ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

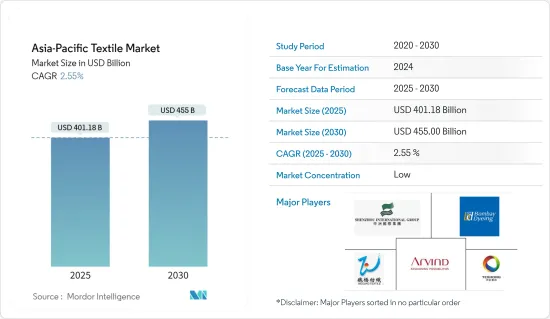

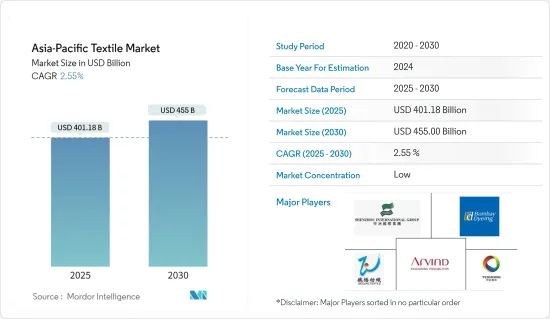

아시아태평양의 섬유 시장 규모는 2025년에 4,011억 8,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 2.55%로 성장할 전망이며, 2030년에는 4,550억 달러에 달할 것으로 예측됩니다.

주요 하이라이트

아시아태평양의 의류와 가정용 가구 수요 증가가 주요 성장 요인입니다.

COVID-19 위기는 세계의 의류 산업에 상당한 손해와 고난을 가져왔으며, 브랜드, 제조업체 및 노동자에게 다양한 영향을 미쳤습니다. 팬데믹은 의류 공급망의 심각한 취약성과 조달 결정이 공급업체 공장과 그 노동자에게 미치는 영향을 드러냈습니다. 세계 의류 생산의 대부분을 차지하는 아시아는 공급망에 파급되는 악영향의 최전선으로 계속 남아 있습니다.

아시아태평양은 가장 크고 가장 급성장하는 실크 시장입니다. 생사의 입수가 용이하기 때문에, 중국이 아시아 태평양의 실크 시장을 리드해, 이 지역의 실크 수요의 약 80%를 차지하고 있습니다. 또, 중국은 세계 최대의 생사 및 견사 생산국이며, 인도, 타이, 우즈베키스탄에 뒤를 잇고 있습니다. 세계 유수의 섬유 수출국으로 세계 섬유 및 의류 수출의 약 40%를 차지합니다. 2만 개 이상의 기업이 있습니다. 아시아 태평양의 경제 성장, 양잠 기술의 급속한 진보, 섬유 산업에서 실크 사용 증가의 결과, 아시아 태평양 실크 시장은 한층 더 확대될 것으로 예상되고 있습니다.

태국은 직물, 스포츠웨어, 유아복, 여성복, 캐주얼웨어의 세계 최대급 생산국으로 세계에 알려져 있습니다. 게다가 정교한 마무리, 염색, 프린트 서비스에 의해, 타이는 세계에서 가장 인기 있는 섬유 아웃소싱처의 하나가 되고 있습니다. 태국은 현재 4,500개의 섬유 및 어패럴 제조업체를 통해 100만 명 가까이를 고용하고 있습니다. 방콕과 태국 동부 주변을 거점으로 하는 이러한 제조업체의 대부분은, 인공 섬유 공장, 방적, 직물로부터 염색, 프린트에 이르기까지, 모든 것을 생산하고 있습니다.

방글라데시 수출 진흥국(EPB)에 따르면 방글라데시 가정용 섬유 제품의 수출 바구니에는 침대 린넨, 침대 시트 및 기타 침실 섬유 제품, 목욕 린넨, 카펫 및 러그, 담요, 주방 린넨, 커튼, 쿠션 및 쿠션 커버, 이불 커버가 포함됩니다. 최근 종료된 2021-2022년 회계연도의 가정용 섬유제품 수출액은 16억 2,000만 달러로 전년 대비 43.28% 증가했습니다. 지난 회계연도의 가정용 섬유 제품의 수출액이 11억 3,000만 달러였던 것은 주목할 만합니다.

세계 의류 생산의 대부분을 차지하는 아시아는 공급망에 파급되는 악영향의 최전선에 있습니다. 과제와 함께, 새로운 제휴나 산업의 장래에 대한 새로운 생각, 한층 더 중요한 것으로서 보다 강인하고 지속가능하며, 인간 중심의 미래를 향해서 어떻게 재구축할 수 있을지를 모색하는 기회의 창이 방문하고 있습니다. 국내 소비자들은 기업들에게 공급망 재고를 촉구하고, 전자상거래와 디지털화는 그 혜택을 받고 있습니다.

아시아의 섬유 시장 동향

아시아의 패션 액세서리에 대한 소비 지출 증가

아시아의 의류와 풋웨어에 대한 소비자 지출은 2024-2028년 총 278억 달러(35.8% 증가)로 지속적으로 증가할 것으로 예측됐습니다. 8년 연속 증가 후 패션 관련 지출은 1,054억 달러에 달하며, 따라서 2028년에는 새로운 정점에 이를 것으로 추정됩니다.

현재 진행중인 노동 시장의 회복도 소비자의 신뢰감, 나아가서는 소비를 뒷받침될 것으로 전망됩니다. 아시아(주로 중국)로부터의 의류품 수요가 증가함에 따라, 이 부문에서의 유럽과 북미의 중요성은 저하하고 있습니다. 북미와 유럽 이외 지역의 의류 매출은 2021년에는 이들 지역의 매출과 맞먹으며 2025년에는 전 세계 의류 매출의 55%에 이를 것으로 예상됩니다.

아시아태평양(베트남, 필리핀, 인도네시아, 말레이시아, 태국, 싱가포르)은 의류 부문에 매우 매력적이며 특히 디지털 솔루션이 중요한 역할을 하고 성장하는 젊은이들의 비율이 많기 때문입니다.

수출 증가가 아시아 수익을 끌어올립니다.

2022년, 세계의 의류 수출국 1위는 중국이었으며, 그 점유율은 약 31.7%, 그 후 EU, 방글라데시, 베트남의 순이었습니다. 이 해, 중국과 EU는 세계 섬유 수출의 선두이기도 했습니다.

많은 아시아 국가들은 의류, 섬유 및 풋웨어(GTF) 제조업을 확립하여 GDP와 세계의 의류 시장에 크게 기여하고 있습니다. 중국의 수출액은 아시아 섬유 수출 시장 전체의 거의 52.2%에 해당합니다.

합리적인 가격으로 쾌적한 의류품에 대한 소비자의 인식이 변화하고 있기 때문에 비스코스, 실크, 대마 등의 고가치 섬유 수요가 높아지고 있습니다. 섬유의 혼방 품종도 또한 인공사와 천연사의 큰 특징에 의해 비약적으로 성장하고 있으며, 그 결과, 향후 수년간에 새로운 시장과 성장 기회가 열릴 것입니다.

폴리에스테르와 면은 이 지역에서 널리 사용되고 있는 섬유사 제품입니다. 소비 패턴의 변화, 인구 증가, 가처분 소득 증가, 아시아태평양에 있어서의 의류나 가정용 가구 수요 증가가 주요 성장 요인입니다.

또, 아시아태평양에서는 홈 텍스타일 수요가 높아지고 있습니다. 홈 텍스타일에는 담요, 침대 시트, 테이블 크로스, 청소용 및 키친용 크로스, 드레이프, 침대 커버, 시어, 벽걸이 카펫, 침낭, 타올켓, 매트리스, 이불, 베개, 태피스트리 등의 제품이 포함되어 가정 , 호텔 , 사무실 등의 인테리어에 이용되고 있습니다.

아시아태평양 섬유 산업 개요

아시아태평양의 섬유 시장은 경쟁이 치열하고 세분화되고 있습니다. 아시아 태평양 섬유산업 기업으로는 Shenzhou International Group, Weiqiao Textile, Texhong Textile Group, Arvind Ltd, Bombay Dyeing and Manufacturing Company Ltd 등이 있습니다. 수많은 토종 기업들은 입지에 제약이 있지만 기술 발전에 따라 인터넷과 전자상거래의 침투가 어려운 시대에도 시장을 견인해 왔습니다. 게다가 합병, 제휴, 인수에 이은 시장의 통합은 기업이 시장에서 견고한 골격을 쌓는 데 도움이 될 것으로 생각됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

분석 방법

조사 단계

제3장 주요 요약

제4장 시장 역학 및 인사이트

현재의 시장 시나리오

시장 역학

성장 촉진요인

고품질 의류에 대한 프리미엄 결제 의욕 증가

천연 섬유 베이스 의류에 대한 지향의 변화

성장 억제요인

공급망 혼란으로 인한 아시아태평양 무역 제한

기회

소셜 미디어 및 전자상거래의 영향력 확대

밸류체인 및 공급망 분석

Porter's Five Forces 분석

신규 참가업체의 위협

구매자 및 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

공급망 및 밸류체인 분석

기술 동향 및 자동화

정부 규제 및 대처

전자상거래 시장 인사이트

COVID-19가 시장에 미치는 영향

제5장 시장 세분화

용도별

의류

공업기술

가정용

기타

재료별

면

황마

실크

합성 섬유

울

지역별

중국

인도

파키스탄

방글라데시

호주

기타 아시아태평양

제6장 경쟁 구도

시장 집중 개요

기업 프로파일

Shenzhou International Group

Weiqiao Textile

Texhong Textile Group

Arvind Ltd

Bombay Dyeing and Manufacturing Company Ltd

Bombay Rayon Fashions Ltd

Fabindia Overseas Pvt Ltd

Raymond Ltd

Vardhman Textiles Ltd

Cotton Corporation Of India*

기타 기업

제7장 시장의 미래

제8장 부록

AJY

영문 목차

영문목차

The Asia-Pacific Textile Market size is estimated at USD 401.18 billion in 2025, and is expected to reach USD 455.00 billion by 2030, at a CAGR of 2.55% during the forecast period (2025-2030).

Key Highlights

Increasing demand for clothing and home furnishing products in the Asia-Pacific region are the major growth factors.

The COVID-19 crisis caused considerable damage and hardship across the global garment industry, affecting brands, manufacturers, and workers in various multitudes. The pandemic has exposed acute vulnerabilities in garment supply chains and the impact that sourcing decisions have on supplier factories and their workers. With the bulk of global garment production in Asia, the region remains the frontline of the adverse effects rippling through the supply chain.

Asia-Pacific is both the largest and fastest-growing silk market. Due to the easy availability of raw silk, China leads the Asia-Pacific silk market, accounting for approximately 80% of the region's demand for silk. China is also the world's largest producer of raw silk and silk yarns, trailing India, Thailand, and Uzbekistan. The country is the world's leading textile exporter, accounting for roughly 40% of global textile and clothing exports. With over 20,000 enterprises. The Asia-Pacific silk market is expected to expand further as a result of the region's growing economy, rapid advances in sericulture technology, and increased use of silk in the textile industry.

Thailand is well-known throughout the world as one of the world's largest producers of fabric, sportswear, children's wear, women's wear, and casualwear. Furthermore, the country's exquisite finishing, dyeing, and printing services make it one of the world's most popular textile outsourcing destinations. Thailand currently employs nearly one million people through its 4,500 textile and apparel manufacturers. Most of these manufacturers, based in and around Bangkok and eastern Thailand, produce everything from man-made fiber plants, spinning and weaving to dyeing and printing.

According to Bangladesh's Export Promotion Bureau (EPB), the country's home textile export basket includes bed linen, bed sheet and other bedroom textiles, bath linen, carpets and rugs, blankets, kitchen linen, curtains, cushions and cushion covers, and quilt covers. Home textiles earned USD 1.62 billion from exports in the recently concluded fiscal year 2021-22, representing year-on-year growth of 43.28%. It is worth noting that home textiles earned USD 1.13 billion in exports in the previous fiscal year.

With Asia accounting for the majority of global garment production, the region remains at the forefront of the negative effects reverberating through the supply chain. With the challenges comes a window of opportunity for new alliances and new thinking about the industry's future and, more importantly, how it can be reshaped for a more resilient, sustainable, and human-centered future. Domestic consumers have prompted businesses to reconsider their supply chains, and e-commerce and digitalization have benefited.

Asia Textile Market Trends

Increase in Consumer Spending in Fashion Accessories in Asia

The total consumer spending on clothing and footwear in Asia was forecast to continuously increase between 2024 and 2028 by a total of 27.8 billion U.S. dollars (+35.8 percent). After the eighth consecutive increasing year, fashion-related spending is estimated to reach 105.4 billion U.S. dollars and, therefore, a new peak in 2028.

The ongoing labor market recovery will also aid consumer confidence and, hence, spending. As demand for clothing from Asia (mainly China) grows, the importance of Europe and North America in this sector is declining. Sales of clothing products outside North America and Europe equaled sales in these regions in 2021, and they are expected to reach 55% of the total world sales of clothing products in 2025.

The Asia-Pacific region (Vietnam, the Philippines, Indonesia, Malaysia, Thailand, and Singapore) is highly attractive to the apparel sector, especially because it has a large proportion of young people for whom digital solutions play an important and growing role.

Increase in Exports Boosting Revenue in Asia

In 2022, China was the top-ranked global clothing exporter, with a share of approximately 31.7 percent, followed by the European Union, Bangladesh, and Vietnam. In that year, China and the European Union were also the leading textile exporters in the world.

Many Asian economies have established garment, textiles, and footwear (GTF) manufacturing industries that contribute considerably to their GDPs and the global apparel market. China's export figures translate to almost 52.2% of the total textile export market in Asia.

The shift in consumer perception of affordable and comfortable clothing increases the demand for high-value fabrics, such as viscose, silk, and hemp. Blended varieties of fibers are also growing exponentially due to significant features of artificial and natural yarn, thus opening up new markets and growth opportunities in the coming years.

Polyester and cotton are widely used textile yarn products in the region. Changing consumption patterns, increasing population, disposable incomes, and the increasing demand for clothing and home furnishing products in the Asia-Pacific region are the major growth factors.

Also, the demand for home textiles is rising in the APAC region. Home textile includes products such as blankets, bedsheets, table cloths, cleaning and kitchen cloths, drapes, bed covers, sheers, wall carpets, sleeping bags, terry towels, mattresses, quilts, pillows, tapestry, etc., which are utilized in the interiors of homes, hotels, offices, etc.

Asia Textile Industry Overview

The Asia-Pacific textile market is highly competitive and fragmented. Some of the companies in the Asia-Pacific Textile industry are Shenzhou International Group, Weiqiao Textile, Texhong Textile Group, Arvind Ltd, and Bombay Dyeing and Manufacturing Company Ltd. Numerous local companies are restricted to their locations, but with technological advancement, Internet and e-commerce penetration has driven the market even in the hard times. Further, integration of the market, followed by mergers, partnerships, and acquisitions, will help the companies to create a strong foothold in the market.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

2.1 Analysis Method

2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

4.1 Current Market Scenario

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising willingness to pay premium for high quality apparel