중국의 살충제 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

China Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683985

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

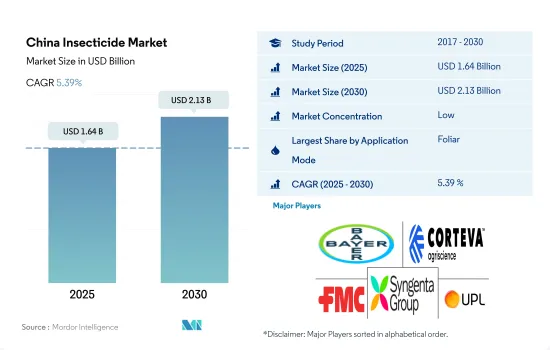

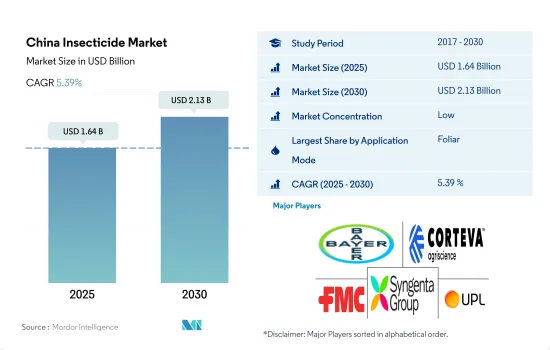

중국의 살충제 시장 규모는 2025년에 16억 4,000만 달러에 달할 것으로 추정됩니다. 2030년에는 21억 3,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 5.39%로 성장할 전망입니다.

해충 압력 상승, 농작물 손실 증가, 효과적인 해충 제거 방법의 필요성이 살충제 수요를 촉진

중국의 살충제 시장은 다양한 살포 방법으로 성장하고 있습니다. 이러한 다양한 살포 기술은 해충을 효과적으로 제거하고 작물을 안전하게 보호하기 위한 다양한 옵션을 제공합니다.

중국의 살충제 시장을 독점하고 있는 것은 엽면 처리입니다. 이 분야는 2023년부터 2029년에 걸쳐 금액 기준으로 CAGR 5.8%를 나타낼 것으로 예측되고 있습니다. 기계화, 강화된 작물 품종, 첨단 농업 기술과 같은 현대 농업 관행의 급속한 도입이 이 성장의 주요 추진력이 되고 있습니다. 농가가 이러한 진보를 채택함에 따라, 작물의 수율을 최적화하는데 있어서 효과적인 해충 방제가 완수하는 역할을 인식하게 되고 있습니다. 이 인식은 중국에서 해충 관리 전략의 필수적인 부분으로서 특히 엽면 살포에 의한 살충제 수요를 더욱 촉진하고 있습니다.

2023년부터 2029년 사이에, 상업용 작물에서 살충제 종자 처리 시장은 450만 달러 성장할 것으로 예측됩니다. 중국의 대규모 상업 생산자는 종자 처리를 표준 방법으로 채택합니다. 이 방법을 채택함으로써, 그들은 가치가 높은 작물에 대한 투자를 보호하는 이점을 알고 있습니다.

토양 처리는 중국의 살충제 시장에서 가장 빠르게 성장하는 부문 중 하나이며 예측 기간 동안 금액 기준으로 CAGR 5.2%를 나타낼 것으로 예상됩니다. 이 나라의 농부들은 장기적인 해충 방제, 토양 전염성 병해 예방, 작물 전체의 건전성과 생산성 향상에 효과적이기 때문에 이 방법을 해충 관리 전략에 도입하는 경향이 강해지고 있습니다. 따라서 중국의 살충제 시장은 2023년부터 2029년에 걸쳐 금액 기준으로 CAGR 5.7%를 나타낼 것으로 예측됩니다.

중국의 살충제 시장 동향

농약 사용량의 제로 성장과 IPM 전략으로 헥타르당 살충제 소비량이 크게 감소

중국의 헥타르당 살충제 소비량은 2017년에서 2022년에 걸쳐 13.1% 감소했지만, 이는 몇 가지 요인 때문입니다. 최근 중국은 살충제의 사용량을 줄이고, 유해한 살충제를 금지하고, 화학농약 소비량의 제로 성장을 달성하기 위한 여러 정부 정책을 시행하고 있습니다. 이러한 정책은 지속 가능한 농업을 추진하고 농법이 환경에 미치는 영향을 최소화하는 국가의 광범위한 노력의 일환입니다. 그 결과, 유전자 재조합 작물이나 식물 유래의 프로테아제 억제제의 사용 등 해충 방제의 대체 방법으로 이동하고 있습니다.

유전자 변형 작물(GMO)로도 알려진 트랜스 제닉 작물은 특정 해충에 대한 저항성을 통합하여 개발되었습니다. 천연 해충 저항성 종의 유전자를 작물에 도입함으로써 화학 살충제를 사용하지 않고 특정 해충으로부터 작물을 보호 할 수 있습니다. 이 접근법은 중국에서 인기를 얻고 있으며 유전자 변형 면화, 옥수수 및 기타 작물 재배에 성공했습니다.

유전자 변형 작물 외에도 중국은 합성 살충제를 대체하는 천연 물질로 식물 유래 프로테아제 억제제의 사용을 모색하고 있습니다. 프로테아제 억제제는 곤충의 다양한 생리 작용에 관여하는 효소인 프로테아제의 활성을 억제하는 물질입니다. 이 억제제를 농작물에 도입하면 해충의 소화 기관을 혼란시켜 식물에 대한 해를 줄일 수 있습니다.

위와 같은 정부 정책의 실시와 대체 해충 방제 방법의 채용 증가로 중국에서는 1헥타르당 살충제 사용량이 감소하고 있습니다.

활성 성분의 가격은 국내 날씨, 질병 발생, 에너지 가격, 인건비 등의 요인에 크게 영향을 받습니다.

중국에서는 작물 해충의 피해를 입은 농지가 지난 50년간 4배로 증가하고 있는데, 이는 주로 기후 변화 때문입니다. 중국에서 가장 많이 발생하는 해충은 나방과 나비를 포함한 비늘 눈(및 가을 육군 웜)으로 피해를 입은 농지의 1/3 이상을 차지합니다. 이어 진딧물, 반, 요코바이를 포함한 동선 눈입니다.

시펠메트린은 피레스로이드계 농약 중에서 가장 널리 사용되고 있으며, 중국에서는 야채와 과일의 미바에, 붕어벌레, 메리충 등 많은 해충을 제거하고 있습니다. 2022년에는 톤당 2만 900달러로 평가되었습니다.

말라티온은 진딧물, 벼룩 및 기타 많은 귀중한 작물의 흡즙성 해충을 포함한 광범위한 해충 치료에 사용됩니다. 중국에서 널리 재배되고 말라티온을 자주 사용하는 다섯 가지 작물은 체리 토마토, 브로콜리, 뽕나무, 크랜베리, 무화과입니다. 2022년 가격은 톤당 12,400달러였습니다. 중국은 잠재적인 환경 위험을 줄이기 위해 저독성의 고효율 농약 개발에 전념하고 있기 때문에 저독성은 말라티온의 가장 큰 장점 중 하나입니다. 이러한 요인은 중국의 말라티온 가격에 더욱 영향을 미칠 것으로 보입니다.

이미다클로프리드는 전형적인 네오니코티노이드계 살충제로, 2022년 가격은 톤당 1만 7,000달러였습니다. 이미다 클로프리드는 주로 벼, 밀, 야채, 면화 등의 작물의 플랜트 호퍼나 진딧물의 방제에 이용됩니다. 이미다클로프리드의 최대 소비국은 쌀이며 밀은 중국에서 재배되는 작물 중 2위입니다.

활성 성분의 가격은 국내 날씨, 질병 발생, 에너지 가격, 인건비 등의 요인에 크게 영향을 받습니다.

중국의 살충제 산업 개요

중국의 살충제 시장은 세분화되어 있으며 상위 5개사에서 37.15%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited(알파벳순 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

중국

밸류체인과 유통채널 분석

제5장 시장 세분화

사용 방법

화학 처리

엽면 처리

훈증 처리

종자 처리

토양 처리

작물 유형

상업 작물

과일 및 채소

곡물

맥류 및 유지종자

잔디 및 관상용 식물

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Jiangsu Yangnong Chemical Co. Ltd

Lianyungang Liben Crop Technology Co. Ltd

Rainbow Agro

Syngenta Group

UPL Limited

Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The China Insecticide Market size is estimated at 1.64 billion USD in 2025, and is expected to reach 2.13 billion USD by 2030, growing at a CAGR of 5.39% during the forecast period (2025-2030).

The rising pest pressure, increasing crop losses, and the need for effective pest control methods are driving the demand for insecticides

The Chinese insecticide market is experiencing growth across various application methods. These diverse application techniques offer a wide range of options to effectively control insect pests and ensure crop protection.

The foliar application method dominates the insecticide market in China. This segment is projected to register a CAGR of 5.8% in terms of value from 2023 to 2029. The rapid adoption of modern agricultural practices, such as mechanization, enhanced crop varieties, and advanced farming techniques, has been a key driver of this growth. As farmers adopt these advancements, they are increasingly realizing the role of effective pest control in optimizing crop yields. This recognition has further fueled the demand for insecticides, specifically through foliar application, as an essential part of pest management strategies in China.

Between 2023 and 2029, the insecticide seed treatment market in commercial crops is projected to grow by USD 4.5 million. Large-scale commercial growers in China are adopting seed treatment as standard practice. By adopting this method, they are recognizing the advantages of protecting their investments in highly valuable crops.

Soil treatment is one of the fastest-growing segments in the insecticide market in China, which is expected to register a CAGR of 5.2% in terms of value during the forecast period. Farmers in the country are increasingly incorporating this method into their pest management strategies due to its effectiveness in long-term pest control, prevention of soil-borne diseases, and enhancement of overall crop health and productivity. Therefore, the Chinese insecticide market is forecast to register a CAGR of 5.7% in terms of value during 2023-2029.

China Insecticide Market Trends

Zero growth in pesticide usage and IPM strategies have contributed to a significant reduction in the per hectare insecticide consumption

The consumption of insecticides in China per hectare decreased by 13.1% from 2017 to 2022, attributed to several factors. In recent years, China has implemented several government policies aimed at reducing the usage of insecticides, banning harmful insecticidal products, and achieving zero growth in chemical pesticide consumption. These policies are part of the country's broader efforts to promote sustainable agriculture and minimize the environmental impact of agricultural practices. As a result, there has been a shift toward alternative methods of pest control, including the use of transgenic crops and plant-derived protease inhibitors.

Transgenic crops, also known as genetically modified organisms (GMOs), have been developed with built-in resistance to certain pests. Introducing genes from naturally pest-resistant species into crops can help them defend themselves against specific insects without the need for chemical insecticides. This approach has gained traction in China, where genetically modified cotton, maize, and other crops have been successfully cultivated.

In addition to transgenic crops, China has been exploring the use of plant-derived protease inhibitors as a natural alternative to synthetic insecticides. Protease inhibitors are substances that inhibit the activity of proteases, which are enzymes involved in various physiological processes of insects. Incorporating these inhibitors into crops can aim to disrupt the digestive systems of insect pests, rendering them less harmful to plants.

The implementation of the above-mentioned government policies and the rising adoption of alternative pest control methods have contributed to a reduction in the usage of insecticides per hectare in China.

Active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country

The amount of farmland hit by crop pests in China has quadrupled in the past 50 years, mainly due to climate change. The most prevalent pests in China are lepidoptera, the order that includes moths and butterflies (and fall armyworms), which accounted for more than a third of the affected cropland. This was followed by homoptera, which includes aphids, cicadas, and leafhoppers.

Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at a price of USD 20.9 thousand per metric ton in 2022.

Malathion is used to control a wide range of pests, including aphids, fleas, and other sucking pests on a number of valuable crops. Five crops that are extensively grown in China that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. It was valued at a price of USD 12.4 thousand per metric ton in 2022. Low toxicity is one of malathion's largest advantages, as China is dedicated to developing low-toxic and highly efficient pesticides to reduce potential environmental risks. Such factors will further influence the price of malathion in China.

Imidacloprid is a typical neonicotinoid insecticide, priced at USD 17.0 thousand per metric ton in 2022. Imidacloprid is mainly used in the control of planthoppers and aphids on crops like rice, wheat, vegetables, and cotton. Rice is the largest consumer of imidacloprid, and wheat ranks second among crops cultivated in China.

The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Insecticide Industry Overview

The China Insecticide Market is fragmented, with the top five companies occupying 37.15%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 China

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Seed Treatment

5.1.5 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 BASF SE

6.4.2 Bayer AG

6.4.3 Corteva Agriscience

6.4.4 FMC Corporation

6.4.5 Jiangsu Yangnong Chemical Co. Ltd

6.4.6 Lianyungang Liben Crop Technology Co. Ltd

6.4.7 Rainbow Agro

6.4.8 Syngenta Group

6.4.9 UPL Limited

6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS