ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

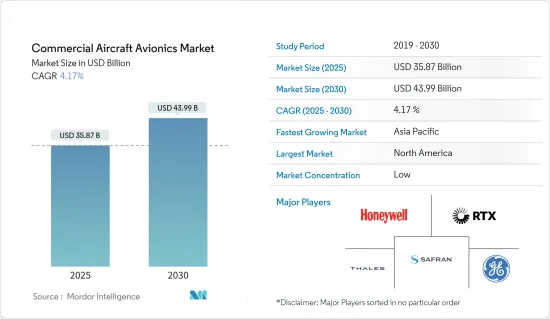

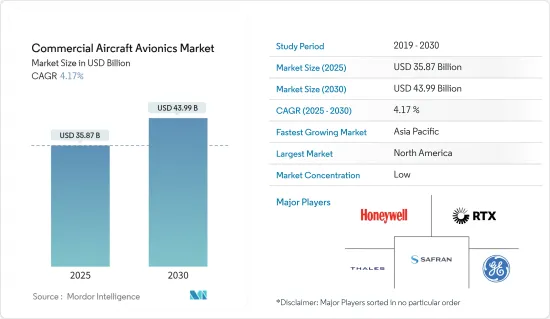

민간항공기 아비오닉스 시장 규모는 2025년에 358억 7,000만 달러, 2030년에는 439억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2025년-2030년) CAGR은 4.17%를 나타낼 전망입니다.

주요 하이라이트

세계의 항공 부문은 COVID-19 팬데믹으로 인해 전례 없는 혼란에 휩쓸려 여객 수송량이 격감해, 항공기 수요에 악영향을 미쳤습니다. 여행 수요가 2023년까지 코로나19 이전 수준으로 정상화될 것으로 예상되어 민간항공기 아비오닉스 시장의 성장에 어려움을 줄 것으로 보입니다.

항공 분야는 구조 및 전자 장비를 포함한 항공기 설계의 모든 측면을 규정하는 엄격한 규제에 의해 관리되고 있습니다.

이 시장은 이 지역을 운항하는 항공사가 시작한 기체 확대 및 근대화 프로그램의 일환으로 신형 민간 항공기 수요가 회복됨에 따라 견인되고 있습니다. 정비를 가능하게 하는 기술력을 촉진할 것으로 예상됩니다.그러나, COVID-19에 의한 와이드 바디기의 조기 퇴역은 네로우 바디기보다 와이드 바디기의 아비오닉스 시스템의 사이즈와 설치 비용이 훨씬 높기 때문에 아비오닉스 레트로 피트 분야에 영향을 줄 것으로 예상됩니다.

민간항공기 아비오닉스 시스템 시장 동향

예측 기간 동안 좁은 바디 부문이 시장을 독점

민간항공기 아비오닉스 시장은 협폭동체 부문이 지배적입니다. 항공기 수요는 증가할 것으로 예상됩니다.

예를 들어, 2021년 12월, 에어프랑스-KLM 네덜란드 항공은 에어버스 A320 네오 패밀리 100기와 추가 60기의 옵션 발주를 발표했습니다. MAX 소동은 보잉사 시장 전망을 저해했지만, FA로부터의 재인증이 성공한 것으로, B737 MAX기 수요가 회복하기 시작하고 있습니다.

예를 들어 2022년 1월 보잉은 카타르항공에서 737 MAX 10개를 25대, 추가 25대 구입하는 옵션과 함께 대규모 수주했다고 발표했습니다. GE 에비에이션, 콜린스 에어로스페이스, L3해리스 테크놀로지스, 하니웰 인터내셔널, 코브햄 PLC와 같은 회사들은 보잉 737 및 777 항공기 제품군에 항공 전자 부품을 공급합니다.

북미가 시장에서 가장 높은 점유율을 차지

이 지역의 항공우주산업은 성숙하고 있으며, 견고한 항공기반에 강하게 지지되고 있습니다.

원재료의 입수가능성, 정치적 안정성, 생산비용이 낮다는 요인이 이 지역에서 새로운 항공우주제조시설의 설립을 뒷받침하고 있습니다.

에어버스는 2022년 초에 A220형기의 생산수를 월산 6기 정도로 늘릴 것이라고 발표했습니다. 에어버스는 2025년까지 A220의 생산 능력을 14대(미라벨 공장에서 매월 10대, 모빌 공장에서 매월 4대)로 끌어올리는 것을 목표로 하고 있습니다. 미국에 본사를 둔 고객 4개, 즉 제트 블루, 델타 항공, 브리즈 에어웨이스, 에어리스 코퍼레이션이 A220 프로그램의 수주 잔액의 절반 이상을 차지하고 있습니다. 레이세온 테크놀로지스는 온보드 컴퓨터, 날씨 매핑 레이더, 전자 비행 계기 시스템 등 A220에 통합된 어비오닉스 서브시스템의 대부분을 제공합니다. 이 지역의 다른 항공사도 유행 후 성장을 노리고 있습니다.

예를 들어, 유나이티드 항공은 2022년 12월, 787 드림 라이너 100대와 추가 100대를 추가하는 옵션이라는 미국 항공사에 의한 상업 항공 역사상 최대의 와이드 바디 기계 발주를 발표했습니다. 이 주문에 따라 유나이티드 항공은 2032년까지 700대의 신형 네로우 바디와 와이드 바디 머신의 납품을 예상하고, 2023년에는 주 평균 2대, 2024년에는 주 평균 3대의 납품을 전망하고 있습니다. 이러한 개발은 예측 기간 동안 북미 시장 전망을 밝게 만듭니다.

민간항공기 아비오닉스 시스템 산업 개요

민간항공기 아비오닉스 시장은 수많은 아비오닉스 시스템 제공업체가 존재하기 때문에 어느 정도 세분화되어 있습니다. Raytheon Technologies Corporation, General Electric Company, Honeywell International Inc., Safran, and THALES는 시장에서 유명한 기업의 일부입니다. 활발한 기업의 시장 점유율은 민간 항공기의 높은 납품에 의해 뒷받침됩니다. 표준 준수를 보장하는 고성능 아비오닉스 컴포넌트와 서브시스템의 끊임없는 연구개발에 의해 지원되고 있습니다.

예를 들어, 2023년 6월의 파리 에어쇼에서 엠브라엘 서비시즈 & 서포트사는 E제트기용의 차세대 버전의 항공기 건전성 분석 및 진단(AHEAD) 시스템을 발표했습니다.

The Commercial Aircraft Avionics Market size is estimated at USD 35.87 billion in 2025, and is expected to reach USD 43.99 billion by 2030, at a CAGR of 4.17% during the forecast period (2025-2030).

Key Highlights

The global aviation sector underwent an unprecedented disruption due to the COVID-19 pandemic, resulting in a drastic reduction in passenger traffic that negatively impacted aircraft demand. Though the sector showed signs of improvement in 2021, the deliveries of commercial aircraft were significantly lower than the pre-COVID levels. Furthermore, the commercial aviation sector is expected to recover slowly, as travel demand is projected to normalize to pre-COVID levels by 2023, which is expected to challenge the growth of the commercial aircraft avionics market.

The aviation sector is governed by stringent regulations that stipulate all aspects of aircraft design, including structures and electronics. Prominent aviation regulatory agencies, such as the Federal Aviation Administration (FAA), have issued strict guidelines for adherence by aircraft OEMs and third-party service providers regarding avionics systems fitment and repair.

The market is driven by the recovering demand for new commercial aircraft as part of the fleet expansion and modernization programs initiated by airlines operating in the region. Additionally, the increasing partnership between aircraft maintenance, repair, and operations (MRO) providers is expected to drive their technical capabilities, enabling them to service new-generation aircraft procured by airlines. However, the early retirement of widebody jets due to COVID-19 is anticipated to impact the avionics retrofit sector since the size and installation costs of avionics systems on a widebody are much higher than a narrowbody aircraft.

Commercial Aircraft Avionics Systems Market Trends

Narrowbody Segment to Dominate the Market During the Forecast Period

The narrowbody segment dominated the commercial aircraft avionics market. The demand for such aircraft is anticipated to increase as most low-cost carriers (LCCs) are trying to modernize their existing fleets to exploit new market opportunities and match the competencies of successive aircraft versions. Airbus, a commercial aircraft manufacturer, delivered 661 commercial aircraft in 2022, up from 609 in 2021. Also, Boeing delivered 480 commercial aircraft in 2022.

For instance, in December 2021, Air France-KLM announced an order for 100 Airbus A320 neo family aircraft, along with options for an additional 60 planes. The order consists of a mix of A320 neo and A321 neo aircraft, with the first deliveries expected in the second half of 2023. On the other hand, though the B737 MAX fiasco has hampered the market prospects for The Boeing Company, the successful recertification from the FAA has started driving back the demand for B737 MAX aircraft. Several airlines have started resuming operations on the 737 MAX jets and ordering new 737 MAX aircraft.

For instance, in January 2022, Boeing announced that it had won a major order from Qatar Airways for 25 737 Max 10 jets, along with options to buy 25 more aircraft. The airline also signed an order for 34 of the upcoming 777X, as well as options for 16 more jets. Companies like GE Aviation, Collins Aerospace, L3Harris Technologies Inc., Honewywell International Inc., and Cobham PLC provide avionic components for the Boeing 737 and 777 families of aircraft. The quicker recovery of domestic air passenger traffic is also anticipated to rake in new orders for the narrowbody aircraft, which may drive the growth prospects of avionics systems providers associated with the narrowbody programs.

North America Held Highest Shares in the Market

The aerospace industry in the region is mature and strongly supported by a robust aviation base. Higher air traffic has resulted in the procurement of several aircraft by regional and international airline operators. Boeing, one of the major aircraft original equipment manufacturers (OEMs) based in the United States, generates a huge demand for avionics systems.

Factors such as the availability of raw materials, political stability, and low production costs have driven the establishment of new aerospace manufacturing facilities in the region. Also, fluctuations in aviation fuel prices have triggered a surge in demand for fuel-efficient new-generation aircraft in North America. Hence, aircraft OEMs have started increasing their production capabilities to cope with the ever-increasing demand.

Airbus announced that it would increase the production rate of the A220 aircraft to around six per month in early 2022. It aims to increase the A220 production rate to 14 by 2025, i.e., 10 aircraft produced each month at its Mirabel facility and four at Mobile. Four United States-based customers, namely JetBlue, Delta Air Lines, Breeze Airways, and Air Lease Corporation, constitute more than half of the backlog of the A220 program. Raytheon Technologies Corporation provides a majority of avionics subsystems integrated into the A220, including onboard computers, weather mapping radar, and electronic flight instrument systems. Other airlines in the region are also looking for post-pandemic growth.

For instance, in December 2022, United Airlines announced its largest widebody aircraft order by a US carrier in commercial aviation history, for 100 new 787 Dreamliners plus options to add 100 more. With this order, the airline is now expecting new deliveries of 700 new narrowbody and widebody aircraft by 2032, on an average of 2 aircraft per week in 2023 and 3 aircraft per week in 2024. Such developments render a positive outlook for the market in North America during the forecast period.

Commercial Aircraft Avionics Systems Industry Overview

The commercial aircraft avionics market is moderately fragmented in nature due to the presence of a large number of avionics systems providers. Raytheon Technologies Corporation, General Electric Company, Honeywell International Inc., Safran, and THALES are some of the prominent players in the market. The market share of the active players is boosted by the high delivery volumes of commercial aircraft. The market dominance of key OEMs is supported through relentless R&D of high-performance avionic components and subsystems that render their products superior and ensure adherence to required safety standards. The availability of several variants and continuous product development cycles enables the enhanced operating life of such systems.

For instance, in June 2023, at the Paris Air Show, Embraer Services & Support launched the next-generation version of its aircraft health analysis and diagnosis (AHEAD) system for its E-Jets. This AHEAD system will integrate and analyze trends from several systems, such as landing gear, navigation, pneumatics, etc., and can detect anomalies and identify potential issues before they become critical.