ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

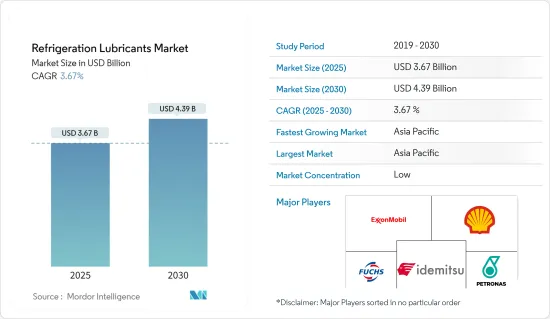

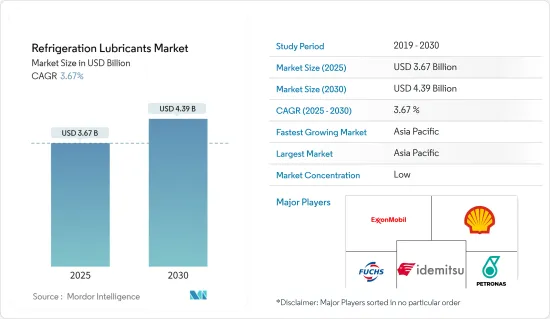

냉동기유 시장 규모는 2025년에 36억 7,000만 달러로 추정 예측되며 예측 기간(2025-2030년) 동안 CAGR 3.67%로 성장하여 2030년에는 43억 9,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 발생으로 세계적인 봉쇄 조치, 제조 활동 및 공급망의 혼란, 생산 정지 사태가 발생하여 조사 대상 시장에 악영향을 미쳤습니다. 그러나 2021년에는 상황이 회복되면서 예측 기간 동안 시장의 성장 궤도가 회복될 것으로 기대됩니다.

주요 하이라이트

에너지 효율에 최적화된 차세대 냉동기유의 출현, 세계 HVACR 산업의 기세 증가, 그리고 자동차 산업의 회복이 냉동기유 시장의 성장을 이끌 것으로 예상됩니다.

반면 끊임없는 규제 개정에 의한 기존 냉매의 단계적 폐지가 시장 성장을 방해할 것으로 예상됩니다.

나노 윤활 기술에 대한 관심 증가와 극저온 용도에 대한 수요 증가는 조사된 시장에 새로운 기회를 가져올 것으로 예상됩니다.

아시아태평양은 세계 시장을 독점하며 인도와 중국과 같은 국가에서 소비가 가장 큽니다.

냉동기유 시장 동향

세계 HVACR 산업의 기세 증가

에어컨(AC) 유닛은 밀폐된 공간의 습도와 온도를 조정하도록 설계되었습니다. 에어컨의 주요 구성요소는 압축기, 증발기, 팽창 밸브, 응축기입니다.

냉동기유에는 열 제거, 가동 부품의 윤활, 실란트로서의 역할, 컴프레서의 중요 부품의 냉각 등 복수의 목적이 있습니다.

국제에너지기구(IEA)에 따르면 2021년에는 모든 건축물의 최종 용도 중에서 공간 냉방 수요가 가장 높은 연간 성장률을 기록면서 건축물 부문의 최종 전력 소비량(약 2,000 TWh)의 16% 가까이를 차지하게 되었습니다.

인도 정부는 2021년 11월, 백색 가전의 생산 연동형 장려금(PLI) 제도로 26건의 신청서를 선정했습니다. 이들은 에어컨(AC) 제조용이며 3,898크로르 루피의 투자가 보장되었습니다.

전기차 동향의 고조는 냉동기유 시장을 더욱 뒷받침할 가능성이 높습니다.

인도의 전기자동차 시장은 2021년에 48% 이상을 차지한 이륜차 부문이 주된 견인역입니다.

위의 요인은 냉동기유 시장에 긍정적인 영향을 미칠 것으로 보입니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 냉동기유의 최대 시장입니다. 냉동기유 수요가 증가하고 있는 것은 가정용 및 산업용 공조 시스템의 사용이 증가하고 있기 때문입니다.

중국은 세계 최대의 자동차 허브입니다. OICA에 따르면, 2021년 동국의 자동차 생산 대수는 전체적으로 2,608만 2,220대였으며 2020년보다 3% 증가했습니다.

중국의 주요 전기자동차 제조업체에는 테슬라, BYD, Nio 등이 있습니다.

OICA의 보고서에 따르면 2021년 1분기부터 3분기까지의 유럽의 생산 대수는 1,188만 6,776대인 반면 중국은 동기간에 1,824만 2,588대를 생산했습니다.

한국자동차기술연구원(KAII)이 수집한 데이터에 따르면 2021년 1-9월 한국의 전기자동차 판매 대수는 96% 증가한 7만 1,006대로 급증했습니다.

2021년, 인도의 제1-3분기 전기자동차 생산 대수는 328만 9,683대로 2020년보다 53%의 대폭적인 증가를 달성하였습니다.

인도는 미국, 러시아, 중국에 이어 세계에서 가장 규모가 큰 철도 시스템으로 4위이며, 선로의 길이는 123,542km, 노선의 길이는 67,415km, 역의 수는 7,300곳 이상입니다.

세계 제2위의 인구를 자랑하는 이 나라의 철도망에서는 13,523개의 여객 열차와 9,146개의 화물 열차가 정기적으로 운행되고 있습니다.

위와 같은 요인으로 아시아태평양이 향후 수년간 시장을 독점할 것으로 예상됩니다.

냉동기유 산업 개요

냉동기유 시장은 각국의 다양한 배기가스 규제로 인해 세분화가 진행되고 있습니다. 시장의 주요 기업(순서부동)에는 ExxonMobil Corporation, Shell PLC, Fuchs, IdemitsuKosan Co. Ltd, PETRONAS Lubricants International 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

에너지 효율에 최적화된 차세대 냉동기유의 등장

세계 HVACR 산업의 기세 증가

자동차산업의 회복

억제요인

규제 강화에 의한 기존 냉매의 단계적 폐지

업계 밸류체인 분석

Porter's Five Forces 분석

공급자의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

베이스 오일별

광유 윤활유

파라핀계 오일

나프텐계 오일

방향족 오일

합성 윤활유별

합성탄화수소

폴리알파올레핀(PAO)

알킬화 방향족

폴리부텐

에스테르별

디에스테르

폴리올 에스테르

인산 에스테르

폴리머 에스테르

폴리알킬렌글리콜(PAG)

기타 합성 윤활유

용도별

에어컨

수송

자동차

기타 수송수단(철도, 항공, 선박)

기타 공조 용도(설치형)

냉동(가정용, 공업용, 극저온용)

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

BASF SE

BP PLC

BVA Oil

Chevron Corporation

China National Petroleum Corporation

China Petroleum & Chemical Corporation(SINOPEC Group)

CPI Fluid Engineering

ENEOS Corporation

ExxonMobil Corporation

Fuchs

HP Lubricants

Idemitsu Kosan Co. Ltd

Isel

Kluber Lubrication

Kuwait Petroleum

Matrix Specialty Lubricants BV

Parker Hannfin Corp

PETRONAS Lubricants International

Shell plc

Tazzetti SpA

TotalEnergies

Xaerus Performance Fluids International

제7장 시장 기회와 미래 동향

나노 윤활 기술에 대한 주목 고조

극저온 용도 수요 증가

CSM

영문 목차

영문목차

The Refrigeration Lubricants Market size is estimated at USD 3.67 billion in 2025, and is expected to reach USD 4.39 billion by 2030, at a CAGR of 3.67% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns around the globe, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market studied. However, the conditions started recovering in 2021, which is expected to restore the market's growth trajectory during the forecast period.

Key Highlights

The emergence of new-generation refrigeration lubricants optimized for energy efficiency, increasing momentum in the global HVACR industry, and recovering automotive industry are expected to drive the growth of the refrigeration lubricants market.

On the flip side, phasing out of existing refrigerants due to constant regulations amendments is expected to hinder the market's growth.

Augmenting prominence for nano lubricant technology and a gain in demand for cryogenic applications are expected to unveil new opportunities for the market studied.

Asia-Pacific dominated the global market, with the most significant consumption from the countries such as India and China.

Refrigeration Lubricants Market Trends

Increasing Momentum in the Global HVACR Industry

Air conditioning (AC) units are designed to modify humidity and air temperature in an enclosed area. The primary components of an air conditioner are compressor, evaporator, expansion valve, and condenser. Lubricants reduce side effects, such as pipeline corrosion, and provide better compatibility with common refrigeration gases.

Refrigeration lubricants have multiple purposes, such as removing heat, lubricating moving parts, acting as a sealant, and cooling the critical components of compressors.

According to the International Energy Agency, space cooling demand experienced the highest annual growth among all buildings end uses in 2021 and accounted for nearly 16% of the buildings sector's final electricity consumption (about 2 000 TWh). This is expected to benefit the air conditioning lubricant market over the forecast period.

The Government of India, in November 2021, selected 26 applications under the production-linked incentive (PLI) scheme for white goods. These are for air-conditioning (AC) manufacturing with a committed investment of INR 3,898 crore. This initiative is likely to boost production in the country and have a positive impact on the refrigeration lubricants market.

The rising trends for electric vehicles are further likely to support the refrigeration lubricant market. China was the leading producer of electric vehicles in 2021. According to the China Passenger Car Association (CPCA), the country sold over 3.3 million units in 2021, which also accounted for an increase of 169% compared to 2020.

The electric vehicles market in India is majorly driven by the two-wheeler segment that accounted for over 48% in 2021. According to the Ministry of Road Transport & Highways (MoRTH), 3,29,190 electric vehicles were sold in the country, representing an increase of 168% compared to the sales in 2020.

The factors mentioned above are likely to impact the refrigeration lubricants market positively.

Asia-Pacific is Expected to Dominate the Market

The Asia-Pacific region was the largest market for refrigeration lubricants. The rising demand for refrigeration lubricants can be attributed to the increasing usage of air conditioning systems for domestic and industrial applications.

China is the largest automotive hub in the world. According to OICA, the overall automotive production in the country in 2021 stood at 2,60,82,220, a 3% increase from 2020.

China's leading electric car manufacturers include Tesla, BYD Co., and Nio Inc. The growing demand for electric vehicles in the country is driving the market for refrigeration lubricants for automotive compressors.

As per the report by OICA, Europe produced 11,886,776 units from quarter 1 to quarter 3 of 2021, whereas China produced 18,242,588 vehicles in the same period. Therefore the demand for AC in automobiles continues to increase.

South Korean sales of electric vehicles surged by 96% to 71,006 units in the first nine months of 2021, according to data collected by the Korea Automotive Technology Institute (KAII). The sales figure is further expected to increase with growing demand from the importing economies in Europe, Asia Pacific, and the Americas.

In 2021, India produced 32,89,683 electric vehicles for the first three quarters of 2021, a massive increase of 53% from 2020. The growing automotive sector is expected to augment the market in the forecast period.

India ranks fourth in the most extensive railway system in the world after the United States, Russia, and China, with 123,542 km of tracks, 67,415 km of route, and more than 7,300 stations.

The second-largest populated country in the world runs 13,523 passenger trains and 9,146 freight trains regularly on its network. The railways carried 1.23 billion metric tons of freight in FY2020-FY2021.

Due to all the factors above, Asia-Pacific is expected to dominate the market in the upcoming years.

Refrigeration Lubricants Industry Overview

The refrigeration lubricants market has a higher degree of fragmentation owing to multiple emission regulations in various countries. Key players (not in any particular order) in the market include ExxonMobil Corporation, Shell PLC, Fuchs, IdemitsuKosan Co. Ltd, and PETRONAS Lubricants International.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Emergence of New Generation Refrigeration Lubricants Optimized for Energy Efficiency

4.1.2 Increasing Momentum in the Global HVACR Industry

4.1.3 Recovering Automotive Industry

4.2 Restraints

4.2.1 Phasing out of Existing Refrigerants due to Constant Regulations Amendments

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

5.1 By Base Oil

5.1.1 Mineral Oil Lubricant

5.1.1.1 Paraffinic Oil

5.1.1.2 Naphthenic Oil

5.1.1.3 Aromatic Oil

5.1.2 By Synthetic Lubricant

5.1.2.1 Synthetic Hydrocarbon

5.1.2.1.1 Polyalphaolefin (PAO)

5.1.2.1.2 Alkylated Aromatics

5.1.2.1.3 Polybutene

5.1.2.2 By Ester

5.1.2.2.1 Diester

5.1.2.2.2 Polyol Ester

5.1.2.2.3 Phosphate Ester

5.1.2.2.4 Polymer Ester

5.1.2.3 Polyalkylene Glycols (PAG)

5.1.2.4 Other Synthetic Lubricants

5.2 By Application

5.2.1 Air Conditioning

5.2.1.1 Transportation

5.2.1.1.1 Automotive

5.2.1.1.2 Other Modes of Transportation (Rail Road, Airways, and Marine)

5.2.1.2 Other Air Conditioning Applications (Stationary Applications)

5.2.2 Refrigeration (Household, Industrial, and Cryogenics)

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BASF SE

6.4.2 BP PLC

6.4.3 BVA Oil

6.4.4 Chevron Corporation

6.4.5 China National Petroleum Corporation

6.4.6 China Petroleum & Chemical Corporation (SINOPEC Group)

6.4.7 CPI Fluid Engineering

6.4.8 ENEOS Corporation

6.4.9 ExxonMobil Corporation

6.4.10 Fuchs

6.4.11 HP Lubricants

6.4.12 Idemitsu Kosan Co. Ltd

6.4.13 Isel

6.4.14 Kluber Lubrication

6.4.15 Kuwait Petroleum

6.4.16 Matrix Specialty Lubricants B.V.

6.4.17 Parker Hannfin Corp

6.4.18 PETRONAS Lubricants International

6.4.19 Shell plc

6.4.20 Tazzetti S.p.A

6.4.21 TotalEnergies

6.4.22 Xaerus Performance Fluids International

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Augmenting Prominence for Nano Lubricant Technology