ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

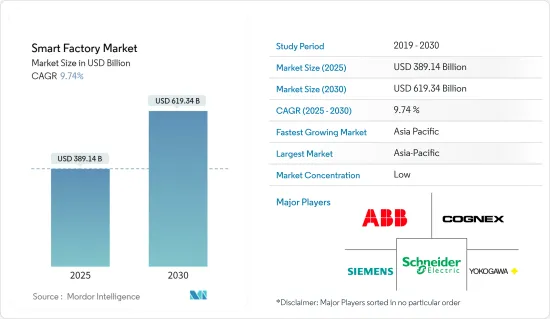

스마트팩토리 시장 규모는 2025년에 3,891억 4,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 9.74%로 성장할 전망이며, 2030년에는 6,193억 4,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

Industry 4.0과 IoT의 승인을 통한 제조업의 대폭적인 변화로 기업은 인간노동을 자동화로 보완 및 확장하고 프로세스 실패로 인한 산업사고를 삭감하는 기술로 생산을 전진시키기 위해 민첩하고 보다 혁신적이고 창조적인 방법을 채용할 필요가 있습니다. 접속된 디바이스 및 센서의 채용률이 높아져, M2M 통신이 촉진됨에 따라, 제조업에서 개발되는 데이터 포인트의 급증을 볼 수 있습니다.

Zebra의 Manufacturing Vision Study에 따르면 IoT와 RFID 기반 스마트 자산 추적 솔루션은 2022년에 기존의 스프레드시트 기반 방법을 추구했습니다. Maryville University의 계산에 따르면, 2025년까지 전 세계에서 연간 180조 기가바이트 이상의 데이터가 작성될 것으로 예상되고 있습니다. IIoT 대응 산업은 이 대부분을 창출할 것으로 보입니다. 또 산업용 IoT(IIoT) 기업인 Microsoft Corporation의 조사에 따르면 기업의 85%가 적어도 하나의 IIoT 유스 케이스 프로젝트를 안고 있는 것으로 나타났습니다. 2022년에는 응답자의 약 95%가 IIoT 전략을 시행했기 때문에 이 숫자는 증가했습니다.

제조시설의 지속적인 개발 증가와 더불어 기술의 진보는 예측 기간 중 시장성 장률에 영향을 미칠 것으로 예상됩니다. 예를 들어 인텔은 최근 텔레콤 이탈리아 및 하드웨어 제조업체 Exor International과 손잡고 인공지능(AI)과 5G 네트워킹을 이용한 스마트 제조시설을 개발했습니다.

또한 AI 및 머신러닝(ML) 기술 시장 침투가 가속화됨에 따라 데이터 분석의 정확성과 속도가 향상되어 시장이 크게 발전할 수 있습니다. 게다가, 필드 디바이스 시장, 로봇, 센서의 진보는 시장의 범위를 더욱 확대할 가능성이 있습니다. Cisco의 예측에 따르면 2022년까지 IoT 애플리케이션을 지원하는 머신투머신(M2M) 연결은 전 세계 285억 연결 장치의 50% 이상을 차지할 수 있습니다. 많은 정부도 스마트 팩토리 도입을 위해 IoT 기술에 투자하도록 제조 기업에 압력을 가하고 있습니다.

그러나, 높은 설치 비용이 시장 성장의 과제가 되고 있습니다. 또한 자동화 인프라를 운용 및 유지하기 위해서 고도의 스킬을 가지는 노동력이 필요한 것이, 전체적인 비용에 한층 더 박차를 가해, 특히 중소규모 산업에서의 대량 채용을 억제하고 있습니다.

게다가, 특히 미국과 중국의 무역분쟁 및 러시아와 우크라이나의 전쟁과 같은 지정학적 문제의 결과로서 최근의 경제적 불안정성도, 다양한 지역에 걸쳐 불확실한 비즈니스 환경에 연결되어 있을 뿐만 아니라, 다양한 지역의 산업 부문 공급망 및 제조 제품 수요에도 영향을 미치고 있기 때문에 시장의 성장에 불리한 환경을 초래하고 있습니다.

스마트 팩토리 시장 동향

반도체 분야가 시장 성장을 견인할 전망

반도체 제조업체는 더 높은 수율과 마진을 창출하기 위해 스마트 제조 공정에 의존합니다. 반도체 기술 혁신을 추진하고 첨단 칩을 탑재한 혁신적인 기술의 추가 구현을 촉진함으로써 제조업체는 공장이 더욱 복잡해지고 연결됨에 따라 수요 증가를 생산이 따라 잡을 수 있습니다.

반도체 제조 공장(팹)의 건설과 유지에는 수십억 달러의 비용이 듭니다. 그 비용은 장비에 달려 있으며 지속적인 운영에는 유지 보수가 필수적입니다. 혁신적인 제조 기술을 사용하여 장비의 건전성을 관찰하고 예측 유지 보수를 수행함으로써 공장은 예기치 않은 유지 보수 시간을 크게 단축할 수 있습니다.

반도체 제조 공장은 세계적으로 증가하는 경향이 있습니다. 또한 반도체 산업협회는 새로운 반도체 장치에 대한 지출 증가를 보고하고 있습니다. 이러한 요인들도 반도체 산업에서 스마트 팩토리 채택을 촉진할 것으로 보입니다. 반도체 산업협회(SIA)에 따르면 2022년 반도체 매출은 전 세계 5,801억 3,000만 달러에 달할 전망입니다. 반도체는 전자기기의 중요한 부품이며 업계 경쟁이 심합니다. 2022년 전년 대비 성장률은 4.4%에 달했습니다. 게다가 2022년 3월 유럽의 반도체 매출은 46억 3,000만 달러로 45억 1,000만 달러를 기록한 지난 달 수치에서 약간 증가했습니다.

또한 이 지역의 여러 나라들은 감세, 자금, 보조금 및 기타 형태의 지원을 제공하는 정부 정책을 통해 반도체 제조를 장려하는 데 주력하고 있습니다. 예를 들어, 정부에 따르면 인도의 반도체 부문은 2020년에 150억 달러로 평가되었고, 2026년에는 630억 달러로 성장할 것으로 예상됩니다(출처 : Ministry of Electronics &IT). 반도체 제조 및 주변 분야에 대한 정부 개입으로 인도는 세계 반도체 공급망의 주요 국가 중 하나가 될 것으로 기대됩니다.

또한 2022년 9월에는 광업 대기업 Vedanta와 대만의 전자기기 제조 대기업인 Foxconn이 구자라트주에 인도 최초의 반도체 공장을 설립하기 위해 18억 6,000만 달러라는 사상 최대급의 투자를 실시했습니다. 이러한 투자는 연구 대상 시장에서 더 큰 수요를 창출할 수 있습니다.

게다가 반도체 산업은 자율주행차나 IoT와 같은 AI 주도의 전자기기나 프로그램에 있어서의 반도체 재료 수요 증가에 대응하기 위해 성장하고 있습니다. 자동차 내비게이션, 안전성, 인포테인먼트 솔루션에 이용되는 전자부품의 소비 증가는 반도체 산업의 성장에 다시 기여합니다.

대폭적인 시장 성장을 이루는 아시아태평양

아시아태평양은 연구 시장에 대한 투자가 활발합니다. 각국 정부는 스마트 제조와 기술 채용을 강화하는 이니셔티브를 지속적으로 취하고 있습니다. 또한 인도 정부의 국가 제조업 정책은 2025년까지 GDP 대비 제조업 비중을 25%로 개선하는 것을 목표로 하고 있습니다. 또, 인도 정부의 'Make in India' 정책에 의해, 현지의 제조업에 의한 기계나 공구의 수요와 소비가 증가할 것으로 예상되고 있습니다.

게다가 2022년 1월, Reliance는 Addverb Technologies에 1억 3,200만 달러를 투자했으며, 54%의 주식을 취득했습니다. 이 시장에 대한 이러한 투자는 제조업에서 자동화 채택을 촉진하고, 이를 통해 예측 기간 동안의 스마트 팩토리 시장을 활성화시킬 것으로 예상됩니다.

지능형 애플리케이션으로의 전환이 진행되는 아시아에서 중국은 필수적인 존재입니다. 중국 정부는 표준 시스템 개발에 있어 다양한 계획 및 실증을 실시함으로써 스마트 제조의 설계를 강화하고 있습니다. 중국은 2025년까지 40개의 제조 혁신 창출을 목표로 하고 있습니다. 중점 분야로는 자동공작기계 및 로봇공학, 새로운 고도 정보기술, 항공우주 및 항공기기, 해양기기, 근대적 철도수송 기기, 하이테크 해운, 신에너지 자동차 및 기기, 전력기기, 농업기기, 신소재, 바이오의약품 및 첨단의료제품이 포함됩니다.

또한 2022년 1월에는 자동화 전문가인 ABB와 중국에서 가장 중요한 자동차 부품 공급업체인 HASCO가 중국 자동차 산업의 차세대 스마트 생산을 추진하기 위해 합작회사의 설립을 발표했습니다. 이 합작사업은 양사의 양호한 파트너십을 기반으로, HASCO의 중국 사업에 있어서, 유연성이 높고 지속 가능한 자동차 부품 생산의 중요한 개발을 실현하는 것입니다.

또한 일본은 'Society 5.0'을 향해 급속히 전진하고 있으며, 이 새로운 초스마트 사회에서의 인류 발전 4개의 주요 단계의 제5장이 시작됩니다. 모든 것이 IoT 기술로 연결되고 모든 기술이 통합되어 삶의 질이 극적으로 향상되고 있습니다. 게다가 일본 정부는 독일 정부의 인더스트리 4.0 프로그램에 호응해 커넥티드 인더스트리를 발표해 새로운 제조업 혁명의 기운이 높아지고 있습니다.

게다가 한국의 상업부문 및 공공 부문은 지역의 스마트 팩토리의 수를 늘리는 것에 합의해 2022년까지 최신의 디지털 기술과 분석 기술을 구사한 3만 이상의 공장을 가동할 예정이었습니다. 한국의 통상 산업 에너지부(MOTIE)는, 중소기업이 스마트 제조 기술을 채용해 확대하는 것을 지원하는 정부의 의욕을 재확인했습니다. 중소기업(SME)은 한국 전체 기업의 99% 이상을 차지하고 있으며, 정부 데이터에 따르면 중소기업의 수출은 증가하고 있습니다.

스마트 팩토리 산업 개요

스마트 팩토리 시장은 세분화되어 있으며, ABB Ltd, Cognex Corporation, Siemens AG, Schneider Electric SE, Yokogawa Electric Corporation 등의 주요 기업이 참가하고 있습니다. 이 시장의 기업은, 혁신, 파트너십, 합병, 인수 등의 전략을 채용해, 제품 제공 개선 및 지속 가능한 경쟁 우위성의 획득을 목표로 하고 있습니다.

2023년 3월-산업 자동화 및 에너지 관리 디지털 변환 솔루션 제공업체인 Schneider Electric은 헝가리에서 새로운 스마트 팩토리에 착공했습니다. 투자액은 4,000만 유로(4,300만 달러)로, 부지 면적은 25,000평방미터, 종업원수는 약 500명이 될 예정입니다.

2023년 3월-대형 소비자용 전자기기 제조업체인 Samsung Electronics는 Noida에 있는 휴대폰 제조공장에 스마트 제조 기능을 설치하기 위한 투자를 확대할 계획을 발표했습니다. 이 회사는 또 경쟁력 있는 현지 생산을 실현하기 위해 국내 연구개발 시설을 확장할 계획도 발표했습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁의 격렬함

산업 밸류체인 분석

거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 역학

시장 성장 촉진요인

밸류체인 전체에서 사물인터넷(IoT) 기술 채용 확대

에너지 효율에 대한 수요 증가

시장 성장 억제요인

변혁을 위한 막대한 설비 투자

사이버 공격에 대한 취약성

제6장 시장 세분화

제품 유형별

머신 비전 시스템

카메라

프로세서

소프트웨어

인클로저

프레임 그래버

통합 서비스

조명

산업용 로봇

다관절 로봇

직교 로봇

원통형 로봇

스칼라 로봇

병렬 로봇

협동형 산업용 로봇

제어기기

릴레이 및 스위치

서보 모터 및 드라이브

센서

통신 기술

유선

무선

기타 제품 유형

기술별

제품 수명주기 관리(PLM)

휴먼 머신 인터페이스(HMI)

기업 자원 계획(ERP)

제조 실행 시스템(MES)

분산 제어 시스템(DCS)

모니터링 제어 및 데이터 수집(SCADA)

프로그래머블 로직 컨트롤러(PLC)

기타 기술

최종 사용자 산업별

자동차

반도체

석유 및 가스

화학제품 및 석유화학제품

제약

항공우주 및 방위

음식

광업

기타

지역별

북미

미국

캐나다

유럽

영국

독일

프랑스

아시아

중국

인도

일본

호주 및 뉴질랜드

라틴아메리카

브라질

아르헨티나

멕시코

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

제7장 경쟁 구도

기업 프로파일

ABB Ltd

Cognex Corporation

Siemens AG

Schneider Electric SE

Yokogawa Electric Corporation

KUKA AG

Rockwell Automation Inc.

Honeywell International Inc.

Robert Bosch GmbH

Mitsubishi Electric Corporation

Fanuc Corporation

Emerson Electric Co.

FLIR Systems Inc.(Teledyne Technologies Incorporated)

제8장 투자 분석

제9장 시장의 미래

AJY

영문 목차

영문목차

The Smart Factory Market size is estimated at USD 389.14 billion in 2025, and is expected to reach USD 619.34 billion by 2030, at a CAGR of 9.74% during the forecast period (2025-2030).

Key Highlights

Tremendous shifts in manufacturing due to Industry 4.0 and the approval of IoT require enterprises to adopt agile, more innovative, and creative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. With the increased rate of adoption of connected devices and sensors and the fostering of M2M communication, a surge in the data points that are developed in the manufacturing industry is being observed.

According to Zebra's Manufacturing Vision Study, smart asset-tracking solutions based on IoT and RFID overtook traditional, spreadsheet-based methods in 2022. Maryville University calculates that by 2025, more than 180 trillion gigabytes of data are anticipated to be created worldwide yearly. IIoT-enabled industries will generate a large portion of this. In addition, an Industrial IoT (IIoT) company Microsoft Corporation survey found that 85 percent of companies have at least one IIoT use case project. This number increased, as approx 95 percent of respondents implemented IIoT strategies in 2022.

Incremental advancement in technology, coupled with a sustained increase in the development of manufacturing facilities, is expected to impact the market growth rate during the forecast period. For instance, Intel has recently partnered with Telecom Italia and hardware manufacturer Exor International to develop a smart manufacturing facility that uses artificial intelligence (AI) and 5G networking.

Furthermore, the glowing market penetration of AI and machine learning (ML) technologies may enhance the accuracy and speed of data analysis, thereby significantly driving the market forward. Moreover, the advancement in the field devices market, robots, and sensors may further expand the scope of the studied market. According to Cisco projections, by 2022, machine-to-machine (M2M) connections that support IoT applications may have accounted for more than 50 percent of the world's 28.5 billion connected devices. Many governments also motivate manufacturing companies to invest in IoT technologies for smart factory adoption, which creates a favorable outlook for the growth of the studied market.

However, a high installation cost is the primary factor challenging the market's growth. Additionally, the requirement of a highly skilled workforce to operate and maintain the automation infrastructure further adds to the overall cost, restraining mass adoption, especially in small and medium-scale industries.

Additionally, the recent economic instability, especially as an outcome of the pandemic and geo-political issues such as the US-China trade dispute and the Russia-Ukraine war, is also challenging the studied market's growth as it has not only led to an uncertain business environment across various regions but are also impacting the supply chain of industrial sectors and demand for manufactured products across various region, leading to an unfavorable environment for the studied market's growth.

Smart Factory Market Trends

Semiconductor Sector is Expected to Drive the Market Growth

Semiconductor manufacturers rely on smart manufacturing processes to produce higher yields and margins. By advancing semiconductor innovation and encouraging the further implementation of innovative technologies powered by advanced chips, manufacturers can ensure that production keeps pace with rising demand as factories become more complex and connected.

Semiconductor fabrication plants, or fabs, cost billions of dollars to build and maintain. The cost goes on equipment, the maintenance of which is vital to ongoing operation. By using innovative manufacturing technologies to observe equipment health and execute predictive maintenance, fabs can decrease unplanned maintenance time significantly.

The semiconductor fabrication plants globally are on the rise. Also, the Semiconductor Industry Association reported increased spending on new semiconductor equipment. These factors will also drive the adoption of smart factories in the semiconductor industry. According to the Semiconductor Industry Association (SIA), in 2022, semiconductor sales reached USD 580.13 billion worldwide. Semiconductors are crucial components of electronic devices, and the industry is highly competitive. The year-on-year growth rate in 2022 reached 4.4 percent. Additionally, semiconductor sales in Europe in March 2022 were USD 4.63 billion, up slightly from last month's figures, which recorded USD 4.51 billion.

Moreover, various countries in this region are focused on encouraging semiconductor manufacturing through government policies offering tax breaks, money, subsidies, and other forms of assistance. For instance, according to the government, the Indian semiconductor sector was valued at USD 15 billion in 2020 and is anticipated to grow to USD 63 billion by 2026 (Source: Ministry of Electronics & IT). Through governmental intervention in the manufacturing of semiconductors and the peripheral sector, India is expected to become one of the leading countries in global semiconductor supply chains.

In addition, in September 2022, mining conglomerate Vedanta and Taiwanese electronics manufacturing giant Foxconn made one of the largest ever investments of USD 1,860 million to set up India's first semiconductor plant in Gujarat. Such investment may further create significant demand in the studied Market.

Besides, the semiconductor industry is growing to accommodate the rising demand for semiconductor materials in AI-driven electronics and programs such as autonomous vehicles and IoT. The growth in the consumption of electronic components utilized in the navigation of automobiles, safety, and infotainment solutions intention again contribute to the semiconductor industry's growth.

Asia-Pacific to Experience Significant Market Growth

Asia-Pacific significantly invests in the studied Market. Governments continuously take the initiative to enhance smart manufacturing and technology adoptions in various countries. In addition, the National Manufacturing Policy of the Government of India aims to improve the share of manufacturing in GDP to 25 percent by 2025. Also, the "Make in India" policy of the Government of India is anticipated to increase the demand and consumption of machinery and tools by the local manufacturing industry.

Moreover, in January 2022, Reliance invested USD 132 million in Addverb Technologies to acquire a 54 percent stake. Such investments in the Market are expected to fuel the adoption of automation in the manufacturing industry, thereby fueling the smart factory market during the forecast period.

China is an integral part of Asia's rising shift to intelligent applications. The Chinese government has strengthened the design of smart manufacturing by implementing various schemes and demonstrations in developing standard systems. China aims to create 40 manufacturing innovations by 2025. The focus areas include automated machine tools and robotics, new advanced information technology, aerospace and aeronautical equipment, marine equipment, modern rail transport equipment, high-tech shipping, new-energy vehicles and equipment, power equipment, agricultural equipment, new materials, biopharma, and advanced medical products.

Further, in January 2022, ABB, an automation expert, and HASCO, China's most significant automotive components supplier, announced the construction of a joint venture to push China's automotive industry's next generation of smart production. The joint venture will build on the two businesses' successful partnership, resulting in the vital development of highly flexible and sustainable car parts production within HASCO's China operations.

Furthermore, Japan is rapidly moving toward "Society 5.0", thus introducing the fifth chapter to the four major stages of human development in this new ultra-smart society. All things are connected through IoT technology, and all technologies are getting integrated, dramatically improving the quality of life. Further, the Japanese government announced connected industries in response to the German government's "Industry 4.0" program, and the momentum for a new manufacturing revolution is rising.

Further, Korea's commercial and public sectors have agreed to boost the number of local smart factories, intending to have more than 30,000 of them working with the newest digital and analytical technology by 2022. Korea's Ministry of Trade, Industry, and Energy (MOTIE) has reaffirmed the government's ambitions to assist small and medium-sized businesses in adopting and expanding smart manufacturing technology. Small and medium-sized firms (SMEs) account for more than 99 percent of all companies in Korea, and government data suggests that SMEs' exports are growing.

Smart Factory Industry Overview

The smart factory market is fragmented, with significant players like ABB Ltd, Cognex Corporation, Siemens AG, Schneider Electric SE, and Yokogawa Electric Corporation. Players in the market are adopting strategies such as innovations, partnerships, mergers, and acquisitions to improve their product offerings and achieve sustainable competitive advantage.

In March 2023, Schneider Electric, a solution provider for the digital transformation of industrial automation and energy management, broke ground on its new smart factory in Hungary. With an expected investment of EUR 40 million (USD 43 million), the new site will span 25,000 m2 with a headcount of about 500 employees.

In March 2023, Samsung Electronics, a leading consumer electronic device manufacturer, announced its plans to increase investment in setting up smart manufacturing capabilities at its mobile phone manufacturing plant in Noida. The company also announced its plans to expand its research and development facility in the country to make production more competitive and localized.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competition

4.3 Industry Value Chain Analysis

4.4 Assessment of Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Adoption of Internet of Things (IoT) Technologies Across the Value Chain

5.1.2 Rising Demand for Energy Efficiency

5.2 Market Restraints

5.2.1 Huge Capital Investments for Transformations

5.2.2 Vulnerable to Cyberattacks

6 MARKET SEGMENTATION

6.1 By Product Type

6.1.1 Machine Vision Systems

6.1.1.1 Cameras

6.1.1.2 Processors

6.1.1.3 Software

6.1.1.4 Enclosures

6.1.1.5 Frame Grabbers

6.1.1.6 Integration Services

6.1.1.7 Lighting

6.1.2 Industrial Robotics

6.1.2.1 Articulated Robots

6.1.2.2 Cartesian Robots

6.1.2.3 Cylindrical Robots

6.1.2.4 SCARA Robots

6.1.2.5 Parallel Robots

6.1.2.6 Collaborative Industry Robots

6.1.3 Control Devices

6.1.3.1 Relays and Switches

6.1.3.2 Servo Motors and Drives

6.1.4 Sensors

6.1.5 Communication Technologies

6.1.5.1 Wired

6.1.5.2 Wireless

6.1.6 Other Product Types

6.2 By Technology

6.2.1 Product Lifecycle Management (PLM)

6.2.2 Human Machine Interface (HMI)

6.2.3 Enterprise Resource and Planning (ERP)

6.2.4 Manufacturing Execution System (MES)

6.2.5 Distributed Control System (DCS)

6.2.6 Supervisory Controller and Data Acquisition (SCADA)

6.2.7 Programmable Logic Controller (PLC)

6.2.8 Other Technologies

6.3 By End-user Industry

6.3.1 Automotive

6.3.2 Semiconductors

6.3.3 Oil and Gas

6.3.4 Chemical and Petrochemical

6.3.5 Pharmaceutical

6.3.6 Aerospace and Defense

6.3.7 Food and Beverage

6.3.8 Mining

6.3.9 Other End-user Industries

6.4 By Geography

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.3 Asia

6.4.3.1 China

6.4.3.2 India

6.4.3.3 Japan

6.4.3.4 Australia and New Zealand

6.4.4 Latin America

6.4.4.1 Brazil

6.4.4.2 Argentina

6.4.4.3 Mexico

6.4.5 Middle East and Africa

6.4.5.1 United Arab Emirates

6.4.5.2 Saudi Arabia

6.4.5.3 South Africa

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 ABB Ltd

7.1.2 Cognex Corporation

7.1.3 Siemens AG

7.1.4 Schneider Electric SE

7.1.5 Yokogawa Electric Corporation

7.1.6 KUKA AG

7.1.7 Rockwell Automation Inc.

7.1.8 Honeywell International Inc.

7.1.9 Robert Bosch GmbH

7.1.10 Mitsubishi Electric Corporation

7.1.11 Fanuc Corporation

7.1.12 Emerson Electric Co.

7.1.13 FLIR Systems Inc. (Teledyne Technologies Incorporated)