Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1686643

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

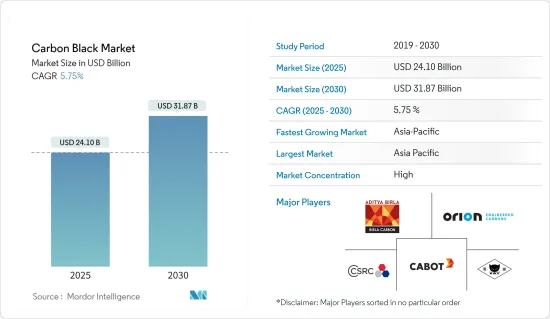

카본블랙 시장 규모는 2025년에 241억 달러로 추계되고, 2030년에는 318억 7,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 5.75%를 나타낼 전망입니다.

시장은 2020년의 COVID-19에 의해 부정적인 영향을 받았습니다. 2020년 상반기에 발생한 COVID-19로 인해 타이어 및 고무 산업은 큰 영향을 받았습니다. 이는 결과적으로 카본블랙 소비에 부정적인 영향을 미쳤습니다. 2021년에는 자동차 생산이 팬데믹의 영향에서 회복되면서 시장이 꾸준히 성장할 것으로 예상되었습니다.

주요 하이라이트

단기적으로 시장을 이끄는 주요 요인은 스페셜티 블랙의 시장 침투율 증가와 배터리 부문의 용도 증가입니다.

반면에 회수 된 카본블랙에 대한 투자 증가와 원자재 가격의 변동성은 연구 된 시장의 성장을 방해하고 있습니다.

전기자동차 채택의 성장은 향후 기회로 작용할 것으로 예상됩니다.

아시아태평양 지역은 중국과 인도에서 가장 많은 소비량을 보이며 전 세계 시장을 지배하고 있습니다.

카본블랙 시장 동향

타이어 및 산업용 고무 제품의 적용 증가

카본블랙은 타이어의 기계적 및 동적 특성에 미치는 영향으로 인해 타이어 산업에서 자주 사용되는 보강재 중 하나입니다.

카본블랙은 주로 내부 라이너, 사이드월, 카카스에 사용됩니다.

카본블랙은 자동차 타이어 및 기타 고무 제품에 필러, 강화제, 보강제로 사용됩니다.

WBCSD에 따르면 타이어 산업은 전 세계 천연 고무의 약 70%를 소비하고 있으며, 천연 고무에 대한 수요가 증가하면서 이 중요한 원자재 생산과 관련된 사회적, 경제적, 환경적 기회가 다양화되고 있습니다.

승용차와 경트럭의 신규 생산 부문에서 타이어에 대한 수요는 전 세계적으로 안정적인 성장세를 보이고 있습니다.

현대 타이어 딜러에 따르면 2022년 미국 내 전체 타이어 출하량은 약 3억 3,500만 개에 달했습니다.

기존 차량과 전기차를 포함한 자동차 산업의 성장은 타이어 및 타이어 부품 제조의 성장을 이끄는 중요한 요인입니다.

OICA에 따르면 2022년 전 세계 자동차 판매 및 등록 대수는 2021년 대비 약 0.8% 감소했습니다.

국제 고무 연구 그룹에 따르면 2022년 전 세계 고무 생산량은 전년 대비 소폭 증가에 그쳤습니다. 이는 주로 하반기에 생산량이 증가했기 때문입니다. 고무의 세계 생산량은 2021년 2,940만 톤에 비해 2022년 2,960만 톤에 달했습니다. 2022년에 생산된 합성고무는 약 1,490만 톤으로, 같은 해 생산된 천연고무를 불과 30만 톤 웃돌았습니다.

따라서 위의 모든 요인으로 인해 타이어 및 산업용 고무 제품에서 카본블랙에 대한 수요가 증가할 것으로 예상됩니다.

아시아태평양에서는 중국이 시장을 독점

중국은 생산량과 소비량 모두에서 전 세계 카본블랙 생산량에서 높은 비중을 차지하고 있습니다. 중국의 수요-공급 불균형은 국내 업체들의 시장 점유율과 실적에 영향을 미칠 수 있습니다.

타타이어 및 기타 고무 기반 제품에 카본블랙을 적용하고 최근 몇 년 동안 중국 고무 및 자동차 산업의 긍정적 인 발전으로 인해 카본블랙 산업의 급속한 발전이 중국에서 각광을 받았으며 전체 산업 생산이 증가하고 있습니다.

중국 국가통계국이 발표한 자료에 따르면 중국 타이어 산업은 국내외 시장에서 타이어에 대한 수요 증가를 반영하여 상당한 성장을 경험하고 있습니다.

2023년 3월, 중국의 타이어 생산량은 전년 동기 대비 11.3% 증가한 9,087만개로 국내 시장에서 수요 증가 동향을 보였습니다. 2023년 1월부터 3월까지 중국의 고무 타이어 생산량은 2억 1,998만개로 전년 동기 대비 6.4% 증가했습니다.

고무 타이어 생산량 증가는 중국이 지난 수년 동안 세계에서 가장 중요한 자동차 생산국이었다는 사실로 입증할 수 있습니다. 중국 자동차공업협회에 따르면 중국은 2023년 상반기에 이미 1,325만대 이상의 자동차를 생산하고 있으며, 전년 동기 대비 9.3%의 대폭적인 성장을 기록하고 있습니다.

타이어 및 고무 제품의 응용 분야와 함께 페인트 및 코팅의 안료 및 섬유 산업의 토너로 카본블랙을 적용하는 것도 중국에서 상당한 수요를 차지합니다. 따라서 중국의 페인트 및 코팅과 섬유 산업의 성장 추세가 시장 수요를 더욱 견인할 것으로 예상됩니다.

중국은 산업화와 제조 부문에서 페인트와 코팅이 널리 요구되는 것으로 유명합니다. 중국은 전 세계 코팅 시장의 4분의 1 이상을 차지합니다.

세계 페인트 및 코팅 산업 협회에 따르면 중국은 현재 5.8%의 연평균 성장률로 성장하고 있는 이 지역 시장을 지배하고 있습니다. 중국 페인트 및 코팅 시장은 2022년에 5.7% 증가할 것으로 예상됩니다.

2022년 중국의 섬유 및 의류 수출은 2.53% 증가하여 총액 3,230억 달러에 이르렀습니다.

중국의 섬유 및 의류 부문을 감독하는 규제 기관인 중국 국가 섬유 및 의류 위원회(CNTAC)는 2025년까지 중국의 연간 의류 소매 판매액이 4,150억 달러를 돌파할 것으로 예상하고 있습니다.

따라서 위에서 언급한 모든 요인은 예측 기간 동안 카본블랙 시장의 성장에 큰 원동력이 될 것으로 예상됩니다.

카본블랙 산업 개요

세계의 카본블랙 시장은 통합 시장으로 상위 10개 업체가 전체 시장에서 상당한 점유율을 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

스페셜티 블랙의 시장 침투 증가

배터리 부문의 성장

억제요인

회수 된 카본블랙에 대한 투자 증가

원자재 가격의 변동성

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

무역 분석

기술 상황 - 퀵 스냅샷

생산 분석

가격 동향 분석

제5장 시장 세분화

프로세스 유형

퍼니스 블랙

가스 블랙

램프 블랙

열 블랙

용도

타이어 및 산업용 고무 제품

플라스틱

토너 및 인쇄 잉크

코팅

섬유

기타 용도

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

시장 점유율(%) 분석

주요 기업의 전략

기업 프로파일

ADNOC Group

Asahi Carbon Co. Ltd

Birla Carbon(Aditya Birla Group)

BKT Carbon

Cabot Corporation

Epsilon Carbon Private Limited

Himadri Speciality Chemical Ltd

Imerys SA

International CSRC Investment Holdings Co. Ltd

Jiangxi Heimao Carbon Black Co. Ltd

Longxing Chemical Stock Co. Ltd

Mitsubishi Chemical Corporation

NNPC Limited

OCI Company Ltd

Omsk Carbon Group

Orion Engineered Carbons SA

PCBL Limited

Tokai Carbon Co. Ltd

제7장 시장 기회와 앞으로의 동향

전기자동차의 보급 확대

HBR

영문 목차

영문목차

The Carbon Black Market size is estimated at USD 24.10 billion in 2025, and is expected to reach USD 31.87 billion by 2030, at a CAGR of 5.75% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Due to the COVID-19 outbreak in the first half of 2020, the tire and rubber industry was significantly affected. This, in turn, had an unfavorable impact on the consumption of carbon black. The market was projected to grow steadily as automotive production recovered from the impact of the pandemic in 2021. The market witnessed a significant growth in 2022.

Key Highlights

In the short term, the major factors driving the market are the increasing market penetration of specialty black and growing applications in the batteries segment.

On the flip side, the increasing investments in recovered carbon black and volatility in the prices of raw materials are hindering the growth of the market studied.

The growth in the adoption of electric cars is expectde to act as an opportunity in the future.

Asia-Pacific dominated the market worldwide, with the largest consumption from China and India.

Carbon Black Market Trends

Increasing Application of Tires and Industrial Rubber Products

Carbon black is one of the reinforcements that is frequently used in the tire industry, owing to its effect on the mechanical and dynamic properties of tires. It is used in various formulations with different rubber types to customize the performance properties of tires.

Carbon black is mainly required in the inner liners, sidewalls, and carcasses. It has heat-dissipation capabilities when added to rubber compounds. It also improves handling, tread wear, and fuel mileage. It also provides abrasion resistance.

Carbon black is used in vehicle tires and other rubber products as a filler, strengthening, and reinforcing agent. Owing to its vital applications in tires and rubber products, the trends in these industries are expected to favor the growth of the market studied.

According to the WBCSD, the tire industry consumes approximately 70% of the world's natural rubber, and the demand for natural rubber is increasing, diversifying the social, economic, and environmental opportunities associated with the production of this important raw material.

The demand for tires in the newly produced segments of passenger cars and light trucks has been witnessing stable growth worldwide. This is depicted through the monthly statistics provided by the Michelin Group, which state that the worldwide original equipment tire market has seen a 10% growth in the first five months of 2023 when compared with 2022.

According to the Modern Tire Dealer, in 2022, overall shipments of tires in the United States amounted to around 335 million units. The majority of tire units shipped in 2022 were replacement passenger tires, with some 222 million units.

The growth in the automotive industry, including both conventional and electric vehicles, is a significant factor driving the growth of tire and tire component manufacturing.

According to the OICA, the global sales and registration of automobiles in 2022 observed a decline of around 0.8% as compared to 2021. It stood at 68,995,575 over 69,560,173 in 2021.

According to the International Rubber Study Group, global rubber production saw a minimal increase in the production in 2022, when compared with the prior year. This was majorly due to the increased production in the second half of the year. The global production of rubber reached 29.6 million metric tons in 2022 as compared to 29.4 million metric tons in 2021. The synthetic rubber produced during 2022 amounted to approximately 14.9 million metric tons, just 0.3 million metric tons higher than the natural rubber produced during the year.

Hence, all the above factors are expected to increase the demand for carbon black in the tires and industrial rubber products.

China to Dominate the Market in the Asia-Pacific Region

China accounts for a higher share of the world's carbon black capacity in terms of both production and consumption. Any demand-supply imbalance in China can affect the market share and performance of domestic players.

Owing to the application of carbon black in tires and other rubber-based products and the positive development of China's rubber and automobile industries in recent years, the carbon black industry's rapid development has taken the country's limelight, and the overall industry production is on the rise.

As per the data released by the National Bureau of Statistics, the Chinese tire industry is experiencing substantial growth, reflecting the increasing demand for tires in the domestic and international markets.

In March 2023, China's output of tires increased by 11.3% to 90.87 million compared to the same period last year, indicating a trend in the growing demand in the domestic market. China produced 219.98 million rubber tires from January to March 2023, a Y-o-Y increase of 6.4%.

The growing rubber tire production can be validated by the fact that the country has been the most significant vehicle producer in the world for the past many years. According to the China Association of Automobile Manufacturers, China has already manufactured more than 13.25 million vehicles in the first half of 2023, witnessing a significant 9.3% growth Y-o-Y.

Along with applications in tires and rubber products, the application of carbon black as a pigment in paints and coatings and as a toner in the textile industry also accounts to significant demand in the country. Hence growth trends in paints and coatings and textile industries in the country is further expected to drive the market demand.

China is known for its industrialization and its manufacturing sector, where paints and coatings are widely required. China accounts for more than one-fourth of the global coatings market. According to the China National Coatings Industry Association, the industry has been registering a growth of 7% in recent years.

According to the World Paint & Coatings Industry Association, China presently dominates the region market, which is growing at a CAGR of 5.8%. The Chinese paints and coatings market was expected to increase by 5.7 % in 2022. China's total paints and coatings sales exceeded USD 45 billion in 2022, thereby depicting the country's dominance in having the largest market share (78%) in East Asia.

In 2022, China experienced a 2.53% increase in its exports of textiles and apparel, reaching a total value of USD 323 billion. Over the year, China's exports in textiles, apparel, and clothing accessories amounted to USD 323.344 billion, showing a modest growth of 2.53% when compared to the previous year.

It is projected by the China National Textile and Apparel Council (CNTAC), the regulatory authority overseeing China's textile and apparel sector, that, by 2025, the annual retail sales of clothing in China could surpass USD 415 billion.

Thus, all the abovementioned factors are expected to provide a huge impetus for the growth of the carbon black market over the forecast period.

Carbon Black Industry Overview

The global carbon black market is a consolidated market, where the top ten players contribute to a significant share of the overall market. Some of the major players in the market include Cabot Corporation, Birla Carbon (Aditya Birla Group), Orion Engineered Carbons SA, Jiangxi HEIMAO Carbon black Co. Ltd, and International CSRC Investment Holdings Co. Ltd, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Market Penetration of Specialty Black

4.1.2 Growing Applications in the Batteries Segment

4.2 Restraints

4.2.1 Increasing Investments for Recovered Carbon Black

4.2.2 Volatility in Prices of Raw Materials

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Trade Analysis

4.6 Technology Landscape - Quick Snapshot

4.7 Production Analysis

4.8 Price Trend Analysis

5 MARKET SEGMENTATION (Market Size in Volume and Value)

5.1 Process Type

5.1.1 Furnace Black

5.1.2 Gas Black

5.1.3 Lamp Black

5.1.4 Thermal Black

5.2 Application

5.2.1 Tires and Industrial Rubber Products

5.2.2 Plastic

5.2.3 Toners and Printing Inks

5.2.4 Coatings

5.2.5 Textile Fiber

5.2.6 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 United Arab Emirates

5.3.5.4 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 ADNOC Group

6.4.2 Asahi Carbon Co. Ltd

6.4.3 Birla Carbon (Aditya Birla Group)

6.4.4 BKT Carbon

6.4.5 Cabot Corporation

6.4.6 Epsilon Carbon Private Limited

6.4.7 Himadri Speciality Chemical Ltd

6.4.8 Imerys SA

6.4.9 International CSRC Investment Holdings Co. Ltd