ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

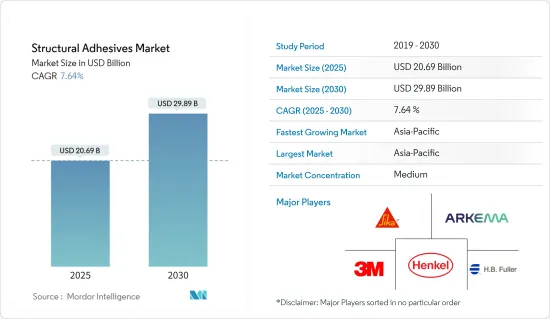

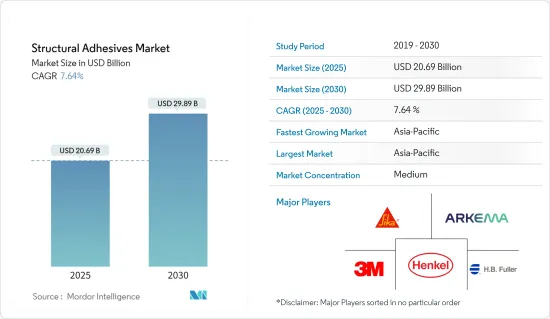

구조용 접착제 시장 규모는 2025년에 206억 9,000만 달러로 추정되고, 2030년에는 298억 9,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년) CAGR은 7.64%를 나타낼 전망입니다.

2020년에는 코로나19로 인해 시장이 부정적인 영향을 받았습니다. 그러나 2021년에는 건설, 자동차, 풍력 에너지 등 다양한 최종 사용자 산업의 소비 증가로 인해 크게 회복되었습니다.

주요 하이라이트

단기적으로는 아시아태평양 경제 개발도상국에 대한 투자 증가와 글로벌 건설 및 자동차 부문의 수요 증가가 연구 대상 시장을 견인할 수 있습니다.

그러나 증가하는 환경 및 건강 문제는 연구 된 시장의 성장을 방해 할 것으로 예상됩니다.

수중 구조용 접착제에 대한 연구 증가는 향후 시장 성장의 기회로 작용할 것으로 보입니다.

아시아태평양이 시장을 지배하고 있으며, 중국에서 가장 많은 소비가 기록되었습니다.

구조용 접착제 시장 동향

건설 산업의 수요 증가

건설 부문에서 구조용 접착제는 하중이나 응력을 견딜 수 있도록 재료를 접착하는 데 사용됩니다. 이러한 접착제는 결합 강도에 영향을 주지 않으면서도 우수한 내충격성, 파괴 인성, 구조적 유연성을 제공합니다.

건설 부문에서 구조용 접착제는 콘크리트, 내하중 재료, 알루미늄 및 강철과 같은 금속, 플라스틱, 엔지니어드 우드 등에 내구성을 제공합니다. 구조용 접착제는 내구성 외에도 에너지 효율이 높고 미적으로도 매력적입니다. 또한 유지보수의 필요성도 줄여줍니다. 이러한 특성 덕분에 건물 외벽과 교량의 수명이 연장됩니다.

건설 산업에서 사용되는 필수 구조용 접착제에는 아크릴 구조용 접착제, 강철 접착제, 앵커 접착제, 붓기 접착제, 탄소 섬유 보강 접착제, 건식 행잉 접착제, 실리콘 구조용 접착제 등이 있습니다.

세계의 건설 활동이 증가함에 따라 구조용 접착제에 대한 수요는 예측 기간 동안 증가할 것으로 예상됩니다. 2021년 전 세계 건설 시장 규모는 약 7조 2,000억 달러였으며 2022년에는 3.6%의 성장률을 보일 것으로 예상됩니다.

아시아태평양의 건설 부문은 세계에서 가장 큰 규모이며 인구 증가, 중산층 소득 증가, 도시화에 힘입어 견조한 속도로 확장되고 있습니다. 중국과 인도의 주택 건설 시장 확대로 인해 아시아 태평양 지역의 주택 시장도 가장 높은 성장률을 기록할 것으로 예상됩니다. 중국 국가통계국에 따르면 2021년 중국의 건설공사 생산액은 25조 9,200억 위안(약 4조 300억 달러)으로, 2020년 23조 2,700억 위안(약 3조 6,200억 달러)에서 증가하고 있습니다.

미국은 북미 건설 산업에서 상당한 비중을 차지하고 있습니다. 캐나다와 멕시코도 건설 산업에 크게 기여하고 있습니다. 미국 인구조사국에 따르면 이 나라의 신규 건설액은 2020년 1조 4,995억 7,000만 달러에서 증가하고, 2021년에는 1조 6,264억 4,400만 달러에 이릅니다.

따라서 위에서 언급한 모든 요인이 연구 대상 시장의 수요에 큰 영향을 미칠 것으로 보입니다.

시장을 독점하는 아시아태평양

아시아태평양은 2021년 구조용 접착제 세계 시장을 독점했습니다. 중국은 세계 최대의 구조용 접착제 소비국 중 하나입니다.

2022년 1월에 발표된 중국의 5개년 계획에 따르면 중국의 건설 산업은 2022년에 약 6%의 성장률을 기록할 것으로 예상됩니다. 중국은 건설 현장에서 발생하는 오염과 폐기물을 줄이기 위해 조립식 건물 건설을 늘릴 계획입니다.

또한 국가개발개혁위원회(National Development and Reform Commission)에 따르면 중국 정부는 약 1,420억 달러를 투자할 것으로 추정되는 26개 인프라 프로젝트를 승인했습니다. 이 프로젝트는 현재 진행 중이며 2023년까지 완료될 것으로 추정됩니다.

중국은 세계 최대의 자동차 제조업체입니다. OICA에 따르면 이 나라의 자동차 생산량은 2021년 2,608만대에 달했으며 2020년 2,523만대에서 3% 증가했습니다. 자동차 생산량 증가는 특히 하이엔드 자동차 제조 분야에서 구조용 접착제 수요를 촉진하는 것으로 추정됩니다.

또한 스톡홀름 국제평화연구소(SIPRI)에 따르면 미국에 이어 세계 2위 군사비 지출국인 중국은 2021년에 추정 2,930억 달러를 군사비에 충당합니다. 이는 2020년 대비 4.7% 증가했습니다. 2021년 중국 예산은 2025년까지 진행되는 제14차 5개년 계획의 첫 번째 예산입니다.

인도의 대규모 건설 부문은 2022년까지 세계에서 세 번째로 큰 건설 시장이 될 것으로 예상됩니다. 스마트 시티 프로젝트, 2022년까지 모두를 위한 주택 등 인도 정부가 시행하는 다양한 정책은 둔화된 건설 산업에 활력을 불어넣을 것으로 기대됩니다.

자동차 및 항공우주 분야는 구조용 접착제의 또 다른 주요 사용처입니다. OICA에 따르면 2021년 인도에서 생산된 자동차는 약 439만 9,112대로 2020년 338만 1,819대에 비해 30% 증가했습니다.

위의 요인들은 예측 기간 동안 아시아태평양 지역의 구조용 접착제 수요에 영향을 미칠 것으로 예상됩니다.

구조용 접착제 산업 개요

세계의 구조용 접착제 시장은 부분적으로 단편화된 성질을 가지고 있으며, 다양한 국내외 기업들이 존재하고 있습니다. 주된 기업는 Henkel AG & Co. KGaA, Sika AG, 3M, HB Fuller Company, Arkema 등입니다(특정한 순서 없음).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

아시아태평양의 개발도상국에 대한 투자 증가

글로벌 건설 및 자동차 부문의 수요 증가

억제요인

증가하는 환경 및 건강 문제

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

수지 유형별

에폭시

폴리우레탄

아크릴

시아노아크릴레이트

메타크릴산메틸

기타 수지 유형

최종 사용자 산업별

건축

자동차

항공우주

풍력에너지

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Arkema

Bondloc UK Ltd

DuPont

Engineered Bonding Solutions LLC

Forgeway Ltd

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

Illinois Tool Works Inc.

LG Chem

Parker Hannifin Corp.

Sika AG

RS Industrial

제7장 시장 기회와 앞으로의 동향

성장하는 수중 구조용 접착제의 조사

HBR

영문 목차

영문목차

The Structural Adhesives Market size is estimated at USD 20.69 billion in 2025, and is expected to reach USD 29.89 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. However, it recovered significantly in 2021, owing to rising consumption from various end-user industries, such as construction, automotive, and wind energy.

Key Highlights

Over the short term, the increasing investments in developing Asia-Pacific economies and increasing demand from the global construction and automotive sectors may drive the market studied.

However, growing environmental and health concerns are expected to hinder the growth of the studied market.

The growing research on underwater structural adhesives is likely to act as an opportunity for market growth in the future.

Asia-Pacific dominated the market, with the most significant consumption recorded in China.

Structural Adhesives Market Trends

Increasing Demand from the Construction Industry

In the construction sector, structural adhesives are used to bond materials to withstand loads or stresses. These adhesives offer good impact resistance, fracture toughness, and structural flexibility without affecting bond strength.

In the construction sector, structural adhesives provide durability to concrete, load-bearing materials, metals such as aluminum and steel, plastics, engineered woods, etc. Apart from durability, structural adhesives are energy-efficient and aesthetically appealing. They also reduce the need for maintenance. These characteristics extend the life cycle of building facades and bridges.

Some essential structural adhesives used in the construction industry include acrylic structural adhesives, steel glue, anchor glue, pouring glue, carbon fiber reinforcement glue, dry-hanging adhesives, and silicone structural adhesives.

With growing construction activity worldwide, the demand for structural adhesives is projected to increase during the forecast period. The global construction market was valued at around USD 7.2 trillion in 2021 and is likely to witness a growth rate of 3.6% in 2022.

The construction sector in the Asia-Pacific region is the largest in the world and is expanding at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization. The highest growth for housing is also expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. According to the National Bureau of Statistics of China, the output value of the construction works in the country in 2021 was CNY 25.92 trillion (~USD 4.03 trillion), increasing from CNY 23.27 trillion (~ USD 3.62 trillion) in 2020.

The United States occupies a significant share of the North American construction industry. Canada and Mexico also contribute significantly to the construction sector. According to the US Census Bureau, the value of new construction put in place in the country accounted for USD 1,626,444 million in 2021, increasing from USD 1,499,570 million in 2020.

Therefore, all the factors mentioned above are likely to impact the demand in the market studied significantly.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region dominated the global structural adhesives market in 2021. China is one of the world's largest consumers of structural adhesives.

According to China's Five-Year Plan, unveiled in January 2022, the country's construction industry is estimated to register a growth rate of approximately 6% in 2022. China plans to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites.

Moreover, as per the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects with an estimated investment of around USD 142 billion. These projects are in progress and are estimated to be completed by 2023.

China is the largest manufacturer of automobiles in the world. According to the OICA, the automotive production in the country reached 26.08 million in 2021, which increased by 3% compared to 25.23 million vehicles produced in 2020. The increase in automotive production is estimated to drive the demand for structural adhesives, especially in the high-end vehicle manufacturing sector.

Furthermore, as per the Stockholm International Peace Research Institute (SIPRI), China, the world's second-largest spender on the military after the United States, allocated an estimated USD 293 billion to its military in 2021. This was an increase of 4.7% compared to 2020. The 2021 Chinese budget was the first under the 14th Five-Year Plan, which runs until 2025.

India's massive construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing for all by 2022, are expected to prove an impetus to the slowing construction industry.

The automotive and aerospace sectors are the other significant users of structural adhesives. According to OICA, around 4,399,112 vehicles were produced in India in 2021, which increased by 30% compared to 3,381,819 units in 2020.

The factors above are expected to affect the demand for structural adhesives in the Asia-Pacific region over the forecast period.

Structural Adhesives Industry Overview

The global structural adhesives market is partially fragmented in nature, with the presence of various international and domestic players. Some of the major players include Henkel AG & Co. KGaA, Sika AG, 3M, H.B. Fuller Company, and Arkema (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increase in Investments in Developing Economies in Asia-Pacific

4.1.2 Increasing Demand from the Global Construction and Automotive Sectors

4.2 Restraints

4.2.1 Growing Environmental and Health Concerns

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Resin Type

5.1.1 Epoxy

5.1.2 Polyurethane

5.1.3 Acrylic

5.1.4 Cyanoacrylate

5.1.5 Methyl Methacrylate

5.1.6 Other Resin Types

5.2 By End-user Industry

5.2.1 Construction

5.2.2 Automotive

5.2.3 Aerospace

5.2.4 Wind Energy

5.2.5 Other End-user Industries

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 Arkema

6.4.3 Bondloc UK Ltd

6.4.4 DuPont

6.4.5 Engineered Bonding Solutions LLC

6.4.6 Forgeway Ltd

6.4.7 H. B. Fuller Company

6.4.8 Henkel AG & Co. KGaA

6.4.9 Huntsman International LLC

6.4.10 Illinois Tool Works Inc.

6.4.11 LG Chem

6.4.12 Parker Hannifin Corp.

6.4.13 Sika AG

6.4.14 RS Industrial

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Research on Underwater Structural Adhesives