비스페놀 A(BPA) - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Bisphenol A (BPA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1685881

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

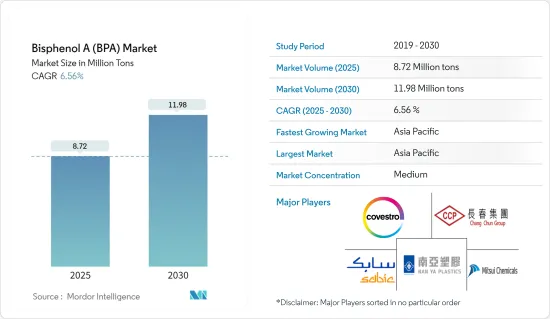

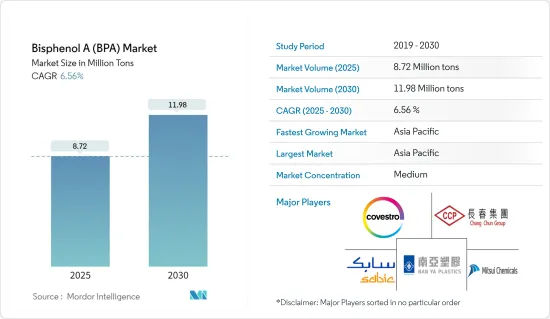

비스페놀 A(BPA) 시장 규모는 2025년에 872만 톤, 2030년에는 1,198만 톤에 달할 것으로 예측됩니다. 예측기간(2025년-2030년) CAGR은 6.56%를 나타낼 전망입니다.

주요 하이라이트

중기적으로는 폴리카보네이트 분야 수요 상승과 에폭시 수지 생산 수요 증가가 비스페놀 A 수요를 견인한다고 생각됩니다.

그러나 식음료 업계에서 비스페놀 A의 사용에 관한 규제 증가는 조사 대상 시장의 성장에 큰 억제요인을 가져옵니다.

한편, 바이오의 비스페놀 A에 대한 잠재적인 시장 수요는 향후 수년간 유리한 시장 기회를 창출할 것으로 보입니다.

아시아태평양이 시장을 독점하고 예측 기간 중에 가장 높은 CAGR을 나타낼 것으로 예상되고 있습니다.

비스페놀 A 시장 동향

폴리카보네이트 수지 수요 증가

폴리카보네이트는 주로 비스페놀 A와 염화카르보닐의 계면 반응에 의해 생성됩니다.

비스페놀 A는 폴리카보네이트 수지의 특성을 높이는 데 중요한 역할을 합니다. BPA는 폴리카보네이트 수지의 강도와 내구성에 기여하고 있습니다. BPA를 사용한 폴리카보네이트는 내충격성으로 알려져 있으며 안전유리, 방탄창, 의료기기 등의 용도에 적합합니다.

BPA를 포함한 폴리카보네이트는 유리 전이 온도가 높고, 휘거나 녹지 않고 고온을 견딜 수 있습니다. 이 특성은 식품 용기와 재사용 가능한 물통에 이상적입니다.

폴리카보네이트는 원래 투명하며 BPA는 이 투명성을 유지하는 데 도움이 됩니다. 따라서 투명한 용기와 렌즈를 생산할 수 있습니다.

폴리카보네이트는 고성능 열가소성 플라스틱으로 건축 용도에 널리 사용됩니다. 폴리카보네이트를 사용하여 제조된 시트는 유리의 대체품으로 다양한 창문 및 채광창 응용 분야에 널리 사용됩니다. 또한, 배럴 볼트, 불투명한 클래딩 패널, 캐노피, 정면, 기호, 반투명 벽, 스포츠 경기장 지붕, 미늘창, 지붕 돔으로도 사용됩니다.

최근, 폴리카보네이트 소재의 온실 이용이 증가하고 있습니다. 독일, 프랑스, 네덜란드, 스페인 등 유럽 국가들은 온실 재배 지역이 넓습니다.

폴리카보네이트 시장의 주요 기업으로는 미쓰비시 엔지니어링 플라스틱 주식회사, 코베스트로 AG, SABIC, 롯데케미칼 주식회사, 테이진 주식회사 등이 있습니다. 이러한 기업들은 M&A와 사업 확대에 많은 투자를 하고 있으며, 폴리카보네이트 중 BPA 수요를 높일 것으로 예측되고 있습니다. 예를 들어, 2024년 3월, 세계 최고의 고품질 고분자 소재 제조업체인 코베스트로 AG는 벨기에 앤트워프에 폴리카보네이트 공중합체를 산업 규모로 생산하는 최초의 공장을 가동했습니다.

2023년 9월, 사우디아라비아의 화학 대기업 SABIC과 중국의 석유 및 가스 기업 Sinopec은 합작 회사 Sinopec SABIC Tianjin Petrochemical(SSTPC)에 의한 폴리카보네이트(PC)플랜트의 신설을 발표했습니다.

2023년 3월, 코베스트로는 태국에서 폴리카보네이트 필름의 생산 능력을 확대했습니다.

따라서, 상기 요인은 예측 기간 중, 폴리카보네이트 용도에 있어서의 BPA 수요에 영향을 미칠 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 다양한 최종 사용자 산업에서 비스페놀 A(BPA)의 최대 제조 및 소비국입니다.

최근 다양한 경제적 및 산업적 요인으로 중국 전역에서 새로운 비스페놀 A(BPA) 생산 설비에 대한 투자가 증가하는 경향이 두드러집니다. 플라스틱스는 중국의 닝보에 있는 BPA 생산공장의 조업을 재개했습니다.

중국의 폴리카보네이트 수지와 플라스틱 제품에 포함된 BPA 수요는 자동차, 전자기기, 건설 등의 산업에서의 사용 확대에 의해 확대되고 있습니다. Petrochemical(SSTPC)를 통해 폴리카보네이트(PC) 신플랜트의 출시를 발표했습니다.

인도는 오랫동안 BPA를 수입했으며, 가격 변동과 지역 간 무역 문제가 인도의 BPA 시장에 문제를 일으키고 있습니다. Limited는 2024년 2월 구자라트주 Dahej에 약 900억 루피를 투자하여 프로젝트를 설립할 의향으로 구자라트 주 정부와 MoU를 체결했습니다.

최근 일본에서는 치열한 경쟁과 낮은 수익으로 인해 BPA 제조 공장이 폐쇄되는 경향이 있으며, 업계에 큰 영향을 미치고 있습니다. 급과잉을 이유로 남일본의 후쿠오카현에 있는 쿠로사키 공장에서 2024년 3월 말까지 BPA의 생산을 영구 정지하는 것을 계획했습니다.

따라서 위의 요인은 아시아태평양의 BPA 수요에 영향을 줄 것으로 예상됩니다.

비스페놀 A 산업 개요

비스페놀 A(BPA) 시장은 본질적으로 부분적으로 통합되어 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

폴리카보네이트 분야 수요 급증

에폭시 수지 수요 증가

억제요인

식품 및 식품 업계의 규제 강화

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

원료 분석

기술 스냅샷

무역 개요

가격 개요

규제 정책 분석

제5장 시장 세분화

용도별

폴리카보네이트 수지

에폭시 수지

불포화 폴리에스테르 수지

난연제

기타 용도

지역별

아시아태평양

중국

인도

일본

한국

ASEAN 국가

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

시장 점유율(%) 분석

주요 기업의 전략

기업 프로파일

Altivia Petrochemicals

Chang Chun Group

China National Bluestar(Group) Co. Ltd

China Petroleum & Chemical Corporation(SINOPEC)

Covestro AG

Dow

Hexion

Idemitsu Kosan Co. Ltd

Kumho P&B Chemicals Inc.

LG Chem

Lihua Yiweiyuan Chemical Co. Ltd

Mitsubishi Chemical Corporation

Mitsui Chemicals Inc.

Nan Ya Plastics Industry Co. Ltd

Nippon Steel Chemical & Material Co. Ltd

PTT Phenol Company Limited

SABIC

Samyang Holdings Corporation

Teijin Limited

Zhejiang Petroleum & Chemical Co. Ltd

제7장 시장 기회와 앞으로의 동향

바이오 BPA의 잠재적 시장 수요

SHW

영문 목차

영문목차

The Bisphenol A Market size is estimated at 8.72 million tons in 2025, and is expected to reach 11.98 million tons by 2030, at a CAGR of 6.56% during the forecast period (2025-2030).

Key Highlights

In the medium term, soaring demand from the polycarbonate sector and increasing demand for epoxy resin production are likely to drive the demand for Bisphenol-A.

However, increasing regulations in the food and beverage industry on the use of Bisphenol-A pose major restraints to the growth of the market studied.

On the other hand, potential market demand for bio-based Bisphenol-A is likely to create lucrative market opportunities in the coming years.

Asia-Pacific is expected to dominate the market and is anticipated to witness the highest CAGR during the forecast period.

Bisphenol-A Market Trends

Increasing Demand for Polycarbonate Resins

Polycarbonate is mainly formed after the reaction of Bisphenol-A with carbonyl chloride in an interfacial process. Among all other application areas, polycarbonate resin application provides a significant market demand for Bisphenol-A (BPA).

Bisphenol-A plays a critical role in enhancing the properties of polycarbonate resins. BPA contributes to the strength and durability of polycarbonate plastics. Polycarbonates made with BPA are known for their impact resistance, which makes them suitable for applications such as safety glasses, bulletproof windows, and medical devices.

Polycarbonates containing BPA have a high glass transition temperature, meaning they can withstand high temperatures without warping or melting. This property makes them ideal for food containers and reusable water bottles.

Polycarbonates are naturally transparent, and BPA helps to maintain this clarity. This allows the production of clear containers and lenses.

Polycarbonates are high-performing thermoplastics that are widely used in construction applications. Sheets manufactured using Polycarbonates are widely used as a substitute for glass in a variety of window and skylight applications. Additionally, they are used as barrel vaults, opaque cladding panels, canopies, facades and signage, translucent walls, sports stadium roofs, louvers, and roof domes.

The application of polycarbonate materials in greenhouses has increased in recent years. European countries, such as Germany, France, the Netherlands, and Spain, have larger areas for greenhouse cultivation.

Some of the key companies in the polycarbonate market include Mitsubishi Engineering-Plastics Corporation, Covestro AG, SABIC, Lotte Chemical Corporation, and Teijin Limited. These companies are investing heavily in mergers, acquisitions, and expansion, which are projected to boost the demand for BPA in polycarbonates. For instance, in March 2024, Covestro AG, one of the world's leading manufacturers of high-quality polymer materials, inaugurated its first plant to produce polycarbonate copolymers on an industrial scale at its Antwerp, Belgium site.

In September 2023, Saudi Arabian chemical giant SABIC and Chinese oil and gas corporation Sinopec announced the launch of a new polycarbonate (PC) plant through their joint venture named Sinopec SABIC Tianjin Petrochemical (SSTPC). With an annual designed capacity of 260 kilotons, the new PC plant is intended as a central piece of SABIC's PC growth strategy in China, providing opportunities for further collaborations with global and local customers.

In March 2023, Covestro expanded its production capacity for polycarbonate films in Thailand, primarily used in identity documents, automotive displays, and electrical and electronic applications. With these developments, the company's additional capacity now exceeds 100,000 metric tons annually.

Therefore, the factors mentioned above are expected to impact the demand for BPA in polycarbonate applications during the forecast period.

Asia-Pacific is Expected to Dominate the Market

Asia-Pacific is the largest manufacturer and consumer of Bisphenol-A (BPA) in different end-user industries. Hence, it is expected to dominate the market.

In recent years, there has been a noticeable trend of increasing investments in new Bisphenol-A (BPA) production facilities across China, driven by various economic and industrial factors. For instance, in January 2024, Nan Ya Plastics, a subsidiary of Formosa Group, restarted operations of the BPA production plant in Ningbo, China. This plant produces about 170,000 tons of BPA per annum. The BPA produced by the company is majorly used in the polycarbonate resins that the company produces.

The demand for BPA in polycarbonate resins and plastic products in China is growing due to its expanding use in industries like automotive, electronics, and construction. In September 2023, Saudi Arabian chemical company SABIC and Chinese oil and gas corporation Sinopec announced the launch of a new polycarbonate (PC) plant through their joint venture, Sinopec SABIC Tianjin Petrochemical (SSTPC). SABIC's portfolio of PC materials produced at SSTPC is marketed under its Lexan resin brand.

India has been importing BPA for a long time, and the fluctuations in prices and trade issues among the regions are creating a problem for the Indian BPA market. The government and a few companies have taken initiatives to manufacture BPA in India. For instance, in February 2024, Deepak Chem Tech Limited signed an MoU with the government of Gujarat with an intent to invest around INR 90,000 million to establish projects at Dahej, Gujarat. The company plans to build world-scale production facilities for advanced polymer resins, such as polycarbonate resins.

In recent years, Japan has seen a trend of BPA manufacturing plants closing down due to intense competition and low profitability, significantly impacting the industry. For instance, in February 2024, Japan's Mitsubishi Chemical planned to permanently halt the production of BPA by the end of March 2024 at its Kurosaki plant in south Japan's Fukuoka prefecture, citing oversupply, mainly from China. This plant produces about 120,000 tons of BPA per annum.

Hence, the above-mentioned factors are expected to impact the demand for BPA in Asia-Pacific.

Bisphenol A Industry Overview

The Bisphenol-A (BPA) market is partially consolidated in nature. Some of the key players (not in any particular order) in the market include Covestro AG, SABIC, Chang Chun Group, Mitsui Chemical Inc., and Nan Ya Plastics Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Soaring Demand from Polycarbonate Sector

4.1.2 Increasing Demand from Epoxy Resin Production

4.2 Restraints

4.2.1 Increasing Regulations in the Food and Beverage Industry

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Feedstock Analysis

4.6 Technological Snapshot

4.7 Trade Overview

4.8 Price Overview

4.9 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Application

5.1.1 Polycarbonate Resins

5.1.2 Epoxy Resins

5.1.3 Unsaturated Polyester Resins

5.1.4 Flame Retardants

5.1.5 Other Applications

5.2 By Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 ASEAN Countries

5.2.1.6 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Spain

5.2.3.6 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Altivia Petrochemicals

6.4.2 Chang Chun Group

6.4.3 China National Bluestar (Group) Co. Ltd

6.4.4 China Petroleum & Chemical Corporation (SINOPEC)