ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

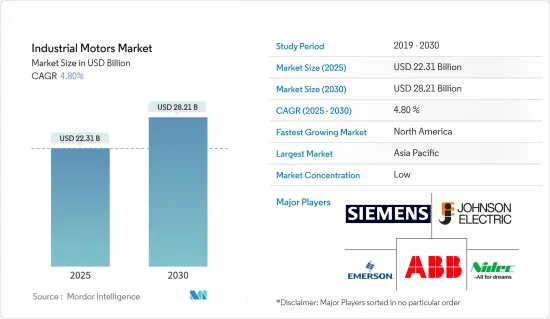

산업용 모터 시장 규모는 2025년에 223억 1,000만 달러로 추계되고, 2030년에는 282억 1,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 4.8%를 나타낼 전망입니다.

산업용 모터는 산업 환경에서 다양한 작업을 수행하기 위해 전기 에너지를 기계 에너지로 변환하는 전기 기계입니다. 산업용 모터는 제조, 석유 및 가스, 건설, 운송 등에 사용되는 다양한 장비와 기계에 동력과 움직임을 제공하도록 설계되었습니다.

주요 하이라이트

모터는 산업 생산을 주도합니다. 모터 모니터링, 정렬, 테스트 및 연결의 혁신적인 방법으로 시간과 비용을 절약하고 안전성을 강화합니다.

전 세계적으로 에너지 효율과 지속 가능성을 추구하는 추세에 따라 제조업체들은 에너지 효율이 높은 모터를 점점 더 많이 선택하고 있습니다.

전 세계적인 산업화로 인해 에너지 효율이 높은 모터에 대한 수요가 증가하고 있습니다. 산업이 발전하고 확장됨에 따라 에너지 소비와 운영 비용을 줄이는 모터의 필요성이 가장 중요해졌습니다. 이러한 에너지 효율적인 모터는 효율성을 높이고 에너지 손실을 최소화하여 시간이 지남에 따라 상당한 비용 절감 효과를 가져옵니다.

자동화 시스템은 제조, 엔지니어링, 건설, 발전 분야에서 중추적인 역할을 하며 효율성과 생산성 향상을 주도합니다. 산업 자동화는 인공지능(AI), 클라우드 컴퓨팅, 빅 데이터, 사물인터넷(IoT)에 힘입어 급속도로 발전하고 있습니다.

이러한 장점에도 불구하고 에너지 효율적인 모터의 광범위한 채택을 방해하는 몇 가지 과제가 있습니다. 근본적인 한계로는 에너지, 유지보수, 초기 구매 비용 등 관련 비용이 있습니다. 또한 에너지 효율적인 모터를 생산하려면 우수한 소재, 첨단 제조 기술, 엄격한 테스트 및 인증이 필요합니다. 이러한 요구 사항은 제조업체의 생산 비용을 증가시켜 소비자 가격 상승으로 이어질 수 있습니다.

산업용 모터 시장 동향

석유 및 가스 부문의 성장 전망

석유 및 가스 부문은 시추, 추출, 정제, 운송 등 다양한 공정에 동력을 공급하기 위한 산업용 모터의 필요성으로 인해 현재 시장을 주도하고 있습니다.

펌프, 압축기 및 터빈에 AC 유도 모터가 많이 사용되고 시추 현장에서 정유 공장으로 석유 및 가스를 추출, 처리 및 운송하여 소비자에게 판매하는 데 적용되기 때문에 석유 및 가스 산업에서 이러한 모터가 유행할 것으로 예상됩니다. 또한 저전압 유도 모터는 정유 공장에서 구동 펌프, 압축기 및 교반기용으로 사용되어 원유를 가솔린, 디젤 및 제트 연료와 같은 여러 제품으로 변환합니다.

개발도상국의 급속한 도시화는 에너지 수요의 상당한 증가를 수반합니다. 결과적으로 액체 연료와 천연가스의 소비가 증가합니다.

석유 및 가스 수요가 증가함에 따라 E&P 기계, 장비 및 부품 시장도 성장하고 있습니다.

Baker Hughes사에 따르면 북미는 전 세계적으로 석유 및 가스 굴착 장치를 가장 많이 보유하고 있습니다.

북미가 상당한 시장 점유율을 차지할 것으로 예상

산업용 모터 시장은 주로 미국 내에서 인더스트리 4.0에 대한 산업계의 관심이 높아짐에 따라 주도되고 있습니다. 산업 자동화는 제조업체가 보다 효과적인 제품을 생산하도록 장려하며, 예측 기간 내내 견고한 성장이 예상됩니다.

산업계와 소비자들이 에너지 소비를 줄이고 탄소 발자국을 최소화하기 위해 노력함에 따라 에너지 효율적인 솔루션에 대한 수요가 증가하고 있습니다. 산업용 전기 모터는 기존 모터보다 효율이 높고 에너지 손실이 적은 것으로 알려져 있습니다.

석유 및 가스는 시추 장비를 사용하여 저류층에서 원유와 천연가스를 추출하기 위해 시추 작업을 수행하는 산업입니다. 전기 모터는 시추 장비의 일반적인 동력원입니다. 베이커 휴즈에 따르면 북미는 석유 및 가스 굴착 장비 보유에서 세계를 선도하고 있습니다. 2024년 8월 현재 이 지역에는 781개의 육상 굴착 장치와 23개의 해상 굴착 장치가 있습니다.

캐나다는 비효율적인 모터를 시장에서 퇴출하기 위해 에너지 효율 규정을 시행하고 있습니다. 캐나다의 기업들은 이 성능 표준을 통해 NEMA MG-1에서 제공하는 모터 효율에 대한 지침을 이용할 수 있습니다.

캐나다 정부는 신규 투자에 대한 세금 감면, 여러 국가와의 다양한 무역 협정, 신기술에 대한 투자, 다양한 기술 교육 프로그램 등 캐나다의 제조업 부문을 육성하기 위한 여러 전략을 시행하고 있습니다. 캐나다 정부는 또한 현지 기업과 기업가들이 성공에 필요한 도구를 갖출 수 있도록 투자해 왔습니다.

예를 들어, 2024년 7월 Hitachi Energy Canada는 캐나다 정부로부터 3,000만 캐나다 달러(2,154만 달러)의 자금을 확보했습니다. 이 자금은 몬트리올에 새로운 HVDC 시뮬레이션 센터를 설립하고 바렌느에 있는 전력 변압기 공장을 현대화하는 데 사용될 것입니다. 이러한 이니셔티브는 지속 가능한 에너지에 대한 북미의 급증하는 수요를 충족하는 것을 목표로 합니다.

산업용 모터 시장 개요

경쟁의 정도는 브랜드 정체성, 강력한 경쟁 전략 및 투명성 정도와 같이 시장에 영향을 미치는 다양한 요인에 따라 달라집니다.

산업용 모터 시장에는 ABB, Emerson Electric Co., Nidec Industrial Solutions, Johnson Electric Holdings Limited, Siemens AG사 등, 다양한 저명 기업이 참가하고 있습니다. 회사와 관련된 브랜드 아이덴티티는이 시장에서 큰 영향을 미칩니다. 강력한 브랜드는 좋은 성과와 동의어이기 때문에 오랜 역사를 가진 기업이 우위를 점할 것으로 예상됩니다.

혁신을 통한 지속 가능한 경쟁 우위가 상당히 높은 시장에서 광업, 석유 및 가스, 에너지와 같은 최종 사용자 산업의 신규 고객 수요가 급증할 것으로 예상되는 점을 고려하면 경쟁은 더욱 치열해질 것입니다. 기존 대기업의 존재로 인해 시장 침투 수준도 높습니다.

시장 침투력과 고급 제품을 제공할 수 있는 능력으로 인해 경쟁이 계속 치열할 것으로 예상됩니다. 시장은 다양한 업체로 구성되어 있지만, 높은 기준과 우수한 품질로 시장에서 두각을 나타내고 있는 업체는 소수에 불과합니다.

통합 기술 발전과 지정학적 시나리오가 증가함에 따라 연구된 시장은 변동을 목격하고 있습니다. 이 외에도 주요 업계 기업은 수익에서 비롯되는 투자 능력을 고려하여 원자재 공급 업체를 계열사에 의존합니다.

혁신 수준, 시장 출시 기간 및 성과는 연구 대상 시장에서 기업이 자신을 차별화하는 주요 용어입니다.

전반적으로 연구 된 시장에서 경쟁 경쟁의 강도는 증가하고 있으며 산업의 성장으로 인해 예측 기간 동안 높을 것으로 예상됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

COVID-19의 영향과 기타 거시 경제 요인이 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

정부 규제로 인한 에너지 효율에 대한 수요

스마트 모터로의 성장하는 변화

시장의 과제

휴대성 문제

신규 장비 조달 및 기존 장비 업그레이드를 위한 높은 초기 투자 비용

제6장 시장 세분화

모터 유형별

교류(AC) 모터

직류(DC) 모터

기타 모터(EC 모터)

전압별

고전압

중전압

저전압

최종 사용자별

석유 및 가스

발전

광업 및 금속

상하수도 관리

화학 및 석유 화학

이산 제조

기타 최종 사용자

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

ABB Ltd.

Emerson Electric Co.

Siemens AG

Nidec Industrial Solutions

Johnson Electric Holdings Limited

Arc Systems Inc.

Ametek Inc.

Toshiba Electronic Devices and Storage Corporation

Wolong Industrial Motors

Allen-Bradly Co. LLC(Rockwell Automation Inc.)

Maxon Motor AG

Franklin Electric Co. Inc.

Fuji Electric Co. Ltd

ATB Austria Antriebstechnik AG

Menzel Elektromotoren GmbH

제8장 투자 분석

제9장 시장의 미래

HBR

영문 목차

영문목차

The Industrial Motors Market size is estimated at USD 22.31 billion in 2025, and is expected to reach USD 28.21 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

An industrial motor is an electrical machine that converts electrical energy into mechanical energy to perform various tasks in industrial settings. Industrial motors are designed to provide power and motion to different equipment and machinery used in manufacturing, oil and gas, construction, transportation, etc. These motors are typically more robust and powerful than motors used in residential or commercial applications, as they need to withstand heavy loads and operate in demanding environments.

Key Highlights

Motors drive industrial production. Innovative methods in motor monitoring, alignment, testing, and connections save time and costs and enhance safety. Concurrently, energy-saving motors and intelligent drives elevate efficiency and performance and simplify troubleshooting.

With a global push towards energy efficiency and sustainability, manufacturers are increasingly opting for energy-efficient motors. These choices aim to reduce energy consumption and operating costs, with IE4 efficiency motors standing out for their significant energy savings over older models.

Global industrialization has heightened the demand for energy-efficient motors. As industries establish and expand, the need for motors that curtail energy consumption and operating costs becomes paramount. These energy-efficient motors enhance efficiency and minimize energy loss, leading to notable cost savings over time. This growing demand spans multiple sectors, including manufacturing, agriculture, construction, and transportation.

Automation systems are pivotal for manufacturing, engineering, construction, and power generation, driving enhanced efficiency and productivity. Industrial automation is witnessing rapid advancements fueled by artificial intelligence (AI), cloud computing, Big Data, and the Internet of Things (IoT).

Despite the advantages, several challenges hinder the widespread adoption of energy-efficient motors. Fundamental limitations include the associated costs: energy, maintenance, and initial purchase. Furthermore, producing energy-efficient motors demands superior materials, advanced manufacturing techniques, and rigorous testing and certification. These requirements can inflate production costs for manufacturers, leading to higher consumer prices.

Industrial Motors Market Trends

The Oil and Gas Segment is Expected to Witness Growth

The oil and gas sector is currently leading the market due to its need for industrial motors to power a range of processes, including drilling, extraction, refining, and transportation. Due to increasing awareness of climate change and the necessity of decreasing CO2 emissions, the oil and gas industry is progressively acknowledging the significance of energy-efficient motors.

Due to the significant use of AC induction motors in pumps, compressors, and turbines, as well as their application for extraction, processing, and transport of oil and gas from drilling sites into refineries, which are sold to consumers, it is estimated that these motors will be trendy within the oil and gas industry. In addition, low-voltage induction motors are used in refineries for drive pumps, compressors, and agitators to convert crude oil into multiple products such as gasoline, diesel, and jet fuel.

Rapid urbanization in developing nations accompanies a considerable increase in energy demand. Consequently, the consumption of liquid fuels and natural gas rises. For instance, according to BP, natural gas production amounted to 4.08 trillion cubic meters in 2023. The escalating global need for electricity and fuel has increased the demand for oil and natural gas.

With rising oil and gas demand, the market for E&P machines, equipment, and components is growing. As a result, the need for AC motors used in different capacities within the downstream and upstream segments of the oil and gas industry is also increasing.

According to Baker Hughes, North America hosts oil and gas rigs globally. As of August 2024, the region boasted 781 land rigs and 23 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

North America is Expected to Hold Significant Market Share

Industrial motor markets are mainly driven by the increasing focus of industries on Industry 4.0 within the United States. Industrial automation encourages manufacturers to produce more effective products, with solid growth expected throughout the projection period. This pattern would result in a desire to develop new industrial motor machines. The spread of industrial automation across all sectors is expected to be evenly distributed. Consequently, to cope with industrial automation's growth, the market for industrial motors is predicted to develop in the United States.

As industries and consumers seek to reduce energy consumption and minimize their carbon footprint, there is a growing demand for energy-efficient solutions. Industrial electric motors are known for their higher efficiency and lower energy losses than traditional motors.

Oil and gas is an industry in which drilling operations are carried out to extract crude oil and natural gas from reservoirs using drilling rigs. Electric motors are a common source of power for drilling equipment. According to Baker Hughes, North America leads the world in hosting oil and gas rigs. As of August 2024, the region boasted 781 land rigs and an additional 23 offshore. By the end of 2023, the United States had 500 active rotary oil rigs and 120 gas rigs, contributing to a total rotary rig count of 622.

Canada has implemented energy efficiency regulations to remove inefficient motors from the market. The guidelines for motor efficiency, provided by NEMA MG-1, are available to Canada's businesses through these performance standards. These regulations cover three-phase induction motors with power between 1 and 500 horsepower. These performance standards cover most motors used in manufacturing and industrial applications. Compliance with these energy standards is mandatory for business owners.

The Government has taken several initiatives to foster Canada's manufacturing sector, including tax reductions on new investments, various trade agreements with different countries, investment in new technologies, and many skill training programs. The Canadian Government has also invested in local companies and entrepreneurs to ensure they have the tools necessary for success.

For instance, in July 2024, Hitachi Energy Canada secured CAD 30 million (USD 21.54 million) in funding from the Government of Canada. This funding will help set up a new HVDC simulation center in Montreal and modernize the power transformer factory in Varennes. These initiatives aim to meet North America's surging demand for sustainable energy.

Industrial Motors Market Overview

The degree of competition depends on various factors affecting the market, such as brand identity, powerful competitive strategy, and degree of transparency.

The industrial motors market comprises various prominent players such as ABB Ltd., Emerson Electric Co., Nidec Industrial Solutions, Johnson Electric Holdings Limited, and Siemens AG, among others. The brand identity associated with the companies has a major influence in this market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand.

In a market where the sustainable competitive advantage through innovation is considerably high, the competition is only going to increase, considering the anticipated surge in demand from new customers from the end-user industries like mining, oil and gas, energy. With the presence of large market incumbents, market penetration levels are also high

Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high. Although the market comprises various players, only a handful are prominent in the market for their high standards and excellent quality.

With the growing consolidation technological advancement, and geopolitical scenarios, the studied market has been witnessing fluctuation. In addition to this, the major industry player depends on their affiliates for raw materials vendors, considering their ability to invest, which result from their revenues.

The level of innovation, time-to-market, and performance are the key terms by which the players differentiate themselves in the market studied.

Overall, the intensity of the competitive rivalry in the studied market is growing and expected to be high during the forecast period owing to the growth of the industry.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Demand for Energy Efficiency Owing to Government Regulations

5.1.2 Growing Shift towards Smart Motors

5.2 Market Challenges

5.2.1 Portability Issues

5.2.2 High Initial Investment for Procuring New Equipment and Upgrading Existing Equipment

6 MARKET SEGMENTATION

6.1 By Type of Motor

6.1.1 Alternating Current (AC) Motors

6.1.2 Direct Current (DC) Motor

6.1.3 Other Types of Motors (Servo and Electronically Commutated Motors (EC))

6.2 By Voltage

6.2.1 High Voltage

6.2.2 Medium Voltage

6.2.3 Low Voltage

6.3 By End User

6.3.1 Oil & Gas

6.3.2 Power Generation

6.3.3 Mining & Metals

6.3.4 Water & Wastewater Management

6.3.5 Chemicals & Petrochemicals

6.3.6 Discrete Manufacturing

6.3.7 Other End Users

6.4 By Geography

6.4.1 North America

6.4.2 Europe

6.4.3 Asia

6.4.4 Australia and New Zealand

6.4.5 Latin America

6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 ABB Ltd.

7.1.2 Emerson Electric Co.

7.1.3 Siemens AG

7.1.4 Nidec Industrial Solutions

7.1.5 Johnson Electric Holdings Limited

7.1.6 Arc Systems Inc.

7.1.7 Ametek Inc.

7.1.8 Toshiba Electronic Devices and Storage Corporation

7.1.9 Wolong Industrial Motors

7.1.10 Allen - Bradly Co. LLC (Rockwell Automation Inc.)