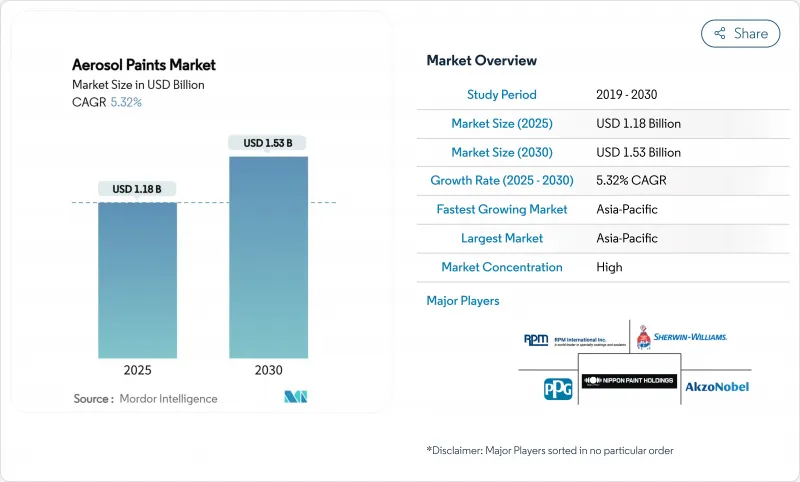

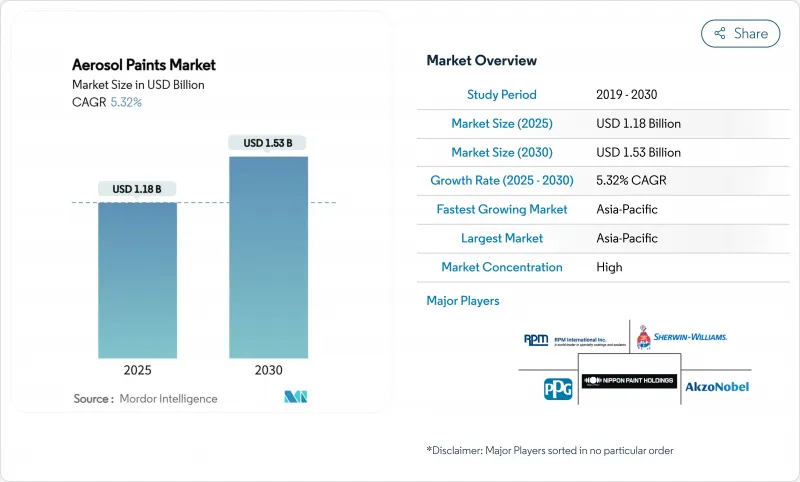

에어로졸 페인트 시장 규모는 2025년에 11억 8,000만 달러, 2030년에는 15억 3,000만 달러에 이를 것으로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.32%를 나타낼 전망입니다.

건설업 회복, 자동차 개인화, DIY 문화의 융성이 판매량 증가를 뒷받침하는 한편, 지속적인 수지 기술 혁신과 자동 디스펜서 시스템이 프리미엄 가격을 지원하고 있습니다. 제조업체는 마무리 품질을 희생하지 않고도 엄격한 VOC 규제를 충족하기 위해 수성으로의 전환을 가속화하고 특수 2-K 폴리 우레탄 시스템은 부스가 필요 없는 보수용으로 지지를 모으고 있습니다. 경쟁의 치열성은 기술 통합, 지속가능성 증명, 지역 실적을 확대하고 이익률이 높은 틈새 시장에 대한 액세스를 뒷받침하는 목표를 좁힌 M&A를 축으로 합니다.

신축 주택 및 개축 프로젝트에서 정밀 터치 업 코팅이 지정되어 에어로졸 페인트 시장이 초기 건설 단계와 유지 보수 단계 모두에 침투함에 따라 수요가 가속화되고 있습니다. 계약자는 거주 공간의 색조, 다운 타임 및 오버 스프레이를 줄이기 위해 에어로졸을 선호합니다. 제조업체 각사는 급속 경화와 내마모성을 겸비한 기재별 블렌드로 대응해, 석재, 복합재, 금속 건구에 일관한 성능을 보증하고 있습니다. 지역 간 규제 조정은 제품 승인을 간소화하고, 통일 라벨 표준을 추진하며, 국경을 넘는 프로젝트의 실행을 더욱 용이하게 합니다.

규칙 1151의 개정은 VOC의 일시적인 완화를 허용하고 고성능 재 마무리 에어로졸의 지속적인 공급을 허용합니다. 코베스트로의 클리어 코트의 벤치마크는 나노변성 2-K 폴리우레탄의 내스크래치성을 입증합니다. 북미와 유럽에서는 매니아가 휠, 캘리퍼스, 트림을 맞춤화하고 있기 때문에 자동차 판매가 정체되었음에도 불구하고 에어로졸 판매량은 안정적입니다. 신흥 시장에서는 개인화가 사회적 스테이터스를 나타내고, 열대 기후에 맞춘 지역 특유의 컬러 팔레트나 자외선에 안정된 배합이 성장하고 있습니다. OEM은 페인트 제조업체와 협력하여 딜러 인증 에어로졸 터치 업 키트를 출시하여 보증 범위를 보호하고 애프터마켓 수익을 얻습니다.

캘리포니아의 2023-2031년 규칙은 허용 VOC 수준을 줄이고 방향족 용매를 금지하므로 비용이 많이 드는 재제조가 필요합니다. 미국 환경보호청(EPA)은 2027년 1월까지 준수를 연기했으나 업계의 테스트 사이클은 여전히 압축된 상태로 남아 있습니다. 캐나다의 2024년 규제는 130개 제품 및 관할마다 다른 SKU가 필요합니다. 블렌딩을 변경하면 원료의 복잡성이 증가하고 특히 콜드 스프레이 환경에서는 광택과 커버력이 저하될 수 있습니다. 그러나 첨단 수성 화학을 신속하게 활용하는 기업은 성능 동등성이 달성되면 세계 배치의 효율화를 기대하고 있습니다.

2024년 에어로졸 페인트 시장에서는 아크릴계 배합제가 32.87%의 점유율을 차지했고, 2030년까지의 CAGR은 5.57%를 나타낼 전망입니다. 접착력, UV 안정성, 낮은 VOC 적합성의 균형은 건축 및 DIY 분야에서 널리 받아 들여집니다. 폴리우레탄은 2액 에어로졸 키트가 공장 수준의 내구성을 제공하는 자동차와 산업 분야에서 프리미엄 지위를 획득하고 있습니다. 에폭시계는 성장이 둔화되었음에도 불구하고 중방식에 필수적이며, 알키드계는 전통적인 마무리를 선호하는 장인들 사이에서 틈새 충성심을 유지하고 있습니다. 기타 '범주에 속하는 하이브리드 나노 강화 수지는 적외선 반사율이나 경화 촉진 등의 목표 달성을 약속하고 공급자를 커스텀 오더를 합리화하는 모듈식 배합 플랫폼으로 향하게 합니다.

아크릴 수지 공급업체는 규제 당국의 감시에 대응하기 위해 물에 의한 정리를 수반하는 용매 경도를 제공하는 자기 가교형 에멀젼에 투자하여 환경 갭을 줄이고 있습니다. 모노머 백본을 공유하면 에어로졸과 벌크 스프레이 형식을 신속하게 전환하고 스케일 이점을 향상시킬 수 있습니다. DIY 사용자가 전체 표면 제품을 요구하는 동안 플라스틱, 금속, 석재에 적합한 다 기재 아크릴이 각광을 받고 있습니다. 동시에, 폴리우레탄 개발자는 활성화 후 냄비 수명을 연장하기 위한 대기 시간 관리를 위해 노력하고 있으며, 원격지에서 활동하는 차량 유지 보수 작업자들에게 촉구를 펼치고 있습니다.

에어로졸 페인트 보고서는 수지별(아크릴 수지, 에폭시 수지, 폴리우레탄 수지, 알키드 수지, 기타 수지), 기술별(용제형, 수성형), 최종 사용자 산업별(자동차, 건축, 목재·포장, 운송, DIY, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 기타)로 분류되고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년에 45.42%의 세계 점유율을 차지했으며 CAGR 5.71%를 나타낼 전망입니다. 중국의 메가 프로젝트가 건축 수요를 지지하는 한편, 인도의 중류 가정이 DIY용 메탈릭이나 파스텔조의 성장에 박차를 가합니다. 일본 페인트에 의한 23억 달러의 AOC 인수와 인도 진출은 이 지역에서 전략적 정착을 보여줍니다. 정부의 인프라 정비는 순환적인 소비 침체기에 안정적인 판매 파이프라인을 제공합니다.

북미는 DIY 문화가 정착하고 있기 때문에 브랜드품이나 프라이빗 브랜드품에 안정적인 현금흐름을 창출하고 있습니다. 인플레이션은 엄청난 리폼에 무겁게 걸려 있지만, 소규모 인테리어의 리모델링은 계속 견조합니다.

유럽 시장은 시험 방법을 표준화하고 수성화에 대한 모범 사례를 공유하는 컴플라이언스 컨소시엄을 통해 기술적 리더십을 키우고 있습니다. 공적 자금은 낮은 GWP 추진제를 사용하는 시험 프로젝트를 장려하고 소비자 에코 라벨은 구매 선택에 달려 있습니다. 지정학적 혼란에 따른 공급망의 회복력 강화책을 통해 제조업체는 주요 원재료를 니어 쇼어화하고 비용 구조와 지역의 생산 능력 배분을 미묘하게 재구성합니다.

The Aerosol Paints Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

Construction recovery, automotive personalization, and a flourishing DIY culture fuel volume growth, while continuous resin innovation and automated dispensing systems support premium pricing. Manufacturers accelerate water-borne transitions to meet stricter VOC rules without sacrificing finish quality, and specialty 2-K polyurethane systems gain traction for booth-free repairs. Competitive intensity pivots around technology integration, sustainability credentials, and targeted mergers and acquisitions that broaden geographic footprints and boost access to high-margin niches.

Demand accelerates as new housing and renovation projects specify precision touch-up coatings, allowing the aerosol paints market to penetrate both initial build and maintenance phases. Contractors favor aerosols for color-matching occupied spaces, reducing downtime and overspray. Manufacturers respond with substrate-specific blends that combine rapid cure with abrasion resistance, ensuring consistent performance across masonry, composites, and metal fixtures. Regulatory alignment across regions is streamlining product approvals and driving uniform label standards that further ease cross-border project execution.

Rule 1151 amendments grant temporary VOC leniency, enabling continued supply of high-performance refinishing aerosols. Covestro's clearcoat benchmarking validates nano-modified 2-K polyurethane dominance in scratch resistance. Enthusiasts in North America and Europe customize wheels, calipers, and trim, driving steady aerosol volumes despite plateauing vehicle sales. In emerging markets, personalization indicates social status, fostering localized color palettes and UV-stable formulations tailored to tropical climates. OEMs collaborate with paint suppliers to launch dealer-approved aerosol touch-up kits that protect warranty coverage and capture aftermarket revenue.

California's 2023-2031 rules cut allowable VOC levels and ban aromatic solvents, compelling costly reformulations. The U.S. EPA deferred compliance to January 2027, yet industry testing cycles remain compressed. Canada's 2024 limits span 130 products, requiring distinct SKUs per jurisdiction. Reformulation increases raw-material complexity and may reduce gloss or coverage, particularly in cold-spray environments. However, early movers leveraging advanced water-borne chemistries anticipate global rollout efficiencies once performance parity is achieved.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acrylic formulations held the leading 32.87% share of the aerosol paints market in 2024, with a parallel 5.57% CAGR to 2030. Their balance of adhesion, UV stability, and low-VOC adaptability underpins widespread acceptance across architectural and DIY channels. Polyurethane earns premium positioning in automotive and industrial sectors, where two-component aerosol kits deliver factory-grade durability. Epoxy systems remain essential for heavy-duty anticorrosion protection despite slower growth, while alkyd retains niche loyalty among craftsmen who favor traditional finishes. Hybrid nano-enhanced resins in the "other" category promise targeted gains such as infrared reflectivity and accelerated cure, nudging suppliers toward modular formulation platforms that streamline custom orders.

In response to regulatory scrutiny, acrylic suppliers invest in self-crosslinking emulsions that deliver solvent-borne hardness with water clean-up, shrinking the environmental gap. Shared monomer backbones allow rapid pivoting between aerosol and bulk-spray formats, improving economies of scale. As DIY users demand all-surface products, multi-substrate acrylics compatible with plastics, metals, and masonry gain prominence. Concurrently, polyurethane developers tackle latency management to extend post-activation pot life, broadening appeal to fleet maintenance crews operating in remote locations.

The Aerosol Paints Report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Alkyd, and Other Resins), Technology (Solvent-Borne, Water-Borne), End-User Industry (Automotive, Architectural, Wood and Packaging, Transportation, Do-It-Yourself (DIY), and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 45.42% global share in 2024 and advances at 5.71% CAGR. China's mega-projects sustain architectural demand, while India's middle-class households spur growth in DIY metallic and pastel shades. Nippon Paint's USD 2.3 billion AOC acquisition and Indian expansions illustrate strategic anchoring in the region. Government infrastructure outlays infuse stable volume pipelines even during cyclical consumer dips.

North America benefits from an entrenched DIY culture, generating steady cash flow for branded lines and private labels alike. Although inflation weighs on big-ticket remodeling, smaller decor touch-ups remain resilient.

Europe's market fosters technology leadership through collaborative compliance consortia that standardize test methods and share best practices on water-borne conversion. Public funding incentivizes pilot projects employing low-GWP propellants, while consumer eco-labels sway purchase choices. Supply-chain resilience exercises following geopolitical disruptions push manufacturers to near-shore key raw materials, subtly reshaping cost structures and regional capacity allocation.