인도의 에폭시 수지 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

India Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1687776

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

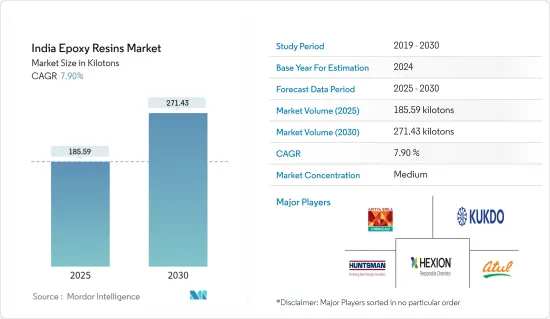

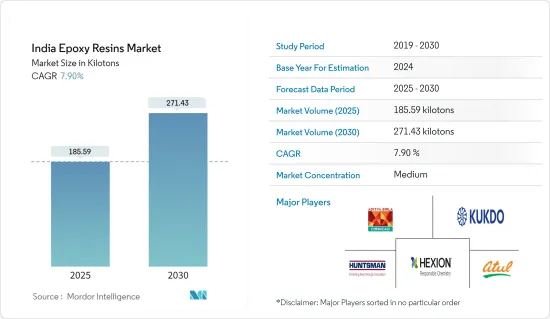

인도의 에폭시 수지 시장 규모는 2025년에 185.59킬로톤으로 추정되고, 예측 기간인 2025-2030년 CAGR 7.9%로 성장할 전망이며, 2030년에는 271.43킬로톤에 달할 것으로 예측됩니다.

COVID-19에 의한 팬데믹기에는 전국적인 봉쇄, 엄격한 사회적 거리두기 의무화, 공급망의 혼란으로 인해 시장은 큰 영향을 받았습니다. 이 때문에 에폭시 수지를 필요로 하는 페인트 및 코팅제, 접착제, 실링제 등의 다양한 제품의 생산과 제조가 일시적으로 정지되었습니다. 그러나 팬데믹 이후 다양한 제조업에 대한 정부의 지원으로 시장의 성장은 가속화되고 있습니다.

주요 하이라이트

건설 산업의 성장 및 자동차 산업으로부터의 접착제 및 실란트 수요 증가가 시장 성장의 요인입니다.

반면, 에폭시 수지의 유해성이 시장 성장에 방해가 될 것으로 예상됩니다.

재활용 가능하고 개질 가능한 에폭시 수지의 채용이 증가하고 있는 것은 예측 기간에 있어서 시장의 호기가 될 전망입니다.

인도의 에폭시 수지 시장 동향

DGBEA(비스페놀 F와 ECH) 수요 증가

비스페놀 A-에피클로로히드린을 기본으로 하는 에폭시 수지는 여전히 가장 널리 사용되고 있는 에폭시 수지입니다. 에폭시 수지는 활성 수소기를 포함하는 화합물을 에피클로로히드린과 반응시켜, 그 다음에 디하이드로할로겐화함으로써 조제됩니다.

비스페놀 A의 디글리시딜 에테르(DGEBA)를 기본으로 하는 에폭시 수지는 접착제, 코팅제, 적층판, 밀봉제 등의 배합에 가장 일반적으로 사용되고 있습니다.

현재, 세계의 에폭시 수지 재료의 약 90%가 비스페놀 A의 디글리시딜에테르(DGEBA)로부터 만들어지고 있습니다. 이 수지는 뛰어난 기계적 특성, 내약품성, 형상 안정성 등의 독특한 특징을 갖추고 있습니다.

폴리카보네이트 및 에폭시 수지는 BPF에서 파생한 주요 제품입니다. 이 에폭시 수지는 DGEBA와 같은 방법으로 제조됩니다. DGEBF(비스페놀F) 에폭시 수지는 DGEBA 에폭시 수지보다 점도가 낮고 기계적, 화학적 특성이 우수합니다.

비스페놀 F형 에폭시 수지는 코팅, 토목, 접착제, 전기 절연 재료, 반응 중간체 등 폭넓은 용도에 사용되고 있습니다. 특히 액상 수지는 점도가 낮기 때문에 작업성이나 성형성이 뛰어나 많은 용도에 적합합니다.

시장을 독점하는 페인트 및 코팅제 부문

인도의 에폭시 수지 업계에서는 건축, 자동차, 에너지, 전자 산업에서 널리 사용되고 있기 때문에 페인트 및 코팅 분야가 가장 급성장할 것으로 예상되고 있습니다.

에폭시 수지는 바닥이나 금속 용도의 코팅의 내구성을 높이기 위해, 코팅 용도의 바인더로서 사용됩니다.

인도는 제조업 및 기계 산업이 급성장하고 있는 국가 중 하나이며, 페인트 및 코팅제의 요구가 높아지고 있습니다. 정부는 국내에 제조 부문을 설치하는 기업에 대해 다양한 편의를 도모하고 제조 부문을 뒷받침하기 위해 다양한 정책을 내놓고 있습니다. 예를 들어, 인도는 2021년 8월에 제조품 수출액 1조 달러라는 목표를 달성하기 위한 계획의 개요를 발표했습니다.

인도의 페인트 산업의 매출은 약 67억 833만 달러로 추정되고 있습니다. 국내 최대 기업인 Asian Paints는 국내에서 10개의 생산시설을 운영하고, Berger paints는 12개의 생산시설을 사용하고 있습니다.

OICA에 의하면, 2021년의 자동차 생산 대수는 약 4,399만 1,112대로 평가되었으며, 2020년의 3,381만 1,819대에 비해 30% 증가했습니다.

승용차(BMW, 메르세데스, 타타 모터스, 볼보 오토를 제외한다), 삼륜차, 이륜차, 사륜차의 자동차 생산 대수는 2021년 10월까지 221만 4,745대가 되었습니다.

IBEF에 따르면 인도 정부는 자동차 부문이 국내외 투자로 2023년까지 80억-100억 달러를 창출한 것으로 평가되었습니다.

이러한 요인에 의해 페인트 및 코팅에 있어서 에폭시 수지 수요가 촉진되어, 예측 기간중 시장의 성장이 높아질 것으로 예상됩니다.

인도의 에폭시 수지 산업 개요

인도의 에폭시 수지 시장은 부분적으로 단편화되어 있으며, 시장에는 다양한 기업이 존재하고 있습니다. 인도의 에폭시 수지 시장에서 주요 기업으로는, Aditya Birla Chemicals, Atul Ltd., KUKDO CHEMICAL, Hexion, Huntsman International LLC등이 있습니다.(순부동)

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건설 업계의 강력한 성장

자동차 산업에서 접착제 및 실란트 수요 증가

성장 억제요인

에폭시 수지의 위험한 영향

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

원재료별

DGBEA(비스페놀 A와 ECH)

DGBEF(비스페놀 F와 ECH)

노볼락(포름알데히드와 페놀류)

지방족(지방족 알코올)

글리시딜아민(방향족 아민 및 ECH)

기타 원재료

용도별

도료 및 코팅제

접착제 및 실란트

복합재료

전기 및 전자

기타 용도

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일(개요, 재무, 제품 및 서비스, 최근 동향)

3M

Aditya Birla Chemicals

Atul Ltd

BASF SE

Daicel Corporation

DuPont

KUKDO CHEMICAL CO., LTD.

Huntsman International LLC

MACRO POLYMERS Pvt Ltd

NAN YA PLASTICS CORPORATION

Olin Corporation

Westlake Corporation(Hexion)

제7장 시장 기회 및 향후 동향

재활용 및 개질 가능한 에폭시 수지 채용 확대

AJY

영문 목차

영문목차

The India Epoxy Resins Market size is estimated at 185.59 kilotons in 2025, and is expected to reach 271.43 kilotons by 2030, at a CAGR of 7.9% during the forecast period (2025-2030).

During the pandemic period due to COVID-19, the market was deeply impacted because of nationwide lockdown, stringent social distancing mandates, and supply chain disruptions. This led to a temporary halt in the production and manufacturing of different products such as paints and coatings, adhesives and sealants, etc., in which epoxy resins are required. However, the market's growth is picking pace because of the government's support to various manufacturing industries in the post-pandemic period.

Key Highlights

The growing construction industry and increasing demand for adhesives and sealants from the automotive industry are the factors driving the market growth.

On the flip side, the hazardous impact of epoxy resins is expected to hinder the growth of the market.

The growing adoption of recyclable and reformable epoxy resin will act as a market oppurtunity in the forecast period.

Epoxy Resin in India Market Trends

Increasing Demand for DGBEA (Bisphenol F and ECH)

Epoxy resins based on bisphenol A-epichlorohydrin are still the most widely used epoxies. Epoxy resins are prepared by reacting compounds containing an active hydrogen group with epichlorohydrin, followed by dehydrohalogenation.

Epoxy resins based on the diglycidylether of bisphenol A (DGEBA) are most commonly used in formulations for adhesives, coatings, laminates, and encapsulants.

Nowadays, roughly 90% of epoxy resin materials worldwide are made from diglycidyl ether of bisphenol A (DGEBA). This resin offers unique features such as outstanding mechanical properties, chemical resistance, and shape stability.

Polycarbonates and epoxy resins are the primary products derived from BPF. These epoxy resins are produced using the same method as performed for DGEBA. The DGEBF (Bisphenol F) epoxy resins have lower viscosity and better mechanical and chemical properties than the DGEBA ones.

Bisphenol F epoxy resins are used in broad applications, including coatings, civil engineering, adhesives, electrical insulating materials, and reactive intermediates. In particular, the liquid resins have low viscosity, so they excel in workability and moldability, which makes them suited to many applications.

Paints and Coatings Segment to Dominate the Market

The paints and coatings segment is expected to grow the fastest in the Indian epoxy resin industry, owing to its widespread use in the building, automotive, energy, and electronic industries.

Epoxy resins are used as binders for coating applications to enhance the durability of coating for floor and metal applications.

India is one of the fastest-growing countries in manufacturing sectors and machinery growth, giving rise to the need for paints and coatings. The government is providing various benefits to the companies setting their manufacturing units in the country and framing various policies to boost the manufacturing sector. For instance, India outlined a plan in August 2021 to reach its goal of USD 1 trillion in manufactured goods exports.

The Indian paint industry is estimated to have a turnover of around USD 6708.33 million. Asian Paints, the largest domestic player in the market, operates ten production facilities in the country, while Berger paints use 12 production facilities.

According to the OICA, around 43,99,112 units of vehicles were produced in 2021, which increased by 30% in comparison to 33,81,819 units manufactured in 2020.

Automotive production for passenger vehicles (except for BMW, Mercedes, Tata Motors & Volvo Auto), three-wheelers, two-wheelers, and quadricycles witnessed 2,214,745 units by October 2021.

According to the IBEF, the government of India expects the automobile sector to generate USD 8-10 billion by 2023 through local and foreign investment.

Such factors are expected to drive the demand for epoxy resins in paints and coatings, thus increasing the market's growth during the forecast period.

Epoxy Resin in India Industry Overview

The Indian epoxy resins market is partially fragmented, with the presence of various players in the market. A few major companies in India's epoxy resins market (not in a particular order) include Aditya Birla Chemicals, Atul Ltd., KUKDO CHEMICAL Co. Ltd, Hexion, and Huntsman International LLC, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Strong Growth in the Construction Industry

4.1.2 Increasing Demand of Adhesives and Sealants in Automotive Industry

4.2 Restraints

4.2.1 Hazardous Impact of Epoxy Resins

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Raw Material

5.1.1 DGBEA (Bisphenol A and ECH)

5.1.2 DGBEF (Bisphenol F and ECH)

5.1.3 Novolac (Formaldehyde and Phenols)

5.1.4 Aliphatic (Aliphatic Alcohols)

5.1.5 Glycidylamine (Aromatic Amines and ECH)

5.1.6 Other Raw Materials

5.2 Application

5.2.1 Paints and Coatings

5.2.2 Adhesives and sealants

5.2.3 Composites

5.2.4 Electrical and Electronics

5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

6.4.1 3M

6.4.2 Aditya Birla Chemicals

6.4.3 Atul Ltd

6.4.4 BASF SE

6.4.5 Daicel Corporation

6.4.6 DuPont

6.4.7 KUKDO CHEMICAL CO., LTD.

6.4.8 Huntsman International LLC

6.4.9 MACRO POLYMERS Pvt Ltd

6.4.10 NAN YA PLASTICS CORPORATION

6.4.11 Olin Corporation

6.4.12 Westlake Corporation (Hexion)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Adoption of Recyclable And Reformable Epoxy Resins