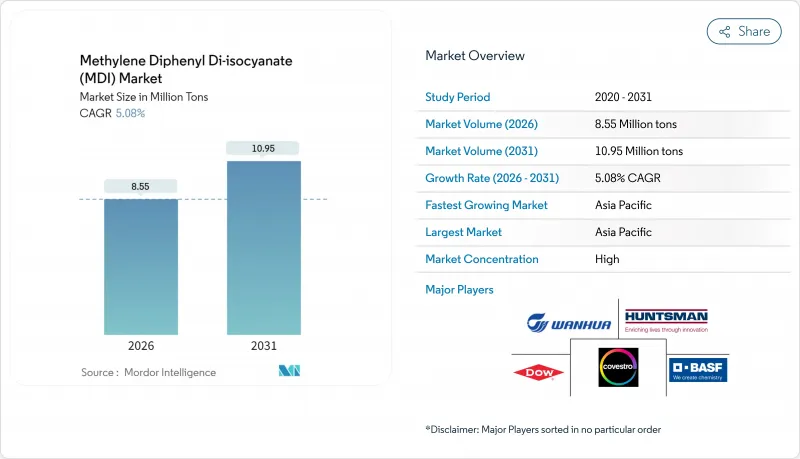

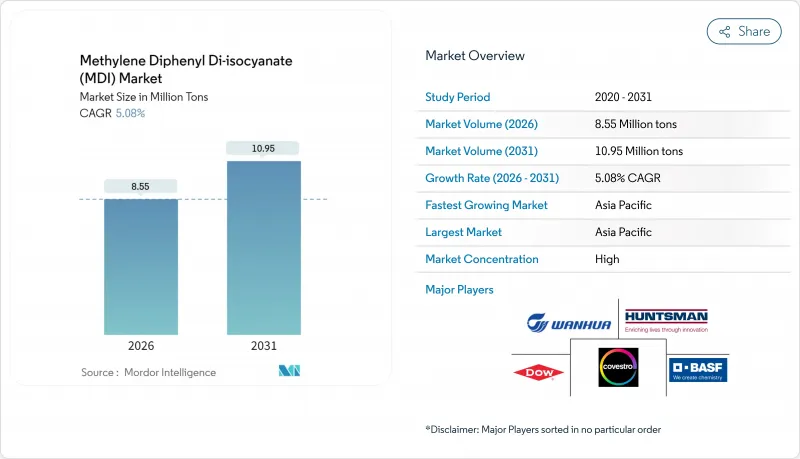

메틸렌 디페닐 디이소시아네이트(MDI) 시장은 2025년 814만 톤에서 2026년 855만 톤으로 성장해 2026-2031년에 걸쳐 CAGR 5.08%의 성장이 예상되며, 2031년까지 1,095만 톤에 달할 것으로 예측되고 있습니다.

아시아태평양 지역의 비용 경쟁력 있는 공급 확대와 북미 및 유럽 전역의 탄소 중립 건물 의무화 및 가전 제품 효율성 기준이 이러한 성장 궤도를 뒷받침하고 있습니다. 업계 선두 기업들은 고객 충성도를 유지하기 위해 바이오 순환 및 질량 균형 등급을 확대하고 있으며, 포스겐 프리 파일럿 라인은 장기적인 공정 혁신을 예고하고 있습니다. 원료 가격 변동성(2025년 아닐린 가격 전년 대비 36.81% 하락)이 마진 변동성을 가중시키지만, 통합 생산업체들은 여전히 더 나은 완충 효과를 유지합니다. 강화되는 근로자 노출 규제와 신규 플랜트의 자본 집약도는 경쟁 장벽을 높게 유지하며 기술력을 보유한 기존 기업들을 중심으로 한 시장 통합을 가속화합니다.

EU의 '건축물의 에너지 성능 지령'을 통해 회원국은 2030년까지 3조 5,000억 유로(3조 8,000억 달러)의 에너지 효율화 투자를 의무화하고 있습니다. 신축 건물은 제로 에너지 목표를 충족해야 하며, 기존 건물은 열전도율 0.022 W/m*K 이하의 경질 폴리우레탄 패널을 선호하는 의무적 심층 리모델링을 거쳐야 합니다. 캘리포니아의 2025년 건축 규정도 유사한 규정을 도입하며 북미에서도 동일한 수요 증가를 이끌고 있습니다. 건물 자동화 사양은 고급 제어 시스템이 더 엄격한 열 외피를 요구함에 따라 MDI 소비를 더욱 촉진합니다. 규제와 성능 간의 시너지는 경질 폼을 MDI 시장에서 가장 높은 성장률을 보이는 분야로 굳건히 자리매김하게 합니다.

팬데믹 이후 백신 물류는 온도 편차의 비용을 보여주며 제약 공급망을 초저온 저장 방식으로 전환시켰습니다. 인도의 보조금 지원 콜드체인 프로그램은 -80°C 열적 무결성을 유지할 수 있는 폴리우레탄 시스템에 의존하는 신규 창고를 추가하고 있습니다. 동시에 도시 생활 방식 변화에 힘입어 동남아시아 및 라틴아메리카 전역에서 고급 냉장 운송 및 소매 진열장이 확대되며 식품 콜드체인도 성장 중입니다. 고성능 사양은 프리미엄 MDI 등급의 마진 구조를 개선하여 원자재 인플레이션 속에서도 판매량 탄력성을 강화합니다.

EU는 직장 노출을 6µg NCO/m3로 제한하고 모든 취급자에 대한 인증 교육 이수를 의무화했습니다. 미국 노동안전보건청(OSHA)도 동일한 조치를 취하고 있습니다. 규정 준수를 위한 환기, 모니터링 및 의료 감시 시스템 투자로 인해 스프레이 폼 계약업체와 소형 가전 제품 라인의 고정 비용이 증가하고 있습니다. 이러한 부담은 자본력이 풍부한 가공업체로의 시장 통합을 가속화하고, 가격 프리미엄을 요구하지만 제형 노하우가 필요한 저모노머 또는 프리폴리머 솔루션으로 수요를 편향시키고 있습니다.

경질 폼은 2025년 MDI 시장 규모의 36.78%를 차지했으며, 2031년까지 연평균 5.63% 성장률(CAGR)로 증가할 것으로 예상됩니다. 이 카테고리는 주거 및 상업 건축에서 넷제로 기준 준수를 가능케 하는 최고 수준의 0.022 W/m*K 열전도율을 제공하는 폴리이소시아누레이트 패널의 혜택을 받습니다. 유연 발포체는 침구 및 자동차 시트 분야에서 여전히 중요성을 유지하지만 성숙도로 인해 성장 한계가 있습니다. 코팅 및 엘라스토머는 산업 유지보수 및 자재 취급 응용 분야에서 지속적인 수요를 확보하여 기본 물량을 강화합니다. 신규 용도로는 열 사이클링 하에서 치수 안정성이 요구되는 전기차 배터리 캡슐화 재료가 포함되며, 이는 MDI 화학의 다용도성을 부각시킵니다. 경질 폼의 지붕 재시공 및 커튼월 시스템의 채택 증가로 MDI 시장 내 지속적인 우위가 거의 확실시됩니다.

전 세계적으로 건축 규정이 강화됨에 따라 보험사 및 금융사는 얇은 벽 두께에서도 경질 폴리우레탄 또는 PIR 제품만이 실질적으로 충족 가능한 최소 R값을 규정하고 있습니다. 레티셀의 유로월 임팩트 보드는 25% 바이오 순환 소재 함유로 열적 성능 저하 없이 내재 탄소 배출량을 43% 절감했습니다. 접착제 및 실란트는 자동차 및 인프라 수리 분야에서 틈새 시장이면서도 수익성이 높은 하위 부문으로, MDI는 빠른 경화 및 구조적 접착력을 제공합니다. 특수 엘라스토머는 채광 스크린 및 산업용 휠에서 비중을 차지하며 안정적인 애프터마켓 수익을 창출합니다. 이러한 하위 부문들은 종합적으로 경질 폼을 MDI 시장의 장기 성장 핵심 요소로 자리매김하게 합니다.

메틸렌 디페닐 디이소시아네이트(MDI) 시장 보고서는 용도별(경질 폼, 연질 폼, 코팅, 엘라스토머, 접착제 및 실란트, 기타), 최종 사용자 산업별(건설, 가구 및 인테리어, 전자 기기, 가전, 자동차, 신발 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)에 분석

아시아태평양 지역은 2025년 MDI 시장의 46.35%를 차지했으며, 2031년까지 지역 최고 수준인 5.90%의 연평균 복합 성장률(CAGR)로 확장될 것으로 전망됩니다. 중국의 친환경 건축 규정과 인프라 붐은 방대한 경질 폼 수요를 흡수하는 반면, 인도의 백신 물류 확대는 냉장 저장 용량을 증가시키고 있습니다. 금호미쓰이의 200kt 병목 해소 프로젝트로 여수 단지를 610kt로 확장하는 등 증설 사업이 지역 공급을 뒷받침합니다.

북미는 리모델링 인센티브와 고성능 주거용 건물에 세액 공제를 제공하는 섹션 45L 세제 혜택으로 여전히 중요합니다. 특히 코베스트로는 칼라일 건설 자재에 바이오 순환형 MDI를 공급하여 화석 기반 등급 대비 업스트림 탄소 배출량을 99% 절감합니다. 국내 가전 제조사들도 2025년 에너지 규정을 충족하기 위해 고밀도 폼을 지정하며 안정적인 기초 수요를 확보하고 있습니다.

유럽의 정책 주도력은 유기적 성장을 넘어선 합성 수요를 창출합니다. EPBD의 3조 5,000천억 유로 규모 리모델링 계획은 경질 폼 채택을 가속화하며, 6 마이크로그램 노출 상한선은 제형 개발사들이 저모노머 변종으로 전환하도록 유도합니다. 생산사들의 초점은 순환경제와 일치합니다. 바스프(BASF)는 190만 톤 규모의 글로벌 MDI 생산망을 최적화하기 위해 상하이 합작사를 분리해 매스밸런스 생산을 위한 자산을 확보했습니다. 한편 중동 및 아프리카 지역은 물류 단지 및 기후 제어 농업으로 인한 성장세를 보이지만, 대부분의 제품은 여전히 유럽과 아시아에서 수입됩니다.

The Methylene Diphenyl Di-isocyanate market is expected to grow from 8.14 Million tons in 2025 to 8.55 Million tons in 2026 and is forecast to reach 10.95 Million tons by 2031 at 5.08% CAGR over 2026-2031.

Cost-competitive supply expansions in Asia-Pacific, paired with net-zero building mandates and appliance efficiency standards across North America and Europe, underpin this growth trajectory. Industry leaders are scaling bio-circular and mass-balanced grades to retain customer loyalty, while phosgene-free pilot lines point to longer-term process disruption. Feedstock price swings-aniline fell 36.81% year-on-year in 2025-add margin volatility, yet integrated producers remain better cushioned. Intensifying worker-exposure regulations and the capital intensity of new plants keep the competitive moat high and accelerate consolidation around technology-rich incumbents.

The Energy Performance of Buildings Directive obliges EU member states to invest EUR 3.5 trillion (USD 3.8 trillion) in energy upgrades by 2030. New builds must meet near-zero energy targets, while older stock faces mandatory deep retrofits that favor rigid polyurethane panels with thermal conductivity down to 0.022 W/m*K. Comparable rules in California's 2025 codes replicate this pull in North America. Building automation specifications further boost MDI consumption because advanced controls demand tighter thermal envelopes. The synergy between regulation and performance cements rigid foams as the highest-growth slice of the MDI market.

Post-pandemic vaccine logistics illustrated the cost of temperature excursions, pivoting pharma supply chains toward ultralow-temperature storage. India's subsidized cold-chain programs add greenfield warehouses that rely on polyurethane systems capable of -80 °C thermal integrity. Parallel food cold-chains, driven by urban lifestyle changes, upscale refrigerated transport and retail cases across ASEAN and Latin America. Higher performance specs elevate margin profiles for premium MDI grades, strengthening volume resilience even amid raw-material inflation.

The EU capped workplace exposure at 6 µg NCO/m3 and mandated certified training for all handlers. OSHA is following suit. Compliance forces investments in ventilation, monitoring and medical surveillance, raising fixed costs for spray-foam contractors and small appliance lines. The burden accelerates market consolidation toward capital-rich processors and biases demand toward low-monomer or prepolymer solutions that command price premiums but require formulation know-how.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Rigid foams contributed 36.78% of the MDI market size in 2025 and are expected to climb at a 5.63% CAGR to 2031. The category benefits from polyisocyanurate panels delivering best-in-class 0.022 W/m*K thermal conductivity, enabling compliance with net-zero standards in residential and commercial construction. Flexible foams maintain relevance in bedding and automotive seats, though maturity limits upside. Coatings and elastomers secure recurring demand from industrial maintenance and materials-handling applications, reinforcing baseline volumes. Emerging uses include EV battery encapsulants that need dimensional stability under thermal cycling, highlighting the versatility of MDI chemistry. Rigid foams' rising uptake in re-roofing and curtain-wall systems all but assures their continued dominance within the MDI market.

With building codes tightening globally, insurers and financiers are prescribing minimum R-values that only rigid polyurethane or PIR products can feasibly meet at slim wall sections. Recticel's Eurowall Impact board, featuring 25% bio-circular content, cut embodied CO2 by 43% without compromising thermal performance. Adhesives and sealants form a niche yet profitable sub-segment in automotive and infrastructure repair, where MDI imparts fast cure and structural bonding. Specialty elastomers carry weight in mining screens and industrial wheels, generating steady aftermarket revenue. Collectively, these sub-segments make rigid foams the linchpin of long-term growth for the MDI market.

The Methylene Diphenyl Di-Isocyanate (MDI) Market Report is Segmented by Application (Rigid Foams, Flexible Foams, Coatings, Elastomers, Adhesives and Sealants, and Others), End-User Industry (Construction, Furniture and Interiors, Electronics and Appliances, Automotive, Footwear, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific controlled 46.35% of the MDI market in 2025 and is projected to expand at a region-leading 5.90% CAGR to 2031. China's green-building codes and infrastructure boom absorb vast rigid-foam volumes, while India's vaccine logistics push inflate cold-storage capacity. Expansion projects, such as Kumho Mitsui's 200 kt debottlenecking that lifted its Yeosu complex to 610 kt, underpin local supply.

North America remains significant through retrofit incentives and the Section 45L tax credit that rewards high-performance residential buildings. Notably, Covestro supplies bio-circular MDI to Carlisle Construction Materials, cutting upstream carbon 99% relative to fossil-based grades. Local appliance makers also specify higher-density foams to satisfy 2025 energy rules, anchoring stable base demand.

Europe's policy leadership creates a synthetic pull exceeding organic growth. The EPBD's EUR 3.5 trillion retrofit agenda accelerates rigid-foam adoption, while the 6 µg exposure cap motivates formulators to shift toward low-monomer variants. Producer focus aligns with circularity: BASF separated its Shanghai joint venture to optimize its 1.9 million-ton global MDI grid, freeing assets for mass-balanced production. Meanwhile, Middle East and Africa register catch-up growth driven by logistics parks and climate-controlled agriculture, though most product still ships in from Europe and Asia.