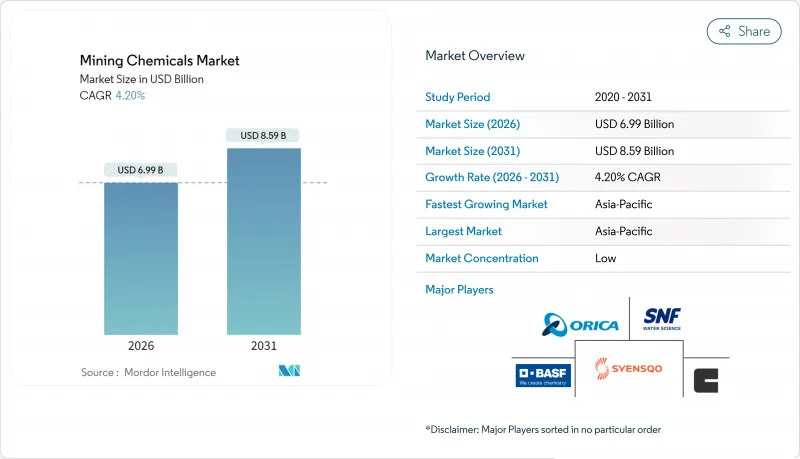

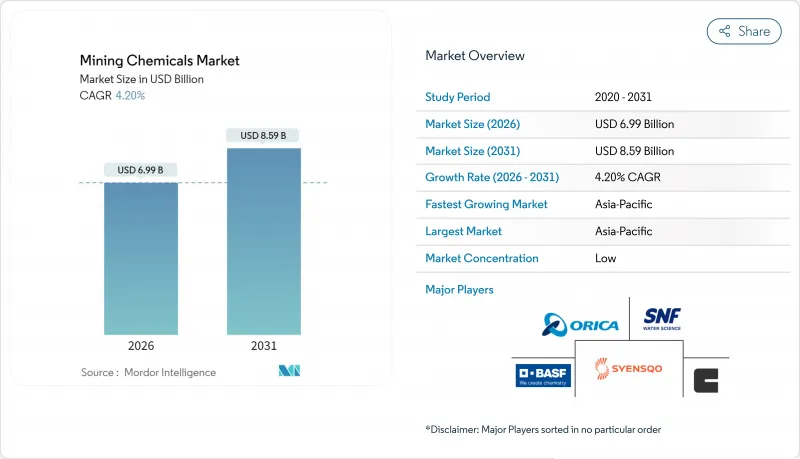

광업용 화학제품 시장은 2025년 67억 1,000만 달러에서 2026년 69억 9,000만 달러로 성장해 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.2%를 나타낼 전망입니다. 2031년까지 85억 9,000만 달러에 달할 것으로 예측됩니다.

배터리용 금속 수요 증가, 환경 규제의 강화, 에너지 전환의 가속에 의해 금속 회수율을 높이면서 물과 전력의 사용량을 삭감하는 보다 선택적이고 환경 효율이 높은 시약 배합에의 구매 판단이 진행되고 있습니다. 아시아태평양은 여전히 주요 생산 기지이며, 북미의 신규 생산 능력과 습식 야금에 대한 전략적 투자는 다른 광업용 화학제품 시장에서의 안정적인 수요 증가를 지원합니다. 부선제가 수익의 기초가 되고 있지만, 가장 강한 기세를 보이고 있는 것은 리튬, 니켈, 코발트, 희토류 원소용의 저탄소 플로우 시트를 가능하게 하는 용매 추출용 시약입니다. 충돌은 중간 정도입니다. 기존 공급업체는 합병 및 인수 및 디지털 최적화를 통해 점유율을 지키는 반면, 소규모 신규 참가 기업은 바이오 화학제품 및 건식 처리 조제를 활용하여 광업용 화학제품 시장에서 미개척 틈새 시장을 개척하고 있습니다.

미국 광업용 화학제품 시장의 시약 수요는 활발해지고 있습니다. 호주 단독에서도 2024-2025년도의 자원 수출 수익은 3,800억 달러에 달했으며, 신규 구리, 리튬, 니켈 프로젝트의 파이프라인 확대에 따라 부선·침출·수처리 패키지용 시약 입찰이 증가하고 있습니다. 동제련소의 처리요금은 2024년 마이너스로 전환되어 농축광 공급의 희박함을 시사함과 동시에 고순도 용매추출제에 의존하는 새로운 습식 야금투자를 촉진하고 있습니다. 금융 분석가의 시산에 따르면 광범위한 산업 설비 투자 사이클에 따라 연간 2.5-5조 달러가 인프라에 투입되어 중요 광물 수요 증가를 통해 광업용 화학제품 시장이 간접적으로 강화될 전망입니다. 디지털 투여 제어와 특수 배합을 통합할 수 있는 공급업체는 사업자가 신규 자산 전체에서 플랜트 화학을 표준화하는 동안 장기 공급 계약을 획득하고 있습니다.

2024년에 가동을 시작한 배터리용 기가팩토리에 의해 미국의 셀 생산량은 40% 급증해 리튬, 니켈, 코발트의 단위당 수요가 가속되었습니다. 이로 인해 2030년까지 세계 광물 수요 예측이 3배로 늘어났습니다. 스포줌 및 라테라이트 처리량이 증가함에 따라 기존의 기본 금속 제련 플로우 시트에 비해 40-200% 많은 화학 시약을 소비하기 때문에 광업용 화학제품 시장 전체에서 용매 추출 및 결정화 시약 수요가 확대되고 있습니다. 동시에 인산철 리튬이나 나트륨 이온 전지 기술로 전환하는 셀 제조업체는 새로운 프로세스 제어상의 과제를 만들어내고 있으며, 이에 대응하기 위해서는 특주의 킬레이트제가 필요합니다. 지정학적 마찰에 의한 중요한 광물 공급의 혼란 우려가 높아지고 있는 가운데, 광산 기업은 공급 리스크를 경감하기 위해 다년간에 걸친 시약 계약을 체결하고 있어 광업용 화학제품 시장의 구조적 성장을 더욱 강화하고 있습니다.

각국 정부는 현재 시안화물, 수은 크산테이트 사용자에게 지속적인 모니터링, 긴급 대응 계획, 폐쇄 후 수처리에 대한 재무 보증을 의무화하는 엄격한 규제 코드에 근거한 등록을 의무화하고 있습니다. 국제 시안화물 관리 코드 및 미국 토지 관리국에 의한 장기 처리 자금에 관한 신규제로 컴플라이언스 비용이 상승하고 있습니다. 유럽 규제 당국은 PFAS계 거품제의 추가 금지를 검토하고 있으며, 광업용 화학제품 시장 전체에서 대체 계면활성제로의 이행이 가속되고 있습니다. 공급업체는 재배합을 할지 시장 접근 제한에 직면할지에 대한 선택을 강요하고 있으며, 단기 성장은 둔화되고 장기적인 혁신을 촉진하는 요인이 되고 있습니다.

2025년 부선약품은 광업용 화학제품 시장 점유율의 55.30%를 차지하고 복잡화하는 광석에서 구리, 아연, 귀금속 황화물을 분리하는데 필수적인 역할을 했습니다. 이 수익의 대부분을 차지하는 컬렉터이며, 억압제, 응집제, 기포제 및 분산제가 이어져 펄프 화학을 최적 동역학으로 조정합니다. Syensqo의 AEROPHINE 시리즈와 같은 프리미엄 콜렉터는 기존의 크산탄계 약에 비해 최대 30% 적은 용량으로 선택성을 향상시키고 비용 절감과 ESG 대응을 양립하고자 하는 광산 사업자로부터 높은 평가를 받고 있습니다. 억제제는 황화철에 의한 희석을 방지하고 합성 기포제는 거친 부유 회로에서 기포 크기를 안정화시킵니다. 광업용 화학제품 시장에서 부선약품 시장 규모는 광석 품위 저하를 배경으로 꾸준한 성장이 예상됩니다. 품위 저하로 인해 회수율을 유지하기 위해서는 분쇄를 미세화하고 보다 많은 화학약품을 추가할 필요가 생기기 때문입니다.

추출제, 희석제, 추출제 및 스트리핑 솔루션은 기능별 부문 중 가장 높은 4.32%의 연평균 복합 성장률(CAGR)로 확장되었습니다. 이 성장 궤도는 리튬 염수, 니켈 라테라이트 및 다금속 정광을 위해 계획된 대규모 습식 야금 라인에 기인합니다. BASF의 수용액 야금 플랫폼은 제련에 비해 40% 적은 에너지로 고순도의 금속염을 생성하기 때문에 용매 추출은 매력적인 탈탄소화 경로가 되고 있습니다.

광업용 화학제품 보고서는 기능별(부선약품, 추출약품, 분쇄조제), 용도별(광물처리 및 폐수처리), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 구리, 니켈 및 희토류 처리에서 중국의 우위성과 인도의 국내 광물 자원 상업화 추진에 의해 2025년 시점에서 광업용 화학제품 시장의 54.10%의 수익 점유율을 유지했습니다. 중국의 리튬 니켈 정련 클러스터와 아프리카 라틴아메리카 광산에 대한 국가 지원 투자가 함께 경제 감속 국면에서도 견조한 수요를 지지하고 있습니다.

북미 시장은 선진 전지 및 중요한 광물 공급망 안전 보장을 추구하는 워싱턴 정책에 의해 성장하고 있습니다. 연방 정부의 인센티브로 1,500억 달러를 넘는 전지 셀·원료 프로젝트가 발표되어, 리튬·니켈·코발트 추출 라인에 있어서 시약 수요를 강화하고 있습니다. 캐나다의 탐사 지출은 2024년에 41억 달러에 달했고, 중소 광산 기업이 희토류·중요 금속 광상의 수용액 야금 시험을 추진했습니다.

유럽은 생산량은 삼가면서 집중적인 기술 혁신을 볼 수 있습니다. EU 중요 원재료법은 국내 정제·리사이클을 지원해, 배터리 재료 순환에 있어서 특수 시약의 채용을 촉진하고 있습니다. BASF사와 클라리언트사는 유럽 공장에서 PFAS 프리의 거품제나 바이오컬렉터를 공급하여 지역의 자급률 향상과 경쟁 차별화를 도모하고 있습니다. 남미의 리튬 삼각지대와 칠레의 구리 광산 확장은 중요한 역할을 하며, 아프리카의 광물 자원은 인프라와 거버넌스의 복잡성을 극복할 수 있는 공급자에게 성장의 여지를 제공합니다. 중동 수요는 작지만 인산 비료와 알루미늄 분야의 수직 통합 메가 프로젝트가 선택적인 성장 영역을 시사합니다.

The Mining Chemicals Market is expected to grow from USD 6.71 billion in 2025 to USD 6.99 billion in 2026 and is forecast to reach USD 8.59 billion by 2031 at 4.2% CAGR over 2026-2031.

Rising demand for battery metals, stricter environmental regulations, and the accelerated energy transition are steering purchasing decisions toward more selective and eco-efficient reagent formulations that raise metal recovery while cutting water and power use. Asia-Pacific remains the dominant production hub, while new capacity in North America and strategic investments in hydrometallurgy underpin steady offtake growth across the rest of the mining chemicals market. Flotation agents continue to anchor revenue, yet the strongest momentum lies in solvent-extraction reagents that enable low-carbon flowsheets for lithium, nickel, cobalt, and rare earths. Competition is moderate: established suppliers defend share through mergers and acquisitions and digital optimization, whereas smaller entrants deploy bio-based chemistries and dry-processing aids to tap under-served niches in the mining chemicals market.

United States is translating into brisk reagent demand in the mining chemicals market. Australia alone expects resource export earnings to reach USD 380 billion in 2024-25, and the pipeline of new copper, lithium, and nickel projects is widening reagent tenders for flotation, leaching, and water treatment packages. Copper smelter treatment charges turned negative in 2024, signaling tight concentrate supply and encouraging fresh hydrometallurgical investments that rely on high-purity solvent-extraction agents. Financial analysts estimate that the broader industrial capex cycle could inject USD 2.5-5 trillion annually into infrastructure, indirectly fortifying the mining chemicals market through higher demand for critical minerals. Suppliers capable of bundling digital dosing control with specialty formulations are winning long-term supply contracts as operators standardize plant chemistry across new assets.

Battery gigafactories commissioned in 2024 catapulted United States cell output by 40%, accelerating the hunt for lithium, nickel, and cobalt units and inflating global mineral demand forecasts three-fold by 2030. Each incremental tonne of spodumene or laterite processed consumes 40-200% more chemical reagents than legacy base-metal flowsheets, lifting solvent-extraction and crystallization reagent volumes across the mining chemicals market. In parallel, cell makers pivoting to lithium iron phosphate and sodium-ion chemistries are creating fresh process-control challenges that require tailor-made chelating agents. Miners are locking in multi-year reagent contracts to de-risk supply as geopolitical friction raises the specter of critical mineral disruptions, reinforcing structural growth for the mining chemicals market.

Governments now compel cyanide, mercury, and xanthate users to register under stricter codes that demand continuous monitoring, emergency response plans, and financial assurance for post-closure water treatment. The International Cyanide Management Code and recent U.S. Bureau of Land Management rules on long-term treatment funds have escalated compliance costs. European regulators consider additional bans on PFAS-based frothers, accelerating the shift toward alternative surfactants across the mining chemicals market. Suppliers must either reformulate or face restricted market access, dampening near-term growth but catalyzing long-run innovation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flotation reagents captured 55.30% of the mining chemicals market share in 2025, underscoring their essential role in separating copper, zinc, and precious-metal sulfides from increasingly complex ores. Collectors account for the largest slice of this revenue, followed by depressants, flocculants, frothers, and dispersants that adjust pulp chemistry for optimum kinetics. Premium collectors such as Syensqo's AEROPHINE series deliver improved selectivity at doses up to 30% lower than legacy xanthates, a feature prized by miners seeking both cost savings and ESG compliance. Depressants eliminate iron sulfide dilution, while synthetic frothers stabilize bubble size in coarse-particle flotation circuits. The mining chemicals market size for flotation reagents is forecast to grow steadily on the back of declining ore grades, which force operators to grind finer and add more chemistries to maintain recovery.

Extraction reagents, diluents, extractants, and stripping solutions, are expanding at a 4.32% CAGR, the highest among functional segments. This trajectory stems from large-scale hydrometallurgical lines planned for lithium brines, nickel laterites, and polymetallic concentrates. BASF's hydrometallurgy platform consumes 40% less energy than smelting and yields high-purity metal salts, making solvent extraction an attractive decarbonization pathway.

The Mining Chemicals Report is Segmented by Function (Flotation Chemicals, Extraction Chemicals, and Grinding Aids), Application (Mineral Processing and Wastewater Treatment), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific maintained a 54.10% revenue hold on the mining chemicals market in 2025 thanks to China's dominant position in copper, nickel, and rare-earth processing as well as India's push to commercialize domestic mineral reserves. China's lithium and nickel refining clusters, coupled with state-backed investments in African and Latin American mines, underpin resilient demand even amid broader economic softening.

North America's market is growing as Washington pursues supply-chain security for advanced batteries and critical minerals. Federal incentives spurred more than USD 150 billion in announced cell and raw-material projects, reinforcing reagent demand in lithium, nickel, and cobalt extraction lines. Canada's exploration spend climbed to USD 4.1 billion in 2024, with junior players driving hydrometallurgy trials for rare-earth and critical-metal deposits.

Europe exhibits modest volume but intensive innovation. The EU Critical Raw Materials Act supports domestic refining and recycling, lifting specialty reagent uptake in battery material loops. BASF and Clariant supply PFAS-free frothers and bio-collectors from European plants, raising regional self-sufficiency and competitive differentiation. South America's lithium triangle and Chilean copper expansions secure a pivotal role, while Africa's mineral wealth offers upside for suppliers able to navigate infrastructure and governance complexities. Middle East demand is minor, yet vertically integrated mega-projects in phosphate fertilizers and aluminum point to selective growth pockets.