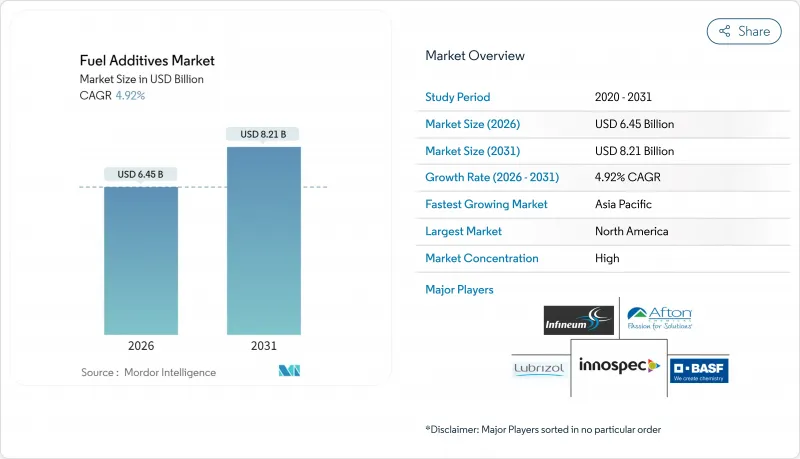

연료 첨가제 시장은 2025년 61억 5,000만 달러로 평가되었고, 2026년 64억 5,000만 달러로 성장할 전망이며, 2026-2031년 연평균 복합 성장률(CAGR) 4.92%로 성장을 지속하여, 2031년까지 82억 1,000만 달러에 달할 것으로 예측되고 있습니다.

세계의 배출 규제 강화가 첨가제 수요를 자극하는 한편, 배터리 전기자동차의 보급에 따른 연료 소비량의 장기적인 감소가 예상됩니다. 지속적인 제트 연료 수요 외에도 신흥 국가에서 초저황 경유(ULSD)의 도입은 연료 첨가제 시장의 상승 추세를 지원합니다. 항공업계의 회복, 확대하는 바이오디젤 의무화, 그리고 중질 및 저품질 원유의 정제 기술의 진보가 함께 꾸준한 제품 혁신을 뒷받침하고 있습니다. 공급업체 각 회사가 다기능으로 바이오연료 대응 패키지로 전환하고 비용 압력 대책으로 원료 조달의 일원화를 도모하는 중, 경쟁은 격화하고 있습니다.

세계의 규제 강화로 인해 연료 생산자가 보다 복잡한 컴플라이언스 요건을 충족하면서 첨가제의 소비 구조가 재구성되었습니다. 미국의 신재생 연료 기준(RFS)은 에탄올과 바이오디젤 혼합에 대한 첨가제 요건을 규정하고, 유럽연합(EU)의 유로 7 배출가스 규정은 보다 긴 드레인 간격에서 후처리 효율을 유지하기 때문에 보다 높은 세척 성능을 요구하고 있습니다. 캘리포니아주 선진 클린카 II(ACCII) 프레임워크는 2035년 내연기관 폐지 목표에도 불구하고 증발성 및 미립자 배출을 억제하는 프리미엄 가솔린 첨가제의 단기 수요를 끌어올리고 있습니다. 국제해사기구(IMO) 2020년 유황규제는 육상용 디젤연료 시장에도 파급되어 다기능 첨가제 패키지의 대응가능 시장을 더욱 확대하고 있습니다. ISO 8217 및 ASTM D975와 같은 공식적인 시험 프로토콜은 공인 시험소를 운영하는 공급업체로 사업을 유도하여 신규 참가자의 진입 장벽을 강화하고 있습니다.

보다 중질하고 오염도가 높은 기회 원유가 정유소의 원료 구성에서 큰 비율을 차지하게 되어, 저장으로부터 연소 사이클 전체에서 퇴적물 형성 리스크가 높아지고 있습니다. 셰일 유래의 파라핀계 원유는 왁스 석출을 촉진하고, 캐나다의 오일샌드 원료는 장거리 수송 중 부식 및 산화 스트레스를 증대시킵니다. 이러한 추세는 가혹한 열적 및 화학적 부하 하에서도 연료의 무결성을 유지하는 퇴적물 억제제, 산화 방지제, 부식 방지제 수요를 강화하고 있습니다. 중동에서도 판매 유연성을 추구하는 중질 원료 처리 정유소는 비슷한 과제에 직면하고 있습니다. 정유소가 저품질 원료로부터 경제성을 끌어내는 가운데, 세정성, 금속 불활성화, 안정화 기능을 조합한 첨가제 패키지가 지지를 모으고 있습니다.

전기 이동성은 에너지 구조를 재구성하고 있습니다. 중국에서는 2024년에 EV 보급률이 45%를 넘어 국제 에너지 기관(IEA)은 2030년까지 세계 경차 판매의 60%가 EV가 될 것으로 예측했습니다. 가솔린 디젤 소비량이 피크를 맞이하는 가운데 도로 운송 관련 첨가제 수요는 구조적인 역풍에 휩쓸리고 있습니다. 대형 차량의 전동화는 특히 디젤 첨가제 공급업체에게 이러한 영향을 증폭시킵니다. 그러나 항공, 선박, 비도로 부문은 여전히 영향을 받기 어려우며, 공급업체들은 이러한 고부가가치 분야에 연구개발 및 자본을 집중시키는 동시에 암모니아 및 수소 캐리어와 같은 대체 연료용 첨가제를 탐색하고 있습니다.

퇴적물 억제 첨가제는 2025년에 연료 첨가제 시장 점유율의 28.78%를 차지해 현대의 연료 품질 관리 체제의 기반으로서의 역할을 확고히 하고 있습니다. EPA Tier 3 및 EN 228 가솔린 표준이 요구하는 흡기 밸브와 인젝터의 청결성을 보장하여 연소 효율 및 배기 시스템의 내구성을 보호합니다. 이 부문은 밸브 퇴적물의 발생 위험이 높은 가솔린 직분사 엔진의 보급에 의해 혜택을 받고 있습니다. 마찬가지로 중요한 점으로, 고압 디젤 분사 시스템에서는 노즐 코크스화를 방지하기 위한 세정제가 요구되고 있습니다.

저온유동성 개량제는 바이오디젤 혼합 비율의 확대 및 캐나다, 북유럽, 중국 동북부에서 동계 가동성의 중요성 증대에 따라 2031년까지 5.43%의 연평균 복합 성장률(CAGR)을 기록하여 제품군 내에서 가장 빠른 성장이 예상됩니다. 이러한 규제가 확대됨에 따라 바이오디젤의 높은 흐림점 및 유동점에 대응하는 유동점 강하제 기술이 주목을 받고 있습니다. 세탄가 향상제는 신뢰성 있는 콜드 스타트와 점화 지연의 감소를 필요로 하는 고효율 엔진으로에 대한 상용 차량의 이행에 따라 수요가 확대되고 있습니다. 다기능 블렌드는 정제업자 및 다운스트림 연료 판매업자에게 첨가율의 복잡성을 줄이고 성능 목표를 단일 SKU로 통합할 수 있기 때문에 지지가 높아지고 있습니다.

연료 첨가물 보고서는 제품 유형별(퇴적물 억제제, 세탄가 향상제, 윤활성 첨가제, 산화 방지제, 부식제, 저온 유동성 향상제, 노킹 방지제, 기타 제품 유형), 용도별(디젤, 가솔린, 제트 연료, 기타 용도), 지역별(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)별로 분류되어 있습니다. 시장 예측은 금액 기준 및 수량 기준으로 제공됩니다.

2025년 북미는 연료 첨가제 시장 점유율의 35.55%를 차지했습니다. 수년간의 EPA 규제와 성숙한 정제 설비가 안정적인 수요량을 지원하는 반면, 캐나다의 가혹한 동계 환경은 저온 유동성 개량제 수요를 촉진하고 있습니다. 가솔린 세정제 수요는 엔진의 청결성을 유지하기 위해 더 높은 퇴적물 억제 수준을 의무화하는 'TOP TIER' 소매 프로그램 하에서 견조하게 변화하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로 2031년까지 5.48%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 중국의 국가 VI 기준과 인도의 BS-VI 기준을 시행함으로써, 정유소가 수소화 탈황 장치를 갱신하는 가운데, 윤활성 첨가제 및 세탄가 향상제 수요가 가속화되고 있습니다. 급속한 도시화로 상용차 플릿이 확대되고 승용전기자동차(EV)의 보급이 진행되고 있는 가운데 디젤 첨가제 소비량이 증가하고 있습니다. 동남아시아 국가에서는 초저황 경유(ULSD)와 E10 가솔린의 도입이 진행되어 바이오디젤 안정제, 산화방지제, 윤활성 향상제 등 여러 제품에 대한 수요를 창출하고 있습니다.

유럽에서는 탈탄소화의 적극적인 목표에 의해 제품 구성이 바이오연료 대응 첨가제로 이행하는 가운데 절대적인 성장은 완만하면서도 견조하게 추이하고 있습니다. ReFuelEU 항공 및 해운 유황 규정은 고수익 특수 첨가제 수요를 낳고 도로 연료 수요 감소를 상쇄합니다. 중동 및 아프리카에서는 사우디아라비아와 나이지리아에서 정유소 복합 시설의 확대로 지역 내 완성 연료 공급이 확대되고 수출 기준을 충족하는 첨가제 수입이 증가합니다. 브라질의 에탄올 프로그램을 견인하는 남미에서는 고혼합 가솔링레이드용 항산화제 및 부식 방지제에 대한 견조한 수요가 지속되고 있습니다.

The Fuel Additives market is expected to grow from USD 6.15 billion in 2025 to USD 6.45 billion in 2026 and is forecast to reach USD 8.21 billion by 2031 at 4.92% CAGR over 2026-2031.

The outlook balances tightening global emission rules that stimulate additive demand against the long-run decline in fuel consumption tied to battery-electric vehicle adoption. Sustained jet-fuel needs, coupled with emerging-economy rollouts of ultra-low sulfur diesel (ULSD), keep the fuel additives market on an upward trajectory. Aviation recovery, expanding biodiesel mandates, and the refinement of heavy, lower-quality crudes collectively underpin steady product innovation. Competitive intensity has risen as suppliers pivot to multifunctional, biofuel-ready packages while securing raw-material integration to offset cost pressures.

Global regulatory tightening is reshaping additive consumption as fuel producers align with more complex compliance layers. The U.S. Renewable Fuel Standard embeds additive requirements for ethanol and biodiesel blending, while Euro 7 emission rules in the European Union call for higher detergency to preserve after-treatment efficiency across longer drain intervals. California's Advanced Clean Cars II framework, despite its 2035 internal-combustion phase-out target, lifts near-term demand for premium gasoline additives that curb evaporative and particulate emissions. Maritime sulfur caps under IMO 2020 have spilled into land-based diesel pools, further widening the addressable market for multifunctional packages. Formal test protocols such as ISO 8217 and ASTM D975 channel business toward suppliers that operate accredited laboratories, tightening the qualification bar for new entrants.

Heavier, higher-contaminant opportunity crudes now fill a larger slice of refinery slates, escalating deposit formation risks throughout storage and combustion cycles. Shale-derived paraffinic crudes elevate wax precipitation, while Canadian oil-sands feedstocks heighten corrosion and oxidation stress during long-haul transport. These dynamics bolster demand for deposit control, antioxidant, and anticorrosion additives that maintain fuel integrity under harsher thermal and chemical loads. In the Middle East, refineries running heavier feed face similar issues as they chase merchandising flexibility. As refiners squeeze economics from lower-grade inputs, additive packages that combine detergency, metal-deactivating, and stabilization functions gain favor.

Electric mobility is redrawing the energy map. China surpassed 45% EV penetration in 2024, and the International Energy Agency sees EVs reaching 60% of global light-duty sales by 2030. As gasoline and diesel consumption peaks, additive volumes linked to road transport face a structural headwind. Heavy-duty fleet electrification compounds the effect, especially for diesel additive vendors. Nevertheless, aviation, marine, and off-road segments remain insulated, prompting suppliers to concentrate research and development and capital around these higher-value niches while exploring additives for alternative fuels such as ammonia and hydrogen carriers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Deposit control additives commanded 28.78% of the fuel additives market share in 2025, cementing their role as the cornerstone of modern fuel quality regimes. They ensure intake-valve and injector cleanliness demanded by EPA Tier 3 and EN 228 gasoline standards, safeguarding combustion efficiency and emission-system longevity. The segment benefits from the proliferation of gasoline direct-injection engines, which are more prone to valve deposits. Equally important, high-pressure diesel injection systems demand detergents to prevent nozzle coking.

Cold flow improvers register a 5.43% CAGR to 2031, the fastest within the product spectrum, as biodiesel blending widens and winter operability becomes mission-critical in Canada, Northern Europe, and Northeast China. As these mandates scale, pour-point depressant technologies that manage biodiesel's higher cloud and pour points gain traction. Cetane improvers follow as commercial fleets upgrade to higher-efficiency engines requiring reliable cold starts and reduced ignition delay. Multifunctional formulations are gaining favor because they reduce treat-rate complexity for refiners and downstream fuel marketers, consolidating performance goals into one SKU.

The Fuel Additives Report is Segmented by Product Type (Deposit Control, Cetane Improvers, Lubricity Additives, Antioxidants, Anticorrosion, Cold Flow Improvers, Antiknock Agents, and Other Product Types), Application (Diesel, Gasoline, Jet Fuel, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value and Volume.

North America accounted for 35.55% of the fuel additives market share in 2025. Long-standing EPA rules and mature refining assets foster dependable volume, while extreme winter conditions in Canada stimulate cold flow improver uptake. Gasoline detergent demand remains buoyant under the TOP TIER retail program, which mandates higher deposit-control levels to maintain engine cleanliness.

Asia-Pacific is the fastest-growing region, charting a 5.48% CAGR to 2031. China's enforcement of National VI and India's BS-VI standards accelerates lubricity and cetane additive demand as refineries update hydrodesulfurization units. Rapid urbanization expands commercial vehicle fleets, boosting diesel additive consumption even as passenger EV adoption rises. Southeast Asian economies pursue ULSD and E10 gasoline rollouts, creating multi-product pull across biodiesel stabilizers, antioxidants, and lubricity improvers.

Europe shows steady but lower absolute growth, underpinned by aggressive decarbonization goals that shift the product mix toward biofuel-compatible additives. ReFuelEU Aviation and maritime sulfur caps generate high-margin specialty demand, offsetting declining road-fuel volumes. In the Middle East and Africa, expanding refinery complexes in Saudi Arabia and Nigeria widen regional availability of finished fuels, drawing additive imports to hit export-grade specifications. South America, led by Brazil's ethanol program, sustains robust antioxidant and corrosion-inhibitor demand for high-blend gasoline grades.