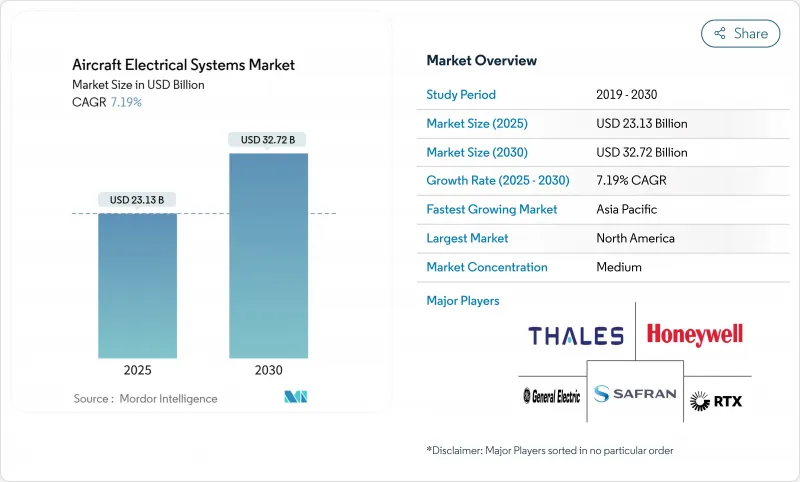

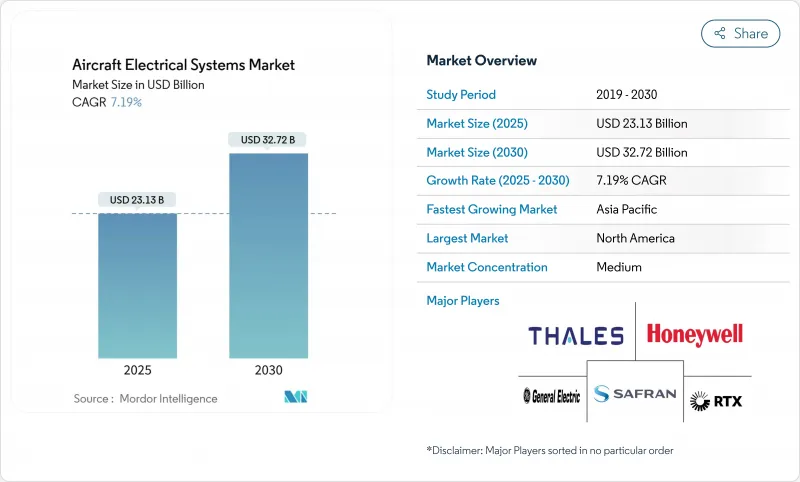

항공기 전기 시스템 시장 규모는 2025년 231억 3,000만 달러, 2030년 327억 2,000만 달러로 확대될 것으로 예상되며 CAGR은 7.19%를 나타낼 전망입니다.

전동화 장비 항공기(MEA) 아키텍처 채택, 단통로 생산량 증가, 객실 가전화를 위한 개조 수요 가속화는 총체적으로 처리할 수 있는 수익 풀을 확대합니다. 고전압 직류(HVDC) 배전, 실리콘 카바이드(SiC) 파워 일렉트로닉스, 모듈식 배터리 팩은 에너지 밀도와 열효율로 경쟁의 축 발을 옮깁니다. 에어버스, 보잉, 기업 프로파일의 지속적인 수주 잔여 및 일부 eVTOL 플랫폼의 초기 생산은 공급망의 제약으로 인해 납기 프로파일이 변화하더라도 기준 수요를 지원합니다. 사이버 보안과 전자파 보호에 대한 병행 투자는 민간 및 방어 프로그램에 걸쳐 확장 가능한 통합 전기 아키텍처에 대한 필요성을 증가시키고 있습니다.

MEA의 도입은 블리드 에어 라인과 유압 펌프를 제거하여 경량화와 유지보수의 합리화를 실현하는 전력 밀도가 높은 전기 대체품으로 대체합니다. B787의 -270V DC 프레임워크는 유압식에 비해 신뢰성이 향상되고 라이프사이클 비용이 절감됨을 입증합니다. 항공사는 연료소비 감소와 라인교환가능한 유닛 고장 감소로 MEA 통합으로 운영비용의 38% 절감을 전망하고 있습니다. F-35의 파워 매니지먼트 모듈은 민간 동향과 동일하며 듀얼 유스의 적용이 가능한 것으로 확인되었습니다. 시스템 수렴과 함께 OEM은 배전 장치에 계층화된 사이버 보호 기능을 통합하여 수동 개입 없이 고장 분리를 보장합니다.

COMAC은 1,000개 이상의 확약 파이프라인을 활용하여 2025년 C919의 생산량을 50대까지 끌어올릴 의향입니다. 에어버스는 A320neo의 출시를 2027년으로 변화했음에도 불구하고, 2025년에 720대 이상의 납품을 목표로 하고 있으며, 전기 인티그레이터에게는 여러 해에 걸친 전망이 확보되고 있습니다. 단통로 제트기가 증설의 대부분을 차지하기 때문에 프레임마다 발전, 변환, 객실 시스템 수요가 증가합니다. 공급업체는 원재료의 가격 변동에 대비하기 위해 인쇄 회로 어셈블리와 하네스를 지역간에 이중으로 조달합니다.

전압의 상승에 의해 도체 표면 온도는 180℃까지 상승하고, EU의 ICOPE 이니셔티브 아래, 어닐 처리된 열분해 흑연 히트 파이프의 채용이 촉진되고 있습니다. EMI 차폐의 요구에 따라 하네스 번들이 대형화되고 설치 시간이 늘어나 기생 질량이 증가하므로 페이로드가 2% 감소할 수 있습니다. 액체 냉각 버스 바는 많은 열 병목 현상을 해결하는 것, 펌프, 냉각수 및 누출 감지 로직을 추가합니다. 공간이 제한된 eVTOL 캐빈은 구조 팀과 전기 팀 간의 학제적 최적화를 강요하기 때문에 패키징과 관련된 심각한 문제에 직면합니다.

에너지 저장 수익은 2030년까지 연평균 복합 성장률(CAGR) 9.21%로 증가할 것으로 예측되며, eVTOL의 항속 거리 목표를 지원하는 모듈식 리튬 이온 팩과 신흥 솔리드 스테이트 옵션이 이를 뒷받침합니다. 에너지 저장 항공기 전기 시스템 시장 규모는 하이브리드 전기 추진의 중심성을 반영하여 예측 기간이 끝날 때까지 64억 달러 이상에 달할 것으로 예상됩니다. 배전은 여전히 기간산업으로 2024년 매출의 36.78%를 차지하며 스마트 컨택터 어레이와 소프트웨어 정의 스위칭 유닛이 이상 동작 시 부하 우선순위를 확보했습니다.

HVDC의 채용은 구성 요소의 로드맵을 재형성하고, 컨버터 설계를 AC115V에서 200kHz의 스위칭 주파수로 동작하는 실리콘 카바이드 스위치를 이용한 멀티 레벨 DC-DC 토폴로지로 변화시키고 있습니다. 사프란 샤프트와 같은 배터리 공급업체는 2025년 60℃의 버스트 방전을 지원하는 1,200V 팩을 발표하여 항공 전자 공학 등급의 고전압 표준의 성숙을 시사했습니다. 장거리 플랫폼은 연료전지의 항속 거리 연장 장치와 배터리 버퍼를 결합한 복합 사이클 아키텍처를 요구하여 통합 전력 관리 제품군의 수명주기 수익을 확대합니다.

배터리 팩과 BMS는 에너지 밀도, 셀 수명, 안전성의 균형을 잡는 역할을 반영하여 CAGR 9.56%를 나타낼 전망입니다. 스마트 BMS 알고리즘은 현재 비행 데크의 어비오닉스와 직접 인터페이스하여 남은 서비스 수명을 방송하고 팩 교체 간격을 예측하여 예정되지 않은 유지보수를 줄입니다. 제너레이터와 스타터 제너레이터는 2024년 항공기 전기 시스템 시장 점유율의 21.19%를 차지하고, 기내 주방의 전기화와 엔벨로프 보호 부하를 지원하기 위해 600-800kW급의 고정격 출력으로의 이행이 계속되었습니다.

DC1,000V, 500A 정격의 커넥터는 터치 세이프 형상이나 아크 억제 스프링을 특징으로 하고, 인정 단계에 들어가고 있습니다. 와이어 하네스공급업체는 전도성을 유지하면서 질량을 30% 줄이기 위해 나노 입자 코팅 알루미늄 코어의 대안을 개발합니다. 임베디드 배전 소프트웨어는 50ms마다 부하 분산 계층을 재계산하는 머신러닝 루틴을 채택하여 아크폴트에 대한 내성을 향상시키고 있습니다.

북미는 미국의 국방 예산과 발전기, 액추에이터, 열 관리 하드웨어에 걸친 풍부한 공급자 기반에 견인되어 2024년 매출의 40.92%를 차지했습니다. 이 지역의 전망은 FAA의 사이버 보안 지침에 의해 강화되고 인증된 데이터 버스가 의무화되어 기존 항공기의 어비오닉스 및 전력 변환 업그레이드에 박차를 가하고 있습니다. 하니웰의 19억 달러의 CAES 인수와 같은 통합 거래는 전자파 보호 포트폴리오를 강화하고 북미를 가장 큰 구매자와 기술 인큐베이터로 만듭니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 7.85%로 가장 빠른 성장을 기록할 전망입니다. COMAC의 C919 생산량이 증가하고 인도에서는 20년간 최대 1,000대의 제트기가 필요할 것으로 예측되어 발전기, 컨버터, 하네스에 대한 수요가 높아집니다. 일본과 한국의 지역 Tier-1은 보잉과 에어버스를 위한 빌드 투 프린트 작업 패키지를 확장하고 지역 컨텐츠를 세계 프로그램에 통합합니다. 싱가포르와 말레이시아 정부 지원을 통한 MRO 회랑은 객실 전화 및 미션 시스템 강화에 중점을 둔 리노베이션 프로그램을 유치하고 있습니다.

유럽은 깨끗한 비행에 대한 자금 지원, 엄격한 배출 정책 및 광범위한 조사 네트워크를 통해 여전히 중요한 위치를 차지하고 있습니다. 사프란은 고전압 배터리와 전기 추진기 분야에서 유럽을 선도하고 있으며, 콜린스 에어로 스페이스의 툴루즈 연구소는 메가와트급 인버터의 검증을 선도하고 있습니다. CS-25/Amdt26에 기반한 EASA의 번개 보호 하모나이제이션은 광대역 테스트를 실시하고 OEM에 실드 강화 솔루션의 인증을 촉구하고 있습니다. 또한, 이 대륙은 히트 파이프 냉각에 종사하는 여러 증명기를 호스팅하여 장거리 하이브리드 차량용 차세대 열 아키텍처를 검증합니다.

The aircraft electrical systems market size is valued at USD 23.13 billion in 2025 and is forecasted to advance to USD 32.72 billion by 2030, translating to a 7.19% CAGR.

Adopting More-Electric Aircraft (MEA) architectures, rising single-aisle production, and accelerating retrofit demand for cabin electrification collectively expand the addressable revenue pool. High-voltage direct current (HVDC) distribution, silicon-carbide (SiC) power electronics, and modular battery packs are pivoting the competitive agenda toward energy density and thermal efficiency. Sustained order backlogs at Airbus, The Boeing Company, and COMAC, and early production runs of several eVTOL platforms anchor baseline demand even as supply-chain constraints shift delivery profiles. Parallel investment in cybersecurity and electromagnetic protection reinforces the need for integrated electrical architectures that can scale across civil and defense programs.

MEA deployment removes bleed-air lines and hydraulic pumps, replacing them with power-dense electrical substitutes that cut weight and streamline maintenance. The +-270 V DC framework on the B787 has demonstrated improved reliability and lower lifecycle cost versus hydraulics. Airlines estimate 38% operating cost savings from MEA integration through lower fuel burn and fewer line-replaceable unit failures. F-35 power management modules echo the civil trend, confirming dual-use applicability. As systems converge, OEMs embed layered cyber-protection into distribution units, ensuring fault isolation without manual intervention.

COMAC intends to raise C919 output to 50 units in 2025, leveraging a pipeline of more than 1,000 firm commitments. Despite shifting its A320neo ramp-up to 2027, Airbus still targets 720-plus deliveries in 2025, locking multiyear visibility for electrical integrators. Since single-aisle jets comprise the bulk of additions, each frame adds incremental demand for power generation, conversion, and cabin systems. Suppliers are dual-sourcing printed-circuit assemblies and harnesses across regions to buffer against raw-material shocks.

Voltage escalation pushes conductor surface temperatures up to 180 °C, prompting the adoption of annealed pyrolytic graphite heat pipes under the EU ICOPE initiative. EMI shielding requirements enlarge harness bundles, increasing installation labor and adding parasitic mass that can subtract 2 % from payload. Liquid-cooled busbars solve many thermal bottlenecks yet introduce extra pumps, coolant, and leak-detection logic. Space-limited eVTOL cabins face acute packaging conflicts, compelling multidisciplinary optimization between structural and electrical teams.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Energy Storage revenue is projected to advance at a 9.21% CAGR to 2030, boosted by modular lithium-ion packs and emerging solid-state options that underpin eVTOL range targets. The aircraft electrical systems market size for Energy Storage is expected to exceed USD 6.4 billion by the end of the forecast window, reflecting its centrality to hybrid-electric propulsion. Power Distribution remains the backbone, controlling 36.78% of 2024 revenue, with smart contactor arrays and software-defined switching units ensuring load prioritization during abnormal operations.

HVDC adoption is reshaping component roadmaps, shifting converter design from 115 V AC to multi-level DC-DC topologies that exploit silicon-carbide switches operating at 200 kHz switching frequencies. Battery suppliers such as Safran-Saft unveiled a 1,200 V pack in 2025 that supports 60C burst discharges, signaling the maturation of avionics-grade high-voltage standards. Long-haul platforms seek combined cycle architectures pairing fuel-cell range extenders with battery buffers, expanding lifecycle revenue for integrated power management suites.

Battery Packs and BMS expand at 9.56% CAGR, reflecting their role in balancing energy density, cell longevity, and safety. Smart BMS algorithms now interface directly with flight-deck avionics, broadcasting remaining useful life and predicting pack swap intervals, thereby reducing unscheduled maintenance. Generators and Starter-Generators, holding 21.19% of the aircraft electrical systems market share in 2024, continue to migrate toward higher power ratings in the 600-800 kW class to support inflight galley electrification and envelope-protection loads.

Connectors rated to 1,000 V DC and 500 A are entering qualification, featuring touch-safe geometries and arc-suppression springs. Wiring harness suppliers develop aluminum-core replacements with nanoparticle coatings to maintain conductivity while trimming mass by 30%. Embedded power-distribution software harnesses machine-learning routines that recalculate load-shed hierarchies every 50 ms, improving resilience against arc-faults.

The Aircraft Electrical Systems Market Report is Segmented by System (Power Generation, Power Distribution, and More), Component (Generators and Starter-Generators, Converters, and More), Platform (Commercial Aviation, Military Aviation, and More), Application (Power Generation Management, Cabin Systems, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 40.92% of 2024 revenue, driven by the United States' defense budget and a deep supplier base that spans generators, actuators, and thermal-management hardware. The regional outlook is reinforced by FAA cybersecurity directives mandating authenticated data buses, which spur avionics and power-conversion upgrades across existing fleets. Consolidation deals such as Honeywell's USD 1.9 billion CAES purchase bolster electromagnetic protection portfolios, making North America the largest buyer and a technology incubator.

Asia-Pacific registers the fastest growth at 7.85% CAGR through 2030. COMAC's C919 production climb and India's forecast requirement for up to 1,000 jets over 20 years anchor demand for generators, converters, and harnesses. Local tier-1s in Japan and South Korea expand build-to-print work packages for Boeing and Airbus, embedding regional content into global programs. Government-backed MRO corridors in Singapore and Malaysia attract retrofit programs focusing on cabin electrification and mission-system enhancements.

Europe remains pivotal owing to Clean Aviation funding, stringent emissions policy, and an expansive research network. Safran leads European efforts in high-voltage batteries and electric propulsors, while Collins Aerospace's Toulouse lab spearheads megawatt-class inverter validation. EASA's lightning-protection harmonization under CS-25/Amdt 26 enforces wide-band testing, compelling OEMs to certify enhanced shielding solutions. The continent also hosts multiple demonstrators tackling heat-pipe cooling, validating next-gen thermal architectures for long-range hybrids.