ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

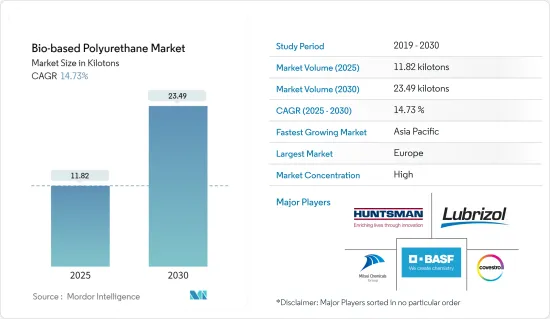

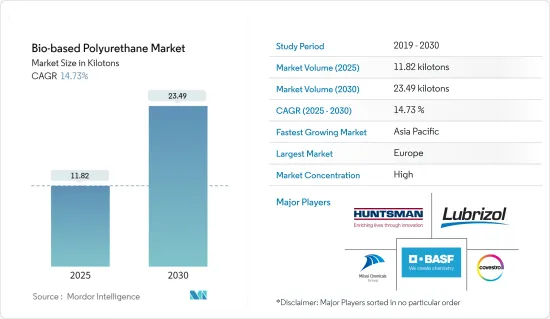

세계의 바이오 기반 폴리우레탄 시장 규모는 2025년 11.82킬로톤으로 추정되며, 예측 기간 중(2025-2030년) CAGR 14.73%로 확대되어, 2030년에는 23.49킬로톤에 달할 것으로 예측됩니다.

주요 하이라이트

시장은 COVID-19 팬데믹의 악영향을 받았습니다.

중기적으로는 신흥국의 건설 업계로부터 수요 증가와, 전자기기 제조로부터 수요 증가가 시장을 견인하는 주된 요인입니다.

그러나 바이오 재료는 비용이 높기 때문에 시장 성장을 방해할 것으로 예상됩니다.

그렇다고는 해도, 중동 및 아프리카의 산업 성장은 예측 기간 중에 호기가 될 것이 예상됩니다.

아시아태평양은 중국이나 인도 등의 나라에서의 소비가 가장 많아, 세계에서 가장 급성장하고 있는 시장이 될 것으로 예상됩니다.

바이오 폴리우레탄 시장 동향

수송산업에서의 수요 증가

바이오 폴리 우레탄의 주요 용도는 자동차, 철도, 항공우주 산업 등의 운송 산업입니다.

OCIA(Organisation Internationale des Constructeurs d'Automobiles)에 따르면, 2022년 세계의 자동차 생산 대수는 8,502만대에 달했습니다. 생산 능력은 2021년 대비 6% 증가했습니다.

최대 자동차 생산지역인 아시아태평양도 2022년에는 7%의 성장률을 기록했습니다.

철도 업계에서는 바이오 기반 PU는 향후 수년간 기존의 PU 제품을 대폭 대체할 수 있기 때문에 잠재적인 용도가 있습니다.

인도 철도는 단일 경영에서 세계 3위 철도 산업이기 때문에 정부의 창의적인 궁리에 의해 확대될 것으로 예측되고 있었습니다.

게다가 항공우주산업에서는 바이오 PU 폼과 코팅이 기존의 PU 재료의 대체가 될 가능성이 있습니다.

따라서, 수송산업 수요가 예측기간 중에 바이오 기반 폴리우레탄 수요를 증가시킬 것으로 예상됩니다.

아시아태평양이 급성장 시장이 될 전망

아시아태평양은 바이오 기반 폴리우레탄의 최대 생산지입니다.

바이오 기반 폴리 우레탄은 건축에 이용되고 있습니다.

중국은 건설 붐에 끓고 있습니다. 이 나라는 이 지역과 세계 최대의 건축 시장을 가지고 있으며, 세계의 모든 건축 투자의 20%를 차지합니다. 중국 정부는 2021년 3조 6,500억 위안(5,200억 달러)에서 2022년 3조 8,500억 위안(5,400억 달러)의 신규 인프라 채권의 연간 한도액을 설정했다고 추정하고 있습니다.

바이오 PU는 범퍼나 범퍼 스포일러, 래터럴 사이딩, 루프 및 부츠 스포일러, 로커 패널, 바디 패널, 대시보드나 대시보드 캐리어, 도어 포켓이나 패널, 콘솔, 난방 환기 공조, 배터리 커버, 에어 덕트, 압력 용기, 스플래시 실드 등의 자동차 용도로 폴리프로필렌을 대체할 수 있습니다.

OICA(Organisation Internationale des Constructeurs d'Automobiles)에 따르면 중국에서는 2021년에 약 2,612만대가 생산된 반면, 2022년에는 약 2,702만대가 생산되어 약 3%의 성장률을 기록했습니다.

바이오 기반의 폴리우레탄은 전기 절연성, 내충격성, 접착성 등의 품질에 가세해, 휴대폰, 모바일 기기, 컴퓨터, TV등의 전기 및 전자 용도에도 널리 이용되고 있습니다.

마찬가지로 인도에서도 일렉트로닉스 시장은 수요의 성장을 목격하고 시장 규모는 급속한 성장률로 증가하고 있습니다. 시장 규모는 2020-2021년 750억 달러에서 2025-2026년 3,000억 달러로 성장할 것으로 예측했습니다.

전술한 요인에 의해 예측 기간 중에 바이오 기반 폴리우레탄 수요가 증가할 가능성이 높습니다.

바이오 폴리 우레탄 산업 개요

바이오 폴리 우레탄 시장은 통합형입니다. 조사 대상 시장의 주요 제조업체는 BASF SE, Covestro AG, Huntsman International LLC, Mitsui Chemicals Inc., The Lubrizol Corporation 등입니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

신흥 국가의 건설 산업에서 수요 증가

전자기기 제조업에서 수요 증가

기타 촉진요인

억제요인

바이오 기반 재료의 높은 비용

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

용도

폼

코팅제

접착제 및 실란트

기타 용도(폴리우레탄 바인더, 폴리우레탄 디스퍼전)

최종 사용자 산업

수송

신발 및 섬유

건축

포장

가구 및 침구

일렉트로닉스

기타 최종 사용자 산업(바이오메디컬, 비료 산업)

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

기타 유럽

세계 기타 지역

브라질

사우디아라비아

남아프리카

기타 국가

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

Arkema

BASF SE

Covestro AG

Huntsman International LLC

Miracll Chemicals Co. Ltd

Mitsui Chemicals Inc.

Stahl Holdings BV

Toray Industries Inc.

Teijin Limited

The Lubrizol Corporation

Woodbridge

제7장 시장 기회와 앞으로의 동향

중동, 아프리카의 산업 성장

바이오 건축자재 개발

JHS

영문 목차

영문목차

The Bio-based Polyurethane Market size is estimated at 11.82 kilotons in 2025, and is expected to reach 23.49 kilotons by 2030, at a CAGR of 14.73% during the forecast period (2025-2030).

Key Highlights

The market was negatively affected by the COVID-19 pandemic. The construction industry was significantly impacted during the pandemic, which affected the demand in the market studied. However, the market is excepted to retain its growth trajectory in the coming years. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Over the mid-term, the key factors driving the market studied are the increasing demand from the construction industry in developing countries and the increasing demand from electronic appliance manufacturing.

However, the high cost of bio-based materials is expected to hinder the growth of the market studied.

Nevertheless, industrial growth in the Middle East and Africa is expected to act as an opportunity during the forecast period.

The Asia-Pacific region is expected to be the fastest-growing market across the world, with the largest consumption from countries such as China and India.

Bio-based Polyurethane Market Trends

Increasing Demand from the Transportation Industry

Bio-based polyurethane finds its key applications in the transportation industry, including the automotive, railway, and aerospace industries. Moreover, the automotive industry consumes bio-based PU foams, coatings, adhesives, and sealants. Specifically, bio-based PU foams are used in seating systems (headrests, headliners, armrests, seat cushioning, and others) and interior parts.

According to Organisation Internationale des Constructeurs d'Automobiles (OCIA), global automotive production reached 85.02 million units in 2022. The production capacity increased by 6% compared to 2021. In 2022, China, the United States, and Germany were the top three manufacturers of cars and commercial vehicles.

Asia-Pacific, the largest automotive production region, also witnessed a growth rate of 7% in 2022. The production increased from 46.76 million in 2021 to 50.02 million in 2022, respectively. Similarly, America and Africa witnessed 10% and 13% growth rates, respectively, in 2022.

In the railway industry, bio-based PU has potential applications, as it can replace conventional PU products by a significant amount in the coming years. In railways, bio-based foams can be used in seat cushioning and thermal insulation applications.

The Indian Railways were predicted to expand with government ingenuity since they were the third biggest railway industry in the world under a single management. According to the India Brand Equity Foundation, the equivalent of USD 124 billion was projected to be invested in the country's railroads between 2018 and 2022, one of 34 infrastructure sub-sectors.

Furthermore, in the aerospace industry, bio-based PU foams and coatings can substitute conventional PU materials. According to Boeing, the size of the worldwide aerospace services industry is anticipated to exceed USD 3.6 trillion between 2022 and 2041, with the United States and Canada accounting for around 30% of that total, followed by Europe with 23.5 percent of the market.

Therefore, the demand in the transportation industry is expected to increase the demand for bio-based polyurethane during the forecast period.

Asia-Pacific Region is Expected to be the Fastest Growing Market

Asia-Pacific is the largest producer of bio-based polyurethane, with a high abundance of synthetic diisocyanates and a large number of bio-based polyurethane in the region.

Bio-based polyurethane is utilized in construction. It is increasingly utilized for window and door profiles, pipes and guttering, cement, flooring, glass, sealants and adhesives, insulation, building panels, and roofing.

China is amid a construction mega-boom. The country has the largest building market in the region and the world, making up 20% of all construction investments globally. The Chinese government is estimated to have an annual limit for new infrastructure bonds worth CNY 3.85 trillion (USD 0.54 trillion) in 2022, up from CNY 3.65 trillion (USD 0.52 trillion) in 2021.

Bio-PU is capable of replacing polypropylene in automotive applications such as bumpers and bumper spoilers, lateral siding, roof/boot spoilers, rocker panels, body panels, dashboards and dashboard carriers, door pockets and panels, consoles, heating ventilation air conditioning, battery covers, air ducts, pressure vessels, and splash shields.

According to Organisation Internationale des Constructeurs d'Automobiles (OICA), around 27.02 million vehicles were produced in China in 2022, compared to 26.12 million vehicles produced in 2021, witnessing a growth rate of about 3%.

In addition to its electrical insulation, shock resistance, adhesion, and other qualities, bio-based polyurethane is also widely utilized in electrical and electronic applications such as cell phones, mobile devices, computers, and TVs.

Similarly, in India, the electronics market witnessed a growth in demand, with market size increasing at a rapid growth rate. The Ministry of Electronics and Information Technology published the second volume of the Vision document on Electronics Manufacturing in India, which predicted that the electronics manufacturing industry in India would grow from USD 75 billion in 2020-21 to USD 300 billion by 2025-26. The growing electronics and appliances markets in India and China may push the market growth further in Asia-Pacific.

The aforementioned factors are likely to increase the demand for bio-based polyurethane during the forecast period.

Bio-based Polyurethane Industry Overview

The bio-based polyurethane market is consolidated in nature. The major manufacturers in the market studied include BASF SE, Covestro AG, Huntsman International LLC, Mitsui Chemicals Inc., and The Lubrizol Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from the Construction Industry in Developing Countries

4.1.2 Growing Demand from Electronic Appliance Manufacturing.

4.1.3 Other Drivers

4.2 Restraints

4.2.1 High Cost of Bio-based Materials

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Application

5.1.1 Foams

5.1.2 Coatings

5.1.3 Adhesive and Sealants

5.1.4 Other Applications (Polyurethane Binders, Polyurethane Dispersions)

5.2 End-user Industry

5.2.1 Transportation

5.2.2 Footwear and Textile

5.2.3 Construction

5.2.4 Packaging

5.2.5 Furniture and Bedding

5.2.6 Electronics

5.2.7 Other End-user Industries (Biomedical, Fertilizer Industry)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 Brazil

5.3.4.2 Saudi Arabia

5.3.4.3 South Africa

5.3.4.4 Rest of the Countries

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements