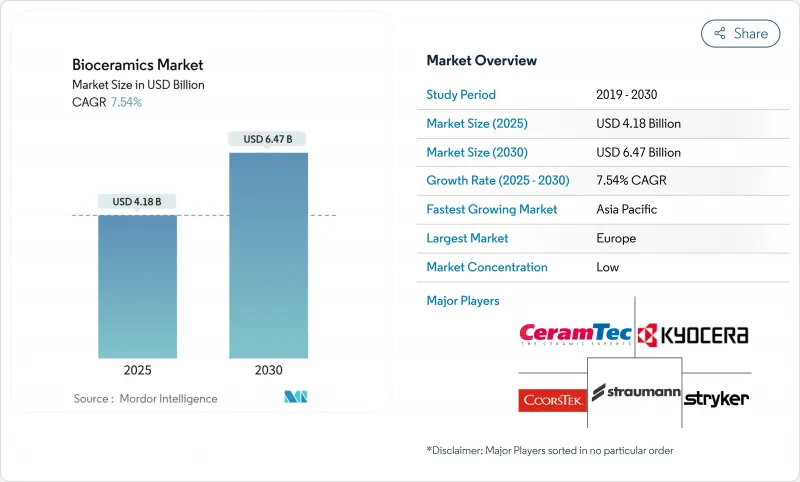

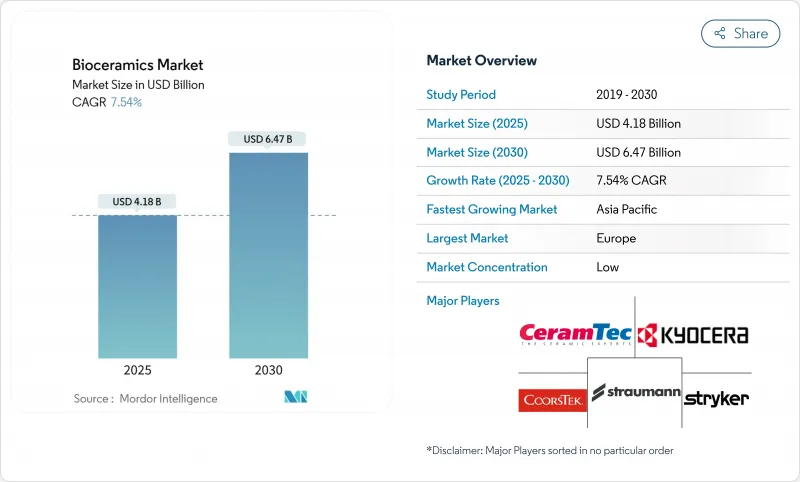

바이오세라믹 시장 규모는 2025년에 41억 8,000만 달러로 추정되고 예측 기간(2025-2030년)의 CAGR은 7.54%를 나타내, 2030년에는 64억 7,000만 달러에 달할 것으로 예상되고 있습니다.

근골격계 및 치과 치료 증가, 3D 프린팅에 의해 제조되는 환자 고유의 임플란트의 폭넓은 채용, 내구성과 생체 적합성이 높은 재료를 요구하는 고령화 사회가 바이오세라믹 시장을 추진하고 있습니다. 유럽과 아시아태평양에서는 고급 정형외과 수술과 치과 치료에 대한 규제 당국의 지원, 디지털 워크플로우에 대한 병원 투자가 수요를 더욱 가속화하고 있습니다. 업계 선두는 재료의 우위성과 생산 효율을 확보하기 위해 인수, 프로세스 혁신, 연구 기관과의 공동 개발 프로그램을 추구하고 있기 때문에 경쟁의 치열성은 여전히 높습니다.

미국 및 캐나다 병원에서는 현재 최적화된 공극률로 환자에 맞는 형상을 제공하는 고밀도 세라믹 라미네이트 성형 라인을 통합하고 있습니다. 층별 제어는 오세오 통합을 개선하여 이전에는 비용이 많이 드는 가공이 필요한 경량 격자 모양을 가능하게 합니다. 임상 피드백에 따르면, 이러한 구조를 채택한 두개 안면과 척추 임플란트의 재치환률이 감소했습니다.

독일, 프랑스, 이탈리아에서는 환자가 자연적인 치열을 모방한 심미성을 요구하기 때문에 금속이 없는 프로토콜이 빠르게 성장하고 있습니다. 투피스 지르코니아 시스템은 보철물의 유연성에 대한 이전의 문제를 해결하고 연조직의 반응을 희생하지 않고 광범위한 임상 적응을 가능하게합니다. 지르코니아를 기반으로 한 픽스처의 5년 생존율은 94-98.4%이며, 티타늄과 거의 동등한 결과를 얻을 수 있습니다. 반투명 지르코니아용 의자 사이드 밀링 유닛에 일찍 투자해 온 실험실은 현재 더 빠른 납기부터 이익을 얻고 있습니다. 티타늄 전문 OEM은 경쟁력을 되찾기 위해 라이선스 계약 및 인수를 통해 조정됩니다.

미국의 규제 당국은 현재 나노스케일 세라믹을 포함하는 장치에 대해 입자 이동 및 응집 거동에 대한 철저한 데이터를 요구하고 있습니다. 평균 심사 기간은 최대 14개월 길어지고 소규모 혁신자의 자본 요건을 끌어올리고 있습니다. 사내에 독물학연구소를 보유한 대기업은 이 장애물을 활용하여 경쟁력을 강화하고, 프로토타입이 후기시험에 이른 후 공동 개발 계약을 맺는 경우가 많습니다. 업계 컨소시엄은 밸리데이션 사이클을 단축할 수 있는 기준 표준을 다루고 있지만 2027년까지 눈에 보이는 형태로 완화될 가능성은 낮습니다.

산화 알루미늄 부문은 바이오세라믹 시장 규모의 49%에 해당합니다. 알루미나의 압축 강도와 내마모성은 고관절과 무릎 관절의 베어링에서 우위를 뒷받침합니다. 서브 미크론 입자 크기의 고순도 등급은 마이크로 균열을 발생시키지 않고 반복 하중을 견디고 인공 관절의 수명을 연장 할 수 있기 때문에 인기를 끌고 있습니다. 동시에 수행되는 표면 코팅에 대한 연구는 알루미나 임플란트를 이중 기능 부품으로 자리 매김하고 생물학적 활성을 추가하는 것을 목표로합니다. 2025년부터 2030년까지, 이 자료는 CAGR 7.89%를 나타내며, 척추 케이지와 봉합 앵커의 새로운 수요에 의해 지원되고 있습니다.

2024년에는 분말 제품이 바이오세라믹 시장 점유율의 48%를 차지했습니다. 과립의 유동성 향상으로 연속 피드 프레스 및 바인더 제트 프린터가 최소한의 후처리로 넷 모양에 가까운 부품을 제공할 수 있게 되었습니다. 분무건조 및 과립기술의 혁신은 바이오세라믹 분말의 유동성과 압축성을 향상시키고, 자동 제조와의 적합성을 높여 제조 비용을 절감했습니다. 주입 가능한 액체는 외과의사에게 불규칙한 결함에 맞는 경화의 빠른 페이스트를 제공함으로써 CAGR 7.75%를 나타낼 전망입니다.

유럽은 2024년 세계 매출의 43%를 차지하며 성숙한 보험 상환의 틀과 깊은 재료 과학 능력을 보여주었습니다. 독일은 인공 고관절 치환술의 기술 혁신을 주도하고 영국은 치주병 재생을 위한 생물활성 유리 연구를 진행하고 있습니다.

아시아태평양은 2025-2030년의 CAGR이 8.01%로 가장 높습니다. 중국의 중앙 집권적인 조달 정책은 현재 현지 조달에 유리하며 소결로와 분무 건조 라인에 대한 투자에 박차를 가하고 있습니다. 일본은 세라믹의 전통을 활용해, 피질에서 해면으로의 이행을 모방한 구배 구조를 개척합니다. 인도와 한국은 치과 관광을 확대하고 세계적인 인증 기준을 충족하는 지르코니아 임플란트를 채용하는 의원의 의욕을 높이고 있습니다.

북미는 여전히 기술 혁신의 도가니입니다. 첨단 병원에서는 수술실에 인접한 부가제조실을 통합하여 설계에서 임플란트 임베디드까지의 사이클을 72시간 이내로 단축하고 있습니다. 라틴아메리카와 중동은 보험 적용 범위가 넓어짐에 따라 새로운 수익 풀을 제공하지만, 멸균 물류와 관련된 공급망의 과제로 인해 지역별 유통 허브가 필요합니다.

The Bioceramics Market size is estimated at USD 4.18 billion in 2025, and is expected to reach USD 6.47 billion by 2030, at a CAGR of 7.54% during the forecast period (2025-2030).

Rising musculoskeletal and dental procedures, wider adoption of patient-specific implants produced through 3D printing, and an aging population that demands durable and biocompatible materials are pushing the bioceramics market forward. Regulatory support for advanced orthopedic and dental interventions in Europe and Asia Pacific, and hospital investments in digital workflows, further accelerate demand. Competitive intensity remains high as industry leaders pursue acquisitions, process innovation, and co-development programs with research institutions to secure material superiority and production efficiencies.

Hospitals across the United States and Canada now integrate high-density ceramic additive manufacturing lines that deliver patient-matched shapes with optimized porosity. Layer-by-layer control improves osseointegration and allows weight-saving lattice geometries that previously required costly machining. Clinical feedback indicates reduced revision rates for craniofacial and spinal implants that employ these structures.

Metal-free protocols are growing swiftly in Germany, France, and Italy as patients request aesthetics that mimic natural dentition. Two-piece zirconia systems solve earlier issues related to prosthetic flexibility, enabling broader clinical indications without sacrificing soft-tissue response. Five-year survival studies register 94-98.4% success for zirconia-based fixtures, almost equaling titanium outcomes while offering lower bacterial adhesion. Laboratories that invested early in chairside milling units for translucent zirconia now benefit from faster turnaround times. Titanium-focused OEMs are adjusting through licensing deals and acquisitions to regain competitive parity.

The United States regulator now requires exhaustive data on particle migration and agglomeration behavior for devices that incorporate nanoscale ceramics. Average review time has lengthened by up to 14 months, raising capital requirements for small innovators. Larger incumbents with in-house toxicology labs leverage this hurdle to reinforce competitive moats, often entering joint-development agreements only after prototypes reach late-stage testing. Industry consortia are working on reference standards that may shorten validation cycles, yet tangible relief is unlikely before 2027.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The aluminum oxide segment is equal to 49% of the bioceramics market size. Alumina's compressive strength and wear resistance underpin its dominance in hip and knee bearings. High-purity grades with sub-micron grain size are gaining traction because they withstand cyclic loads without micro-cracking, extending prosthesis service life. Concurrent surface-coating research aims to add bioactivity, positioning alumina implants as dual-function components. From 2025 to 2030, the material posts a 7.89% CAGR, supported by emerging demand in spinal cages and suture anchors.

Powder products captured 48% of the bioceramics market share in 2024. Granule flowability improvements allow continuous-feed presses and binder jet printers to deliver near-net-shape parts with minimal post-processing. Innovations in spray drying and granulation techniques have enhanced the flowability and compaction of bioceramic powders, making them more compatible with automated manufacturing and cutting production costs. Injectable liquids rise at 7.75% CAGR by offering surgeons fast-setting pastes that conform to irregular defects.

The Bioceramics Market Report Segments the Industry by Material Type (Aluminum Oxide, Zirconia, Calcium Phosphate, and More), Form (Powder, Liquid (Injectable), and More), Type (Bio-Inert, Bio-Active, Bio-Resorbable), Application (Orthopedics, Dental, and Biomedical), End-User Industry (Hospitals and Surgical Centers, Dental Clinics and Laboratories, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Europe accounted for 43% of global revenue in 2024, underlining mature reimbursement frameworks and deep material science capabilities. Germany champions hip arthroplasty innovation; the United Kingdom advances bioactive glass research for periodontal regeneration.

Asia Pacific registers the highest 8.01% CAGR during 2025-2030. China's centralized procurement policies now favor local content, spurring investment in sintering furnaces and spray-drying lines. Japan leverages its ceramic heritage to pioneer gradient structures that mimic cortical-trabecular transitions. India and South Korea expand dental tourism, motivating clinics to adopt zirconia implants that meet global accreditation standards.

North America remains an innovation crucible. Leading hospitals integrate additive manufacturing suites adjacent to operating theaters, condensing design-to-implant cycles to under seventy-two hours. Latin America and the Middle East offer emerging revenue pools as insurance coverage widens, though supply-chain challenges involving sterilization logistics require localized distribution hubs.