InGaAs 카메라- 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

InGaAs Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1687736

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

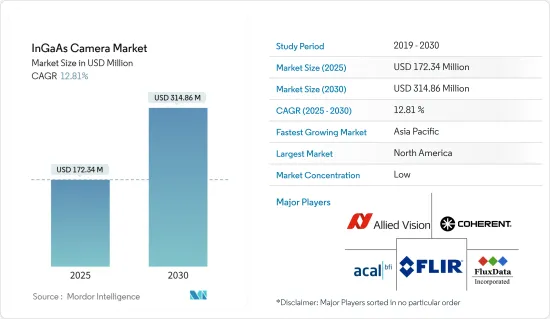

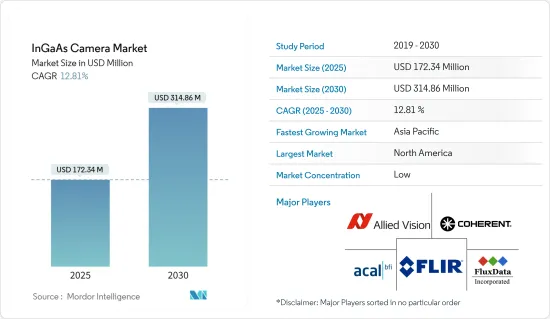

InGaAs 카메라 시장 규모는 2025년에 1억 7,234만 달러에 달할 것으로 추정됩니다. 예측 기간(2025-2030년)의 CAGR은 12.81%를 나타내 2030년에는 3억 1,486만 달러에 이를 것으로 예상되고 있습니다.

비전 가이드 로봇 시스템과 같은 자동화 솔루션의 채택이 증가하고 있으며, 오염 및 결함 감지를 위해 이러한 카메라의 사용이 증가하고 있다는 점이 조사한 시장 성장을 가속하는 중요한 요소 중 하나입니다.

주요 하이라이트

InGaAs는 근적외선(NIR)과 단파장 적외선(SWIR)으로 높은 광감도를 가진 III-V족 화합물 반도체입니다.

InGaAs는 항공우주, 군사, 통신, 공업 검사, 분광 등에 사용되는 냉각 기반의 카메라입니다. 소형, 비냉각, 경량 설계, 고품질의 암시 기능, 부속의 은밀한 아이 세이프 레이저, 대상 인식, 야광에 대한 감도 등의 성능 특성에 의해 이러한 카메라는 방위 부문으로 많은 용도를 찾아내고 있습니다.

InGaAs 카메라는 실리콘 검출기가 더 이상 작동하지 않는 NIR 파장 950-1,700nm와 실리콘 검출기가 더 이상 감도가 없는 950-1,700nm 사이의 갭을 메우고 있습니다. 따라서 InGaAs는 보다 종합적인 NIR 영역에서 감도를 기재하고 있습니다. FPA 카메라에서는 불필요한 노이즈원을 저감하기 위해(-85℃까지) 강력한 냉각이 필요합니다.

게다가 InGaAs는 검출기 재료로서 습도 측정, 표면막 분포, 폴리머와 천연 재료의 분리 등의 선별 작업 등 근적외(NIR) 산업용도에 저렴한 대체 수단을 제공했습니다.

인더스트리 4.0은 로봇 등의 기술 개발을 가속화하고 현재는 산업 자동화에서 중요한 역할을 담당하고 있으며, 로봇이 산업의 많은 핵심 업무를 관리하고 있습니다. 비전 유도 로봇 등이 있습니다.이 비전 가이드 로봇은 빈에서 임의의 부품을 찾아 피킹하는 IR 이미저와 각 부품의 방향을 분석하여 벨트 컨베이어에 올리는 카메라로 구성되어 있습니다.

게다가 머신 비전의 사용은 해마다 증가하고 있습니다. Automation에 의하면, 자동 검사와 가이던스용 머신 비전은 2022년 상반기도 북미에서 플러스 성장을 계속했고, 향후 수년간 양호한 시장 성장이 예측되고 있습니다.

그러나, InGaAs 카메라의 비용 고가 조사 시장의 성장을 저해하는 주요인의 하나입니다. 또한, 여러 나라에서의 엄격한 수출입 규제 증가가 조사 시장의 개척을 억제하고 있습니다.

InGaAs 카메라 시장 동향

산업 자동화가 최대 시장 점유율을 차지할 전망

시장 성장을 가속하는 주요 요인 중 하나는 다양한 용도에서 InGaAs 카메라 수요 증가입니다. 또한 산업 자동화 부문에서 InGaAs 카메라의 사용이 증가하고 있는 것도 시장 성장을 가속하는 요인 중 하나입니다.

머신 비전 시스템의 채용이 증가하고 있기 때문에 산업 자동화 부문에서의 InGaAs 카메라 수요가 예상되고 있습니다.머신 비전 환경에서는 카메라 시스템은 생산 라인으로 제품을 스캔하기 위해서 사용됩니다.

또한 머신 비전은 로봇의 효율성과 비즈니스의 전반적인 가치를 향상시키기 위해 로봇과 함께 사용되는 경우가 많습니다. 드포지션에 설치되어 있습니다. 예를 들어 IFR의 2023년 보고서에 따르면 2022년 전 세계 작업 로봇 재고는 약 350만 대에 달해 최고치를 기록할 것으로 예상됩니다.

게다가 예측기간 중에 산업용 로봇의 도입이 증가할 것으로 예상되므로, 조사 대상 시장에서는 산업용 부문에서의 수요가 플러스로 변할 것으로 전망됩니다.

다양한 산업이 이 기술을 이용하여 생산을 자동화해 제품의 품질과 속도를 향상시키고 있습니다.

예를 들어, 2023년 1월, Lucid Vision Labs는 1.3MP와 0.3MP의 신제품 Triton SWIR IP67 표준 산업용 비전 카메라를 발표했습니다. InGaAs 센서를 탑재하고 있어, 가시광과 불가시광의 스펙트럼으로 화상을 캡쳐 할 수 있어 픽셀 사이즈는 5m입니다.

북미가 최대 시장 점유율을 차지할 전망

군사 및 방위 용도로 UAV나 UGV와 같은 로봇의 사용이 증가하고 있기 때문에 북미에서는 InGaAs 카메라 수요가 증가할 것으로 예상됩니다.

기업, 학술기관, 연방 정부에 최첨단 자동화 기술에 대한 투자를 장려하는 것을 목적으로 한 선진 제조 파트너십과 같은 정부 프로그램의 결과, 머신 비전 시스템의 생산은 증가합니다.

InGaAs 카메라는 연기, 안개, 연무, 수증기 등의 악조건을 전망하기 위해 군사 및 방위 부문에서 널리 사용되고 있기 때문에 미국과 같은 국가는 방위 예산과 첨단 장비에 지출 예를 들어, 미국은 2023 회계 연도에 8,133억 달러의 국방 예산을 요구했습니다.

게다가 실리콘 웨이퍼의 패턴 검사 등의 용도로 InGaAs 카메라 수요가 증가하고 있는 반도체 산업은 미국을 중심으로 한 북미에서 견인력을 늘리고 있습니다.

InGaAs 카메라는 광간섭 단층계(OCT)나 분광법 등의 의료 화상 용도에 있어서 고감도·저노이즈를 실현합니다.

북미의 InGaAs 카메라 시장은 이 지역에서 활동하는 다양한 최종 사용자로부터의 고도로 효과적인 이미징 시스템에 대한 수요가 꾸준히 증가하고 있기 때문에 예측되는 기간 동안 양호한 성장률을 경험할 것으로 예측되고 있습니다.

InGaAs 카메라 산업 개요

InGaAs 카메라 시장은 많은 대기업과 신규 참가 기업에 의해 구성되어 있어 경쟁이 격렬합니다. Allied Vision Technologies GmbH, Acal BFI Limited Company, Coherent Inc., and Flir Systems Inc. 등을 들 수 있습니다.

2022년 12월, JAI는 복수의 CMOS 센서와 단파장 적외(SWIR) 스펙트럼으로부터 화상 데이터를 수집하기 위한 인듐 갈륨 비소(InGaAs) 기술에 의한 센서로 구성된 4센서 라인 스캔 기술을 특징으로 하는 새로운 산업용 프리즘 베이스라인 스캔 카메라, SW-4010Q-MCL의 출시를 발표했습니다.

2022년 11월 Allied Vision은 1.9μm 또는 2.2μm까지의 파장을 높은 양자 효율로 검출할 수 있는 InGaAs 센서를 확대 탑재한 Goldeye SWIR 카메라 4기종의 발매를 발표했습니다.

The InGaAs Camera Market size is estimated at USD 172.34 million in 2025, and is expected to reach USD 314.86 million by 2030, at a CAGR of 12.81% during the forecast period (2025-2030).

The increasing adoption of automation solutions, such as vision-guided robotic systems, and the increasing use of these cameras for contamination and defect detection are among the significant factors driving the growth of the studied market.

Key Highlights

InGaAs is an III-V compound semiconductor with high photosensitivity in the near-infrared (NIR) and short-wave infrared (SWIR). The InGaAs camera uses this feature in various applications, including real-time in-line non-destructive inspection. The rise in demand for line scan InGaAs cameras for machine vision applications is a crucial driver of the InGaAs camera market.

InGaAs are cooling-based cameras used in aerospace, military, telecommunications, industrial inspection, and spectroscopy. It has infrared (IR) technology, which allows for night vision or visibility through atmospheric haze and is primarily used by military and defense forces. Because of their performance characteristics, such as small, uncooled, lightweight design, high-quality night vision, attached covert eye-safe lasers, target recognition, and sensitivity to nightglows, these cameras find many applications in defense.

InGaAs cameras bridge the gap between NIR wavelengths 950-1700 nm, where silicon detectors no longer work, and 950 - 1700 nm, where silicon detectors are no longer sensitive. Because of its lower bandgap, InGaAs provide sensitivity over a more comprehensive NIR range. When compared to Si-CCDs, the lower bandgap is also responsible for a much higher dark current (thermally generated signal). As a result, scientific InGaAs FPA cameras require intense cooling (down to -85°C) to reduce some unwanted noise sources.

Moreover, as a detector material, InGaAs provided an affordable alternative for near-infrared (NIR) industrial applications such as humidity measurement, surface film distributions, and sorting tasks such as separating polymers from natural materials. As a result, the use of technology in industrial manufacturing and automation is increasing.

Industry 4.0 accelerated the development of technologies such as robots, which now play a critical role in industrial automation, with robots managing many core operations in industries. New applications for InGaAs cameras include vision-guided robotics and automated butchering. These vision-guided robots are made up of IR imagers that find and pick random parts from a bin, followed by a camera that analyzes the orientation of each part and places it on a conveyor belt.

Furthermore, the use of machine vision is increasing year after year. Machine vision sales are at an all-time high in some regions. According to the Association for Advancing Automation, machine vision for automated inspection and guidance continued its positive growth trajectory in North America in the first half of 2022, with favorable market growth predicted throughout the year. This is expected to drive demand for InGaAs cameras in such applications during the forecast period.

However, the higher cost of InGaAs cameras is one of the major factors impeding the growth of the studied market. Furthermore, a rise in stringent import and export regulations across various countries restrains the development of the studied market.

InGaAs Camera Market Trends

Industrial Automation Expected to Occupy the Largest Market Share

One of the key factors driving market growth is the increasing demand for InGaAs cameras in various applications. Another factor driving market growth is the increasing use of InGaAs cameras in the industrial automation sector. InGaAs cameras are used in industrial automation applications like thermal imaging, machine vision, and quality control because they outperform other types of cameras.

The increasing adoption of machine vision systems is expected to drive demand for InGaAs cameras in the industrial automation segment. In a machine vision environment, a camera system is used to scan products on a production line. The camera captures the image and compares it to pre-defined criteria.

Moreover, machine vision is increasingly being used in conjunction with robots to improve their effectiveness and overall value to the business. These robots have a camera mounted at the hand position that guides them through the task at hand. For example, according to IFR's 2023 report, the global stock of operational robots was to reach a new high of approximately 3.5 million units in 2022. In the meantime, the value of installations reached an estimated USD 15.7 billion.

Furthermore, with the adoption of industrial robots expected to increase over the forecast period, the studied market is expected to see a positive increase in demand from the industrial segment. The annual installation of industrial robots is expected to reach 518 thousand units by 2024, according to IFR.

Different industries use this technology to automate production and improve product quality and speed. The growing need for high-quality inspection and automation in various industries drives the demand for machine vision, eventually boosting the InGaAs camera market. Furthermore, increased R&D and the launch of new products by InGaAs camera market players are propelling the InGaAs camera market significantly.

For instance, in January 2023, Lucid Vision Labs unveiled its brand-new 1.3MP and 0.3MP Triton SWIR IP67-rated industrial vision cameras. The Triton SWIR is a GigE PoE camera with wide-band and high-sensitivity Sony SenSWIR 1.3MP IMX990 and 0.3MP IMX991 InGaAs sensors capable of capturing images in visible and invisible light spectrums and a pixel size of 5m.

North America is Expected to Account for the Largest Market Share

The rising use of robotics like UAVs and UGVs in military and defense applications is expected to increase demand for InGaAs cameras in North America. Moreover, higher penetration of automation and advanced technologies in the industrial domain favors the growth of the studied market in the region.

The production of machine vision systems will be increased as a result of government programs like the Advanced Manufacturing Partnership, which aims to encourage businesses, academic institutions, and the federal government to invest in cutting-edge automation technologies. This will create a positive outlook for the market's growth.

As InGaAs cameras are widely used in the military and defense sector to see through unfavorable conditions such as smoke, fog, haze, and water vapor, countries like the United States have increased their defense budgets and expenditure on advanced equipment. For example, a budget request for national defense of USD 813.3 billion in the United States has been made for the fiscal year 2023. Such defense spending is expected to drive market demand.

Furthermore, the semiconductor industry, where demand for InGaAs cameras in applications such as silicon wafer pattern inspection is increasing, is gaining traction in the North American region, particularly in the United States. Favorable government investments, such as the US CHIPS Act, and vendor investments in the chip industry are thus expected to drive demand for InGaAs cameras during the forecast period.

InGaAs cameras provide high sensitivity and low noise in medical imaging applications such as optical coherence tomography (OCT) and spectroscopy. Countries such as the United States, Canada, and others are constantly investing in advancing their medical industries, which is expected to drive growth opportunities in the increasing use of InGaAs cameras in medical imaging applications.

The InGaAs camera market in North America is anticipated to experience favorable growth rates during the anticipated period due to the steadily increasing demand for advanced and effective imaging systems from various end-users operating in the area. Furthermore, advancements in industrial automation with the widespread adoption of robots and government spending in the defense and military industries are expected to drive the market in the coming years.

InGaAs Camera Industry Overview

The InGaAs camera market is competitive due to the market consisting of many large players as well as new players. Companies are trying to innovate their existing products to cater to increasing consumer demand, making the market competitive. Furthermore, the growing demand attracts new players, making the market fragmented. Some of the major players are Allied Vision Technologies GmbH, Acal BFI Limited Company, Coherent Inc., and Flir Systems Inc., among others.

In December 2022, JAI announced the launch of SW-4010Q-MCL, a new industrial prism-based line scan camera featuring 4-sensor line scan technology consisting of multiple CMOS sensors and a sensor based on indium gallium arsenide (InGaAs) technology to collect image data from the short wave infrared (SWIR) spectrum.

In November 2022, Allied Vision announced the launch of four new Goldeye SWIR camera models equipped with an extended range of InGaAs sensors, capable of detecting wavelengths up to 1.9 μm or 2.2 μm at high quantum efficiencies. The integrated dual-stage sensor cooling and several onboard image correction features are among the key factors to make specific spectral features visible with outstanding image quality.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview?

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

4.4 Technology Snapshot

4.4.1 Uncooled

4.4.2 Cooled

4.5 Market Drivers

4.5.1 Increasing Adoption in Machine Vision Applications

4.5.2 Rising Demand in Military and Defense Operations

4.6 Market Challenges

4.6.1 High Procurement Cost of InGaAS Cameras

4.6.2 Stringent Regulation on Export and Import

4.7 Assessment of Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

5.1 By Application

5.1.1 Military and Defense

5.1.2 Industrial Automation

5.1.3 Surveillance and Security

5.1.4 Other Applications

5.2 By Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.2 Europe

5.2.2.1 United Kingdom

5.2.2.2 Germany

5.2.2.3 France

5.2.2.4 Italy

5.2.3 Asia

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Japan

5.2.3.4 Australia and New Zealand

5.2.3.5 South East Asia

5.2.4 Latin America

5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Allied Vision Technologies GmbH (TKH group)

6.1.2 Acal BFI Limited Company (Discoverie Group PLC)