ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

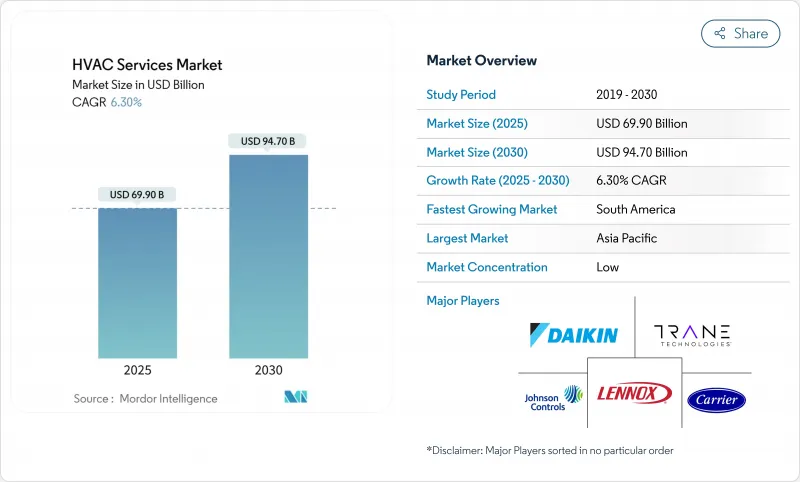

HVAC 서비스 시장 규모는 2025년에 699억 달러로 평가되었고 2030년에는 947억 달러로 확대될 것으로 예측되며 CAGR은 6.30%를 나타낼 전망입니다.

수요는 하이퍼스케일 데이터센터 건설, 의무적 HFC 감축으로 촉발된 개조 열풍, 그리고 사후 대응적 수리를 예측형 서비스 계약으로 전환하는 디지털화에서 비롯됩니다. 아시아태평양 지역의 경제 성장세, 급속한 도시화, 데이터센터 붐은 매출 측면에서 해당 지역의 주도적 위치를 공고히 하는 한편, 전 세계 하이퍼스케일 운영사들은 HVAC 서비스 시장을 전문 냉각, 액체 기반 열 관리, 가동 시간 보장을 위한 구독형 가격 정책으로 이끌고 있습니다. 기존 공급업체들은 IoT 기반 분석 플랫폼을 통해 설치 기반을 수익화하며, 고장 수리 방문을 지속적인 최적화 서비스로 전환하고 있습니다. 그러나 숙련된 노동력 부족과 투입 비용 인플레이션이 마진을 위협하고 있습니다. 따라서 경쟁 압력은 대규모 조달과 강력한 내부 교육을 결합한 기업들에게 유리하게 작용하여, 임금 인플레이션을 흡수하면서도 소규모 경쟁사로부터 시장 점유율을 확보할 수 있게 합니다.

세계의 HVAC 서비스 시장 동향 및 인사이트

신흥국의 건설 활동 확대

아시아태평양 및 라틴아메리카 전역의 가속화된 도시화는 신규 건물 공급을 지속시키며, 이는 자동적으로 HVAC 서비스 시장의 설치 및 시운전 수요로 이어집니다. 건축 허가에 포함된 에너지 효율 규정은 수명 주기 지출을 긴급 수리보다 예방적 유지보수 및 성능 계약으로 전환시키고 있습니다. 인도와 브라질의 정부 녹색 건축 인센티브는 고효율 HVAC의 조기 도입을 장려하여 개발자들이 설계 단계에서 서비스 계약을 체결하도록 유도합니다. 인도 및 브라질 정부의 친환경 건축 인센티브는 고효율 HVAC의 조기 도입을 장려하여 개발자들이 설계 단계에서 서비스 계약을 체결하도록 유도하고 있습니다. 인계 시점에 디지털 모니터링을 통합할 수 있는 공급업체는 건물 수명 주기 전반에 걸쳐 연금형 수익을 확보합니다. 캘리포니아주가 Lincus에 DC 전원 상업용 HVAC에 대해 176만 달러의 보조금을 지급한 것은 전문 서비스 기술에 의존하는 차세대 시스템에 대한 정책 입안자의 의지를 입증합니다.

하이퍼스케일 데이터센터 구축 확대

하이퍼스케일 시설은 정밀한, 종종 액체 기반 냉각을 필요로 하며, 이는 기존 기계 계약업체가 상당한 기술 역량 강화 없이는 서비스할 수 없습니다. 냉각 비용은 데이터센터 전력 예산의 50%에 달할 수 있어, 효율성 증대는 운영자의 총소유비용(TCO)에 핵심적이며 서비스 제공업체 선정의 결정적 요인입니다. 따라서 HVAC 서비스 시장은 고장 발생 전 핫스팟을 예측하는 고급 유체 처리 기술과 AI 기반 모니터링 역량을 보유한 기업에 유리합니다. 트레인 테크놀로지스의 리퀴드스택과의 협력은 OEM이 액체 냉각 전문가와 협력하여 역량 구축을 가속화하는 방식을 보여줍니다. 2024년 초 데이터센터 자본 지출은 185% 급증한 540억 달러를 기록하며, 전문 서비스 수요의 견고한 파이프라인을 보장합니다.

숙련 노동자 부족과 임금 상승

전 세계 HVAC 서비스 시장에는 추가로 11만 명의 기술자가 필요한 반면, 현재 인력의 절반은 이미 45세 이상입니다. 공급업체들은 현재 평균 59,620달러를 지급하며, 데이터센터 전문 직무는 훨씬 더 높은 보수를 요구해 계층적 가격 책정 능력이 부족한 소규모 계약업체들을 압박하고 있습니다. IoT 플랫폼이 IT와 OT를 융합하면서 기계-디지털 하이브리드 기술력을 요구함에 따라 인재 격차는 더욱 심화됩니다. 사내 아카데미에 투자하는 기업들은 서비스 품질과 가동 시간 보장을 유지할 수 있는 반면, 자본력이 부족한 경쟁사들은 고객 이탈 위험에 직면합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장의 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

시장 개요

시장 성장 촉진요인

신흥국의 건설 활동 증가

하이퍼스케일 데이터센터 확장

의무적 냉매 단계적 감축으로 인한 개조 수요 증가

OECD 시장의 노후 건물 재고에 대한 업그레이드 필요성

원격 진단 및 로봇공학으로 인한 서비스 비용 절감

서비스형 HVAC(HVAC-as-a-Service) 계약으로 인한 정기 수익 창출

시장 성장 억제요인

숙련 노동자 부족과 임금 상승

변동성 있는 HVAC 부품 공급 및 원자재 가격 상승

커넥티드 빌딩 시스템의 사이버 보안 위험

구독 기반 혁신 기업으로 인한 마진 압박

가치/공급망 분석

규제 상황

기술의 전망

Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

투자와 M&A의 상황

제5장 시장 규모와 성장 예측

구현 유형별

신축

개조 건물

서비스 유형별

설치 및 교환 서비스

유지보수 및 수리 서비스

에너지 효율 및 보수 서비스

HVAC 제어 업그레이드 및 통합

컨설팅 및 기타 서비스

시스템 유형별

난방 서비스

냉방 서비스

환기 및 IAQ 서비스

통합 건물 관리 서비스

최종 사용자별

주거용

상업용

산업용

용도별

데이터센터

의료시설

교육기관

접객 및 레저

소매

정부 및 공공 건물

기타

지역별

북미

미국

캐나다

멕시코

남미

브라질

아르헨티나

멕시코

기타 남미

유럽

영국

독일

프랑스

베네룩스

기타 유럽

아시아태평양

중국

인도

일본

기타 아시아태평양

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

시장 집중도

전략적 동향

시장 점유율 분석

기업 프로파일

Johnson Controls International PLC

Carrier Global Corporation

Daikin Industries Ltd.

Trane Technologies plc

Lennox International Inc.

Honeywell International Inc.

Siemens AG

LG Electronics Inc.

Electrolux AB

Robert Bosch GmbH

Fujitsu General Ltd.

Nortek Global HVAC

Mitsubishi Electric Corporation

Rheem Manufacturing Company

Danfoss A/S

GREE Electric Appliances Inc.

Midea Group Co. Ltd.

Johnson Service Group plc

Comfort Systems USA, Inc.

EMCOR Group Inc.

제7장 시장 기회와 장래의 전망

HBR

영문 목차

영문목차

The HVAC services market size reached USD 69.90 billion in 2025 and is projected to advance to USD 94.70 billion by 2030, translating to a 6.30% CAGR-evidence that the HVAC services market remains resilient despite refrigerant phase-downs, talent shortages, and supply volatility.

Demand stems from hyperscale data-center construction, a wave of retrofits triggered by mandatory HFC reductions, and digitization that converts reactive fixes into predictive service contracts. Asia-Pacific's economic momentum, rapid urbanization, and data-center boom secure the region's leadership in revenue terms, while hyperscale operators everywhere are propelling the HVAC services market toward specialized cooling, liquid-based thermal management, and subscription pricing for uptime assurance. Established providers are monetizing their installed base through IoT-enabled analytics platforms that transform break-fix visits into continuous optimization services, yet skilled-labor scarcity and input-cost inflation threaten margins. Competitive pressure therefore favors companies that combine scale procurement with strong in-house training, allowing them to absorb wage inflation while capturing share from smaller rivals.

Global HVAC Services Market Trends and Insights

Growing Construction Activity in Emerging Economies

Accelerating urbanization across Asia-Pacific and Latin America sustains new building pipelines that automatically translate into installation and commissioning demand for the HVAC services market. Energy-efficiency codes now embedded in building permits shift lifetime spending toward preventive maintenance and performance contracts rather than emergency repairs. Government green-building incentives in India and Brazil reward early adoption of high-efficiency HVAC, nudging developers to lock in service contracts during the design phase. Providers able to embed digital monitoring at handover secure annuity-style revenue across a building's lifecycle. California's USD 1.76 million grant to Lincus for DC-powered commercial HVAC validates policymaker commitment to next-generation systems that depend on specialist service expertise

Expansion of Hyperscale Data-Center Build-Outs

Hyperscale facilities require precise, often liquid-based cooling that traditional mechanical contractors cannot service without significant up-skilling. Cooling can reach 50% of a data center's power budget, making efficiency gains central to operators' total cost of ownership and a decisive service-provider selection factor . The HVAC services market therefore rewards firms with advanced fluid-handling skills and AI-driven monitoring that predict hot-spots before failures occur. Trane Technologies' collaboration with LiquidStack illustrates how OEMs partner with liquid-cooling experts to accelerate capability build-out. Data-center capital outlays surged 185% to USD 54 billion in early 2024, guaranteeing a robust pipeline of specialized service demand.

Skilled-Labor Shortages and Escalating Wage Bills

The HVAC services market needs an additional 110,000 technicians worldwide, while half the current workforce is already older than 45 . Providers now pay USD 59,620 on average, with specialized data-center roles commanding far higher compensation, squeezing smaller contractors that lack tiered pricing power. The talent gap becomes more acute as IoT platforms converge IT and OT, demanding hybrid mechanical-digital skills. Companies funding in-house academies can maintain service quality and uptime guarantees, while less capitalized rivals risk client attrition.

Other drivers and restraints analyzed in the detailed report include: