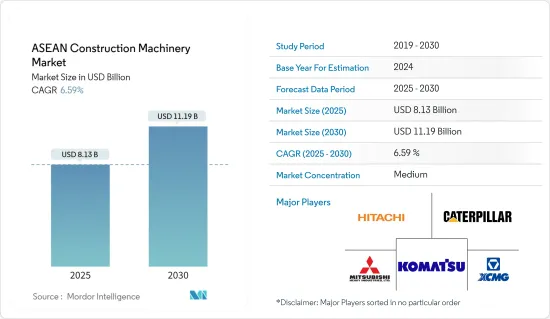

ASEAN의 건설장비 시장 규모는 2025년 81억 3,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 6.59%로 확대되어, 2030년에는 111억 9,000만 달러에 달할 것으로 예측됩니다.

COVID-19 팬데믹은 조사한 시장에 부정적인 영향을 미쳤으며, 주요 원인은 건설 및 제조 활동의 중단이었습니다. 또한 ASEAN 국가 정부는 파이프라인 프로젝트를 일시중지하고 현장 노동력을 줄였습니다. 이것은 건설 생산량의 감소로 이어졌습니다. 그러나 예측기간 동안 건설활동이 증가함에 따라 시장은 크게 성장할 것으로 예상되며, 주요 요인은 세계 정부 지원 증가와 건설활동 회복에 있을 것으로 보입니다.

중기적으로는 ASEAN 지역의 건설장비 수요는 인프라 지출 증가로 인한 것입니다. 또한 이 지역의 제조업이 성장함에 따라 세계 제조업체들이 비용 저하, 국내 소비 증가, 인프라 개선 및 확대 등을 이유로 동남아시아 국가로의 사업 시프트를 계획하고 있으며, 그 결과 건설장비 수요도 증가하고 있습니다.

게다가 인프라 활동을 장려하는 정부의 대처나, 전동화 및 자율화된 기술적으로 선진적인 기계의 채용이 증가하고 있는 것도, 동 시장에서 사업을 전개하는 참가 기업에 새로운 기회를 제공하는 경향에 있습니다. 건설 산업은 더 스마트해지고 있습니다. 디지털화, 연결성, 자동화가 개발을 추진하고 건설 프로젝트에 큰 영향을 미치고 있습니다. 게다가 임대기업은 첨단 건설장비에 대한 수요 증가에 대응하기 위해 신기술에 대한 투자에 임하고 있으며, 구식 건설장비를 새로운 기계 및 업그레이드된 기계로 대체하고 있습니다.

급속한 도시화, 산업화, 이어지는 인프라 시장 개척에 대한 정부 투자 증가, 지역 전체의 부동산 및 건설회사의 확대 및 성장 활동 등의 요인이 시장 수요를 높일 것으로 예상됩니다.

베트남 건설장비 시장의 최근 동향은 베트남의 건설 인프라 개척 프로젝트 증가로 인한 것입니다.

베트남의 기계 ? 설비 산업은 지난 10년간 크게 성장했습니다. 이는 2010-2019년 사이에 이 산업 기업이 보고한 순수입이 매년 14.3% 증가하고 있다는 사실을 보여줍니다. 2020년 베트남에는 기계설비를 생산하는 기업이 2,200개 이상 있어 총 46억 달러를 가져왔습니다.

관민 파트너십 모델 하에 베트남 공항 확대 등 많은 공공 인프라 프로젝트가 실시되고 있습니다.

2030년까지 정부는 도로 정비에 650억 달러를 투입하려는 의향입니다. 롱타인 국제공항(160억 달러), 호치민 시 지하철(62억 달러), 남북고속도로(185억 달러), 하노이 순환도로(3억6,800만 달러), 하이반 2터널(3억1,200만 달러), 다낭의 리엔티에 항구(1억4,700만 달러)는 모두 2022년에 완성되는 중요한 도로 건설 프로젝트입니다.

베트남에서 진행 중과 미래의 건설 활동을 모두 고려하면, 크레인 시장은 예측 기간 동안 안정적인 성장을 이루고 나라의 건설장비 시장을 견인할 것으로 예상됩니다.

ASEAN의 건설장비 시장은 국제적 및 지역적인 참가기업이 다수 존재하는 것이 특징이며, 그 결과 시장경쟁환경이 격화하고 있습니다.

2022년 3월 Iridium Communications Inc.는 Sumitomo Construction Machinery와 링크 벨트 굴삭기를 공동 개발했다고 발표했습니다.

The ASEAN Construction Machinery Market size is estimated at USD 8.13 billion in 2025, and is expected to reach USD 11.19 billion by 2030, at a CAGR of 6.59% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market studied, primarily attributed to halted construction and manufacturing activities. In addition, governments across the ASEAN countries paused the pipeline projects and reduced the workforce over the sites. This has led to a reduction in construction output. However, the market is anticipated to witness significant growth during the forecast period due to the increase in construction activities, which is likely to be primarily attributed to increasing government support and restoration of construction activities worldwide.

Over the medium term, demand for construction machinery in the ASEAN region is driven by increased infrastructure spending. Additionally, with growth in the manufacturing industry in the region, manufacturers from all across the world are planning to shift their operations to the Southeast Asian nations due to lower costs, increasing domestic consumption, and improving and expanding infrastructure, which, in turn, resulted in higher demand for construction machinery.

Moreover, the government initiatives encouraging infrastructure activities and the rising adoption of technologically advanced machinery, both electrified and autonomous, tend to offer new opportunities for players operating in the market. The construction industry is getting smarter. Digitalization, connectivity, and automation are driving the development forward, substantially impacting construction projects. Moreover, renting companies are geared to invest in new technologies to cope with the growing demand for advanced construction machinery and replace the older ones with new or upgraded machinery fleet.

Factors such as rapid urbanization, industrialization, followed by rising government investments in the development of infrastructure, and expansion and growth activities of the real estate and construction companies across the region are expected to enhance demand in the market.

Vietnam's rising construction and infrastructure development projects are mostly to credit for the country's recent growth in the market for construction equipment.

Vietnam's machinery and equipment industry has grown significantly over the past ten years. This is demonstrated by the fact that between 2010 and 2019, the net revenue reported by businesses in this industry grew by 14.3% annually. Until 2020, Vietnam had over 2,200 businesses that produced machinery and equipment, bringing in a combined USD 4.6 billion.

Under the Public-Private Partnership model, a number of public infrastructure projects are undertaken, such as the expansion of Vietnam's airport. The Vietnamese government intends to invest USD11 billion in airport development over the following five years, with the project scheduled to begin in 2022.

By 2030, the government intends to spend 65 billion on road improvements. By 2030, the building of a road network is anticipated to account for around 48% of all investments made in the transportation sector. The Long Thanh Airport (USD16 billion), the Ho Chi Minh City Metro (USD6.2 billion), the North-South Express (USD18.5 billion), the Hanoi Ring Road (USD368 million), the Hai Van Tunnel 2 (USD312 million), and the Lien Chieu Port in Da Nang (USD147 million) are all significant road construction projects that will be completed in 2022.

Considering all the ongoing and future construction activities in Vietnam, the crane market is expected to witness steady growth over the forecast period, propelling the country's construction machinery market.

The ASEAN construction machinery market is characterized by numerous international and regional players, resulting in a highly competitive market environment. The big players have increased their R&D expenditure exponentially to integrate innovation with excellence in performance. The demand for high-performance, highly efficient, and safe handling equipment from the end market is expected to make the market more competitive over the forecast period.

In March 2022, Iridium Communications Inc. announced that it had jointly developed a Link-Belt excavator with Sumitomo Construction Machinery Co., Ltd. Through this partnership, SCM initially integrated Iridium's Short Burst Data Service into its Remote CARE service platform.