ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

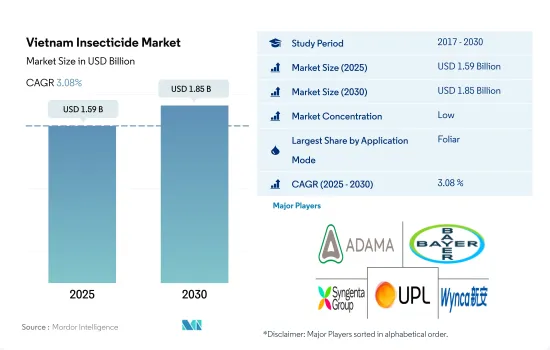

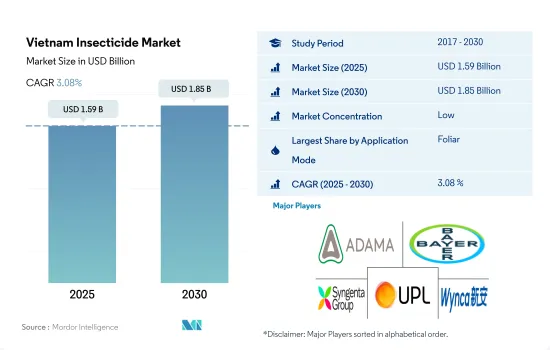

베트남의 살충제 시장 규모는 2025년에 15억 9,000만 달러로 추정·예측되며, 2030년에는 18억 5,000만 달러에 달하며, 예측 기간(2025-2030년)의 CAGR은 3.08%로 성장할 것으로 예측됩니다.

스템보러, 아미웜, 진딧물에 의한 농작물 손실이 빈번하게 발생, 살충제 사용량 증가

베트남 농가는 주요 작물에 위협이 되는 해충을 퇴치하기 위해 주로 살충제에 의존하고 있습니다. 농가는 특정 해충과 작물에 따라 적절한 살포 방법을 채택하여 다양한 작물에서 해충을 효과적으로 방제하고 있습니다. 이러한 접근 방식은 해충의 피해를 줄이고 농작물을 보호할 수 있습니다.

2022년 시장에서는 살충제 엽면 살포가 57.7%로 가장 큰 점유율을 차지했습니다. 이러한 우위는 이 방법과 관련된 여러 가지 장점에 기인하는 것으로 보입니다. 살충제를 식물의 잎에 직접 뿌려서 원하는 해충에 신속하고 효율적으로 작용할 수 있습니다. 또한 벼와 옥수수와 같은 이 국가의 주요 작물은 벼멸구, 벼멸구, 진딧물 등의 해충에 매우 취약합니다. 엽면 살충제 살포를 통해 농가는 해충의 개체수를 효과적으로 방제하고 관리할 수 있습니다. 이 유리한 접근 방식이 국내에서의 엽면살포의 채택 확대에 기여하고 있습니다.

2022년에는 종자 처리가 살충제 살포의 또 다른 중요한 방법으로 부상하여 16.8% 시장 점유율을 차지했습니다. 이 방법은 종자를 적절한 살충제로 처리하여 초기 단계에서 작물 성장에 큰 영향을 미치는 곤충 유충과 선충을 방제하는 데 효과적입니다. 이 방법의 채택이 확대되고 있는 이유는 종자 처리 살충제의 최신 발전으로 지상과 지하 모두에서 해충을 효과적으로 방제할 수 있게 되었기 때문입니다.

농가가 사용하는 다른 살포 방법으로는 화학 관개, 훈증, 토양 처리 등이 있습니다. 해충 확산 증가와 생산성 향상에 대한 요구가 CAGR 3.3%로 시장을 촉진할 것으로 예상됩니다.

베트남 살충제 시장 동향

해충 발생 증가, 기상 조건의 변화, 집약적 농법 채택으로 살충제 소비 증가 전망

베트남에서는 기상 조건의 변화와 전통적인 해충 방제 방법에 저항하는 해충의 출현으로 인해 해충 발생이 증가함에 따라 농작물용 살충제 소비가 증가할 것으로 예상됩니다. 이 두 가지 요인 모두 증가하는 해충 문제를 해결하기 위한 살충제 수요를 증가시키고 있습니다.

2019년 FAW의 전국적인 급속한 확산은 농업 부문에 큰 영향을 미쳐 농작물에 상당한 피해를 입혔습니다. 올해 40개 성에서 35,000헥타르 이상의 옥수수가 FAW의 피해를 입었습니다. 그 결과 농가가 농작물을 보호하기 위해 살충제 사용을 늘리면서 이 기간 중 제초제 소비가 눈에 띄게 증가했습니다.

식량 수요 증가에 따라 농업 활동이 크게 확대되고 있습니다. 이러한 확대로 인해 농작물을 보호하기 위한 해충 방제 대책이 강화될 가능성이 있습니다. 그 결과, 특히 집약적인 농법을 사용하는 지역에서는 살충제 사용량이 증가할 것으로 예상됩니다.

베트남에서도 유전자 변형 옥수수의 재배가 크게 증가하여 2020년 현재, 내충성 품종을 포함한 GE 옥수수의 재배 면적은 약 92,000헥타르에 달하며 전체 재배 면적의 약 10%를 차지합니다. 베트남에서 GE 옥수수의 재배가 증가함에 따라 살충제 소비에 영향을 미쳤습니다.

따라서 해충 발생 증가, 기상 조건의 변화, 집약적 농법의 채택은 베트남 농작물에 대한 살충제 사용량을 증가시킬 것으로 예상되는 주요 요인입니다.

베트남은 대부분의 살충제를 중국, 인도, 미국에서 수입하고 있으며, 세계 3위의 살충제 수입국입니다.

베트남은 살충제 유효성분을 수입에 의존하고 있으며, 베트남 국내에서 살충제 유효성분을 생산하는 기업은 제한적입니다. 베트남은 시퍼메트린과 이미다클로프리드의 대부분을 중국, 독일, 인도에서 수입하고 있습니다. 이들 유효 성분의 가격은 해충 발생률, 환율, 수입 관세 등 다양한 요인에 따라 달라집니다.

시퍼메트린은 합성 피레스로이드계 살충제로 2022년 톤당 2만 1,100달러로 평가되었습니다. 시퍼메트린은 베트남의 곡물과 두류에 영향을 미치는 비늘날개목, 칼날날개목, 쌍날개목, 반날개목 등 다양한 해충을 방제합니다. 마찬가지로 이미다클로프리드는 침투성 살충제이며, 2022년 톤당 1만 7,200달러로 평가되었습니다. 이미다클로프리드는 다양한 작물의 흡즙성 및 씹는 곤충을 방제하는 데 사용됩니다.

말라티온은 유기인계 살충제로 2022년 톤당 1만 2,500달러의 가치가 있습니다. 말라티온은 남베트남의 주요 해충인 지렁이, 파리 등의 해충을 방제하는 데 사용됩니다. 이들 해충은 구아바, 사포타, 사워솝, 파파야, 용과 등의 작물에서 연간 30.0%의 수확량 손실을 가져옵니다.

베트남은 대부분의 살충제를 중국, 인도, 미국에서 수입하고 있습니다. 전 세계에서 베트남은 세 번째로 큰 살충제 수입국이며, 2018년에는 국내 홍수가 발생하여 국내외 공급망이 끊어졌습니다. 그 결과, 운송 경로가 영향을 받아 수요 증가와 유효 성분의 제한된 공급으로 이어졌습니다. 이로 인해 2018년에는 유효 성분의 가격이 상승했습니다.

베트남의 살충제 산업 개요

베트남의 살충제 시장은 단편화되어 있으며, 상위 5사에서 12.07%를 차지하고 있습니다. 이 시장의 주요 기업은 다음과 같습니다. ADAMA Agricultural Solutions Ltd., Bayer AG, Syngenta Group, UPL Limited and Wynca Group(Wynca Chemicals)(알파벳순).

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 개요와 주요 조사 결과

제2장 리포트 오퍼

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효 성분의 가격 분석

규제 프레임워크

베트남

밸류체인과 유통 채널 분석

제5장 시장 세분화

사용 방법

약제 살포

엽면살포

훈증

종자 처리

토양 처리

작물 유형

상업 작물

과일·채소

곡물

두류·지방 종자

잔디·관상용

제6장 경쟁상황

주요 전략 동향

시장 점유율 분석

기업 상황

기업 개요(세계 레벨의 개요, 시장 레벨의 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 랭크, 시장 점유율, 제품·서비스, 최근 동향 분석 포함)

ADAMA Agricultural Solutions Ltd.

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

PI Industries

Syngenta Group

UPL Limited

Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 개요

개요

Porter's Five Forces 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고 문헌

도표

주요 인사이트

데이터 팩

용어집

KSA

영문 목차

영문목차

The Vietnam Insecticide Market size is estimated at 1.59 billion USD in 2025, and is expected to reach 1.85 billion USD by 2030, growing at a CAGR of 3.08% during the forecast period (2025-2030).

Frequent crop losses due to stem borers, armyworms, and aphids increase the usage of insecticides

Vietnamese farmers primarily rely on insecticides to combat insect pests that pose a threat to major crops. Depending on the specific pests and crops, farmers adopt suitable application methods to control the pests effectively across a wide range of crops. This approach allows them to mitigate the damage caused by pests and protect their agricultural produce.

In 2022, the market was largely dominated by the foliar application of insecticides, which held a significant share of 57.7%. This dominance could be attributed to the numerous benefits associated with this method. Directly applying insecticides to the leaves of plants enables rapid and efficient action against targeted pests. Moreover, the country's prominent crops, such as rice and maize, are highly susceptible to insect pests like rice stem borers, armyworms, and aphids. Through the utilization of foliar insecticide applications, farmers can effectively control and manage pest populations. This advantageous approach has contributed to the growing adoption of foliar applications in the country.

In 2022, seed treatment emerged as another significant mode of applying insecticides, representing a market share of 16.8%. This method involves treating seeds with suitable insecticides, which proves effective in controlling insect larvae and nematodes that significantly impact crop growth during the early stages. The growing adoption of this approach can be attributed to the latest advancements in seed treatment insecticides, enabling effective control of pests both above and below the ground.

Other application modes used by the farmers include chemigation, fumigation, and soil treatment. Increasing pest infestations and the need for higher productivity are expected to drive the market at a CAGR of 3.3%.

Vietnam Insecticide Market Trends

The increasing occurrence of pests, changes in weather conditions, and the adoption of intensive farming practices are expected to increase the consumption of insecticides

In Vietnam, the consumption of pesticides for crops is expected to increase due to the increasing prevalence of pests as a result of changing weather conditions and the emergence of pest populations that are resistant to conventional control methods. Both these factors have driven demand for insecticides to combat the growing pest issues.

The rapid spread of FAW across the country in 2019 significantly impacted the agricultural sector, causing considerable damage to crops. Over 35,000 hectares of corn were affected by FAW in 40 provinces during that year. As a consequence, the consumption of herbicides witnessed a notable increase during this period as farmers increased their usage of insecticides to safeguard their crops.

Agricultural activities have expanded significantly in response to the rising demand for food. This expansion may necessitate enhanced pest control measures to protect crops from damage. Consequently, the usage of insecticides is expected to increase, particularly in regions where intensive farming practices are employed.

Vietnam has also witnessed a substantial rise in the cultivation of GE corn varieties. As of 2020, approximately 92,000 hectares of GE corn were planted, including insect-resistant varieties, which accounted for approximately 10% of the total crop area. This increase in GE corn cultivation in Vietnam impacted insecticide consumption.

Therefore, the increasing occurrence of pests, changes in weather conditions, and the adoption of intensive farming practices are the primary factors that are expected to increase the utilization of insecticides for crops in Vietnam.

Vietnam imports most of its insecticides from China, India, and the United States and is the third-largest importer of insecticides in the world

Vietnam is an import-dependent country in terms of active ingredients for insecticides; there are limited companies in Vietnam that produce active ingredients for pesticides. Vietnam imports the majority of Cypermethrin and Imidacloprid from China, Germany, and India. The prices of these active ingredients depend on various factors such as pest incidence, currency exchange rates, and import tariffs.

Cypermethrin is a synthetic pyrethroid insecticide, which was valued at USD 21.1 thousand per metric ton in 2022. Cypermethrin controls a wide range of pests, including Lepidoptera, Coleoptera, Diptera, and Hemipteran, that affect cereals and pulses in Vietnam. Similarly, Imidacloprid is a systemic insecticide, which was valued at USD 17.2 thousand per metric ton in 2022. Imidacloprid is used to control sucking and chewing insects in various crops.

Malathion is an organophosphate insecticide, which was valued at USD 12.5 thousand per metric ton. Malathion is used to control weevils and fruit flies, which are major pests in South Vietnam. These pests cause up to 30.0% annual yield losses in crops such as guava, sapota, soursop, papaya, and dragon fruit.

Vietnam imports most of its insecticides from China, India, and the United States. Globally, Vietnam is the third-largest importer of insecticides. In 2018, there was a flood in the country that disrupted supply chains, both domestically and internationally. As a result, transportation routes were affected, leading to increased demand and a limited supply of active ingredients. Owing to that, the prices of active ingredients increased in 2018.

Vietnam Insecticide Industry Overview

The Vietnam Insecticide Market is fragmented, with the top five companies occupying 12.07%. The major players in this market are ADAMA Agricultural Solutions Ltd., Bayer AG, Syngenta Group, UPL Limited and Wynca Group (Wynca Chemicals) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Seed Treatment

5.1.5 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd.

6.4.2 BASF SE

6.4.3 Bayer AG

6.4.4 Corteva Agriscience

6.4.5 FMC Corporation

6.4.6 PI Industries

6.4.7 Syngenta Group

6.4.8 UPL Limited

6.4.9 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS