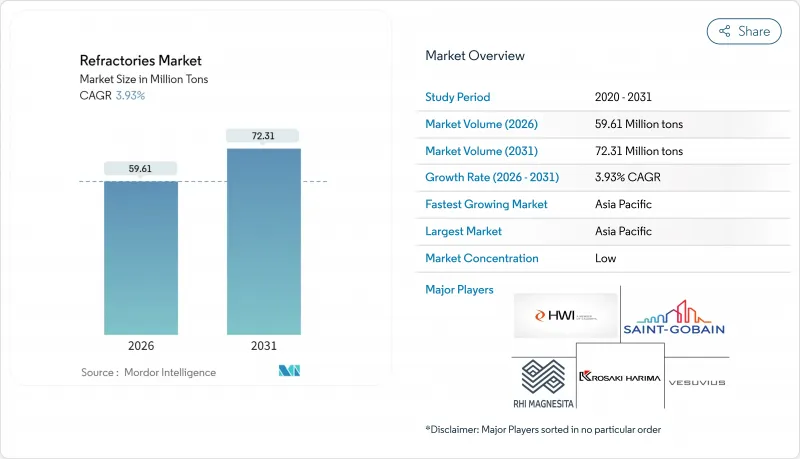

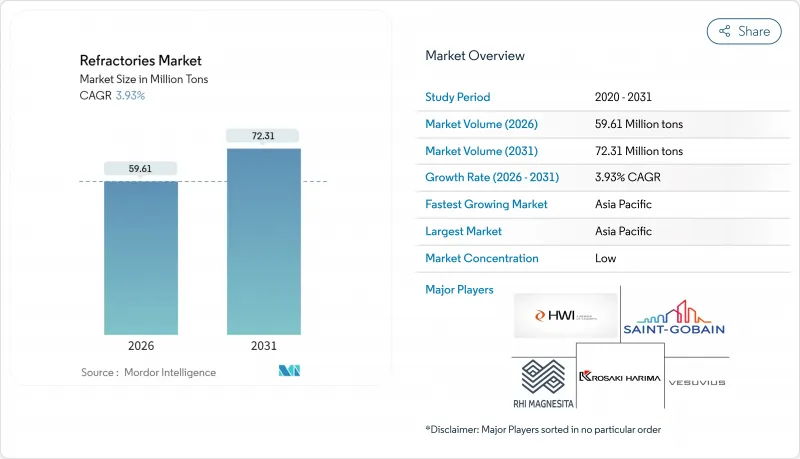

내화물 시장은 2025년 5,736만 톤에서 2026년에는 5,961만 톤으로 성장하고, 2026년에서 2031년에 걸쳐 CAGR 3.93%를 나타내, 2031년까지 7,231만 톤에 이를 것으로 예측되고 있습니다.

이 성장 추세는 내화물 시장이 변화하는 제철 기술, 확대되는 에너지 집약형 산업, 증가하는 규제 요건에 적응하는 능력을 반영합니다. 아시아 제철소의 생산 능력 확대, 수소 기반 직접 환원철(DRI)로로의 전환, 차세대 배터리, 시멘트, 폐기물 에너지화 시설의 규모 확대가 모두 단기적인 수요를 뒷받침하고 있습니다. 동시에 실리카 분진 배출 규제의 강화와 탄소 국경 조정세의 도입이 재료 기술 혁신을 가속화함과 동시에 주요 공급업체 간의 전략적 통합을 촉진하고 있습니다. 예를 들어 RHI 마그네시타는 판매 수량이 감소했음에도 불구하고 2023년 조정 후 EBITA를 전년 대비 7% 증가한 4억 900만 유로로 늘리고 있으며, 엄격한 가격 설정과 목표를 좁힌 인수가 경기 변동을 완화할 수 있음을 보여줍니다.

아시아 전역에서의 철강 생산 능력의 증강이 전례 없는 내화물 수요를 견인하고 있습니다. 중국에서는 2024년 상반기에 12기의 신고로(총생산능력 1,897만t)가 가동을 시작했습니다. 노후화된 설비를 고효율로로 대체함으로써 가동기간의 연장이 예상되는 한편, 열부하가 증대하기 때문에 내화물 시장에서는 고품위 마그네시아 카본 제품이나 모놀리식 솔루션의 개발이 급선무가 되고 있습니다. 인도의 급성장도 마찬가지로 중요합니다. RHI 마그네시타 인디아사는 2023-2024년도에 3,781캐롤 루피(4억 5,300만 달러)의 수익을 계상해, 9거점에서 700사 이상의 고객에게 서비스를 제공하며 국내 수요의 깊이를 부각했습니다. 지역 집중화는 리드 타임 단축으로 현지 생산자에게 이익을 가져오는 한편, 구미 공급업체의 점유율 유지를 과제로 하고 있습니다. 한편, 한국의 생산량은 2024년에 5.7% 감소하여 내화물 시장 전체에 있어서 성장의 불균형을 부각했습니다.

수소 기반 DRI(직접 환원철)는 온도 프로파일과 분위기를 변화시키기 때문에 우수한 내열 충격성과 수소 취화 내성을 갖춘 내화물이 필요합니다. 마그네시아사의 조사에 의하면, “그린·스틸”용 전기 용해로에는 수소 풍부한 가스에 견딜 수 있는 새로운 내화물 화학 조성이 요구됩니다. 이 공정은 제강시의 CO2 배출량을 강철 1톤당 0.1톤까지 줄일 수 있지만, 설비 투자와 에너지 가격의 장벽은 여전히 존재합니다. 2025년 아르세롤 미탈사가 독일 프로젝트에서 철수하고 13억 유로의 보조금 반환을 실시한 것은 경제적인 불확실성을 돋보이게 합니다. 그러나 에너지경제연구소는 2050년까지 DRI용 철광석 수요가 10배로 증가할 것으로 예측하고 있으며 특수 DRI 내화물에 장기적인 기회를 제시하고 있습니다.

EU의 탄소 국경 조정세와 북미의 탈탄소화 정책에 의해 종래의 마그네시아·카본 벽돌 수요가 억제되고 있습니다. 수명주기 평가는 무탄소 마그네시아 대체품이 환경 부하를 줄이는 것을 보여주지만, 산업 수준에서 광범위한 입증이 여전히 필요합니다. 미국의 중국·멕시코산 마그네시아·카본 벽돌에 대한 반덤핑 관세(일부 생산자로 236%에 달한다)는 비용 압력을 가해 내화물 시장을 저탄소 솔루션으로 이끌고 있습니다. RHI 마그네시타사의 고리사이클 마그네디아 카본 시리즈는 잠정적인 옵션을 제공하지만, 장기적인 방향성으로는 카본 프리의 결합제나 세라믹 매트릭스 복합재가 우위입니다.

비점토질 내화물은 조사 기간 동안 CAGR 4.57%로 확대되어 2031년까지 점토질 제품을 초과하는 성장을 계속합니다. 수소 베이스 제강, 선진 전지, 폐기물 소각 발전에 있어서 내식성·내열 충격성의 우위성이 성장의 기반입니다. 마그네시아 벽돌은 슬래그 화학에 대한 내성으로부터 기초제강으로 주류를 차지하고, 지르코니아 벽돌은 가혹한 사이클 환경이나 극고온 영역에서 뛰어난 성능을 발휘합니다. 규산염 벽돌은 코크스로의 체커 벽에 불가결합니다만, 결정성 실리카 노출 규제(분진 농도 50μg/m3 상한)에 의해 사용은 억제되고 있습니다. 크롬산염 벽돌은 우수한 금속 침투 저항성에 의해 비철 금속 제련 분야에서의 지위를 유지. 점토질 내화물이 출하량으로 우위를 유지하고 있는 가운데, 이러한 비점토계 카테고리가 가치 성장을 지지하고 있습니다.

고알루미나 질 내화물을 포함한 점토질 내화물은 2025년 내화물 시장 점유율의 54.88%를 차지하여 다양한 로 내장재에 있어서 비용 효율의 높이를 나타냈습니다. 내화 점토 벽돌은 중온의 냄비와 보일러에 사용되며 단열 내화물은 산업 전체에서 에너지 절약을 실현합니다. 연구자들은 플라이 애쉬계 지오폴리머 벽돌에 있어서 1,100℃의 소성 후 84MPa의 압축 강도를 달성해, 점토질 내화물의 순환형 경제에의 길을 시사하고 있습니다. 산고반의 초고온 세라믹, 특히 SiC(탄화규소)와 지르코니아는 1,400℃를 넘는 성능 한계를 밀어 올려 하이브리드 배합이 종래의 점토계/비점토계의 경계를 모호하게 하는 실례를 나타내고 있습니다.

내화물 시장 보고서는 제품 유형(비점토질 내화물 및 점토질 내화물), 최종 사용자 산업(철강, 시멘트, 에너지 및 화학, 비철금속, 유리, 세라믹 및 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)으로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

2025년 시점에서 아시아태평양은 내화물 시장의 73.20%를 차지했고 2031년까지 연평균 복합 성장률(CAGR) 4.12%를 나타낼 것으로 전망됩니다. 중국에서는 고로의 근대화가 진행되고 있는 한편, 구식 설비의 폐쇄에 의해 고품위 내화 벽돌·캐스터블 수요가 지속적으로 증가하고 있습니다. 인도는 기타 국가를 크게 웃도는 성장을 보이고 있으며, RHI 마그네시타의 CEO는 국내 내화물 시장의 연간 성장률을 6-13%로 예측됩니다. 이것은 대규모 철강 및 시멘트 확장을 반영합니다. 일본에서는 JFE 홀딩스에 의한 22억 6,000만 달러의 투자를 배경으로 전기로 기술로의 이행이 진행되어, 내장 사양이 전기로 최적화 기본 혼합물로 전환하고 있습니다. 한국에서는 2024년 5.7%의 생산 감소가 보였지만 여전히 고품질 내화물이 필요한 고부가가치 강재 제품으로의 전환을 목표로 하고 있습니다. 중국과 동남아시아 전역에서 리튬 이온 배터리 기가팩토리 건설의 가속은 이 지역이 내화물 시장의 성장 핵심 역할을 확고히 하고 있습니다.

북미는 성숙하면서도 전략적으로 중요한 시장으로 남아 있습니다. 하비슨 워커 인터내셔널 사가 미주리 주 풀턴에서 실시하는 1,390만 달러의 확장 계획은 경량 모놀리식 제품의 생산량을 60% 증가시켜, 이 지역의 고부가가치 용도에 대한 대처를 구현하고 있습니다. OSHA(미국노동안전보건국)의 실리카 분진규제 강화는 밀폐식 처리기술과 저분진재료에 대한 투자를 촉진하고 제품 포트폴리오의 재구축을 촉진하고 있습니다. 캐나다는 녹색철 수출에서 주도권 획득을 목표로 하며, 이는 특수 DRI용 내화물 수요를 자극할 수 있습니다. 한편, 멕시코의 경쟁력은 마그네슘 탄소 벽돌의 비용을 밀어 올리는 미국의 반 덤핑 관세에 의해 억제됩니다.

유럽은 환경정책의 선도역을 담당하고 있습니다. EU 탄소 국경 조정 메커니즘은 고탄소 내화물 비용을 밀어 올려 탄소 프리 본드 및 재활용 솔루션의 도입을 촉진합니다. 알세롤미탈사가 독일의 수소제강 프로젝트를 위한 보조금 13억 유로를 반환한 결정은 녹색이행에 따른 경제적 부담을 여실히 보여줍니다. 그러나 연구개발 파이프라인은 견조합니다. 산고방의 뉴욕주 위트필드에 계획된 4,000만 달러의 NorPro 공장은 미국에 거점을 두면서도 유럽의 촉매 공급을 담당하고 대서양을 가로지르는 공급망 통합을 강조하고 있습니다. 중동 및 아프리카는 사우디아라비아의 산업 다각화와 남아프리카 광업 사업을 통해 새로운 잠재력을 보여주지만 정치적 확실성과 인프라 부족은 프로젝트 진행에 영향을 미칩니다.

The Refractories Market is expected to grow from 57.36 Million tons in 2025 to 59.61 Million tons in 2026 and is forecast to reach 72.31 Million tons by 2031 at 3.93% CAGR over 2026-2031.

This forward momentum reflects the ability of the refractories market to adapt to shifting steelmaking technologies, expanding energy-intensive industries, and rising regulatory expectations. Capacity expansions across Asian steel plants, the pivot toward hydrogen-based direct-reduced-iron (DRI) furnaces, and the scale-up of next-generation battery, cement, and waste-to-energy facilities all reinforce near-term demand. At the same time, tighter silica-dust limits and carbon-border tariffs are accelerating materials innovation and spurring strategic consolidation among leading suppliers. RHI Magnesita, for example, delivered 7% growth in 2023 Adjusted EBITA to EUR 409 million despite softer volumes, underscoring how disciplined pricing and targeted acquisitions can buffer cyclical swings.

Steel capacity additions across Asia are driving unprecedented refractory demand, with China commissioning 12 new blast furnaces totaling 18.97 million tons in H1 2024. Replacing aging units with high-efficiency furnaces lengthens campaign life expectations and raises thermal loads, prompting the refractories market to innovate higher-grade magnesia-carbon and monolithic solutions. India's surge is equally pivotal; RHI Magnesita India posted INR 3,781 crore (USD 453 million) FY 2023-24 revenue while serving more than 700 customers across nine sites, highlighting the depth of domestic pull. Regional concentration benefits local producers through shorter lead times yet challenges Western suppliers to sustain share. Meanwhile, Korean production fell 5.7% in 2024, underscoring uneven growth within the broader refractories market.

Hydrogen-based DRI alters temperature profiles and atmospheres, demanding refractories with superior thermal-shock resistance and hydrogen embrittlement resilienceMagnesita research confirms that electric melting furnaces intended for "green steel" require novel refractory chemistries capable of withstanding hydrogen-rich gases. Although the process can slash steelmaking CO2 emissions to 0.1 tons per ton of steel, capex and energy-price hurdles persist; ArcelorMittal's 2025 withdrawal from a German project and return of EUR 1.3 billion in subsidies highlights the economic uncertainties. Nevertheless, the Institute for Energy Economics forecasts a ten-fold rise in DR-grade iron ore demand by 2050, signaling long-run opportunities for specialized DRI refractories,

EU carbon-border tariffs and North American decarbonization policies are curbing demand for traditional magnesia-carbon bricks. Life-cycle assessments show that carbonless magnesia alternatives deliver lower environmental impacts but still need broader industrial validation. US antidumping duties on certain Chinese and Mexican mag-carbon bricks-reaching 236% for some producers-add cost pressure and push the refractories market toward lower-carbon solutions. RHI Magnesita's high-recycling mag-carbon series offers an interim path, yet long-term trajectories favor carbon-free bonds and ceramic-matrix composites.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Non-clay refractories grew at a 4.57% CAGR during the review period and continue to outpace clay grades through 2031. They thrive on superior corrosion and thermal-shock resistance critical in hydrogen-based steelmaking, advanced batteries, and waste-to-energy incinerators. Magnesite bricks dominate basic steelmaking for their resistance to slag chemistry, while zirconia bricks excel in severe cycling and extremely high temperature zones. Silica bricks remain indispensable for coke-oven checker walls, yet usage is moderated by rising crystalline-silica exposure rules capping dust at 50 µg/m3. Chromite bricks maintain a foothold in non-ferrous smelting thanks to strong metal-penetration resistance. Together, these non-clay categories underpin value growth even as clay refractories retain volume leadership.

Clay refractories, topped by high-alumina variants, captured 54.88% of refractories market share in 2025, reflecting their cost-effectiveness across multiple furnace linings. Fireclay bricks serve moderate-temperature ladles and boilers, while insulating refractories unlock energy savings across industries. Researchers have achieved 84 MPa compressive strength in fly-ash geopolymer bricks after 1,100 °C exposure, hinting at circular-economy pathways for clay refractories. Saint-Gobain's ultra-high-temperature ceramics, particularly SiC and zirconia, stretch performance ceilings above 1,400 °C and illustrate how hybrid formulations blur the traditional clay/non-clay divide.

The Refractories Market Report is Segmented by Product Type (Non-Clay Refractories and Clay Refractories), End-User Industry (Iron and Steel, Cement, Energy and Chemicals, Non-Ferrous Metals, Glass, Ceramic, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific owned 73.20% of the refractories market in 2025 and is slated to grow at a 4.12% CAGR through 2031. China continues modernizing blast furnaces while shutting obsolete capacity, driving sustained uptake of higher-grade bricks and castables. India outpaces all peers; RHI Magnesita's CEO forecasts 6-13% annual domestic refractory growth, reflecting large-scale steel and cement expansions. Japan's shift toward EAF technology, supported by JFE Holdings' USD 2.26 billion investment, redirects lining specifications toward EAF-optimized basic mixes. South Korea encountered a 5.7% production dip in 2024 but aims to pivot toward higher-value steel products that still require premium refractories. Accelerating lithium-ion battery gigafactory construction across China and Southeast Asia cements the region's role as the growth nucleus of the refractories market.

North America remains a mature yet strategically vital arena. HarbisonWalker International's USD 13.9 million expansion in Fulton, Missouri, will lift lightweight monolithic output by 60% and embodies the region's commitment to high-value applications. Heightened OSHA silica-dust limits incentivize investment in sealed handling and low-dust materials, reshaping product portfolios. Canada eyes leadership in green-iron exports, which could stimulate specialized DRI refractory demand. Mexico's competitiveness, however, is tempered by US antidumping duties that inflate costs for mag-carbon bricks.

Europe sets the pace on environmental policy. The EU Carbon Border Adjustment Mechanism raises the cost of high-carbon refractories, propelling adoption of carbon-free bonds and recycling solutions. ArcelorMittal's decision to return EUR 1.3 billion in subsidies for a German hydrogen-steel project illustrates the economic strain in the green transition. Yet R&D pipelines stay robust; Saint-Gobain's planned USD 40 million NorPro plant in Wheatfield, New York, although US-based, will serve European catalysts and emphasizes trans-Atlantic supply-chain integration. The Middle East and Africa offer emergent promise through Saudi industrial diversification and South African mining ventures, although political certainty and infrastructure gaps influence project pacing.