ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

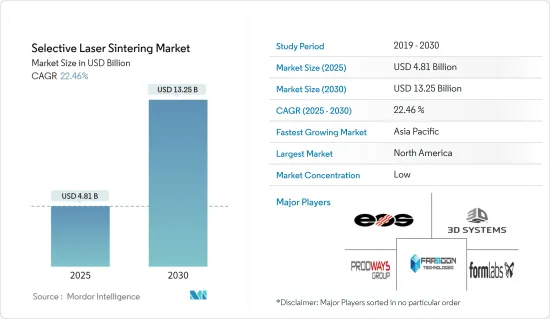

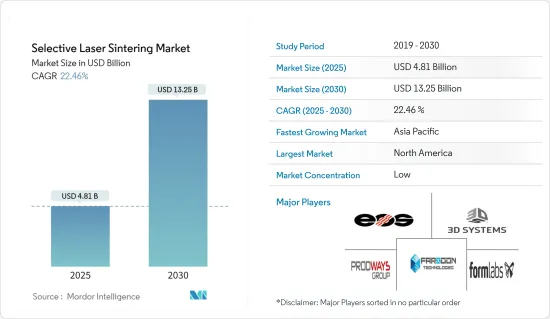

선택적 레이저 소결 시장 규모는 2025년에 48억 1,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 22.46%로, 2030년에는 132억 5,000만 달러에 달할 것으로 예측됩니다.

AM(Additive Manufacturing) 기술 중 하나인 선택적 레이저 소결(SLS)은 고출력 레이저 빔을 분말 재료(보통 나일론 또는 폴리아미드) 베드에 조사하여 원하는 물체의 층을 소결하는 과정입니다. 그 층이 완성된 후, 물체는 새로운 분말 층으로 덮여 있고, 또 다른 층이 소결됩니다.

주요 하이라이트

SLS 장비 시장은 선진국의 R&D 시설의 존재로 인한 수요 증가에 의해 견인될 것으로 예측됩니다. 프로토타입 모델 및 부품 제작을 위한 비금속 분말을 쉽게 구할 수 있으므로 레이저 소결 프린터의 채택이 증가하고 있습니다. 또한 레이저 소결 프린터는 금속 부품을 인쇄할 때 가장 정밀도가 높습니다.

선택적 레이저 소결(SLS)은 인쇄 용도에 사용되는 다른 기술보다 다양한 장점을 가지고 있으므로 가장 선호되는 기술 중 하나로 확인되었으며, 예측 기간 중 견고한 성장이 예상됩니다.

SLS는 스테레오리소그래피에 사용되는 감광성 수지를 대체하기 위해 나일론 분말을 원료로 사용합니다. 전 세계 기업 및 연구기관들이 햇빛에 노출되면 수지가 부서지기 쉬운 문제를 해결하기 위해 이 소재와 기술을 활용하고 있습니다. 또한 SLS는 인쇄 후 전용 지지 구조가 필요하지 않기 때문에 비용 및 재료 친화적임이 입증되었습니다. 또한 SLS는 내구성이 향상되어 기능성 부품 및 시제품과 동등한 성능을 발휘합니다.

SLS는 항공우주, 국방, 자동차 등 다양한 수직 분야에서 폭넓게 활용될 수 있습니다. 우주개발이 패러다임의 변화를 맞이하고 있는 가운데, 인공위성 발사를 준비하는 국가들이 증가하고 있으며, SLS 프린팅에 대한 수요는 더욱 증가할 것으로 예측됩니다.

다양한 항공우주 기업이 효율적인 생산을 촉진하기 위해 이 기술을 채택하고 있습니다. 예를 들어 항공우주 우주 비행 분야에서 NASA와 비상장 회사는 더 적은 부품으로 로켓 엔진(Relativity Space의 경우 전체 로켓)을 제조하기 위해 노력하고 있습니다. 이것은 3D 프린팅의 중요한 능력이며, 제조 시간과 비용을 절감하는 방법입니다. 선택적 레이저 소결 및 금속 분말(예 : 고온에 견딜 수있는 인코넬 구리 초합금 파워)의 배치 및 용융을 사용하여 부품은 층별로 구성됩니다. 예를 들어 여러 부품을 단 며칠 만에 하나의 통합 부품으로 인쇄 할 수 있습니다. 테스트 중에 로켓이 실패한 경우, 3D 모델링 소프트웨어를 수정하여 새로운 로켓을 만들고 다른 테스트를 신속하게 설정할 수 있습니다.

또한 2021년 12월, 적층제조 부품 제조업체인 Primaeam Solutions Pvt Ltd는 인도 첸나이에 새로운 적층제조 고객 경험 센터, 헬스케어 혁신 및 인큐베이션 센터를 오픈했습니다. 이 1만 평방피트 규모의 센터는 전자빔 용융(EBM), 선택적 레이저 소결(SLM), 용융 증착 모델링(FDM), 스테레오리소그래피(SLA), 멀티젯 융합(MJF), 섬유 강화 연속 필라멘트 제조(CFF) 등의 기술을 활용하여 적층제조 서비스 뷰로의 유력한 기업으로 자리매김하고 있습니다.

COVID-19 팬데믹은 전 세계 중소기업과 대기업에 경제적 혼란을 가져왔습니다. 제조업의 대부분은 생산성을 높이기 위해 사람들이 밀접하게 접촉하는 공장 현장에서의 작업을 포함하기 때문입니다.

선택적 레이저 소결(SLS) 시장 동향

항공우주 및 방위산업이 큰 시장 점유율을 차지할 것으로 예상

항공우주 산업은 현 세대 기술의 대부분을 조기에 채택하고 있습니다. 항공기 제조업체와 엔진 제조업체 모두 효율성을 높이기 위해 경량 부품을 개발하기 위해 3D 프린팅 기술에 의존하고 있습니다.

3D 프린팅은 미 항공우주국(NASA)이 수십년간 프로토타이핑과 기능 부품 제작, 그리고 최근에는 달과 화성의 건설 시스템 구축 목적으로 사용해왔습니다.

벨 텍스트론은 적층제조를 실험한 최초의 항공우주 기업 중 하나이며, SLS의 첫 번째 용도는 금형 및 실험 부품의 신속한 프로토타입 제작이었습니다. 그러나 적층제조 산업이 발전함에 따라 회사는 적층제조 산업이 성숙해야 할 필요성을 깨달았습니다. 적층제조을 시작한 이래 벨 텍스트론은 SLS만으로 제품에 광범위하게 흩어져 있는 550개 이상의 부품을 생산했습니다. 생산된 부품의 대부분은 실험용이지만, 550개 부품 중 200개 이상이 생산 목적의 부품이라는 점은 주목할 만합니다.

또한 GKN Aerospace는 2022년 7월 영국에 위치한 세계 기술 센터에 RenAM 500 Flex를 도입하여 금속 적층제조기 라인업을 확장했으며, RenAM 500Q Flex는 4레이저 적층제조기로 항공우주 분야의 적층제조을 최적화할 것으로 기대됩니다. 기대되고 있습니다.

또한 미국 인구조사국에 따르면 미국의 항공우주 제품 및 부품 제조 매출은 2024년까지 약 2,644억 달러에 달할 것으로 예측됩니다. 또한 캐나다의 항공우주 제품 및 부품 제조 매출은 2024년까지 약 193억 달러에 달할 것으로 예측됩니다. 이러한 발전은 시장 성장을 적극적으로 촉진할 것으로 보입니다.

스톡홀름 국제평화연구소(SIPRI)에 따르면 미국은 2021년 군비 지출이 가장 많은 국가 순위에서 1위를 차지했으며, 군비는 8,010억 달러로 전 세계 군비 2조 1,000억 달러의 38%를 차지했습니다.

북미가 주요 시장 점유율을 차지할 것으로 예상

북미에는 적층제조를 개발, 채택, 투자하는 많은 기업이 있습니다. 이 지역에서는 프로토타이핑에 대한 수요가 증가하고 있으며, 이는 이 지역 시장을 크게 견인하고 있습니다. 또한 북미의 SLS 수요는 다양한 산업 분야에서 R&D 및 테스트에 대한 관심이 증가하고 있는 것이 주요 요인으로 작용하고 있습니다.

캐나다 통계청에 따르면 캐나다 기업은 2021년에 219억 달러, 2022년에는 224억 달러를 사내 산업 연구개발에 투자할 것으로 예측됩니다. 이러한 연구개발의 성장은 북미 선택적 레이저 소결 시장을 촉진할 것으로 예측됩니다.

이 지역의 기업은 더 넓은 고객층에 솔루션을 제공하기 위해 전략적 제휴를 맺고 있습니다. 예를 들어 2022년 5월 미국의 Essentium Inc는 블루 레이저 솔루션 프로바이더인 Nuburu와 제휴하여 블루 레이저 기반 금속 적층제조 플랫폼을 개발했습니다.

그 결과, 제조업체는 고해상도 및 고속 처리량으로 생산 등급의 금속 부품을 생산할 수 있을 것으로 기대됩니다. 또한 이번 계약의 일환으로 Nubble은 적층제조 응용 특허에 대한 라이선스를 부여합니다.

3D 프린팅과 같은 신기술의 이용이 증가하고 있는 것도 이 지역의 SLS 시장을 촉진할 것으로 예측됩니다. 예를 들어 세계경제포럼(WEF)에 따르면 2022년까지 미국 조사 대상 기업의 47%가 3D 프린팅 기술을 사용할 것으로 예측됩니다.

선택적 레이저 소결(SLS) 산업 개요

선택적 레이저 소결 시장은 전 세계에서 사업을 전개하고 있는 기존 기업과 통합된 시장 공간에서 주목을 받기 위해 경쟁하는 소수의 지역 기업으로 구성되어 있으며, 3D Systems Inc. Fathom Manufacturing 등 이 분야에 풍부한 전문성을 가진 기업이 다수 존재함에 따라 경쟁 기업 간의 적대적 관계는 더욱 심화될 것으로 예측됩니다.

2022년 6월 - 3D Systems와 EMS GRILTECH가 적층제조 재료 개발을 강화하기 위한 전략적 제휴를 발표했습니다. 양사는 상업용 선택적 레이저 소결(SLS) 프린터에서 사용하도록 설계된 새로운 나일론 공중합체 듀라폼 PAx Natural을 출시할 예정입니다.

2021년 11월 - Evonik Industries AG는 개인 맞춤형 이식형 의료기기의 3D 프린팅을 가능하게 하는 RESOMER PrintPowder 폴리머를 보다 폭넓게 제공한다고 발표했습니다. 이 새로운 파우더는 선택적 레이저 소결법(SLS)을 통한 3D 프린팅을 위해 전 세계에서 사용할 수 있습니다. 이 새로운 파우더는 다양한 맞춤형 기계적 특성과 열화 속도 범위로 인해 다양한 정형외과, 치과, 연조직 용도 등 보다 복잡한 맞춤형 의료기기에 사용할 수 있습니다.

2021년 2월 - 3D Systems는 사우스캐롤라이나주 록힐에 100,000평방피트를 추가하여 기존 본사 캠퍼스에 100,000평방피트를 추가하는 확장 계획을 발표했습니다. 이번 확장을 통해 재료 제조, 품질 및 물류 업무를 통합하고 재료 개발 연구소를 신설 및 확장하여 업무 효율성을 높이고 솔루션 개발 속도를 높이며 시장 출시 기간을 단축할 계획입니다.

기타 특전:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 개요

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

바이어의 교섭력

신규 진출업체의 위협

대체품의 위협

경쟁 기업 간 경쟁 강도

시장에 대한 COVID-19의 영향 평가

3D 프린팅 기술의 분석(FDM, SLA, SLS;재료와 기술에 관한 정성 분석;벤치탑 산업용 SLS와 기존 산업용 SLS 프린터의 비교)

제5장 시장 역학

시장 성장 촉진요인

최종 제품이 시장에 도달할 때까지의 시간 단축

각 지역에서 정부 구상의 강화

시장이 해결해야 할 과제

추가 자본 지출과 대량생산에서의 제약

제6장 시장 세분화

소재별

금속

플라스틱

부품별

하드웨어

소프트웨어

서비스

최종사용자 산업별

자동차

항공우주·방위

헬스케어

일렉트로닉스

기타 최종사용자 산업

지역별

북미

유럽

아시아태평양

세계의 기타 지역

제7장 경쟁 구도

기업 개요

3D Systems Inc.

EOS GmbH Electro Optical Systems

Farsoon Technologies

Prodways Group

Formlabs Inc.

Ricoh Company Ltd

Concept Laser GmbH(General Electric)

Renishaw PLC

Sinterit Sp. Zoo

Sintratec AG

Sharebot SRL

Red Rock SLS

제8장 투자 분석

제9장 시장의 미래

KSA

영문 목차

영문목차

The Selective Laser Sintering Market size is estimated at USD 4.81 billion in 2025, and is expected to reach USD 13.25 billion by 2030, at a CAGR of 22.46% during the forecast period (2025-2030).

Selective Laser Sintering (SLS), an additive manufacturing (AM) technique, is a process in which a high-powered laser beam is aimed into powdered material (typically nylon or polyamide) bed to sinter a layer of the desired object. Following the completion of that layer, the object is covered with a new layer of powder, and another layer is sintered.

Key Highlights

The market for SLS equipment is anticipated to be driven by the rising demand from developed countries, owing to the presence of research and development facilities in the countries. The adoption of laser sintering printers has increased due to the ease of availability of non-metal powders to create prototype models and parts. Also, laser sintering printers are the most precise when printing metal parts.

Selective Laser Sintering (SLS) has been identified as one of the most-preferred technology and is expected to witness robust growth during the forecast period, owing to its various benefits over other technologies used for printing applications.

SLS utilizes nylon powder as raw material as a substitute for the photosensitive resin used in Stereolithography. Companies and research organizations across the globe have been identified to take advantage of this material and technology to tackle concerns, such as the brittle nature of the resin when exposed to sunlight. In addition, SLS has also been proven to be cost and material friendly, as it does not require any dedicated support structure post-printing. In addition, SLS provides enhanced durability and can perform as well as either functional parts or prototypes.

SLS further finds a wide array of applications across various verticals, such as aerospace, defense, and automotive, among others. With space exploration witnessing a paradigm shift, the demand for SLS printing is expected to mount, with an increasing number of countries gearing up to launch satellites.

Various aerospace companies are adopting the technology to foster efficient production. For instance, in the space flight branch of aerospace, NASA and private companies are working to build rocket engines (and even entire rockets in the case of Relativity Space) with fewer parts, which is a crucial capability of 3D printing and a way to reduce production time and costs. Using selective laser sintering and the laying down and melting of metal powder (for example, Inconel copper super alloy power that can withstand high temperatures), parts are built up layer by layer. The SLS technique offers several benefits, like multiple parts can be printed as one unified part in just days; the rocket's weight can be reduced with fewer nuts, bolts, and welds. If the rocket proves faulty during a test, changes can be made to the 3D modeling software for a new rocket, and another test can be quickly set up.

Further, in December 2021, Primaeam Solutions Pvt Ltd, an additive parts manufacturing company, inaugurated its new Additive Manufacturing Customer Experience Centre, Innovation & Incubation Centre for Healthcare, in Chennai, India. The 10,000 sq. ft. center would allow the company to develop its position as a prominent player in the additive manufacturing service bureau with technologies such as Electron Beam Melting (EBM), Selective Laser Sintering (SLM), Fused Deposition Modelling (FDM), Stereolithography (SLA), Multi Jet Fusion (MJF), and Continuous Filament Fabrication with Fiber reinforcement (CFF).

The COVID-19 pandemic outbreak has created economic turmoil for small, medium, and large-scale industries worldwide. Adding to the woes, country-wise lockdown inflicted by the governments across the globe (to minimize the spread of the virus) has further resulted in industries taking a hit and disruption in supply chain and manufacturing operations across the world, as a large part of manufacturing includes work on the factory floor, where people are in close contact as they collaborate to boost the productivity.

Selective Laser Sintering (SLS) Market Trends

Aerospace and Defense Industry is Expected to Hold Significant Market Share

The aerospace industry has an early rate of adoption of most of the technologies in the current generation. Both aircraft and engine manufacturers have been relying on 3D printing technology in order to develop lightweight parts to gain efficiency.

3D printing has been used by the National Aeronautics and Space Administration (NASA) for decades for the purposes of prototyping and creating functional parts and, most recently, for building construction systems for the Moon and Mars.

Bell Textron Inc. was one of the first aerospace companies to experiment with additive manufacturing. The first use of SLS was for quick prototypes of tooling and experimental parts. However, as the additive manufacturing industry progressed, the company understood the need to allow the additive manufacturing industry to mature. Since the start of additive efforts, Bell Textron has produced over 550 parts widely spread among its products with just SLS. While a majority of parts produced are experimental, it is to be noted that over 200 of those 550 parts are for production purposes.

Moreover, in July 2022, GKN Aerospace expanded its range of metal additive manufacturing machines at the company's global technology center in the United Kingdom by installing RenAM 500 Flex. The RenAM 500Q Flex is a four-laser Additive Manufacturing machine that is expected to optimize Additive Manufacturing for aerospace applications.

Furthermore, according to the US Census Bureau, it is expected that the revenue of aerospace products and parts manufacturing in the United States will amount to about USD 264.4 billion by 2024. Moreover, It is likely that the revenue of aerospace products and parts manufacturing in Canada will amount to approximately USD 19.3 billion by 2024. Such developments would drive the market's growth positively.

According to Stockholm International Peace Research Institute (SIPRI), the United States led the ranking of countries with maximum military spending in 2021, with 801 USD billion dedicated to the military, which was 38 percent of the global military expenditure of USD 2.1 trillion.

North America is Expected to Hold Major Market Share

North America is home to many companies developing, adopting, or investing in additive manufacturing. There has been a growth in the demand for prototyping in the region which has been majorly driving the market in the region. Further, the demand for SLS in North America is driven by a higher focus on research and development and increased testing in various industries.

According to Statistics Canada, Canadian businesses intend to spend USD 21.9 billion on in-house industrial research and development in 2021, while USD 22.4 billion is expected to be spent in 2022. Such growth in research and development is expected to push the market for Selective Laser Sintering in North America.

Companies in the region are doing strategic collaborations to provide their solutions to a broader customer base. For instance, in May 2022, Essentium Inc, a US-based company, partnered with Nuburu, a blue laser solution provider, to develop a blue laser-based metal Additive Manufacturing platform.

The resulting machine is hoped to enable manufacturers to create production-grade metal parts with high resolution and fast throughput. Further, as a part of the contract, Nuburu will license its additive manufacturing application patents.

The increase in the usage of new technologies, such as 3D printing, is also expected to drive the market of SLS in the region. For instance, according to World Economic Forum, it is expected that by 2022, 47% of the surveyed companies in the United States will use 3D printing technology.

Selective Laser Sintering (SLS) Industry Overview

The Selective Laser Sintering Market majorly comprises incumbents operating globally, along with a few regional players vying for attention in a consolidated market space. The presence of several players, such as 3D Systems Inc., EOS GmbH Electro Optical Systems, Ricoh Company Ltd., and Fathom Manufacturing, among others with considerable expertise in the field, is expected to intensify the competitive rivalry further.

June 2022 - 3D Systems and EMS GRILTECH announced the strategic partnership to enhance additive manufacturing materials development. Both companies will introduce a novel nylon copolymer - DuraForm PAx Natural- designed to be used with any commercially-available selective laser sintering (SLS) printer.

November 2021 - Evonik Industries AG announced that it offers a broader range of RESOMER PrintPowder polymers to enable the 3D printing of personalized implantable medical devices. The new powders are available globally for 3D printing through selective laser sintering (SLS). Due to a broader range of customizable mechanical properties and degradation rates, the new powders could be used for more complex and tailored medical devices, including diverse orthopedic, dental, or soft tissue applications.

February 2021 - 3D Systems announced the expansion plan of its Rock Hill, South Carolina, location, adding 100,000 square feet to its existing headquarters campus. This expansion will enable the company to consolidate its materials manufacturing, quality, and logistics operations, with new and expanded materials development laboratories to improve operational efficiencies, accelerate solution development, and reduce time to market.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porters Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of Impact of COVID-19 on the Market

4.4 Analysis of 3D Printing Technologies (FDM, SLA, SLS; Qualitative Analysis on Materials and Technologies; Benchtop Industrial SLS Vs Traditional Industrial SLS Printers)

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Reduced Time for the End Product to Reach the Market

5.1.2 Increased Government Initiatives Across Various Regions

5.2 Market Challenges

5.2.1 Additional Capital Expenditure and Restrictions in Mass Production