ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

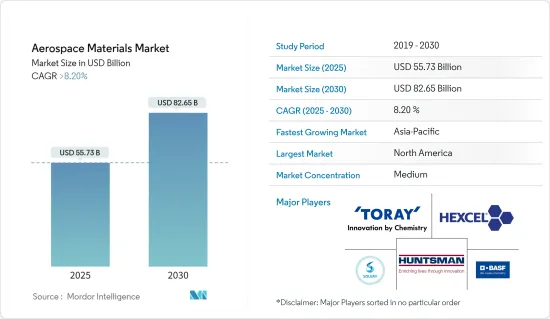

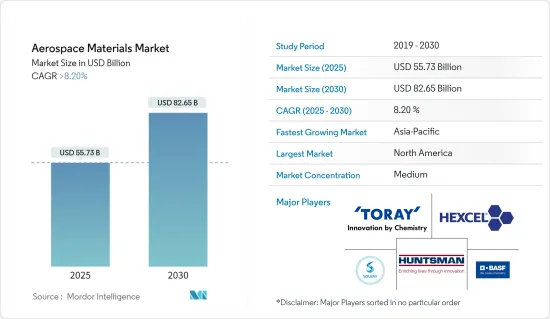

세계의 항공우주 재료 시장 규모는 2025년 557억 3,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 8.2%를 넘어 2030년에는 826억 5,000만 달러에 달할 것으로 예측되고 있습니다.

COVID-19 팬데믹은 2020년 시장에 부정적인 영향을 미쳤습니다.

주요 하이라이트

중기적으로는 항공기 제조에 있어서의 복합재료의 사용량 증가, 우주산업의 성장, 미국과 유럽 국가에서 방위에 대한 정부 지출 증가가 시장의 성장을 견인할 것으로 예상됩니다.

반면, 탄소섬유의 제조 비용의 높이와 합금의 사용량의 감소가, 예측 기간 중에 대상 산업의 성장을 억제할 것으로 예상되는 주된 요인입니다.

에폭시 접착제에 탄소나노튜브나 나노첨가제를 사용하는 것으로, 향후 수년간은 시장에 비즈니스 기회가 생길 가능성이 높습니다.

북미는 민간 항공기의 높은 수요, 군사비에 있어서의 정부 지원의 확대, 우주선 부문에 있어서의 기회 확대에 의해 시장을 독점할 것으로 예상됩니다.

항공우주 재료 시장 동향

일반 및 민간 항공기 수요 증가

일반 및 민간 항공기는 민간항공(개인 및 상업 모두), 여객 및 화물운송 등 다양한 목적으로 사용되고 있습니다.

항공우주 산업은 여객 수요의 강화로 성장이 정체되고 있습니다. 신규 항공기의 수주 잔여와 비즈니스 항공기의 끊임없는 부활이 더욱 성장에 기여할 수 있습니다.

세계의 부유층 및 초부유층 증가에 따라, 개인 여행 수요가 증가하고 있어, 그 결과, 기내의 내장을 개선한 헬리콥터나 비즈니스 제트기의 조달이 진행되고 있습니다.

IATA(국제항공운송협회)에 따르면 2023년 세계항공운송량의 연간 성장률은 2022년 36.9% 증가했습니다.

항공우주산업은 급속한 기술진보와 기술 혁신이 진행되고 있어 항공기 제조업계에 호황을 가져오고 있습니다. Boeing Commercial Outlook 2023-2042에 따르면 국제 항공 운송량의 부활과 국내 항공 여행이 유행 전의 수준으로 돌아온 것으로, 회사는 2042년까지 48,575대의 새로운 민간 제트기의 세계 수요를 예측했습니다.

중국은 가장 큰 항공기 제조업체 중 하나이며 국내 항공 여객의 최대 시장 중 하나입니다. 게다가 이 나라의 항공기 부품 및 조립 제조 부문은 증가의 일도를 따르고 있으며, 소규모 항공기 부품 제조업체는 200사를 넘습니다.

IBEF(인도브랜드 에퀴티재단)와 IATA의 예측에 따르면 인도 항공시장은 2024년까지 세계 3위가 될 것으로 예상됩니다. 항공 분야는 최근의 동향으로서 다양한 투자와 개발이 이루어지고 있습니다. 예를 들어, 2022년 1월, Tata Sons는 18,000캐롤 루피(24억 달러)를 제공하여 국영 Air India 주식을 100% 취득했습니다. 2024년 6월에는 인도 회사 법원(NCLT)이 Air India와 Vistara의 합병을 승인하여 인도 최대의 국제 항공사가 탄생했습니다.

북미가 시장을 독점할 전망

북미는 미국이나 캐나다 등 국가들에서의 수요 증가로 시장을 독점할 것으로 예상됩니다.

미국은 북미 최대의 항공시장을 갖고 있으며 항공기 보유대수도 세계 최대 수준입니다.

2022년부터 2023년까지 미국 정부가 국방을 위해 할당한 금액은 550억 달러 증가했습니다.

일반항공공업회(GAMA)는 2023년 3분기 비즈니스 항공기 제조업체의 실적이 호조였다고 발표했습니다. 또한 미국 제조업체의 생산이 증가해, 2023년 제3분기에 512기를 납입, 전 분기 473기로부터 증가해, 8.2%의 성장을 나타냈습니다. 이것은 제3분기의 세계 총 출하량의 70%에 상당합니다.

캐나다 항공우주 산업 협회(AIAC)에 따르면 항공우주 산업의 연간 매출은 310억 캐나다 달러(230억 달러)였습니다.

몬트리올은 워싱턴주 시애틀, 프랑스의 툴루즈에 이은 세계 제3위의 항공우주 허브입니다.

항공우주 재료 산업 개요

세계의 항공우주 재료 시장은 그 특성상 부분적으로 통합되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

항공기 제조에서의 복합재 사용 증가

우주산업의 성장

미국 및 유럽 국가에서 국방에 대한 정부 지출 증가

억제요인

탄소섬유의 높은 제조 비용

합금의 사용량 감소

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

구조용

복합재

유리 섬유

탄소섬유

아라미드 섬유

기타 복합재

플라스틱

합금

티타늄

알루미늄

강철

슈퍼

마그네슘

기타 합금

비구조용

코팅

접착제 및 실란트

에폭시

폴리우레탄

실리콘

기타 접착제 및 실란트

폼

폴리에틸렌

폴리우레탄

기타 폼

씰

항공기 유형별

일반 및 상업

군 및 방위

우주선

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Acerinox SA(VDM Metals)

Akzo Nobel NV

Aluminum Corporation of China Limited(Chalco)

Arkema

ATI

Axalta Coating Systems

BASF SE

Beacon Adhesives Inc.

Carpenter Technology Corporation

Corporation VSMPO-AVISMA

DELO Industrie Klebstoffe GmbH & Co. KGaA

Evonik Industries AG

Greiner AG

Henkel AG & Co. KGaA

Hentzen Coatings Inc.

Hexcel Corporation

Howmet Aerospace

Huntsman International LLC

HYOSUNG

ISOVOLTA AG

Jiangsu Hengshen Co. Ltd

Mankiewicz Gebr & Co.

Mitsubishi Chemical Corporation

Nanjing Yunhai Special Metal Co. Ltd

NIPPON STEEL CORPORATION

PPG Industries Inc.

Precision Castparts Corp.

Reliance Industries Ltd

Rogers Corporation

SGL Carbon

Socomore

Solvay

Tata Steel(Corus)

The Sherwin-Williams Company

Toray Industries Inc.

제7장 시장 기회와 앞으로의 동향

탄소나노튜브와 나노 첨가제의 에폭시 접착제에 대한 이용

JHS

영문 목차

영문목차

The Aerospace Materials Market size is estimated at USD 55.73 billion in 2025, and is expected to reach USD 82.65 billion by 2030, at a CAGR of greater than 8.2% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market in 2020. Passenger air travel facilities were temporarily shut down because of the pandemic and the lockdowns imposed to curb the spread of the virus. However, the market showed significant growth in 2021 and is continuing to grow in recent years.

Key Highlights

Over the medium term, the increasing usage of composites in aircraft manufacturing, the growing space industry, and increasing government spending on defense in the United States and European countries are expected to drive the market's growth.

On the flip side, the high manufacturing cost of carbon fibers and the declining usage of alloys are the key factors anticipated to restrain the growth of the target industry during the forecast period.

The use of carbon nanotubes and nano-additives with epoxy adhesives is likely to create opportunities for the market in the coming years.

North America is expected to dominate the market due to the high demand for commercial aircraft, growing government support in military spending, and expanding opportunities in the spacecraft segment.

Aerospace Materials Market Trends

The Demand for General and Commercial Aircraft is Increasing

General and commercial aircraft are used for various purposes, including civil aviation (both private and commercial) and passenger and freight transportation.

The aerospace industry is experiencing stagnant growth owing to the strengthening of passenger travel demand. The backlog of new aircraft orders and the constant resurgence of business aircraft may further contribute to its growth.

Demand for private travel has increased as the number of high- and ultra-high-net-worth individuals has increased globally, resulting in the procurement of helicopters and business jets with improved cabin interiors.

According to IATA (International Air Transport Association), the annual growth of global air traffic in 2023 increased by 36.9% in 2022.

The aerospace industry is undergoing rapid technological advancements and innovation, creating upswings for aircraft manufacturing industries. According to the Boeing Commercial Outlook 2023-2042, with a resurgence in international traffic and domestic air travel back to pre-pandemic levels, the company has projected global demand for 48,575 new commercial jets by 2042.

China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been increasing, with over 200 small aircraft parts manufacturers.

As per IBEF (India Brand Equity Foundation) and IATA forecasts, India's aviation market is expected to be the world's third-largest by 2024. The aviation sector has witnessed various investments and developments in recent times. For instance, in January 2022, Tata Sons acquired 100% shares of the state-run Air India by offering INR 18,000 crore (USD 2.4 billion). In June 2024, the National Company Law Tribunal (NCLT) approved the merger of Air India and Vistara to form the largest international carrier in India.

North America is Expected to Dominate the Market

North America is expected to dominate the market due to increasing demand from countries like the United States and Canada.

The United States has the largest aviation market in North America and one of the world's largest fleet sizes. Strong exports of aerospace components to countries such as France, China, and Germany, along with robust consumer spending in the United States, have been driving the aerospace industry's manufacturing activities, which is expected to induce a positive momentum for the country's aerospace material market.

From 2022 to 2023, the amount of money the United States government allocated for defense rose by USD 55 billion, partly because of extra military assistance provided to back Ukraine during its continuous battle. The United States allocates more funds to defense than the next eight nations. Also, the United States government has signed the Fiscal 2023 National Defense Authorization Act into law, allotting USD 816.7 billion to the Department of Defense.

The General Aviation Manufacturers Association (GAMA) announced that business aircraft manufacturers had a strong performance in the third quarter of 2023. In addition, the United States manufacturers saw an increase in production, delivering 512 aircraft in Q3 2023, a rise from 473 in the previous quarter, marking an 8.2% growth. This represents 70% of the total global shipments in the third quarter.

According to the Aerospace Industries Association of Canada (AIAC), the aerospace industry generates CAD 31 billion (USD 23 billion) in annual revenue. Approximately 80% of Canada's aerospace industry is civil-oriented, and 20% is military-oriented.

Montreal is the world's third-largest aerospace hub after Seattle, Washington, and Toulouse, France. Aerospace leads the Canadian manufacturing sector in innovation-related investment, with an annual expenditure of over USD 1.4 billion on R&D activities.

Aerospace Materials Industry Overview

The global aerospace materials market is partially consolidated in nature. Some of the major players in the market (no particular order) include BASF SE, Toray Industries Inc., Hexcel Corporation, Solvay, and Hunstman International LLC.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Use of Composites in Aircraft Manufacturing

4.1.2 Growing Space Industry

4.1.3 Increasing Government Spending on Defense in the United States and European Countries

4.2 Restraints

4.2.1 High Manufacturing Cost of Carbon Fibers

4.2.2 Declining Usage of Alloys

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

5.1 Type

5.1.1 Structural

5.1.1.1 Composites

5.1.1.1.1 Glass Fiber

5.1.1.1.2 Carbon Fiber

5.1.1.1.3 Aramid Fiber

5.1.1.1.4 Other Composites

5.1.1.2 Plastics

5.1.1.3 Alloys

5.1.1.3.1 Titanium

5.1.1.3.2 Aluminium

5.1.1.3.3 Steel

5.1.1.3.4 Super

5.1.1.3.5 Magnesium

5.1.1.3.6 Other Alloys

5.1.2 Non-structural

5.1.2.1 Coatings

5.1.2.2 Adhesives and Sealants

5.1.2.2.1 Epoxy

5.1.2.2.2 Polyurethane

5.1.2.2.3 Silicone

5.1.2.2.4 Other Adhesives and Sealants

5.1.2.3 Foams

5.1.2.3.1 Polyethylene

5.1.2.3.2 Polyurethane

5.1.2.3.3 Other Foams

5.1.2.4 Seals

5.2 Aircraft Type

5.2.1 General and Commercial

5.2.2 Military and Defense

5.2.3 Space Vehicles

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 Acerinox SA (VDM Metals)

6.4.3 Akzo Nobel NV

6.4.4 Aluminum Corporation of China Limited (Chalco)

6.4.5 Arkema

6.4.6 ATI

6.4.7 Axalta Coating Systems

6.4.8 BASF SE

6.4.9 Beacon Adhesives Inc.

6.4.10 Carpenter Technology Corporation

6.4.11 Corporation VSMPO-AVISMA

6.4.12 DELO Industrie Klebstoffe GmbH & Co. KGaA

6.4.13 Evonik Industries AG

6.4.14 Greiner AG

6.4.15 Henkel AG & Co. KGaA

6.4.16 Hentzen Coatings Inc.

6.4.17 Hexcel Corporation

6.4.18 Howmet Aerospace

6.4.19 Huntsman International LLC

6.4.20 HYOSUNG

6.4.21 ISOVOLTA AG

6.4.22 Jiangsu Hengshen Co. Ltd

6.4.23 Mankiewicz Gebr & Co.

6.4.24 Mitsubishi Chemical Corporation

6.4.25 Nanjing Yunhai Special Metal Co. Ltd

6.4.26 NIPPON STEEL CORPORATION

6.4.27 PPG Industries Inc.

6.4.28 Precision Castparts Corp.

6.4.29 Reliance Industries Ltd

6.4.30 Rogers Corporation

6.4.31 SGL Carbon

6.4.32 Socomore

6.4.33 Solvay

6.4.34 Tata Steel (Corus)

6.4.35 The Sherwin-Williams Company

6.4.36 Toray Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Use of Carbon Nanotubes and Nano Additives with Epoxy Adhesives