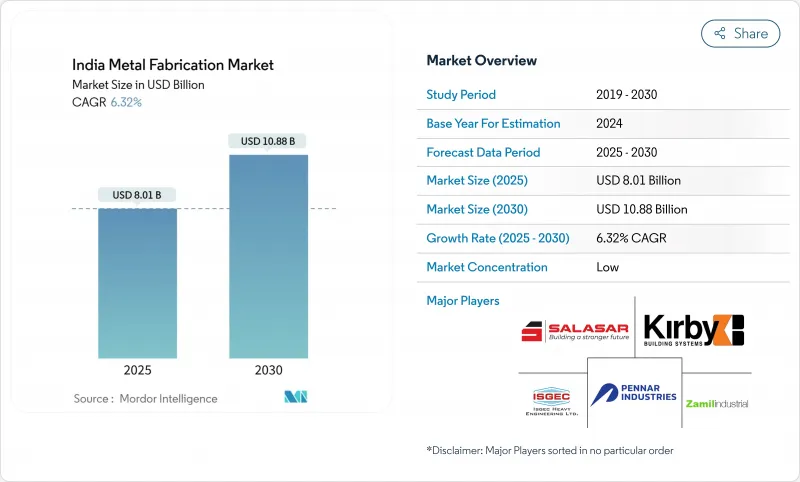

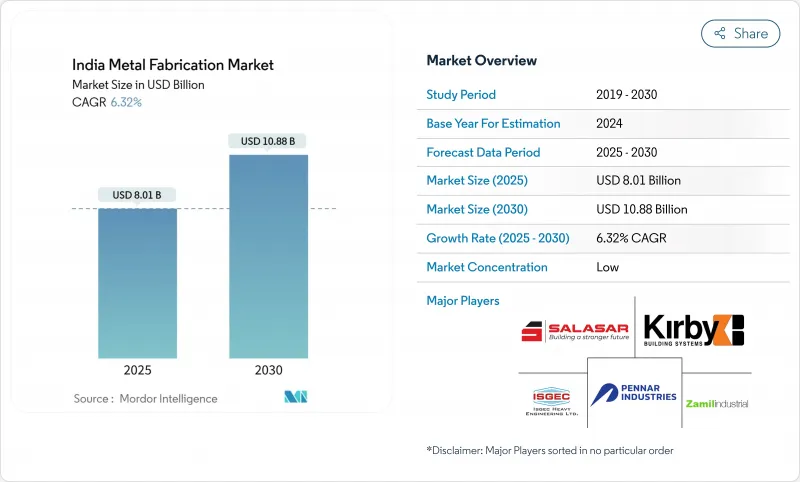

인도의 금속 가공 시장 규모는 2025년에 80억 1,000만 달러, 2030년에는 108억 8,000만 달러에 이르고, CAGR은 6.32%를 나타낼 것으로 예측되고 있습니다.

Gati Shakti 총리 하에서의 대규모 인프라 정비, 국방 오프셋 증가, 신재생 에너지 설비의 규모 확대가 확대를 이끌어 냅니다. 항공우주, 데이터센터, 그린 수소 프로젝트가 보다 가볍고 고정밀 어셈블리를 요구하기 때문에 가공은 여전히 지배적인 서비스이지만, 용접과 알루미늄 가공이 급성장하고 있습니다. 남부의 가공 클러스터는 방어 회랑과 인더스트리 4.0의 채택으로부터 혜택을 받지만, 서부 허브는 여전히 메가 강철과 물류 투자의 대부분을 끌고있습니다. 인도의 금속 가공 시장은 데이터센터 및 조립식 건축을 위한 모듈식 솔루션을 제공하는 반면, 변동성이 뛰어난 원료탄 비용을 헤지하고 엄격한 환경 기준을 준수할 수 있는 종합 기업에게 계속 유리합니다.

국내 태양전지 모듈의 생산 능력은 2026년까지 110GW에 달하며 정밀 가공이 필요한 가대, 트래커, 인버터 하우징의 안정된 파이프라인이 확보됩니다. 2024년 철강 수요는 신재생에너지의 보급을 배경으로 7.7% 증가했습니다. 국가 그린 수소 미션은 그린 수소의 통합에 146억 6,000만 루피(1억 7,663만 달러)를 계상해, 전해조 프레임과 압력 용기의 계약을 개시했습니다. 이미 부품의 70-80%를 현지 조달하고 있는 풍력 터빈 제조업체는 미국에의 수출용으로 타워와 나셀의 가공을 육상에서 실시했습니다. 프로젝트 개발자가 짧은 리드타임과 현지 조달률을 선호하기 때문에 이러한 프로그램을 종합하면 인도의 금속 가공 시장에 수년간의 수량을 공급하게 됩니다.

마스터 플랜은 200개 이상의 프로젝트를 동기화하여 다리 갑판, 역 지붕, 가선 전기 갠트리 등의 필요성을 촉진합니다. 2만 8,602캐롤 루피(34억 5,000만 달러)의 자금이 투입된 12개의 신산업 노드는 물류공원과 유틸리티코리도(유틸리티용 통로)에 걸친 중·경가공 부대수주를 약속하고 있습니다. 제철 능력은 2047년까지 3배의 5억톤으로 증가할 계획으로, 후판의 절단, 압연, 단면 용접 수요가 증가합니다. 델리 뭄바이 간 산업 대동맥의 진전으로 타타 일렉트로닉스와 같은 앵커 테넌트가 이미 확보되어 강하의 가공 계약이 확대되고 있습니다.

원료탄의 수입량은 2025년도 상반기에 2,960만톤과 6년 만의 피크를 기록했고, 공장이 할인을 요구했기 때문에 러시아의 카고는 전년 동기 대비 200%의 급증이 되었습니다. 호주산 점유율은 2022년도의 80%에서 54%로 떨어졌지만 여전히 해저탄에 대한 의존도는 총 수요의 85%를 넘어섰습니다. 정부는 변동성을 억제하기 위해 컨소시엄 스케일 임베디드과 몽골 회랑을 모색하고 있지만, 눈앞의 판가격은 영향을 받기 쉽습니다. 열연 코일 가격이 상승하면 가공업자의 조율이 80-120 베이시스 포인트 떨어지고 EPC 고객에게 비용을 전가하거나 소규모 수주를 연기하지 않을 수 없게 됩니다. 이와 같이 인도의 금속 가공 시장은 일시적인 압력에 직면하고 있지만, 최종 국산 코크스의 개척에 의해 장기적인 이익을 얻고 있습니다.

2024년 인도의 금속 가공 시장 점유율은 기계가공이 33.4%를 차지하며 항공우주, 자동차, 방위 관련 다축 CNC가공공장에서 공급되었습니다. Hurco의 ChatCNC로 대표되는 AI 호환 CAM 소프트웨어의 채택은 프로그래밍 시간을 단축하고, 스핀들 가동률을 향상시키고, 수출 되찾기에 신속하게 대응할 수 있도록 합니다. 자동화 업그레이드는 숙련 노동자의 부족을 완화하고 고가치 어셈블리의 로트 크기 원 생산을 가능하게 합니다.

용접은 고층 인프라, 풍력 타워, LNG 모듈 등에서 비파괴 검사가 끝난 특수한 접합부가 필요하기 때문에 규모가 작은 것으로 CAGR은 가장 빠른 7.01%로 성장을 지속하고 있습니다. 통합된 기업은 로봇 MIG 라인과 실시간 용접 풀 분석을 통합하여 품질 규정과 압축된 프로젝트 일정을 모두 충족합니다. 절단 서비스에서는 25mm의 탄소강을 3m/분으로 슬라이스하는 파이버 레이저 시스템이 위력을 발휘하고, 성형 셀에서는 서보 프레스 브레이크를 사용하여 고도의 고강도 강을 구부립니다. 펀칭, 스탬핑 및 마무리 공정은 환경 기준을 충족하기 위해 인라인 집진기와 수성 페인트 부스로 업그레이드하고 있습니다. SAMARTH Udyog Bharat 4.0 프로그램은 푸네와 벵갈루루 체험센터를 통해 이러한 업그레이드를 지원하고 인도의 금속 가공 시장에서 기술 대응 워크숍에 새로운 주문을 유도합니다.

The India Metal Fabrication Market size stands at USD 8.01 billion in 2025 and is forecast to reach USD 10.88 billion by 2030 while advancing at a 6.32% CAGR.

Expansion is guided by large-scale infrastructure roll-outs under PM Gati Shakti, rising defense offsets, and the scale-up of renewable-energy equipment. Machining remains the dominant service, yet welding and aluminum processing are the fastest climbers as aerospace, data-center, and green-hydrogen projects demand lighter, high-precision assemblies. Southern fabrication clusters benefit from defense corridors and Industry 4.0 adoption, whereas Western hubs still attract the bulk of mega-steel and logistics investments. The India metal fabrication market continues to favor integrated players that can hedge volatile coking coal costs and comply with tightening environmental norms while supplying modular solutions for data centers and pre-engineered buildings.

Domestic solar module capacity is set to hit 110 GW by 2026, ensuring a steady pipeline of mounting structures, trackers, and inverter housings that require precision fabrication. Steel demand increased 7.7% in 2024 on the back of renewable roll-outs. The National Green Hydrogen Mission earmarks INR 14.66 billion(USD 176.63 million) for green hydrogen integration, opening contracts for electrolyzer frames and pressure vessels. Wind turbine manufacturers, who already source 70-80% of components locally, keep tower and nacelle fabrication work onshore for export shipments to the United States. Collectively, these programs channel multi-year volumes to the India metal fabrication market as project developers prioritise short lead times and local content.

The master plan synchronises 200-plus projects, driving the need for bridge decks, station roofs, and overhead electrification gantries. Twelve new industrial nodes, cleared with INR 28,602 crore(USD 3.45 billion), promise ancillary orders for heavy and light fabrications across logistics parks and utility corridors. Steelmaking capacity is planned to triple to 500 million tonnes by 2047, ushering in incremental demand for plate cutting, rolling, and section welding. Progress on the Delhi-Mumbai Industrial Corridor has already secured anchor tenants such as Tata Electronics, broadening downstream fabrication contracts.

Coking-coal imports hit a six-year peak of 29.6 million tonnes in H1 FY25, and Russian cargoes surged 200% year-on-year as mills hunted discounts. Australian share slipped to 54% from 80% in FY 2022, yet reliance on seaborne coal still tops 85% of total demand. The government is exploring consortium-scale buying and Mongolian corridors to tame volatility, but near-term plate prices remain susceptible. Fabricators' gross margins drop by 80-120 basis points when hot-rolled coil prices spike, forcing them to pass costs to EPC clients or defer smaller orders. The India metal fabrication market thus faces temporary pressures yet benefits long-term from eventual domestic coke development.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Machining accounted for 33.4% of India metal fabrication market share in 2024, supplied by a network of multi-axis CNC shops that serve aerospace, automotive, and defense contracts. Adoption of AI-enabled CAM software, typified by Hurco's ChatCNC, cuts programming time and improves spindle utilization, letting shops respond quickly to export call-offs. Automation upgrades soften the skilled-labour deficit and allow lot-size-one production for high-value assemblies.

Welding, although smaller, registers the fastest 7.01% CAGR as high-rise infrastructure, wind towers, and LNG modules need specialized non-destructive-tested joints. Integrated players embed robotic MIG lines and real-time weld-pool analytics to meet both quality codes and compressed project schedules. Cutting services benefit from fiber-laser systems that slice 25 mm carbon steel at 3 m/min, while forming cells use servo-press brakes to bend advanced-high-strength steel. Punching, stamping, and finishing segments upgrade to inline dust-collection and water-borne paint booths to align with environmental norms. The SAMARTH Udyog Bharat 4.0 program backs these upgrades through experiential centres in Pune and Bengaluru, steering fresh orders to tech-ready workshops within the India metal fabrication market.

The India Metal Fabrication Market is Segmented by Service Type (Cutting, and Others), by Material (Carbon Steel, and Others), by End-User Industry (Construction & Infrastructure, and Others), and by Region (Western India, Southern India, Northern India, Eastern India, and Central India). The Market Forecasts are Provided in Terms of Value (USD).