ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

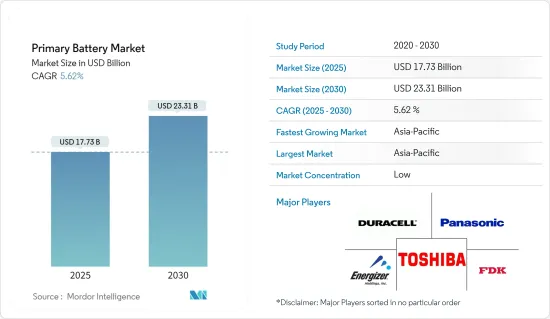

1차 전지 시장 규모는 2025년 177억 3,000만 달러에서 예측 기간(2025-2030년) 동안 CAGR 5.62%로 성장하여 2030년에는 233억 1,000만 달러에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 소비자 일렉트로닉스나 군사 및 헬스케어 용도의 1차 전지 수요 증가 등이 예측 기간 중 시장을 견인할 것으로 보입니다.

한편, 1차 전지의 기능을 대체하는 2차 전지의 점유율 확대가 시장 성장을 억제할 가능성이 높습니다.

그럼에도 불구하고 휴대용 기기와 사물인터넷(IoT) 기기에서 1차 전지의 인기가 높아지면서 1차 전지 시장에 큰 성장 기회를 제공합니다.

아시아태평양은 예측 기간 동안 크게 성장할 것으로 예상되며 중국과 인도와 같은 국가들이 수요의 대부분을 견인합니다.

1차 전지 시장 동향

알칼리 1차 전지가 시장을 독점할 전망

알칼리 1차 전지는 비충전식 배터리 시장에서 가장 인기 있는 화학전지 중 하나입니다. 비에너지가 높고 비용 효과가 뛰어나 친환경적이며 완전히 방전해도 액이 누출되지 않습니다. 알칼리 전지는 최대 10년간 저장이 가능하며 안전성이 높고 유엔 운송규제 및 기타 규제를 받지 않고 항공기에 탑재할 수 있습니다.

알칼리 건전지는 아연과 이산화망간을 전극으로 하는 유형의 일회용 전지입니다. 이 배터리에 사용되는 알칼리 전해액은 수산화칼륨 또는 수산화나트륨입니다. 이 전지는 전압이 안정적이며 탄소 아연 전지보다 에너지 밀도와 누액성이 우수합니다.

또한 알칼리 1차 전지는 에너지 수요가 적은 제품을 중심으로 일상 생활에 필수품으로 자리잡고 있습니다. 알칼리 건전지는 AAA형, AA형, 9V형 등 다양한 사이즈가 있으며 AAA형이나 AA형은 가전 리모컨과 같은 저전력 용도에 적합하고, C형, D형, 9V형은 고전력 용도에 사용되고 있습니다. 그러나 마이크로 알칼리 코인 배터리 및 버튼 배터리와 같은 다른 유형은 소수의 산업용 및 의료용 용도에 사용됩니다.

알칼리 건전지의 1차 수요는 가전, 의료기기, 방위 산업의 소비 확대가 견인하고 있습니다. 예를 들어 재무부 및 일본 전지 공업회에 따르면 2022년 일본 전지산업에서 알칼리 1차 전지의 판매 수량은 2020년 대비 약 12억 5,000만개(0.8% 증가)를 기록했습니다.

알칼리 건전지는 환경친화적이고 쓰레기로 버릴 수 있습니다. 또, 적극적인 회수 및 리사이클의 필요성도 없습니다. 그러나 현재 거의 모든 주요 제조업체가 제조하는 배터리는 수은을 사용하지 않으므로 폐기시 환경 오염이나 위험을 초래하지 않습니다. 다른 충전식 배터리는 적절하게 회수 및 재활용되어야 하기 때문에 이러한 배터리에 대한 적극적인 수요가 발생하고 있습니다.

1차 알칼리 건전지 시장은 예측 기간 동안 2차 전지에 비해 비교적 완만한 성장이 예상됩니다. 그러나 알칼리 전지의 폐기가 쉽고, 대부분의 가전제품이 여전히 1차 알칼리 전지로 작동하고 있는 점 등의 요인이 시장을 견인할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 지금까지 최첨단을 달려왔습니다. 이 지역은 장난감, 리모컨, 시계 등의 전자기기, 포도당 모니터나 혈압계 등의 의료기기 제조의 핫스팟이기 때문에 예측 기간 동안도 1차 전지 시장의 주요 지역의 하나로서 우위를 유지할 것으로 예상됩니다.

중국은 휴대용 전자기기의 주요 제조국이며 수출국 중 하나입니다. 연간 가처분 소득이 증가함에 따라 소비자 전자기기 수요는 예측 기간 동안 상당한 성장이 예상됩니다. 예를 들어 세계은행에 따르면 중국의 1인당 구매력평가(PPP)는 2012년 이후 상승하여 2022년에는 21,475.6달러에 이르렀고 이는 가처분소득 또는 구매력이 크게 증가하고 있음을 보여줍니다.

중국국가통계국에 따르면 2021년 중국 내 가전 및 소비자 일렉트로닉스의 소매 거래 수입은 1,270억 달러였으며, 전년 대비 성장률은 6.16%였습니다.

이 동향은 이 나라에서 가전제품의 판매를 촉진할 것으로 예상됩니다. 그 결과 중국에서는 향후 수년간 가전 시장이 1차 전지의 판매 부문을 지배할 가능성이 높습니다.

마찬가지로, 1차 전지는 일반적으로 TV 리모컨의 전원으로 사용됩니다. 중국 국가 통계국에 따르면 2021년 중국에서는 100가구당 119대의 컬러 TV가 있으며, TV는 가장 일반적인 가정용품 중 하나로 사용되고 있습니다.

일본은 세계 유수의 가전제품 소비국입니다. 일본의 급속한 도시화와 국민의 가처분소득 증가가 이 지역의 가전제품 소비 확대에 기여하고 있습니다. 또한 이 지역의 기술 진보로 현지 가전 제조업체가 증가하여 1차 전지 수요 증가로 이어지고 있습니다.

일본전자정보기술산업협회에 따르면 일본의 일렉트로닉스산업의 총생산액은 2022년 779억 3,000만 달러에 달했습니다. 이러한 제품에는 소비자 전자제품, 산업용 전자 장비, 전자 부품 및 장치가 포함됩니다.

일본의 일렉트로닉스 산업의 일부로서, 가전기기는 2022년에 약 26억 달러를 차지했습니다. 소비자 일렉트로닉스는 산업용 장비 및 전자 부품과 함께 업계에서 가장 중요한 부문 중 하나입니다.

위와 같은 점에서 예측 기간 동안 아시아태평양은 1차 전지 시장을 독점할 것으로 예상됩니다.

1차 전지 산업 개요

1차 전지 시장은 세분화되어 있습니다. 이 시장에 진입하고 있는 주요 기업(순서부동)에는 Duracell Inc., Energizer Holdings Inc., FDK Corporation, Panasonic Corporation, Toshiba Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2028년까지 시장 규모 및 수요 예측(단위 : 달러)

최근 동향 및 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

소비자 일렉트로닉스 시장의 성장

헬스케어 분야에서의 1차 전지 채용 증가

억제요인

2차 전지와의 경쟁

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

유형

알칼리 1차 전지

리튬 1차 전지

기타 유형

지역

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

러시아

기타 유럽

아시아태평양

중국

일본

태국

인도네시아

말레이시아

인도

기타 아시아태평양

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Camelion Battery Co. Ltd

Duracell Inc.

Energizer Holdings Inc.

Ultralife Corporation

FDK Corporation

GP Batteries International Ltd

Panasonic Corporation

Saft Groupe SA

Toshiba Corporation

제7장 시장 기회와 앞으로의 동향

휴대형 및 사물인터넷(IoT) 기기에 대한 수요 증가

CSM

영문 목차

영문목차

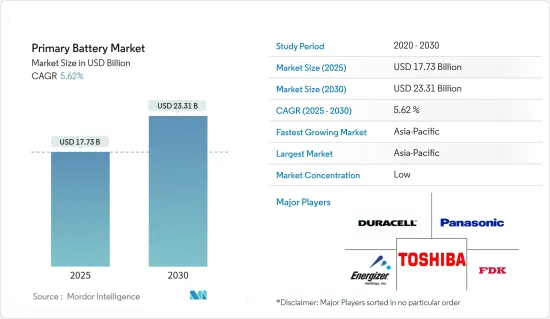

The Primary Battery Market size is estimated at USD 17.73 billion in 2025, and is expected to reach USD 23.31 billion by 2030, at a CAGR of 5.62% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as rising demand for consumer electronics and primary batteries in military and healthcare applications are expected to drive the market during the forecast period.

On the other hand, the increasing share of secondary batteries that replace primary battery functions is likely to restrain the market's growth.

Nevertheless, the increasing popularity of primary batteries in portable and Internet of Things (IoT) devices offers a significant growth opportunity for the primary battery market.

Asia-Pacific is expected to grow significantly during the forecast period, with countries like China and India driving most of the demand.

Primary Battery Market Trends

Primary Alkaline Battery Expected to Dominate the Market

Primary alkaline batteries are among the most popular battery chemistries in the non-rechargeable battery market. It has a high specific energy and is cost-effective, environment-friendly, and leak-proof, even when fully discharged. Alkaline can be stored for up to 10 years, has a good safety record, and can be carried on an aircraft without being subject to UN Transport and other regulations.

Alkaline batteries are the type of disposable batteries that have zinc and manganese dioxide as electrodes. The alkaline electrolyte used in these batteries is either potassium or sodium hydroxide. These batteries have a steady voltage, offering better energy density and leakage resistance than carbon-zinc batteries.

In addition, primary alkaline batteries have become an indispensable part of daily lives, especially for products with low energy demand. Alkaline batteries come in various sizes ranging from AAA, AA, and 9V, where AAA and AA are suited for low-drain applications like consumer electronic remotes, and C, D, and 9V are used for high-drain applications. However, other sizes, such as micro alkaline coin cells and button cells, are used in a few industrial and medical applications.

The primary alkaline battery demand is driven by the growing consumption of consumer electronics, medical devices, and the defense industry. For instance, according to the Ministry of Finance Japan and the Battery Association of Japan, in 2022, the sales quantity of primary alkaline batteries in Japan's cells and batteries industry registred about 1.25 billion units (+0.8%) compared to 2020.

Alkaline batteries are environmentally friendly and can be disposed of as trash. Moreover, they do not require active collection and recycling. However, the batteries made currently by almost all major manufacturers are mercury-free and hence, do not pose any environmental pollution or hazard on disposal. This creates a positive demand for these batteries since other rechargeable consumer batteries must be appropriately collected and recycled.

The primary alkaline battery market is expected to witness growth during the forecast period at a relatively slower rate than secondary batteries. However, factors such as the easy disposal of alkaline batteries and most of the consumer electronics still operating on primary alkaline batteries are anticipated to drive the market.

Asia-Pacific Expected to Dominate the Market

Asia-Pacific has been at the forefront in the past. It is likely to continue its dominance as one of the major regions in the primary battery market during the forecast period as well due to the region being the hotspot for the manufacturing of toys, electronic devices, like remote controls, watches, and medical equipment, like glucose monitors and blood pressure monitors.

China is one of the major manufacturing hubs and exporters of portable electronic devices. With increasing annual disposable income, the demand for consumer electronics is expected to witness considerable growth during the forecast period. For instance, according to the World Bank, purchasing parity per capita (PPP) in China has increased since 2012 and reached USD 21,475.6 in 2022, indicating a substantial increase in disposable income or buying power.

According to the National Bureau of Statistics of China, retail trade revenue for household appliances and consumer electronics in China was USD 127 billion in 2021, with a growth rate of 6.16% from the previous year.

The trend is expected to drive consumer electronics sales in the country. As a result, the consumer electronics market is likely to dominate the primary battery sales segment in China in the coming years.

Similarly, primary batteries are commonly used to power TV remote controls. According to the National Bureau of Statistics of China, in 2021, there were almost 119 color TV sets per hundred households in China, making TVs one of the most common household items.

Japan is one of the largest consumers of consumer electronics products in the world. The rapid urbanization of Japan and the increase in its citizens' disposable income have contributed to the increased consumption of consumer electronics products in the region. Also, technological advances in the region have increased the number of local consumer electronics manufacturers, leading to increased demand for primary batteries.

According to the Japan Electronics and Information Technology Industries Association, the total production value of the electronics industry in Japan reached close to USD 77.93 billion in 2022. These products include consumer electronics, industrial electronics, and electronics components and devices.

As part of the Japanese electronics industry, consumer electronics equipment accounted for approximately USD 2.6 billion in 2022. Consumer electronics is one of the industry's most significant segments, alongside industrial equipment and electronics components.

Therefore, owing to the above-mentioned points, Asia-Pacific is expected to dominate the primary battery market during the forecast period.

Primary Battery Industry Overview

The primary battery market is fragmented. Some of the major players operating in this market (in no particular order) include Duracell Inc., Energizer Holdings Inc., FDK Corporation, Panasonic Corporation, and Toshiba Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast, in USD, till 2028

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Consumer Electronics Market

4.5.1.2 Increasing Adoption of Primary Batteries in the Healthcare Sector

4.5.2 Restraints

4.5.3 Competition from Secondary Batteries

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Primary Alkaline Battery

5.1.2 Primary Lithium Battery

5.1.3 Other Types

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 France

5.2.2.3 United Kingdom

5.2.2.4 Russia

5.2.2.5 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 Japan

5.2.3.3 Thailand

5.2.3.4 Indonesia

5.2.3.5 Malaysia

5.2.3.6 India

5.2.3.7 Rest of Asia-Pacific

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 United Arab Emirates

5.2.5.3 South Africa

5.2.5.4 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Camelion Battery Co. Ltd

6.3.2 Duracell Inc.

6.3.3 Energizer Holdings Inc.

6.3.4 Ultralife Corporation

6.3.5 FDK Corporation

6.3.6 GP Batteries International Ltd

6.3.7 Panasonic Corporation

6.3.8 Saft Groupe SA

6.3.9 Toshiba Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Demand for Portable And Internet Of Things (IoT) Devices