ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

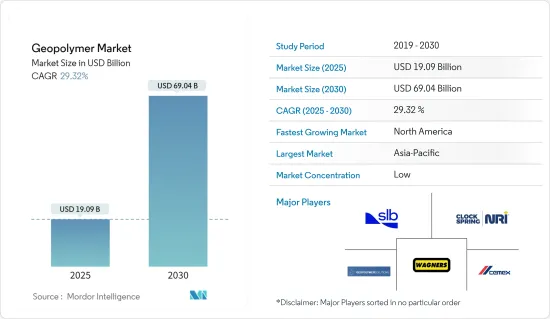

지오폴리머 시장 규모는 2025년에 190억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 29.32%로 성장할 전망이며, 2030년에는 690억 4,000만 달러에 달할 것으로 예측되고 있습니다.

COVID-19의 도입은 지오폴리머 사업에 악영향을 미쳤습니다. 건설산업은 가장 큰 타격을 입은 산업 중 하나로, 근로자 부족과 2020년까지 만연을 막는 것을 목적으로 한 정부의 엄격한 기준으로 인해, 진행 중인 프로젝트는 중단되고 신규 프로젝트도 모두 연기되었습니다. 그러나 2021년에는 건축 및 건설 활동이 활발해지기 때문에 시장은 견조하게 성장할 것으로 예측됩니다.

주요 하이라이트

단기적으로는 시멘트 산업에 대한 환경 규제와 배출 부하, 보수·복구 시장 수요 증가가 조사 대상 시장의 성장을 가속하는 주요 요인입니다.

그러나, 통일된 규칙이나 기준이 없는 것이, 예측 기간 중에 대상 산업의 성장을 둔화시킬 것으로 예상되는 주요인 중 하나입니다.

그래도 소비자는 지오폴리머 제품의 장점을 인식하고 있으며, 가까운 미래에 세계 시장의 성장 기회로 이어질 것으로 예상됩니다.

아시아태평양에서는 건설 활동이 활발해지고 있으며, 세계 시장을 석권하고 있습니다.

지오폴리머 시장 동향

시장을 독점하는 건축 부문

건축물 건설에 있어서의 지오폴리머의 사용은 중요한 역할을 담당하고 있습니다. 전 세계적으로 급속히 확대되는 건설 활동과 인구의 증가로 대량의 온실가스가 대기 중으로 방출되어 환경에 큰 영향을 주고 있습니다. 시멘트 제조 시 및 그 외의 방법으로 배출되는 온실 효과 가스가 환경에 미치는 영향이 증대하는 가운데, 건축 자재의 건설 전반에 있어서, 지오폴리머를 개발 및 사용할 여지가 생겼습니다.

건축 및 건설 분야는 최근 몇년간 급속한 성장을 이루고 있습니다. 세계은행에 따르면 세계 건설산업은 2020년에 22조 3,600억 달러에 이르렀으며, 2021년에는 27조 1,800억 달러까지 성장할 것이라고 합니다.

건설 산업에 있어서의 그린 기술의 개발은 수년전에 거슬러 올라갑니다. 최근 전 세계적으로 환경에 대한 인식이 높아지면서 건축 재료의 기술적 특성과 더불어 환경에 미치는 영향도 적극적으로 평가받게 되었습니다.

지오폴리머 콘크리트, 지오폴리머 시멘트, 바인더, 지오폴리머 벽돌, 패널 등 여러 유형의 지오폴리머 재료는 온실가스의 삭감이나 에너지 절약 등 그 다용도의 특성에 의해 건축물의 건설시에 사용되고 있습니다.

건축물에 있어서 지오폴리머의 최근 용도 예로는 2021년 1월부에서 런던에 건설된 사상 최초의 말뚝을 들 수 있습니다. 이 말뚝은 지오폴리머의 대기업 중 하나인 Wagner의 어스 프렌들리 콘크리트(EFC)를 사용한 것으로 Keltbray Group과 Capital Concrete라는 영국 대기업 2곳과 협력하고 있습니다.

또한 호주에서는 Hassel이 Bligh Tanner와 Wagners와 공동으로 설계한 퀸즐랜드 대학의 지구 변동 실험실(GCI)이 구조 목적으로 지오폴리머 콘크리트를 사용한 세계 최초의 건물입니다.

게다가, 건축물 건설에 있어서의 지오폴리머의 사용량 증가에 따라, 지오폴리머 콘크리트를 사용하는 이점에 대해서, 일반 시민이나 정부의 사이에서 인식이 높아지고 있습니다. 이는 투움바 웰캠프 공항과 관련이 있으며, 이 공항에서는 지오폴리머 콘크리트가 대부분 사용되었습니다.

전체적으로 건축물 건설에서 지오폴리머의 사용은 증가하고 있습니다. 지오폴리머에는 많은 이점이 있기 때문입니다.

아시아태평양시장을 독점하는 중국

아시아태평양에서는 건설 활동의 활성화와 건축자재 수요 증가에 의해 중국이 세계 시장 점유율을 독점하고 있습니다.

팬데믹 시기의 손실을 회복하기 위해 경제 성장을 가속시키기 위해 중국의 재정 및 국가개발성은 2022년 3분기에 인프라 지출을 촉진하는 것을 목적으로 한 국가인프라기금의 설립에 5,000억 위안(718억 6,000만 달러)을 투자할 계획입니다.

게다가 국내 제4위의 국제 허브 공항인 청두 텐후 국제 공항에의 접속성을 향상시키기 위해, 30개의 공항의 확대에 임하고 있습니다.

CAAC에 따르면 중국의 1차 3차 5개년 계획에는 2020년 빈곤 완화를 위해 저소득 지역에서 항공 운송 서비스를 확대하는 것이 포함되어 있습니다. 이 나라는 2025년까지 향후 5년간, 초고압 에너지 프로젝트, 빅 데이터 센터, 고속철도, 도시간 선로 및 역, 5G 기지국, 전기차 충전 스테이션, 그 외 다양한 주요 건설 프로젝트에 1조 4,300억 달러를 투자합니다.

국가개발개혁위원회(NDRC)에 따르면, 상하이의 계획에는 향후 3년간 387억 달러의 투자가 포함되어 있습니다.

또한 2025년까지 향후 5년간 5G 기지국을 현재의 25배에 해당하는 500만국 건설하는 것을 목표로 하고 있습니다. 이러한 대규모 인프라 개발 프로젝트가 중국의 지오폴리머 수요를 끌어올리고 있습니다.

이 나라는 2020년에 시작된 도로 프로젝트에도 임하고 있으며, 이를 위해 16억 1,000만 달러를 투자하는 광남 나사와 하후흥걸, 18억 6,000만 달러를 투자하는 청강과 화닝, 15억 4,000만 달러를 투자하는 클라우드 남성의 위북과 연산과 같은 도시간의 고속도로 건설이 포함되어 2023년의 완성이 전망되고 있습니다.

게다가 구이저우성의 Nayong과 Qinglong, Liuzzii와 Anlong을 연결하는 86억 8,000만 달러를 투자하는 2개의 새로운 고속도로 프로젝트의 건설은 중국 지오폴리머 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

이로 인해 이 나라의 주택 건설이 증가해, 나아가 이 나라의 지오폴리머 시장에 플러스의 효과를 가져올 것으로 예상됩니다.

ㅍ지오폴리머 산업 개요

지오폴리머 시장은 매우 세분화되어 있습니다. 지오폴리머 시장의 주요 기업은 Wagners, Geopolymer Solutons LLC, SLB, ClockSpring|NRI, CEMEX SAB de CV 등입니다(순부동).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

시멘트 산업에 대한 환경 규제 및 배출 변형

보수 및 복구 시장 수요 증가

성장 억제요인

통일규격과 규제의 부족

COVID-19의 발생에 의한 불리한 상황

산업의 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

제품 유형별

시멘트, 콘크리트 및 프리캐스트 패널

그라우트 및 바인더

기타

용도별

건축

도로 및 포장

활주로

파이프 및 콘크리트 보수

교량

터널 라이닝

철도 침목

코팅 시공

내화 피복

핵 및 기타 유해폐기물의 고정화

특정 금형 제품

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

기타

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Banah UK Ltd

CEMEX SAB de CV

Ceskych Lupkovych Zavodech AS

ClockSpring|NRI

Geopolymer Solutions LLC

IPR

Murray & Roberts

PCI Augsburg GMBH

Rocla Pty Limited

Schlumberger Limited

Wagners

Zeobond Pty Ltd

제7장 시장 기회 및 향후 동향

지오폴리머 제품의 이점에 관한 소비자 의식 증가

AJY

영문 목차

영문목차

The Geopolymer Market size is estimated at USD 19.09 billion in 2025, and is expected to reach USD 69.04 billion by 2030, at a CAGR of 29.32% during the forecast period (2025-2030).

The introduction of COVID-19 had a negative influence on the geopolymer business. The construction industry was one of the hardest hit, with ongoing projects halted and all new projects postponed due to a shortage of workers and government-imposed rigorous standards aimed at preventing the spread of the disease by the year 2020. However, the market is projected to grow steadily, owing to increased building and construction activities in 2021.

Key Highlights

Over the short term, environmental regulations and emission strain on the cement industry and higher demand from the repair and rehabilitation market are major factors driving the growth of the market studied.

But the lack of uniform rules and standards is one of the main things that is expected to slow the growth of the target industry during the forecast period.

Still, consumers are becoming more aware of the benefits of geopolymer products, which is likely to lead to growth opportunities for the global market in the near future.

With rising construction activity in the region, Asia-Pacific dominated the global market.

Geopolymer Market Trends

Building Segment to Dominate the Market

The use of geopolymers in building construction has a vital role. Due to the rapidly growing construction activities and the overgrowing population across the world, large amounts of greenhouse gases are being emitted into the atmosphere, causing a huge environmental impact. With the increasing impact of greenhouse gases on the environment emitted either during cement manufacturing or in other alternate ways, the overall construction of building materials has created scope for the development and use of geopolymers in building construction.

It has been noted that the building and construction sector has experienced rapid growth in the past few years. According to the World Bank, the value of the global construction industry reached USD 22.36 trillion in 2020 and registered growth compared to USD 27.18 trillion in 2021.

The development of green technology in the construction industry dates back years. The increase in environmental awareness in recent years around the world has led to a positive assessment of the environmental impact of building materials in addition to their technical properties.

Several types of geopolymer materials, such as geopolymer concrete, geopolymer cement, binders, geopolymer bricks, panels, and many others, are being used during building construction, owing to their versatile properties in reducing greenhouse emissions as well as energy savings.

One of the recent applications of geopolymers in the building is cited as the first ever pile constructed in London, dated January 2021, using one of the leading geopolymer manufacturers, Wagner's Earth Friendly Concrete (EFC), by working with two leading UK firms, Keltbray Group and Capital Concrete.

Additionally, in Australia, the University of Queensland's Global Change Institute (GCI), designed by Hassell in conjunction with Bligh Tanner and Wagners, is the world's first building to use geopolymer concrete for structural purposes.

Moreover, with such growing usage of geopolymers in building construction, awareness has been growing among the public and governments over the advantages of using geopolymer concrete, and this can be related to Toowoomba Wellcamp Airport, in which mostly geopolymer concrete was used; approximately 23.000 m3 were used.

Overall, the use of geopolymers in building construction has been growing. This is because geopolymers have a lot of benefits.

China to Dominate the Asia-Pacific Market

In the Asia-Pacific region, China dominated the global market share with growing construction activities and increasing demand for construction materials.

To fasten up its economic growth to recover the losses during the pandemic period, China's Ministry of Finance and National Development has planned to invest CNY 500 billion (USD 71.86 billion) in building up a state infrastructure fund in the third quarter of 2022, aimed at promoting infrastructure spending.

Additionally, the country is working on the expansion of 30 airports to improve the connectivity to the country's fourth largest international hub Chengdu Tianfu International Airport.

According to CAAC, China's 13th five-year plan include the expansion of air transportation services in low-income areas for poverty alleviation in 2020. The country is investing USD 1.43 trillion in the next five year till 2025, in major construction projects which includes ultra-high voltage energy projects, big data centers, high-speed railway, and intercity tracks & stations, 5G base stations, electric vehicle charging station, and various others.

According to National Development and Reform Commission (NDRC), Shanghai plan includes the investment of USD 38.7 billion in the next three years, whereas Guangzhou has signed 16 new infrastructure projects with and investment of USD 8.09 billion.

Additionally, the country is targeting to build five million 5G base stations in the next five years till 2025, a growth of 25 times from the current number of 5G base stations. These massive infrastructure development projects in the country are propelling the demand for geopolymers in China.

The country is also working on road projects initiated in 2020 which include the construction of an expressway between the cities such as Guangnan Nasa and Xiahou Xingjie with an investment of USD 1.61 billion, Chengjiang and Huaning with an investment of USD 1.86 billion, and Quibei and Yanshan in Yunan province with an investment of USD 1.54 billion which are estimated to get completed in 2023.

Additionally, the construction of two new highway projects connecting Nayong with Qinglong, andLiuzzii with Anlong in Guizhou Province with and investment of USD 8.68 billion is expected to positively impact the geopolymers market in China.

Thereby, increasing the residential construction in the country which in turn will have a positive effect on the geopolymers market in the country.

Geopolymer Industry Overview

The geopolymer market is highly fragmented in nature. The major players in the geopolymers market are Wagners, Geopolymer Solutons LLC, SLB, ClockSpring|NRI, and CEMEX S.A.B. de C.V., among others (not in particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Environmental Regulations and Emission Strain on the Cement Industry

4.1.2 Higher Demand from the Repair and Rehabilitation Market

4.2 Restraints

4.2.1 Lack of Uniform Standards and Regulations

4.2.2 Unfavorable Conditions Arising Due to the COVID-19 Outbreak

4.3 Industry Value-chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Product Type

5.1.1 Cement, Concrete, and Precast Panel

5.1.2 Grout and Binder

5.1.3 Other Product Types

5.2 Application

5.2.1 Building

5.2.2 Road and Pavement

5.2.3 Runway

5.2.4 Pipe and Concrete Repair

5.2.5 Bridge

5.2.6 Tunnel Lining

5.2.7 Railroad Sleeper

5.2.8 Coating Application

5.2.9 Fireproofing

5.2.10 Nuclear and Other Toxic Waste Immobilization

5.2.11 Specific Mold Products

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Banah UK Ltd

6.4.2 CEMEX SAB de CV

6.4.3 Ceskych Lupkovych Zavodech AS

6.4.4 ClockSpring|NRI

6.4.5 Geopolymer Solutions LLC

6.4.6 IPR

6.4.7 Murray & Roberts

6.4.8 PCI Augsburg GMBH

6.4.9 Rocla Pty Limited

6.4.10 Schlumberger Limited

6.4.11 Wagners

6.4.12 Zeobond Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Consumer Awareness Regarding Benefits of Geopolymer Products