주와 칠레에서는 태양광발전과 축전지를 결합한 전력구매계약(PPA)의 가격이 동등하게 되어 4시간 배터리가 경쟁력 있는 요금으로 저녁부터 피크까지 안정공급을 제공할 수 있음이 증명되었습니다. 데이터센터의 전력 수요 증가와 정치적 지지를 받은 공급망의 재조달이 이 분야의 기세를 더욱 강화하고 있습니다.

의무화된 조달은 개발 상황을 재구성하고 있습니다. 캘리포니아에서는 2GW, 중국 전력에서는 16GWh, 한국에서는 540MW/3,240MWh를 대상으로 한 장기 모집이 이루어져 개발업체에게 수익과 자금 조달 가능성을 보여주고 있습니다. 유럽에서는 인터넷 제로산업법이 국내 컨텐츠에 인센티브를 주고 중국의 최근 개혁에서는 엄격한 할당 규칙이 철폐되어 시장의 펀더멘탈스가 경제성을 이끌게 되었습니다. 이러한 프로그램은 대출 비용을 낮추고 그리드 서비스 성능 보증을 충족하는 적격 인티 그레이터에 양을 흘립니다.

계통 추종형에서 계통 형성형 아키텍처로 이행함으로써 계통 운용자가 지금까지 동기 발전에서 조달했던 서비스인 합성 관성과 전압 서포트를 배터리가 제공할 수 있게 됩니다. 4.8GW 그리드 형성의 필요성을 보여주는 트랜스그리드 조사와 30만kW의 플루언스 호주 프로젝트는 상업적 실현 가능성을 강조합니다. 유럽의 사업자 TenneT는 2030년까지 520-1270만 kW의 축전을 전망하고 있어 폭넓은 적용 가능성을 강조하고 있습니다. 관성 제품의 추가 수입과 상호 연결 조건의 강화는 프로젝트의 경제성을 개선하고 태양광 및 축전의 하이브리드 개발에 유리하게 작용합니다.

중국은 세계 흑연의 90%를 가공하고 있으며, 인도네시아의 니켈 수출 금지는 국내 정련을 촉구하고 집중 위험을 초래하고 있습니다. 몇 기가와트의 경매가 급증하고 있는 화살촉, 재료 부족이 셀 생산을 위협하고 있습니다. Group14와 같은 신흥기업이 실리콘을 많이 포함하는 애노드를 시험적으로 생산하고 있지만, 상업생산량은 아직 수년 앞입니다. 재활용 프로그램은 1차 수요를 완화시킬 수 있지만 물류상의 장애물이 높기 때문에 고순도 원료를 필요로 하는 유틸리티 스케일 프로젝트에 대한 직접적인 영향은 제한적입니다.

리튬 이온은 2024년에 88.6% 배터리 에너지 저장 시스템(BESS) 시장 점유율을 유지했습니다. 그러나 LFP의 비용과 열안정성의 우위성은 BYD의 40GWh의 2024년 도입으로 대표되는 CAGR 19%를 견인하고 있습니다. NMC Chemistry는 에너지 밀도가 중요시되는 분야에서 계속 중요하며, 바나듐 흐름과 나트륨 이온 기술은 장시간 사용 및 하이사이클 응용 분야에서 틈새 관심을 끌고 있습니다. 리튬 이온 배터리의 에너지 저장 시스템(BESS) 시장 규모는 미세화에 의해 킬로와트 시간당 비용이 낮아짐에 따라 확대될 것으로 예측됩니다. 화학의 다양화는 공급망의 위험을 줄이고 프로젝트 자금 조달을 자산에 특화된 위험 회피 구조로 개방합니다.

실시 전술은 지역에 따라 다릅니다. 중국의 전력 회사는 초저가의 LFP 랙을 제공하고, 유럽의 전력 회사는 한랭지에 대한 내성을 높이기 위해 나트륨 이온을 테스트하고 미국 계통 운영자는 8 시간 서비스를 위해 아연 브롬 플로우 배터리를 시험적으로 도입하고 있습니다. 이 병렬 경로는 화학 선택이 다목적 패러다임이 아니라 듀티 사이클에 최적화되고 있음을 보여줍니다.

온그리드 시스템은 표준화된 상호 연결과 왕성한 상업 수익 기회에 힘입어 2024년 도입의 78%를 차지했습니다. 그러나 오프 그리드 분야는 농촌 지역의 전기와 산업의 탄력성 요건으로 인해 CAGR 18.5%로 가속화되고 있습니다. 파키스탄의 2030년까지의 수입 예측은 8.75GWh로 취약한 국가 인프라를 우회하는 마이크로그리드에 대한 신흥 시장 수요를 상징하고 있습니다.

그리드 모드와 아일랜드 모드 간의 전환 하이브리드 구성은 수요가에게 수요 충전 감소 및 백업 전력을 제공하는 하위 집합으로 증가하고 있습니다. 이러한 유연한 자산은 가상 발전소 어그리게이션을 통해 도매 시장에 참여합니다. 이 동향은 현재 미국의 독립 시스템 운영자 여러 회사의 탈리프 업데이트로 체계화되고 있습니다.

배터리 에너지 저장 시스템(BESS) 시장 보고서는 배터리 유형(리튬 이온, 인산철 리튬 등), 연결 유형(On-grid, 오프 그리드), 구성 요소(배터리 팩 및 랙, 전력 변환 시스템 등), 에너지 용량 범위(100MWh 미만, 기타), 최종 사용자 응용(유틸리티, 주택, 기타), 지역(북미, 유럽)

아시아태평양은 2024년에 50.4%의 점유율을 유지했으며, 중국의 7,000만kW 설치 기준이 매년 두배로 늘고 있습니다. 인도는 SECI의 1GW/2GWh 경매로 전환점을 맞이해, 일본은 167만 kW의 용량 시장 입찰로, 용량 충전에 있어서 스토리지의 역할을 증명했습니다. 한국은 540MW의 입찰을 진행했고 LG에너지 솔루션은 몇 GWh의 시스템을 유럽과 일본에 수출해 이 지역의 제조력을 강조했습니다.

중동 및 아프리카는 CAGR 19.5%로 가장 빠르게 성장하는 지역입니다. 사우디아라비아의 Sungrow와 7.8GW의 파트너십과 이집트의 200MWh AfDB 대출 프로젝트는 대규모 약속을 보여줍니다. 남아프리카의 1GW 상은 축전이 만성 송전망의 불안정성을 어떻게 다루는지를 강조합니다. 또한 아랍에미리트(UAE)은 19GWh를 5.2GW의 태양광 발전소와 통합하여 사막 기후에서 베이스 로드 재생에너지의 선구자가 되었습니다.

북미와 유럽은 계속 절대량이 많습니다. 미국은 1,000억 달러의 투자를 발표하고 있지만, 2,600 GW 프로젝트에 4년간의 상호 연결 대기가 발생하고 있습니다. 유럽의 넷 제로 산업법은 공급망의 지역화를 목표로 하고 있지만, 발표된 기가팩토리의 절반 이상이 자금 조달의 지연에 직면하고 있습니다. 영국 용량 시장, 이탈리아 함대 의무, 캐나다 생산 크레딧 등 지역 정책의 다양성은 정교한 개발자가 재정 거래를 수행하는 수익 모델의 모자이크를 창출합니다.

The Battery Energy Storage System Market size is estimated at USD 76.69 billion in 2025, and is expected to reach USD 172.17 billion by 2030, at a CAGR of 17.56% during the forecast period (2025-2030).

Rapid cost declines in lithium-ion cells, supportive procurement mandates, and rising grid-modernization spending are turning large-scale storage from a niche reliability tool into mainstream infrastructure. Policy tailwinds such as the Inflation Reduction Act in the United States and the Net-Zero Industry Act in the European Union have anchored multi-gigawatt project pipelines, while grid-forming inverter requirements are expanding revenue streams beyond energy arbitrage. Simultaneously, price parity for solar-plus-storage power purchase agreements (PPAs) in Australia and Chile proves that four-hour batteries can offer firm, evening-peak supply at competitive rates. Growing data-center electricity demand and politically driven supply-chain reshoring further reinforce the sector's momentum.

Mandated procurements are reshaping the development landscape. California's long-duration solicitation targets 2 GW, Power China tender seeks 16 GWh, and South Korea awarded 540 MW/3,240 MWh, giving developers visibility on revenue and bankability. In Europe, the Net-Zero Industry Act incentivizes domestic content, while recent Chinese reforms removed rigid allocation rules, letting market fundamentals guide economics. Such programs lower financing costs and channel volume to qualified integrators who meet grid-service performance guarantees.

Moving from grid-following to grid-forming architectures lets batteries deliver synthetic inertia and voltage support, services that grid operators historically procured from synchronous generation. Transgrid's study showing 4.8 GW of grid-forming needs and Fluence's 300 MW Australian project highlight commercial viability. European operator TenneT foresees 5.2-12.7 GW storage by 2030, underscoring broad applicability. Added revenue from inertia products and strengthened interconnection terms improve project economics and favor hybrid solar-storage development.

China processes 90% of global graphite, and Indonesia's nickel export bans push domestic refining, introducing concentration risk. Material shortages threaten cell production just as multi-gigawatt auctions surge. Start-ups such as Group14 are piloting silicon-rich anodes, but commercial volumes remain years away. Recycling programs can ease primary demand, yet logistic hurdles limit immediate impact for utility-scale projects that require high-purity inputs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Lithium-ion maintained 88.6% battery energy storage system market share in 2024. Yet LFP's cost and thermal-stability advantages drive its 19% CAGR, exemplified by BYD's 40 GWh 2024 installations. NMC chemistries remain relevant where energy density matters, while vanadium flow and sodium-ion technologies attract niche interest for long-duration or high-cycle use. Lithium-ion variants' battery energy storage system market size is projected to widen as scaling lowers per-kilowatt-hour costs. Diversification across chemistries reduces supply-chain risk and opens project financing to asset-specific hedging structures.

Implementation tactics vary by region. Chinese players offer ultra-low-priced LFP racks, European utilities test sodium-ion for cold-weather resilience, and U.S. grid operators pilot zinc-bromine flow batteries for eight-hour services. These parallel pathways illustrate how chemistry choice is increasingly optimized for duty cycle rather than a one-size-fits-all paradigm.

On-grid systems captured 78% of 2024 deployments, supported by standardized interconnection and robust merchant revenue opportunities. The off-grid segment, however, is accelerating at 18.5% CAGR owing to rural electrification and industrial resilience requirements. Pakistan's import projection of 8.75 GWh by 2030 typifies emerging-market demand for microgrids that bypass weak national infrastructure.

Hybrid configurations that switch between grid and islanded mode are a rising subset, offering customers demand-charge reduction plus backup power. These flexible assets partake in wholesale markets through virtual-power-plant aggregation, a trend now codified in several U.S. independent system operators' tariff updates.

The Battery Energy Storage System (BESS) Market Report is Segmented Into Battery Type (Lithium-Ion, Lithium Iron Phosphate, and Others), Connection Type (On-Grid and Off-Grid), Components (Battery Pack and Racks, Power Conversion System, and Others), Energy Capacity Range (Below 100 MWh, and Others), End-User Application (Utility, Residential, and Others), and Geography (North America, Europe, Asia-Pacific, and Others).

Asia-Pacific retained a 50.4% share in 2024, powered by China's 70 million kW installed base that doubled yearly. India reached an inflection point with SECI's 1 GW/2 GWh auction, and Japan's 1.67 GW capacity-market awards validated storage's role in capacity adequacy. South Korea advanced a 540 MW tender, and LG Energy Solution exported multi-GWh systems to Europe and Japan, underscoring the region's manufacturing clout.

The Middle East and Africa are the fastest-growing regions at 19.5% CAGR. Saudi Arabia's 7.8 GW partnership with Sungrow and Egypt's 200 MWh AfDB-financed project illustrate large-scale commitments. South Africa's 1 GW awards highlight how storage addresses chronic grid instability. Moreover, the United Arab Emirates integrates 19 GWh with a 5.2 GW solar plant, pioneering baseload renewables in desert climates.

North America and Europe continue to post high absolute volumes. The United States hosts USD 100 billion in announced investments but suffers four-year interconnection queues for 2,600 GW of projects. Europe's Net-Zero Industry Act seeks to localize supply chains, yet over half of announced gigafactories face financing delays. Regional policy diversity-capacity markets in the United Kingdom, fleet mandates in Italy, and production credits in Canada-produces a mosaic of revenue models that sophisticated developers arbitrage.