영국의 작물 보호 화학제품 시장 :시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

UK Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1686575

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

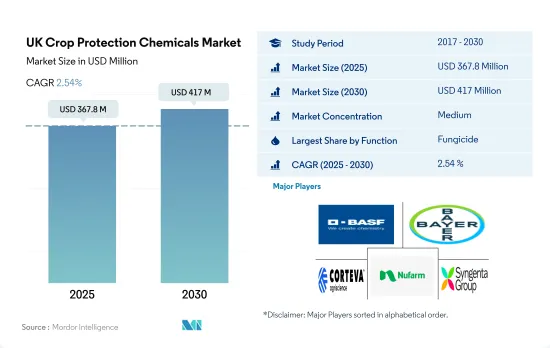

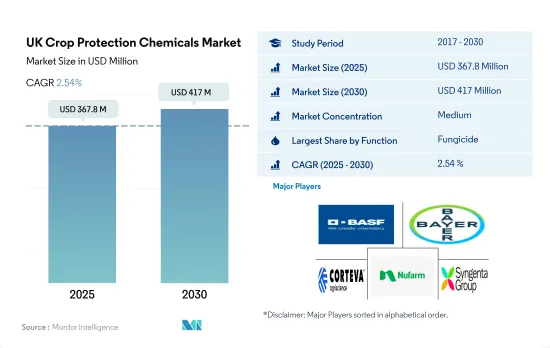

영국의 작물 보호 화학제품 시장 규모는 2025년에는 3억 6,780만 달러로 추정되고, 2030년에는 4억 1,700만 달러에 달할 것으로 예측되며, 예측 기간 2025-2030년 CAGR 2.54%로 성장할 전망입니다.

이 나라에서는 해충이나 병해의 만연이 증가하고 있으며, 심각한 수율 감소로 이어져 다양한 작물 보호 화학제품 시장을 견인하고 있습니다.

영국의 살균제 시장은 2022년에 1억 8,290만 달러로 평가되었습니다. 같은 해 시장 점유율은 53.2%로 작물 보호 화학제품 중 가장 많이 소비되고 있습니다.

영국에서 가장 널리 사용되는 살균제로는 클로로탈로닐, 에폭시코나졸, 프로티오코나졸, 테부코나졸 등이 있습니다. Septoria tritici는 영국의 밀에서 가장 피해가 큰 엽면병해이며 기압이 높은 계절에는 30-50%의 수확 손실을 일으킵니다. 많은 밀 생산자들은 수확량 손실을 줄이기 위해 살균제 사용을 늘리고 있습니다.

잡초는 면화와 겨울 밀과 같은 영국 작물에 영향을 미칩니다. 주요 섬유 작물인 면화에서는 30%의 수확량 감소를 일으키고 있습니다. 토종 잡초인 블랙그라스(Alopecurus myosuroides)는 영국 농장에 만연해 있습니다. 이 심각한 만연으로 농가는 주요 곡물인 겨울 밀을 포기할 수밖에 없게 됩니다. 잡초는 자원을 서로 빼앗고 작물의 성장을 방해하며 수확량을 감소시키기 때문에 경제적 손실을 야기하고 제초제 채택으로 이어졌습니다. 제초제는 2022년 영국 작물 보호 화학제품 시장의 38.2%를 차지했습니다.

기후 변화와 기온 상승으로 해충의 개체수와 식성이 증가하고 있습니다. 한 조사에 따르면 작물에 대한 열 스트레스가 강해짐에 따라 영국에서는 기온이 2℃ 상승하면 곡물 수율이 약 10% 감소할 것으로 예측되고 있습니다. 그 결과, 이 나라의 농가는 해충의 압력에 대처하기 위해 살충제에 의존하지 않을 수 없게 되었습니다.

이 나라에서는 해충과 병해의 만연이 증가하고 있어 심각한 수량 감소로 이어지고 있기 때문에 농가의 요구에 근거한 다양한 농작물 보호제 시장을 견인하고 있습니다. 이 시장은 예측 기간 2023-2029년 CAGR 2.4%를 기록할 것으로 예측됩니다.

영국 작물 보호 화학제품 시장 동향

영국에서는 농민들이 비화학적 대체품을 채택하는 등 다양한 요인으로 인해 농약 소비가 감소하고 있습니다.

영국에서는 농약의 소비량이 감소하고 있습니다. 2017-2022년 축산으로의 경작 면적 변경, 특정 활성 물질 철수, 날씨가 해충과 질병 수준에 미치는 영향, 농가의 비화학적 대체 물질 채택 등으로 헥타르당 소비량은 24만 3,800톤 감소했습니다.

영국에 대한 농약 사용 감소 압력 증가는 향후 수년간 농약 소비에 영향을 줄 수 있습니다. 정부는 농약의 사용을 줄이기 위해 몇 가지 이니셔티브를 취하고 있습니다. 예를 들어, 2018년 1월 영국 정부는 'A Green Future : Our 25-Year Plan'을 발표하고 환경을 개선하고 종합적 병해충 관리(IPM)와 지속 가능한 작물 보호 도입을 확대하려고 합니다.

2020년 영국 농업에서 글리포세이트의 사용량은 발암과의 관련성이 지적되었음에도 불구하고 무게, 처리 면적, 헥타르당 산포율로 4년간 16% 증가했습니다. 정부는 수확 전 건조(글리포세이트를 사용하여 작물을 인공적으로 건조시키는) 증가, 또는 경작에 의해 토양으로부터 탄소를 방출하지 않고 잡초에 대처하기 위해 글리포세이트 및 기타 제초제에 의존하는 경향이 있는 불경기 농업 증가에 의해 종래의 화학제품에 대한 의존을 줄일 계획입니다. 유사하게, 살균제 이마자릴의 사용은 53% 증가하였고, 동시기에 이 약으로 처리된 토지 면적은 63% 증가하여 8만 1,000헥타르를 초과하였습니다.

식물의 질병과 해충은 농업 생산에 큰 영향을 미치므로 기후 변화, 병해충 및 수확 손실은 농작물을 보호하고 해충의 수확 손실을 줄이기 위해 농약 소비를 촉진할 수 있습니다.

규제 변경 및 농약 감소에 중점을 둔 정부는 작물 보호 화학제품의 가격에 영향을 미칠 수 있습니다.

시펠메트린과 에마멕틴 벤조산염은 대규모로 사용되는 중요한 살충제 성분입니다. 2022년, 이러한 성분의 가격은 각각 톤당 2만 1,100달러, 톤당 1만 7,300달러였습니다.

2022년에 1톤당 8,700달러로 평가된 메탈락실은 보호 및 처리 작용으로 알려진 침투성 페닐아미드계 살균제입니다. 포자낭의 형성, 균사의 성장, 새로운 감염의 확립을 억제함으로써 효과를 발휘합니다. 곰팡이의 핵산 합성(RNA 중합 효소 1)을 억제합니다. 이 살균제는 열대 및 아열대 작물에 대한 엽면 살포, 토양 전염성 병원균의 방제를 위한 토양 처리제, 베토병 관리를 위한 종자 처리제로서 추천되고 있습니다.

글리포세이트는 잡초 제거를 위한 제초제로서, 또한 경작하는 대신 농가에게 널리 사용되고 있지만, 토양 생태계를 파괴하고 탄소를 방출하는 것이 관찰되고 있습니다. 영국에서는 농업에서 글리포세이트의 사용량이 2020년까지 4년간 16% 증가했습니다. 농약 살포 면적은 9%(23만 헥타르) 확대했습니다. 밀 농부는 수확 전 작물 건조를 위해 글리포세이트를 현저하게 사용합니다. 2022년 글리포세이트 가격은 전년 대비 2.2% 상승했습니다.

선택적 제초제인 펜디메탈린은 디니트로아닐린계 제초제에 속합니다. 다양한 원예작물, 잔디, 임업에 있어서, 1년초, 다년초, 활엽수, 목본류 등 폭넓은 잡초의 방제에 사용됩니다. 2022년 펜디메탈린 가격은 톤당 3,300달러였습니다.

영국 작물 보호 화학제품 산업 개요

영국의 작물 보호 화학제품 시장은 적당히 통합되어 상위 5개사에서 63.61%를 차지하고 있습니다. 이 시장의 주요 기업으로는 BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group 등이 있습니다.(알파벳순 정렬)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 오퍼

제3장 서문

조사의 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

영국

밸류체인 및 유통채널 분석

제5장 시장 세분화

기능별

살균제

제초제

살충제

연체동물 구제제

선충 구제제

용도별

화학적 처리

잎면 살포

훈증

종자 처리

토양처리

작물 유형별

상업 작물

과일 및 야채

곡물

콩류 및 지방종자

잔디 및 관상용 식물

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

ADAMA Agricultural Solutions Ltd.

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Nufarm Ltd

Sumitomo Chemical Co. Ltd

Syngenta Group

UPL Limited

Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The UK Crop Protection Chemicals Market size is estimated at 367.8 million USD in 2025, and is expected to reach 417 million USD by 2030, growing at a CAGR of 2.54% during the forecast period (2025-2030).

Increasing pests and disease infestations in the country are leading to severe yield losses and driving the market for different crop protection chemicals

The UK fungicide market was valued at USD 182.9 million in 2022. It was the most consumed among crop protection chemicals, with a market share of 53.2% in the same year.

The most extensively used fungicide formulations in the United Kingdom include chlorothalonil, epoxiconazole, prothioconazole, and tebuconazole. Septoria tritici is UK wheat's most damaging foliar disease, causing yield losses that range from 30% to 50% in high-pressure seasons. Many wheat growers have increased the use of fungicides in their crops to mitigate yield loss.

Weeds impact UK crops like cotton and winter wheat. They cause a 30% yield loss in cotton, the main fiber crop. Black grass (Alopecurus myosuroides), a native weed, frequently infests UK farms. Severe infestations force farmers to abandon winter wheat, the main cereal crop. Weeds compete for resources, hinder crop growth, and reduce yields, causing economic losses and leading to the adoption of herbicides. Herbicides accounted for 38.2% of the UK crop protection chemicals market in 2022.

The changing climate and rising temperatures are causing an increase in the population and feeding habits of insect pests. A study reveals that as heat stress on crops intensifies, cereal yields in the United Kingdom are projected to decline by approximately 10% with a 2 °C increase in temperature. Consequently, these circumstances are prompting farmers in the country to rely on insecticides to manage pest pressures.

Increasing pests and disease infestations in the country have led to severe yield losses, thus driving the market for different crop protection chemicals based on farmers' needs. The market is estimated to register a CAGR of 2.4% during the forecast period (2023-2029).

UK Crop Protection Chemicals Market Trends

The United Kingdom is experiencing a decline in the consumption of pesticides due to various factors, including the adoption of non-chemical alternatives by farmers

The United Kingdom is experiencing a decline in the consumption of pesticides. From 2017 to 2022, the consumption per hectare decreased by 243.8 thousand metric ton due to changes in the area of cultivation to livestock farming, withdrawal of certain active substances, the impact of the weather on pest and disease levels, and the adoption of non-chemical alternatives by farmers.

The rising pressure on the United Kingdom to reduce the use of pesticides could impact the consumption of pesticides in the coming years. The government is taking several initiatives to reduce the use of pesticides. For instance, in January 2018, the UK government launched "A Green Future: Our 25-Year Plan" to improve the environment and increase the uptake of integrated pest management (IPM) and sustainable crop protection.

In 2020, the use of glyphosate in UK farming grew by 16% over four years in terms of weight, the area treated, and application rate per hectare despite being linked to causing cancer and the government plans to reduce reliance on conventional chemicals due to rising pre-harvest desiccation (where crops are artificially dried using glyphosate) and/or an increase in no-till agriculture, which tends to rely upon glyphosate and other herbicides to deal with weeds without releasing carbon from the soil via plowing. Similarly, the use of the fungicide imazalil increased by 53%, while the land area treated with the chemical rose by 63% to more than 81,000 ha during the same period.

Changing climate, pests and diseases, and harvest losses could drive the consumption of pesticides to protect crops and reduce pest yield losses, as plant diseases and pests can have a significant impact on agriculture production.

Regulatory changes and the government's focus on reducing pesticides may influence the prices of crop protection chemicals

Cypermethrin and emmamectin benzoate are significant insecticide ingredients used on a large scale. In 2022, these ingredients were priced at USD 21.1 thousand per metric ton and USD 17.3 thousand per metric ton, respectively.

Metalaxyl, valued at USD 8.7 thousand per metric ton in 2022, is a systemic phenylamide fungicide known for its protective and curative mode of action. It works by suppressing sporangial formation, mycelial growth, and the establishment of new infections. It disrupts fungal nucleic acid synthesis - RNA polymerase 1. This fungicide is recommended for foliar spray on tropical and sub-tropical crops, as a soil treatment for controlling soil-borne pathogens, and as a seed treatment to manage downy mildew.

Glyphosate, widely used by farmers as a herbicide for weed control and as an alternative to plowing, has been observed to disrupt the soil ecosystem and release carbon. In the United Kingdom, its usage in farming witnessed a growth of 16% over four years till 2020, with regenerative farming practices encouraging reduced plowing. The area of land sprayed with pesticides expanded by 9% (230,000 ha). Wheat farms are notable users of glyphosate for crop desiccation before harvest. In 2022, the price of glyphosate experienced a 2.2% increase compared to the previous year.

Pendimethalin, a selective herbicide, belongs to the dinitroaniline herbicide family. It is used to control a broad range of weeds, including annual and perennial grasses, broadleaf species, and woody species in various horticultural crops, turf, and forestry. In 2022, pendimethalin was priced at USD 3.3 thousand per metric ton.

UK Crop Protection Chemicals Industry Overview

The UK Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 63.61%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 United Kingdom

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Function

5.1.1 Fungicide

5.1.2 Herbicide

5.1.3 Insecticide

5.1.4 Molluscicide

5.1.5 Nematicide

5.2 Application Mode

5.2.1 Chemigation

5.2.2 Foliar

5.2.3 Fumigation

5.2.4 Seed Treatment

5.2.5 Soil Treatment

5.3 Crop Type

5.3.1 Commercial Crops

5.3.2 Fruits & Vegetables

5.3.3 Grains & Cereals

5.3.4 Pulses & Oilseeds

5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd.

6.4.2 BASF SE

6.4.3 Bayer AG

6.4.4 Corteva Agriscience

6.4.5 FMC Corporation

6.4.6 Nufarm Ltd

6.4.7 Sumitomo Chemical Co. Ltd

6.4.8 Syngenta Group

6.4.9 UPL Limited

6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS