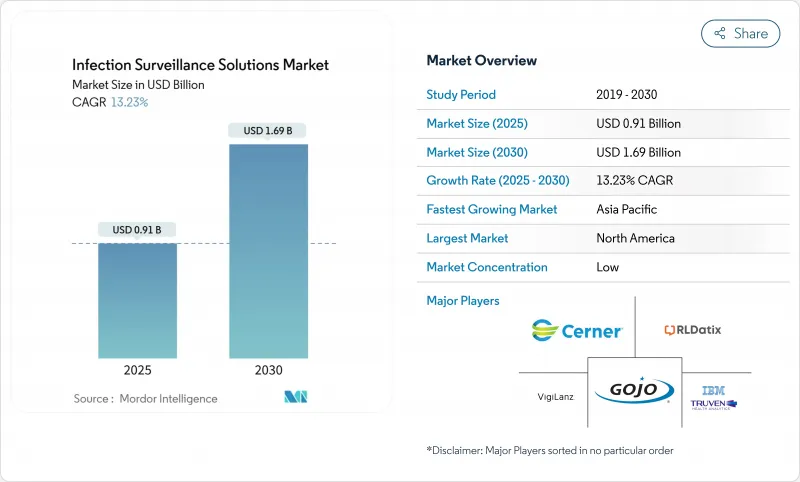

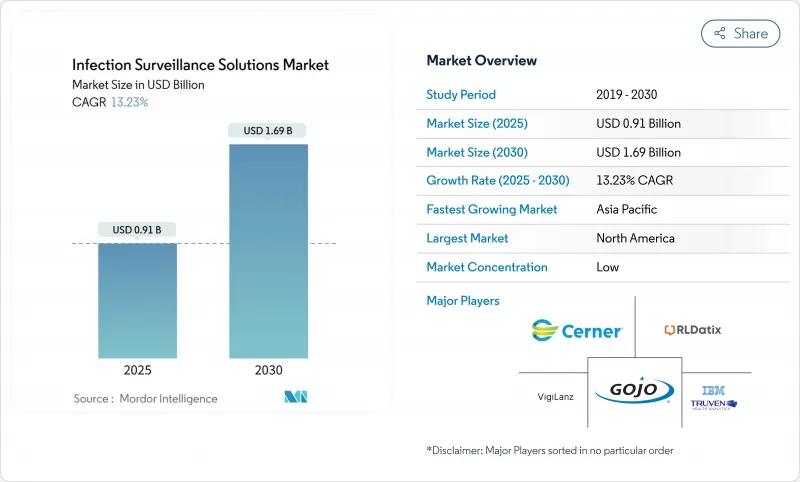

감염 감시 솔루션 시장 규모는 2025년에 9억 1,000만 달러, 2030년에는 16억 9,000만 달러에 이를 것으로 예상되고 있으며, 유행에 따라 배운 디지털 감염 제어 워크플로우를 의료 제공자가 제도화함으로써 CAGR은 13.2%를 나타낼 전망입니다.

의료 관련 감염(HAI) 데이터의 전자 제출을 의무화하는 미국과 EU의 새로운 규칙, 가치 기반 상환 엄격화, 패혈증 검출 시간을 단축하는 AI 기반 조기 경고 알고리즘의 급속한 보급이 확대를 뒷받침합니다. 병원은 호흡기 질환 보고와 관련된 CMS의 처벌을 피하기 위해 지출을 가속화하고, 소규모 시설은 2024년 변경 건강 관리의 침해에 이어 사이버 보안의 두려움에도 불구하고 자본 예산을 줄이는 클라우드 구독으로 이어졌습니다. 벤더는 EHR과의 상호 운용성, HL7-FHIR에 대한 대응, 내장된 예측 분석으로 차별화를 도모하고 있으며, 대부분은 인력 부족을 해소하기 위해 코어 소프트웨어에 매니지드 서비스를 거듭하려고 하고 있습니다. 전반적으로 감염 감시 솔루션 시장은 디지털 감시를 "nice-to-have"에서 필수 임상 인프라로 바꾸는 규제, 경제 및 기술의 융합으로부터 이익을 얻고 있습니다.

의료 관련 감염으로 인해 미국 병원은 연간 250-450억 달러의 손실을 입었으며, 감시 투자는 경제적으로 필수적입니다. CMS는 2025년도의 규칙집으로 카테터 관련 요로 결석과 중심 정맥 라인 감염에 대한 새로운 품질 평가 지표를 최종 결정하고 유럽 의료 데이터 공간은 2029년까지 27개 회원국에서 표준화된 감염증 보고를 의무화할 예정입니다. 독일 시설에서는 1건의 원내 감염 에피소드를 예방함으로써 12일의 병상 추가를 피하고 390-650유로의 증수를 창출하고 있습니다. 벌칙이 강화됨에 따라 감염 감시 솔루션 시장은 비재량적인프라가 될 것입니다.

CMS의 병원 후유증 감소 프로그램은 가장 성적이 나쁜 1/4 병원에 1%의 지불 감소를 부과하고 수익을 감염 지표에 직접 연결시킵니다. 2024년 11월에 시행되는 새로운 참여 규칙에서 호흡기 질환의 주간 업로드가 의무화되고 의료기관은 보고의 자동화를 강요받았습니다. 일본에서는 인증된 EHR과 감시의 접속에 진료 보수의 증액이 부수되는 틀이 병행하여 도입되고 있습니다. 벌칙 또는 지불 여부라는 역학은 급성기부터 급성기까지 감염 감시 솔루션 시장 예측 가능한 수요를 창출합니다.

기본적인 EMR 도입에는 의료기관당 1만 3,100달러, 풀기능 감시에는 연간 5만 달러가 필요하며, 지방 병원에 있어서는 엄격한 숫자입니다. 그럼에도 HAI 회피와 진료 보상 획득으로 5년간의 순이익은 8만 6,400달러에 이릅니다. 미국에서는 지역 병원 도입을 조성하는 법이 제정될 예정이며, 클라우드 기반 SaaS는 비용과 이용 상황을 일치시켜 감염 감시 솔루션 시장에의 진입을 용이하게 합니다.

수술 부위 감염은 2024년에 4억 7,000만 달러 기여하고 감염 감시 솔루션 시장의 최대 슬라이스가 되었습니다. CMS의 처벌 구조와 공적 보고서를 통해 수술 지표는 경영진의 대시보드에 표시되며, 수술기 모니터링 모듈에 대한 투자가 유지됩니다. 인공지능을 활용 한 이미지 및 생체 신호 분석기는 몇 시간 이내에 상처 악화를 신고하고 규정 준수를 강화하고 재 입원 위험을 줄입니다. 한편, 혈류 감염은 머신러닝에 의한 패혈증 예측에 대한 지속적인 생리적 데이터 스트림 덕분에, 베이스는 작은 것, CAGR은 13.8%로 최고를 기록했습니다. 혈류 모니터링의 감염 감시 솔루션 시장 규모는 검증 연구에 의해 26%의 사망률 저하가 입증되었기 때문에 2030년까지 4억 1,000만 달러에 이를 것으로 예상되고 있습니다. 카테터 관련 요로 결석 및 인공 호흡기 관련 폐렴과 같은 다른 범주에는 장치 사용 상황을 감사하고 실시간으로 치료 순응도 알림을 푸시하는 침대 옆 대시보드가 유용합니다.

공급업체의 로드맵은 임상 우선순위의 차이에 따라 달라집니다. 수술실 모듈은 수술실 스케줄링 링크와 항균제 예방 타이머를 강조하며, 혈류 모듈은 실시간 검사 배양 및 항생제 스튜어드십 도구를 축으로 합니다. 전체 유전체 시퀀싱과 연계함으로써 감염의 유형에 병원체의 계통을 겹치는 통합 대시보드가 가능해지고 경계가 모호해질 가능성이 높습니다. 그럼에도 불구하고, 병원은 2030년까지 개별 분석 번들의 라이선스를 취득할 것으로 예상되며, 감염 감시 솔루션 시장은 여전히 유형별 수익원을 확보하게 됩니다.

소프트웨어 플랫폼은 2024년 매출 전체의 67.8%를 차지하고 의료 시스템이 통합 EHR 플러그인을 선호하기 때문에 계속 RFP의 대부분을 차지했습니다. 시장 맵자는 감염 관리 팀이 프로그래머 지원 없이 경보 임계값을 미세 조정할 수 있도록 로우코드 구성에 투자하고 있습니다. 그러나 시설은 규칙 튜닝, 보고, AI 모델의 재교육을 아웃소싱하기 때문에 서비스 수입은 14.7%라는 빠른 속도로 증가하고 있습니다. 매니지드 서비스 제공업체는 24시간 365일 모니터링, 규제 업데이트, 애널리틱스 인력을 패키징하고 자원에 제약이 있는 세이프티넷 병원에 호소하고 있습니다. 그 결과, 서비스로 인한 감염 감시 솔루션 시장 규모는 2030년까지 6억 2,000만 달러에 달할 수 있어 기존 제품 대 서비스의 구별이 모호해집니다.

벤더의 전략은 HAI 벤치마크의 실적에 따라 월별 요금이 변동하는 성과 기반 계약을 묶어 왔습니다. 이 변화는 병원의 균형 시트에서 위험을 제거하는 동시에 공급업체에게 지속적인 수익을 보장합니다. 플랫폼+서비스의 구독으로의 전환이 더욱 진행되어 감염 감시 솔루션 시장 전체의 롱테일의 가치 획득이 확고한 것이 될 것으로 기대됩니다.

북미는 2024년 매출액의 38.1%를 차지했으며, NHSN 보고의 의무화와 CMS의 상환수단에 의해 모든 급성기 의료시설에 인증 전자 서베이런스의 유지가 의무화되었습니다. 2024년 11월 발효 연방규칙에 따라 병원은 매주 COVID-19, 인플루엔자 및 RSV 수를 업로드해야 하며 자동화 플랫폼에 대한 수요가 증가하고 있습니다. 미국의 주요 IDN이 주목할만한 AI 조종사는 동업자의 도입을 촉진하고 예산위원회의 ROI 계산을 검증합니다.

아시아태평양은 일본, 중국, 한국이 레거시 아키텍처를 클라우드 네이티브 배포로 대체함으로써 2030년까지 연평균 복합 성장률(CAGR)이 13.5%로 가장 높습니다. 일본의 초고령화 사회는 에너지 절감 모니터링의 가치 제안을 증폭시키고 중국의 하향식 디지털화는 Tier2 도시에서도 EHR 노드에 자금을 공급합니다. 원격 의료 및 가정 의료 모델로의 개인 자금의 유입은 감염 감시 솔루션 시장을 더욱 확대합니다.

유럽은 유럽 의료 데이터 공간을 배경으로 꾸준히 전진하고 있습니다. EHDS는 2029년까지 상호 운용 가능한 EHR과 국경을 넘어서는 감염증 보고를 의무화하고 있으며, 이 기한에 따라 조달 사이클이 가속화됩니다. 엄격한 GDPR(EU 개인정보보호규정) 규칙은 익명화와 안전한 처리 구역을 통합하는 플랫폼에 대한 수요를 증가시키고 EU10 국가에 걸친 폐수 플러스 유전체 시험은 병원체 모니터링에 대한 이 지역의 통합된 다중 모달 접근법을 보여줍니다.

The infection surveillance solutions market size stands at USD 0.91 billion in 2025 and is projected to reach USD 1.69 billion by 2030, delivering a 13.2% CAGR as healthcare providers institutionalize digital infection-control workflows learned during the pandemic.

Expansion is propelled by new U.S. and EU rules obligating electronic submission of healthcare-associated infection (HAI) data, tighter value-based reimbursement, and rapid uptake of AI-based early-warning algorithms that cut sepsis detection times. Hospitals accelerate spending to avoid CMS penalties tied to respiratory illness reporting, while smaller facilities gravitate toward cloud subscriptions that trim capital budgets despite lingering cybersecurity fears following the 2024 Change Healthcare breach. Vendors differentiate on interoperability with EHRs, HL7-FHIR readiness, and embedded predictive analytics, and most are layering managed services on top of core software to relieve staffing constraints. Overall, the infection surveillance solutions market benefits from a convergence of regulation, economics, and technology that turns digital surveillance from a "nice-to-have" into mandatory clinical infrastructure.

Healthcare-associated infections cost U.S. hospitals USD 25-45 billion a year, making surveillance investment an economic imperative. CMS finalized fresh quality measures for catheter-associated UTIs and central-line infections in its FY 2025 rule set, and the European Health Data Space will require standardized infection reporting across 27 member states by 2029. German facilities illustrate the payoff: preventing a single nosocomial episode can avoid 12 added bed-days and generate EUR 390-650 in incremental revenue. As penalties tighten, the infection surveillance solutions market becomes non-discretionary infrastructure.

CMS's Hospital-Acquired Condition Reduction Program imposes 1% payment cuts on the worst-performing quartile of hospitals, linking revenue directly to infection metrics. New participation rules effective November 2024 extend mandatory weekly respiratory-illness uploads, forcing institutions to automate reporting or forfeit Medicare dollars. Parallel frameworks in Japan attach reimbursement uplifts to certified EHR and surveillance connectivity. The penalty-or-pay dynamic generates predictable demand for infection surveillance solutions market deployments across acute and post-acute settings.

Basic EMR deployments still demand USD 13,100 per provider and full-featured surveillance can add USD 50,000 annually-tough numbers for rural hospitals. Nonetheless, five-year net benefits reach USD 86,400 via avoided HAIs and charge capture. Pending U.S. legislation aims to subsidize rural adoption, while cloud Software-as-a-Service offerings align spend with usage, easing entry into the infection surveillance solutions market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Surgical-site infections contributed USD 0.47 billion in 2024, representing the largest slice of the infection surveillance solutions market. CMS penalty structures and public reporting keep surgical metrics in executive dashboards, sustaining investment in perioperative surveillance modules. AI-augmented image and vital-sign analyzers now flag wound deterioration within hours, enhancing compliance and trimming readmission risks. In contrast, blood-stream infections generated a smaller base but clock the highest 13.8% CAGR thanks to continuous physiological data streams that feed machine-learning sepsis predictors. The infection surveillance solutions market size for blood-stream monitoring is projected to hit USD 0.41 billion by 2030 as validation studies prove 26% mortality reduction. Other categories such as catheter-associated UTIs and ventilator-associated pneumonia benefit from device usage audits and bedside dashboards that push adherence reminders in real time.

Clinical priority differences steer vendor road maps. Surgical-site modules emphasize operating-room scheduling links and antimicrobial prophylaxis timers, while blood-stream modules pivot around real-time lab cultures and antibiotic stewardship tools. Emerging whole-genome sequencing tie-ins will likely blur boundaries, enabling unified dashboards that overlay pathogen lineage on infection type. Still, hospitals are expected to license separate analytic bundles through 2030, ensuring the infection surveillance solutions market continues to generate type-specific revenue streams.

Software platforms delivered 67.8% of overall revenue in 2024 and continue to anchor most RFPs due to health systems' preference for integrated EHR plug-ins. Market leaders invest in low-code configurations so infection-control teams can tweak alert thresholds without programmer support. Yet services revenue rises at a faster 14.7% clip as facilities outsource rule tuning, report generation, and AI model retraining. Managed-service providers package 24/7 monitoring, regulatory updates, and analytics talent, appealing to resource-strained safety-net hospitals. As a result, the infection surveillance solutions market size attributable to services may near USD 0.62 billion by 2030, blurring the classic product-versus-services distinction.

Vendor strategies increasingly bundle outcome-based contracts in which monthly fees flex with performance on HAI benchmarks. That shift moves risk off hospital balance sheets while guaranteeing recurring revenue for suppliers. Expect further migration toward platform-plus-service subscriptions, solidifying long-tail value capture across the infection surveillance solutions market.

The Infection Surveillance Solutions Market Report is Segmented by Type (Surgical-Site Infections, Blood-Stream Infections, Catheter-Associated UTIs, and Ventilator-Associated Pneumonia), Offering (Software and Services), Deployment Model (On-Premise and Cloud), End User (Hospitals, Long-Term Care Facilities, Ambulatory Surgery Centers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 38.1% of 2024 revenue, underpinned by mandatory NHSN reporting and CMS reimbursement levers that compel every acute-care facility to maintain certified electronic surveillance. Federal rules effective November 2024 now require hospitals to upload weekly COVID-19, influenza, and RSV counts, cementing demand for automated platforms. High-profile AI pilots across leading U.S. IDNs stimulate peer adoption and validate ROI calculations for budget committees.

Asia-Pacific records the highest 13.5% CAGR through 2030 as Japan, China, and South Korea leapfrog legacy architectures with cloud-native deployments. Japan's super-aged demographics amplify the value proposition for labor-saving surveillance, while China's top-down digitization funds EHR nodes even in tier-2 cities. Private equity flows into telehealth and hospital-at-home models further expand the infection surveillance solutions market because remote-care workflows still require infection-risk oversight.

Europe advances steadily on the back of the European Health Data Space. EHDS mandates interoperable EHRs and cross-border infection reporting by 2029, a deadline accelerating procurement cycles. Strict GDPR rules elevate demand for platforms with embedded anonymization and secure-processing zones, and wastewater-plus-genomic pilots across 10 EU nations showcase the region's integrated, multi-modal approach to pathogen monitoring.