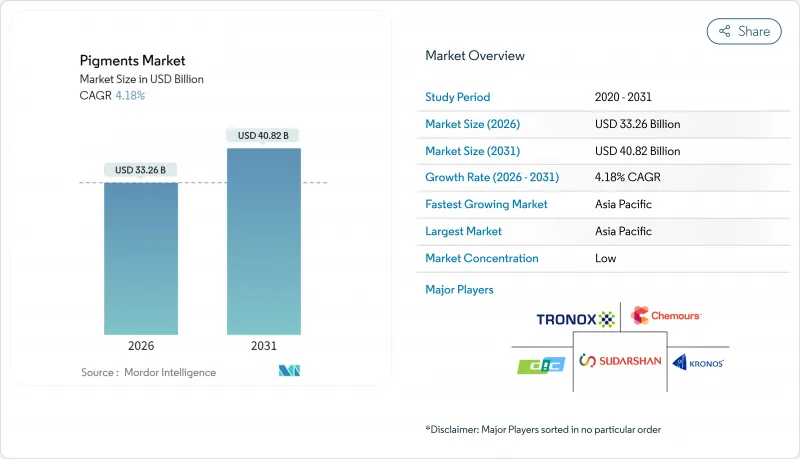

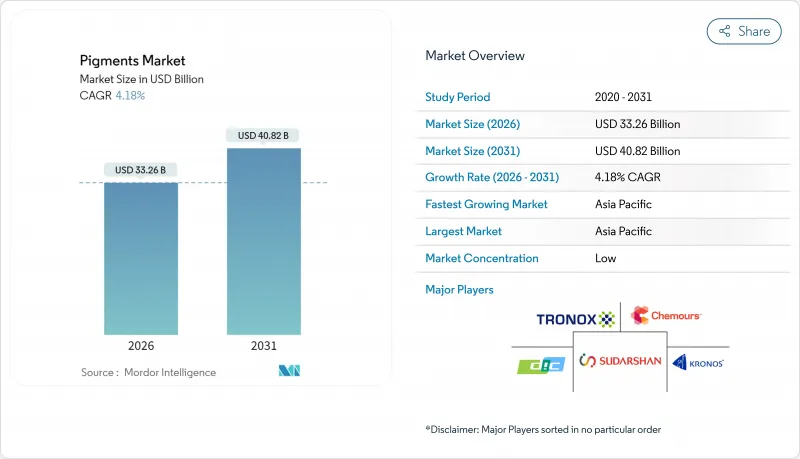

안료 시장은 2025년 319억 3,000만 달러로 평가되었고, 2026년 332억 6,000만 달러에서 2031년까지 408억 2,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 4.18%를 나타낼 전망입니다.

건설, 포장, 모빌리티 분야의 탄탄한 수요가 공급망 재편과 강화되는 안전 규정을 헤쳐나가는 생산자들의 확장을 뒷받침하고 있습니다. 무기계급은 대량 건축용 페인트 시장에서 비용 기반 우위를 유지하는 반면, 유기 및 특수 화학 물질은 고성능 자동차 및 전자 제품 분야에서 점유율을 확보하고 있습니다. 이산화티타늄(TiO2) 조달의 지역적 다각화와 PFAS 및 기타 제한 물질 단계적 폐지 노력은 안료 시장 전반에 걸쳐 제품 재구성 활동을 가속화하고 있습니다. 크로노스 월드와이드의 2024년 7월 루이지애나 안료 회사 인수를 비롯한 통합 움직임은 경쟁 구도를 더욱 형성하며, 이를 통해 규모를 갖춘 기업들은 원자재 조달을 효율화하고 하류 유통망을 강화할 수 있게 되었습니다.

인도네시아, 나이지리아, 베트남의 인프라 프로그램은 건축용 코팅 물량의 꾸준한 증가를 주도하고 있으며, 이는 2024년 10월 인도네시아의 페인트 생산량이 100만 톤을 넘어선 것으로 입증됩니다. 2023년 완료된 9개 중국 지원 프로젝트와 2024년 예정된 5개 프로젝트로 강화된 사하라 이남 아프리카 지역의 시멘트 생산 능력 증가는 건설용 안료 수요를 지속적으로 끌어올리고 있습니다. 정부의 수성, 저휘발성 유기화합물(VOC) 제형 추진으로 공급업체들은 더 엄격한 배출 제한에 부합하는 비용 경쟁력 있는 분산액 공급이 요구되고 있습니다. 그 결과, 주요 건설 클러스터 인근에서 혼합 및 물류 운영을 현지화할 수 있는 중견 안료 생산사들의 잠재적 시장 규모가 확대되고 있습니다. 중기적으로 반복되는 주택 및 교통 인프라 지출은 민간 부문의 재도장 주기가 둔화되더라도 물량을 안정화시키는 다년간 공급 계약으로 이어질 전망입니다.

세계의 규제 기관들은 허용되는 안료 화학 물질의 범위를 체계적으로 축소하고 있습니다. 캘리포니아의 AB 418 법안은 2025년 1월부터 식품 내 TiO2 사용을 금지하며, 뉴질랜드의 화장품 내 PFAS 금지 조치는 2026년 12월 발효됩니다. 로레알과 같은 대형 제형사는 2030년까지 원료의 95%를 바이오 기반 성분으로 조달하겠다고 약속하며, 재생 가능한 착색제로의 산업 전반적 전환을 예고하고 있습니다. 학계와 산업계의 공동 연구를 통해 해조류 유래 피코빌리프로틴과 푸코잔틴을 효소 보조 추출 및 유체역학적 캐비테이션 기술로 상용화하고 있으며, 기존 아조 안료에 필적하는 발색력을 달성하고 있습니다. 기존 화학물질의 규제 준수 비용이 증가함에 따라 초기 규모의 바이오 기반 공급업체들은 대량 시장에서는 이전에 접근할 수 없었던 가격 경쟁력을 활용할 수 있습니다. 그러나 도입은 새로운 바이오 정제 시설의 자본 비용 극복과 실외 코팅과 같은 까다로운 최종 용도의 내구성 기대 충족에 달려 있습니다.

OEKO-TEX는 2024년 10월 제한 물질 테스트 프로토콜을 업데이트하여 PFAS에 대한 알칼리 가수분해 스크리닝을 포함시켰으며, 캐나다는 2025년 3월 전국적인 콜타르 사용 금지를 시행했습니다. 동월 EU REACH 항목 79는 PFHxA 규제를 도입했으며, 여러 미국 주에서는 2025년 1월부터 섬유 제품에 대한 PFAS 금지를 시행했습니다. 각 신규 규정은 안료 공급업체로 하여금 대체 화학 물질을 검증하고 상이한 기준을 적용하는 관할권을 위해 이중 재고를 구축하도록 강제합니다. 준수를 위해서는 ISO 22716 기준의 정교한 품질 관리 시스템이 필요하며, 이는 소규모 생산자가 감당하기 어려운 고정 비용 증가를 초래합니다. 즉각적인 영향은 성숙 시장에서 생산 능력 합리화 물결로 이어져 전술적 가격 경쟁은 감소하지만 신규 진입자의 전략적 진입 장벽은 높아집니다.

2025년 무기 클러스터는 안료 시장의 75.42% 점유율을 유지했으며, 이는 건축 및 포장 제형에서 불투명도와 백색도를 위한 TiO2의 필수성에 기반한 위치입니다. 이 그룹 내에서 산화철은 비용 및 내구성 이점으로 인해 석조 코팅 및 건설 자재 시장을 계속해서 지배하고 있습니다. 유기 안료는 규모는 작지만, 낮은 중금속 함량을 요구하는 응용 분야에서 우수한 채도와 규제 완화 여력을 활용하여 2031년까지 연평균 5.18% 성장률을 보일 전망입니다. 고성능 퀴나크리돈 및 페릴렌은 현재 자동차 기반코트에 널리 사용되고 있으며, 디케토피롤로피롤 레드는 소비자 가전 제품 외장재로 진출하고 있습니다. 열변색 및 자성 안료와 같은 특수 하위 부문은 보안 인쇄 및 전자 부품 마킹 분야에서 프리미엄 계약을 따내고 있습니다.

티타니아 원료의 비용 상승으로 일부 유연 포장 작업이 고불투명도 유기 대체재로 전환되고 있으나, 기능적 동등성으로 인해 광범위한 대체는 여전히 제한적입니다. 선케어 화장품에 아연산화물 자외선 차단제가 도입되면서 광물성 안료의 점진적 성장이 촉진되어 기존 종이 응용 분야의 수요 부진을 상쇄하고 있습니다. 카본 블랙은 전도성 폴리머 화합물 및 토너 시스템에서 안정적인 입지를 유지하고 있습니다. 전반적으로 무기 부문은 성숙 단계에 접어들면서 경쟁의 초점이 공정 효율성으로 이동한 반면, 유기 공급업체들은 분자 혁신과 최종 사용자 협력을 중심으로 경쟁하고 있습니다.

본 안료 보고서는 제품 유형별(무기 안료, 유기 안료, 특수 안료 및 기타 제품 유형), 용도별(페인트 및 코팅, 섬유, 인쇄 잉크, 플라스틱, 가죽, 기타 용도), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

아시아태평양 지역은 2025년 세계의 매출의 45.60%를 차지했으며, 2031년까지 연평균 5.32%의 가장 빠른 성장률을 기록할 것으로 예상되어 규모와 성장 동력 모두에서 선도적 위치를 공고히 할 것입니다. 중국은 지역 안료 생산량의 약 절반을 차지하며, TiO2 생산 능력 변동과 에너지 집약도 부과금을 통해 세계의 가격 결정에 지속적으로 영향을 미치고 있습니다. 인도의 특수 화학 분야 생산 연계 인센티브는 일본 및 유럽 안료 대기업과의 합작 투자를 촉진하여 해당 지역의 제품 포트폴리오를 확대하고 있습니다. 인도네시아의 건축용 페인트 생산량은 2024년 말 100만 톤을 초과하며, 품질 기대치가 상승하는 성숙한 국내 시장을 시사합니다.

북미와 유럽은 총량은 상대적으로 적지만, 기술적 차별화와 공급망 안정성을 보상하는 부가가치 높은 틈새 시장으로 전환 중입니다. 미국 국방수권법에 따른 특수화학물질 연방 자금 지원은 국내 안료 중간재 생산에 자본을 유입시켜 구매자들이 지정학적 혼란으로부터 부분적으로 보호받고 있습니다.

중동 및 아프리카는 기회주의적 성장 지역으로 부상 중입니다. 걸프협력회의(GCC) 국가들은 다운스트림 다각화의 일환으로 염화물 공정 TiO2에 투자하고 있으며, 북아프리카 섬유 클러스터는 근해 조달을 원하는 유럽 브랜드를 유치하고 있습니다. 남미의 성장 궤적은 인프라 지출 및 자동차 조립량에 영향을 미치는 거시경제 안정화와 원자재 수출 주기에 연동됩니다.

The Pigments Market was valued at USD 31.93 billion in 2025 and estimated to grow from USD 33.26 billion in 2026 to reach USD 40.82 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031).

Resilient demand for construction, packaging, and mobility applications underpins this expansion even as producers navigate supply chain realignments and tightening safety rules. Inorganic grades retain cost-based advantages in bulk architectural coatings, while organic and specialty chemistries capture share in high-performance automotive and electronics uses. Regional diversification of titanium dioxide (TiO2) sourcing, coupled with initiatives to phase out PFAS and other restricted substances, is accelerating product reformulation activity across the pigments market. Competitive dynamics are further shaped by consolidation, exemplified by Kronos Worldwide's July 2024 acquisition of Louisiana Pigment Company, which is allowing scale players to streamline raw-material procurement and reinforce downstream distribution reach.

Infrastructure programs in Indonesia, Nigeria, and Vietnam are driving a steady uptick in architectural coatings volumes, evidenced by Indonesia's paint output surpassing 1.00 million tons in October 2024. Growing cement capacity across sub-Saharan Africa-bolstered by nine Chinese-backed projects completed in 2023 and five more slated for 2024-continues to lift demand for construction-grade pigments. Governments' drive toward water-based, low-VOC formulations is forcing suppliers to deliver cost-competitive dispersions compatible with stricter emission limits. The result is a larger addressable base for mid-tier pigment producers able to localize blending and logistics operations near major construction clusters. Over the medium term, recurring housing and transport infrastructure outlays are expected to translate into multi-year offtake contracts that stabilize volumes even when private sector repaint cycles slow.

Global regulators are methodically narrowing the palette of allowable pigment chemistries. California's AB 418 will prohibit TiO2 in foods from January 2025, while New Zealand's cosmetics ban on PFAS enters force in December 2026. Large formulators such as L'Oreal have pledged to source 95% bio-based ingredients by 2030, signaling an industry-wide pivot toward renewable colorants. Academic and industrial programs are commercializing seaweed-derived phycobiliproteins and fucoxanthin using enzyme-assisted extraction and hydrodynamic cavitation, achieving color strength comparable with conventional azo pigments. As compliance costs rise for incumbent chemistries, early-scale bio-based suppliers can exploit a pricing corridor that was previously unavailable in volume markets. Adoption, however, hinges on overcoming the capital cost of new biorefinery infrastructure and meeting the durability expectations of demanding end uses such as outdoor coatings.

OEKO-TEX updated its restricted-substance testing protocol in October 2024 to include alkaline hydrolysis screening for PFAS, and Canada enacted a nationwide coal-tar ban in March 2025. EU REACH Entry 79 introduced PFHxA controls in the same month, while several U.S. states imposed PFAS prohibitions on textiles from January 2025. Each new rule forces pigment suppliers to validate alternative chemistries and establish dual inventories to serve jurisdictions with divergent thresholds. Compliance requires sophisticated quality-management systems under ISO 22716, raising fixed costs that smaller producers struggle to absorb. The immediate impact is a wave of capacity rationalization in mature markets, reducing tactical price competition but heightening strategic barriers for new entrants.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The inorganic cluster maintained 75.42% share of the pigments market in 2025, a position anchored by TiO2's indispensability for opacity and whiteness in architectural and packaging formulations. Within this cohort, iron oxides continue to dominate masonry coatings and construction materials thanks to cost and durability advantages. Organic pigments, although smaller in volume, are set to advance at a 5.18% CAGR to 2031, leveraging superior chroma and regulatory headroom in applications that demand low heavy-metal content. High-performance quinacridones and perylenes now populate automotive basecoats, while diketopyrrolo-pyrrole reds are penetrating consumer electronics housings. Specialty sub-segments, such as thermochromic and magnetic pigments, are winning premium contracts in security printing and electronic component marking.

Cost inflation for titania feedstock is tilting certain flexible-packaging jobs toward high-opacity organic alternatives, though functional equivalence still limits broader substitution. The introduction of zinc-oxide UV blockers in sun-care cosmetics is driving incremental growth for mineral pigments, offsetting softer demand in legacy paper applications. Carbon blacks retain a stable foothold in conductive polymer compounds and toner systems. Overall, the inorganic segment's maturity has shifted competitive emphasis toward process efficiency, whereas organic suppliers compete on molecular innovation and end-user collaboration.

The Pigments Report is Segmented by Product Type (Inorganic Pigments, Organic Pigments, and Specialty Pigments and Other Product Types), Application (Paints and Coatings, Textiles, Printing Inks, Plastics, Leather, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held a 45.60% share of global revenue in 2025 and is expected to post the fastest 5.32% CAGR through 2031, cementing its lead in both scale and momentum. China accounts for roughly half of regional pigment output and continues to influence global price discovery through its TiO2 capacity swings and energy-intensity levies. India's production-linked incentives for specialty chemistry are encouraging joint ventures with Japanese and European pigment majors, thereby broadening the region's product breadth. Indonesia's output of architectural coatings exceeded 1.00 million tons in late 2024, signaling a maturing domestic market with rising quality expectations.

North America and Europe, though collectively smaller in volume, are pivoting toward value-add niches that reward technical differentiation and supply-chain security. U.S. federal funding for specialty chemicals under defense authorization acts is channeling capital into domestic pigment intermediates, partially insulating buyers from geopolitical disruptions.

The Middle East and Africa are emerging as opportunistic growth zones. Gulf Cooperation Council countries are investing in chloride-route TiO2 as part of downstream diversification, while North African textile clusters are courting European brands seeking near-shore sourcing. South America's trajectory is tied to macroeconomic stabilization and commodity export cycles that affect infrastructure spending and automotive assembly volumes.