ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

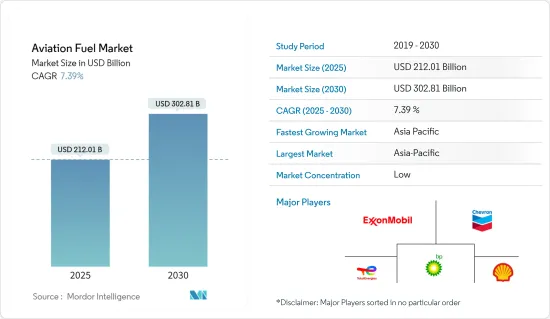

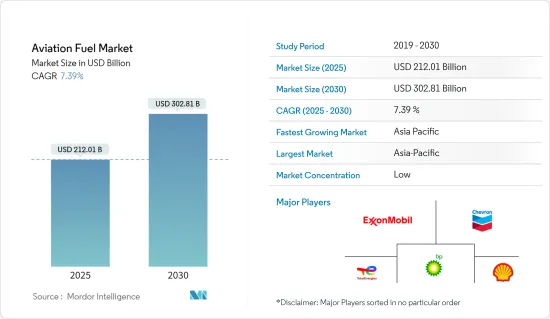

항공 연료 시장 규모는 2025년에 2,120억 1,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 7.39%로 성장할 전망이며, 2030년에는 3,028억 1,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로 항공 수요 증가 및 항공기 보유 수 증가는 예측 기간 동안 시장을 견인할 것으로 보입니다.

반면 대기오염에 대한 환경문제 증가는 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

지속가능한 항공 연료 기술의 진보가 진행됨에 따라 항공 연료 시장에 큰 비즈니스 기회가 생길 것으로 기대되고 있습니다.

아시아태평양은 이 지역에서 항공 여행 및 항공기 보유량이 증가함에 따라 항공 연료 시장의 지배적인 지역이 될 것으로 예상됩니다.

항공 연료 시장 동향

항공 터빈 연료가 시장을 독점할 전망

일반적으로 제트 연료로 알려진 항공 터빈 연료(ATF)는 등유와 유사한 구성을 가진 석유 유래 연료입니다. 제트 A, 제트 A-1, 제트 B 등 세계적으로 다양한 등급이 있으며 제트 A-1이 가장 일반적으로 사용됩니다. 제트 A-1은 다양한 항공기의 터빈 엔진에 적합합니다. 최저 인화점은 섭씨 38도(100°F), 최고 동결점은 섭씨 -47도입니다.

항공 터빈 연료는 민간 여객기, 군용기, 비즈니스 제트기 등 다양한 항공기에 사용되고 있습니다. 현재 취항하고 있는 대부분의 항공기, 특히 대형 민간항공기는 1차 에너지원으로서 제트 연료에 의존하고 있습니다. 다양한 유형의 항공기에서 제트 연료가 널리 사용되는 것이 시장에서의 제트 연료의 우위성에 기여하고 있습니다.

또한 민간항공 및 군용항공에 널리 사용되는 제트엔진은 효율적으로 작동하기 위해 항공터빈 연료를 필요로 합니다. 이 엔진들은 제트 연료의 에너지 함량과 연소 특성을 이용하도록 설계되어 있습니다. 제트 엔진이 항공 산업에서 지배적인 추진 기술로 남아 있는 한, 항공 터빈 연료의 수요는 계속 성장합니다.

예를 들어, 미국 에너지 정보국에 따르면, 미국에서의 제트 연료 소비량은 2022-2021년 사이에 14% 가까이 증가했으며, 이것은 항공기의 운항과 연료 소비 증가를 나타내고 있습니다.

항공 터빈 연료는 피스톤 엔진 기계에 사용되는 아베가스와 같은 다른 연료보다 에너지 밀도가 높습니다. 이는 제트 연료가 단위 부피당 더 많은 에너지를 공급할 수 있다는 것을 의미하며 장거리 비행이나 대형 항공기에 매우 중요합니다. 항공 터빈 연료의 높은 에너지 밀도는 제트 엔진의 동력원으로 이상적이며, 효율적이고 장시간 비행을 가능하게 합니다.

2023년 1월, Indian Oil Corp(IOC)는 소형 항공기와 무인 항공기(UAV)의 요구에 부응하는 항공 연료 수출을 시작했습니다. 이 움직임으로 인도는 석유 수출에 나서 약 27억 달러로 평가되는 세계 시장에 진출할 수 있습니다. Jawaharlal Nehru Port Trust(JNPT)는, 파푸아뉴기니에의 80 배럴의 항공 연료로 이루어진 최초의 위탁품의 출하를 촉진했습니다. 1배럴의 용량은 16킬로리터로, 상당한 양의 항공 가스를 수송할 수 있습니다.

따라서 논의된 바와 같이 항공 터빈 연료는 예측 기간 동안 시장을 축소시킬 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 현저한 경제 성장을 이루고 있으며, 중국, 인도, 동남아시아 국가 등이 이 확대를 견인하고 있습니다. 경제 성장에 따라 항공 수요가 증가하고, 항공 연료 소비량의 증가로 직결됩니다. 이 지역의 강력한 경제 성장은 항공 연료 시장의 우위성을 높이고 있습니다.

아시아태평양은 항공산업이 활발해 수많은 항공사가 존재하며 항공기 보유대수도 증가하고 있습니다. 이 지역의 항공사는 지속적으로 사업을 확대하고 신규 노선을 늘리고 비행 빈도를 늘리고 있습니다. 이러한 확대가 항공 연료 수요를 높이고 이 지역의 항공 연료 시장 우위에 기여하고 있습니다.

또한 아시아태평양의 급속한 도시화와 중류 계급의 인구 증가가 항공 여행의 급증으로 이어지고 있습니다. 이 지역에서 항공 수송을 이용하는 사람이 늘어남에 따라 항공 연료의 수요도 증가하고 있습니다. 도시화의 진전과 중산층의 급증이 아시아 태평양에서의 시장의 우위성을 높이는 주요인이 되고 있습니다.

게다가 아시아태평양에서는 저렴한 항공사(LCC)의 출현과 성장을 볼 수 있습니다. 이 항공사들은 저렴한 항공 운임을 제공하여 더 많은 인구층을 끌어들이고 항공 수요를 자극하고 있습니다. LCC는 통상적으로 높은 탑승률로 운항하기 때문에 연료 소비량의 증가로 이어지고, 그 결과 이 지역에서 항공 연료 시장의 우위성을 높이고 있습니다.

게다가 아시아태평양의 많은 국가들이 공항 인프라 개발에 많은 투자를 하고 있습니다. 새로운 공항이 건설되면서 기존 공항도 확대와 현대화가 진행되고 있습니다. 이러한 인프라 투자는, 항공 교통량과 연료 소비량의 증가에 유리한 조건을 낳아, 항공 연료 시장에 있어서 동지역의 우위성을 한층 더 높이고 있습니다.

예를 들어, 2023년 5월, Indian Oil Corp.는 탈탄소 목표를 달성하기 위해 항공사가 필요로 하는 세계 공급이 크게 부족하기 때문에 1억 2,200만 달러의 지속가능한 항공 연료(SAF) 플랜트를 건설할 예정입니다. 이 계획 시설은 연간 8만 8,000톤의 SAF를 제조할 능력을 가지고 있습니다.

이상의 것으로부터, 예측 기간 중 아시아태평양이 시장을 독점할 것으로 예상됩니다.

항공 연료 산업 개요

항공 연료 시장은 세분화되어 있습니다. 시장의 주요 기업으로는 ExxonMobil, Chevron Corporation, Shell Plc., TotalEnergies SE, BP 등이 있습니다.(순부동)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

서문

시장 규모 및 수요 예측(단위 : 달러)(-2028년)

최근 동향 및 개발

정부 규제 및 시책

시장 역학

성장 촉진요인

항공 수요 증가

항공기재 확대

성장 억제요인

불안정한 원유 가격

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 세분화

연료 유형별

에어 터빈 연료

제트 A-1

제트 A

제트 B

항공 바이오연료

AVGAS

최종 사용자별

상업

방위

일반항공

시장 분석 : 지역별 시장 규모 및 수요 예측(-2028년)

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

남미

브라질

아르헨티나

칠레

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

Exxon Mobil Corporation

Chevron Corporation

Shell Plc.

TotalEnergies SE

BP Plc

Gazprom Neft'PAO

Neste Oyj

Swedish Biofuels AB

Red Rock Biofuels LLC

Abu Dhabi National Oil Company

Bharat Petroleum Corp. Ltd.

Indian Oil Corporation Ltd.

Emirates National Oil Company

Valero Energy Corporation

Allied Aviation Services Inc.

제7장 시장 기회 및 향후 동향

바이오연료 및 지속가능한 대체연료

AJY

영문 목차

영문목차

The Aviation Fuel Market size is estimated at USD 212.01 billion in 2025, and is expected to reach USD 302.81 billion by 2030, at a CAGR of 7.39% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing demand for air travel and an increasing fleet of aircraft is expected to drive the market during the forecasted period.

On the other hand, the increasing environmental concerns for air pollution are expected to hinder the growth of the market during the forecasted period.

Nevertheless, the increasing advancements in sustainable aviation fuel technology are expected to create huge opportunities for the aviation fuel market.

Asia-Pacific is expected to be a dominant aviation fuel market region due to the increasing air travel and aircraft fleets in the region.

Aviation Fuel Market Trends

Aviation Turbine Fuels Expected to Dominate the Market

Aviation Turbine Fuel (ATF), commonly known as jet fuel, is a petroleum-derived fuel with a composition resembling kerosene. It is available in different grades globally, including Jet A, Jet A-1, and Jet B, with Jet A-1 being the most commonly utilized. Jet A-1 is compatible with a wide range of aircraft turbine engines. It exhibits a minimum flash point of 38 degrees Celsius (100°F) and a maximum freeze point of -47 degrees Celsius.

Aviation turbine fuels are used in various aircraft, including commercial airliners, military, and business jets. Most aircraft in service today, especially larger commercial aircraft, rely on jet fuel as their primary energy source. The widespread usage of jet fuel in various aircraft types contributes to its dominance in the market.

Moreover, jet engines, prevalent in commercial and military aviation, require aviation turbine fuels to operate efficiently. These engines are designed to utilize jet fuel's energy content and combustion properties. As long as jet engines remain the dominant propulsion technology in the aviation industry, the demand for aviation turbine fuels will continue to be significant.

For instance, according to the United States Energy Information Administration, the consumption of jet fuel in the United States increased by almost 14% between 2022 and 2021, signifying the increasing air ravels and fuel consumption.

Aviation turbine fuels have a higher energy density than other fuels, such as avgas used in piston-engine aircraft. This means that jet fuel can provide more energy per unit of volume, which is crucial for long-haul flights and larger aircraft. The high energy density of aviation turbine fuels makes them ideal for powering jet engines and allows for efficient and extended flight operations.

In January 2023, The Indian Oil Corporation (IOC) initiated the export of aviation fuel, catering to the requirements of small aircraft and unmanned aerial vehicles (UAVs). This move allows India to enter the global market, valued at approximately USD 2.7 billion, by venturing into petroleum exports. The Jawaharlal Nehru Port Trust (JNPT) facilitated the shipment of the first consignment comprising 80 barrels of aviation fuel to Papua New Guinea. Each barrel has a capacity of 16 kiloliters, enabling the transport of a significant quantity of aviation gas.

Therefore as per the points discussed, aviation turbine fuel is expected to diminish the market during the forecasted period.

Asia-Pacific Expected to Dominate the Market

The Asia-Pacific region is experiencing significant economic growth, with countries like China, India, and Southeast Asian nations driving this expansion. As economies grow, there is a corresponding increase in air travel demand, directly translating to higher aviation fuel consumption. The region's robust economic growth fuels the dominance of the aviation fuel market.

The Asia-Pacific region has a flourishing airline industry with numerous carriers and a growing fleet of aircraft. Airlines in the region continuously expand their operations, adding new routes and increasing flight frequencies. This expansion necessitates a higher demand for aviation fuel, contributing to the dominance of the market in the region.

Moreover, rapid urbanization in the Asia-Pacific region and the rise of the middle-class population has led to a surge in air travel. As more people in the region access air transportation, the demand for aviation fuel grows. The increasing urbanization and a burgeoning middle-class population are key factors driving the dominance of the market in the Asia-Pacific region.

Furthermore, Asia-Pacific region has witnessed the emergence and growth of low-cost carriers (LCCs). These airlines offer affordable airfares, attracting a larger segment of the population and stimulating air travel demand. LCCs typically operate with higher load factors, leading to increased fuel consumption and subsequently driving the aviation fuel market's dominance in the region.

Additionally, many countries in the Asia-Pacific region are investing heavily in airport infrastructure development. New airports are being built, and existing ones are undergoing expansion and modernization. These infrastructure investments create favorable conditions for increased air traffic and fuel consumption, further contributing to the region's dominance in the aviation fuel market.

For instance, in May 2023, Indian Oil Corp. intends to construct a sustainable aviation fuel (SAF) plant worth USD 122 million due to the substantial shortfall in global supplies required by airlines to achieve decarbonization targets. The planned facility will have the capability to manufacture 88,000 tons of SAF annually.

Therefore as per the above-mentioned points the Asia-Pacific region is expected to dominate the market during the forecasted period.

Aviation Fuel Industry Overview

The Aviation fuel market is fragmented. Some of the major players in the market (in no particular order) include ExxonMobil Corporation, Chevron Corporation, Shell Plc., TotalEnergies SE, and BP Plc. among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Air Travel Demand

4.5.1.2 Expanding Airline Fleet

4.5.2 Restraints

4.5.2.1 Volatile Crude Oil Prices

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Fuel Type

5.1.1 Air Turbine Fuel

5.1.1.1 Jet A-1

5.1.1.2 Jet A

5.1.1.3 Jet B

5.1.2 Aviation Biofuel

5.1.3 AVGAS

5.2 End-User

5.2.1 Commercial

5.2.2 Defence

5.2.3 General Aviation

5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Russia

5.3.2.5 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Chile

5.3.4.4 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 United Arab Emirates

5.3.5.3 Egypt

5.3.5.4 South Africa

5.3.5.5 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements