미국의 EV 배터리 팩 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2029년)

US EV Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029)

상품코드:1683886

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

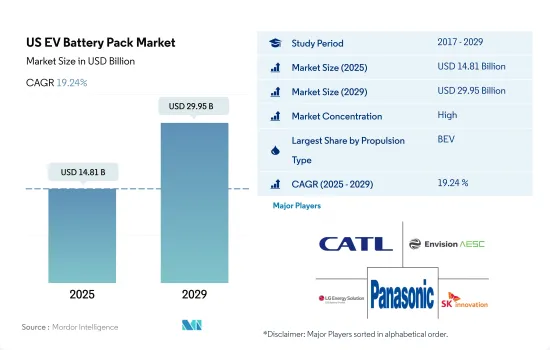

미국의 EV 배터리 팩 시장 규모는 2025년에 148억 1,000만 달러에 달할 것으로 추정됩니다. 2029년에는 299억 5,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2029년) CAGR은 19.24%를 나타낼 것으로 전망됩니다.

미국은 2030년까지 신차의 50%를 전기차로 만드는 것을 목표로 하고 있으며, 이는 EV 수요를 밀어 올립니다.

미국에서는 최근 EV의 생산과 판매의 급증에 힘입어 전기자동차(EV)용 배터리 팩의 채용이 일관되게 증가하고 있습니다. 특히 테슬라, 제너럴 모터스, 포드, 닛산 등 선도적인 자동차 제조업체는 EV의 성능과 효율을 높이기 위해 연구 개발에 많은 투자를 하고 있습니다. 동시에 미국의 배터리 기술도 크게 진보하고 있으며, 그 진보는 항속 거리의 향상과 충전의 고속화로 이어지고 있습니다. Panasonic, LG Chem, CATL과 같은 배터리 제조업체들은 이러한 수요가 급증하면서 미국에서 생산 능력을 확대하고 있습니다.

인프라의 중요한 역할을 인식하는 미국 정부는 EV 배터리 인프라 및 충전소 개발에 적극적인 인센티브와 자금을 제공하여 보급을 더욱 강화하고 있습니다. 정부는 EV 배터리 팩 시장을 활성화하기 위해 다양한 우대 조치를 취하고 있습니다. 예를 들어, EV 구매자는 최대 7,500달러의 연방세 혜택을 받을 수 있으며, 일부 주에서는 리베이트, 감세, 심지어 충전소 무료 제공 등의 혜택을 제공합니다. 미국에서는 현재 주로 중국과 한국에서 배터리 팩의 대부분이 수입되고 있지만 국내 생산으로의 전환이 현저해지고 있습니다. 네바다에 있는 테슬라의 광대한 배터리 공장과 미시간에 있는 LG Chem의 시설은 이 동향을 상징합니다.

앞으로 바이든 정권은 2030년까지 미국에서 판매되는 신차의 50%를 전기차로 삼는다는 야심적인 목표를 내걸고 있어 EV 수요의 급증이 예상됩니다. 이 나라의 EV의 미래는 밝고 시장은 2024년부터 2029년까지 강력한 성장을 이룰 것으로 예측됩니다.

미국의 EV 배터리 팩 시장 동향

테슬라, 도요타, 포드, 현대, 혼다가 미국 전기자동차 배터리 팩 시장을 독점

전기자동차 시장은 고도로 통합되어 2023년에는 테슬라, 도요타그룹, 포드그룹, 현대자동차, 혼다 등 5곳이 시장의 75% 가까이를 차지했습니다. 테슬라는 미국 최대의 전기자동차 판매 회사로 시장의 약 30%를 차지하고 있습니다. 이 회사는 혁신적인 기술에 주력하고 있으며 다양한 EV 부품(배터리 등) 제조업체와 강력한 전략적 파트너십을 맺고 있습니다. 미국에 기반을 둔 기업이기 때문에 미국 전역에서 우수한 제품과 서비스를 제공하는 강력한 고객 기반을 보유하고 있습니다.

도요타 그룹은 전기차 판매 대수로 2위이며 미국 전체에서 약 28%를 차지하고 있습니다. 이 회사는 강력한 공급 및 유통망을 가지고 있으며 다양한 전기자동차를 폭넓게 제공함으로써 고객들 사이에서 신뢰할 수 있는 브랜드로 운영되고 있습니다. 포드그룹은 미국 전체 EV 판매에서 3위를 차지하며 시장 점유율은 약 10%입니다. 국산 브랜드이기 때문에 미국에서의 폭넓은 제품 및 서비스망을 가져, 고객으로부터의 강한 신뢰를 얻고 있습니다.

현대는 4위로 미국 전체 EV 판매 점유율의 약 5.4%를 차지하고 있습니다. 이 회사는 강력한 생산과 공급망의 네트워크를 가지고 있으며, 다양한 브랜드보다 합리적인 가격으로 다양한 혁신적인 제품을 제공합니다. 혼다는 EV 시장에서 5위를 차지하며 약 5% 시장 점유율을 유지하고 있습니다. 미국에서 EV를 판매하는 다른 기업에는 기아, 지프, BMW, 볼보가 포함됩니다.

테슬라는 압도적인 점유율을 유지하고 미국에서 배터리 팩의 주요 수요에 기여하고 있습니다.

미국은 북미에서 가장 인기 있는 국가 중 하나이며 2017-2023년 사이에 EV 수요가 꾸준히 증가했습니다. 소비자의 선호도가 세단 등 다른 EV와 동등한 가격대에서 보다 스포티하고 모험적인 달리기 및 기타 이점으로 점진적으로 전환하고 있기 때문에 전동 SUV 시장은 꾸준히 확대되고 있습니다. SUV는 발과 헤드룸이 넓고, 쾌적한 승차감이 우선사항의 하나이기 때문에 고객을 끌어안고 있습니다.

미국의 EV 배터리 팩 시장에서는 테슬라 모델 Y의 판매가 크게 성장하고 있습니다. 이 차량은 항속거리가 길고, 좌석수가 많고, 대용량의 짐이 쌓이는 전기자동차를 요구하는 고객을 끌어들이고 있습니다. 전기 세단을 제공하는 기업도 미국 인구에서 좋은 반응을 얻고 있습니다. 테슬라 모델 3도 2023년 미국의 EV 배터리 팩 시장에서 베스트셀러로 들어갔으며, 완전 전기 기술, 고성능, 급속 충전 기술 및 양호한 항속 거리를 제공했습니다.

미국의 EV 배터리 팩 시장에서는 국제 브랜드도 전기 SUV와 세단을 제공합니다. 도요타 RAV4 플러그인 하이브리드는 인기 자동차 중 하나로 2023년에는 호조로 팔리는 것을 보여주었습니다. 좋은 서비스 네트워크, 다른 브랜드보다 저렴한 가격, 신뢰할 수있는 브랜드 이미지가 도요타 자동차의 판매 대수가 늘고있는 이유입니다. 미국의 EV 배터리 팩 시장에서 도요타가 판매하는 또 하나의 판매 트럭은 하이브리드 파워트레인을 탑재한 시에나입니다. 7인승차를 요구하는 대가족 소비자는 도요타 시에나에게 호의적인 반응을 보이고 있습니다. 미국의 EV 배터리 팩 시장에서 다른 경쟁 차종은 도요타 Highlander, 지프 Wrangler, 도요타 Camry, 혼다 Accord, 포드 Mustang Mach-E 등입니다.

미국의 EV 배터리 팩 산업 개요

미국의 EV 배터리 팩 시장은 상당히 통합되어 상위 5개사에서 93.29%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Contemporary Amperex Technology(CATL), Envision AESC Japan, LG Energy Solution Ltd., Panasonic Holdings Corporation and SK Innovation Co. Ltd.(알파벳순 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

전기자동차 판매 대수

OEM별 전기자동차 판매 대수

베스트셀러 EV 모델

선호되는 배터리 화학을 가진 OEM

배터리 팩 가격

배터리 재료 비용

각 배터리 화학의 가격표

누가 누구에게 공급하는지

EV 배터리의 용량과 효율

EV의 출시 모델 수

규제 프레임워크

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

바디 유형

버스

LCV

M&HDT

승용차

추진 유형

BEV

PHEV

배터리 화학

LFP

NCA

NCM

NMC

기타

용량

15 kWh-40 kWh

40 kWh-80 kWh

80kWh 이상

15kWh 미만

배터리 형상

원통형

파우치

프리즘형

방식

레이저

와이어

구성 요소

양극

음극

전해질

분리기

재료 유형

코발트

리튬

망간

천연 흑연

니켈

기타 재료

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

Ambri Inc.

Contemporary Amperex Technology Co. Ltd.(CATL)

Envision AESC Japan Co. Ltd.

Imperium3 New York(IM3NY)

LG Energy Solution Ltd.

Panasonic Holdings Corporation

Samsung SDI Co. Ltd.

Sila Nanotechnologies Inc.

SK Innovation Co. Ltd.

Tesla Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The US EV Battery Pack Market size is estimated at 14.81 billion USD in 2025, and is expected to reach 29.95 billion USD by 2029, growing at a CAGR of 19.24% during the forecast period (2025-2029).

The United States aims for 50% of new cars to be electric by 2030, boosting EV demand

The United States has witnessed a consistent rise in the adoption of electric vehicle (EV) battery packs in recent years, propelled by the surge in EV production and sales. Notably, major automakers like Tesla, General Motors, Ford, and Nissan are heavily investing in R&D to enhance the performance and efficiency of their EVs. Concurrently, battery technology in the United States has made significant strides, with advancements translating into improved range and faster charging. Battery manufacturers, including Panasonic, LG Chem, and CATL, are scaling up their production capacities in the country to meet this surging demand.

Recognizing the pivotal role of infrastructure, the US government has been proactive in incentivizing and funding the development of EV battery infrastructure and charging stations, further bolstering the adoption. The government is offering a range of incentives to boost the market for EV battery packs. For instance, federal tax incentives of up to USD 7,500 are extended to EV buyers, while several states sweeten the deal with rebates, tax breaks, and even complimentary charging stations. Although the majority of battery packs in the US are currently imported, primarily from China and South Korea, there is a noticeable shift toward domestic manufacturing. Tesla's sprawling battery plant in Nevada and LG Chem's facility in Michigan exemplify this trend.

Looking ahead, the Biden administration has set an ambitious target of 50% of new cars sold in the US being electric by 2030, further underlining the anticipated surge in EV demand. The future of EVs in the country appears bright, with the market projected to witness robust growth from 2024 to 2029.

US EV Battery Pack Market Trends

Tesla, Toyota, Ford, Hyundai, and Honda dominate the US electric vehicle battery pack market

The electric vehicle market is highly consolidated, with five major players, Tesla, Toyota Group, Ford Group, Hyundai, and Honda, accounting for almost 75% of the market in 2023. Tesla is the largest seller of electric vehicles in the United States, accounting for around 30% of the market. The company focuses on innovative technologies and has strong strategic partnerships with manufacturers of various EV components (such as batteries). Being a US-based company, it has a strong customer base with great product and service offerings across the United States.

Toyota Group is the second largest seller of electric vehicles, accounting for around 28% across the United States. The company has a strong supply and distribution network and operates as a reliable brand among customers with wide product offerings of various electric cars. The Ford Group holds 3rd place in EV sales across the United States, with around 10% of the market share. Being a domestic brand, the company has strong goodwill among customers with a wide product and service network in the United States.

Hyundai is the fourth-largest player, accounting for around 5.4% of the market share in EV sales across the United States. The company has a strong production and supply chain network, with wide innovative products offered at reasonable prices over other brands. Honda is the fifth-largest player in the EV market, maintaining its market share at around 5%. Other players selling EVs in the United States include Kia, Jeep, BMW, and Volvo.

Tesla maintains dominance, holding the majority share, and contributes to the major demand for battery packs in the United States

The United States is one of the most popular countries in North America, where the demand for EVs steadily increased during 2017-2023. The market for electric SUVs is steadily increasing as consumer preferences gradually move to a more sporty and adventurous drive and other benefits at a comparable price point as other EVs like sedans. SUVs offer more leg and headroom, which attracts customers as a comfortable ride is one of the main priorities.

In the US EV battery pack market, sales of the Tesla Model Y have grown significantly. The car attracts customers seeking an electric car with long-range, good seating capacity, and large cargo capacity. Companies offering electric sedans are also getting good responses from the US population. Tesla Model 3 was also among the best sellers in the US EV battery pack market in 2023, owing to its full electric technology, high-performance capabilities, fast charging technology, and good range offerings.

International brands also offer electric SUVs and sedans in the US EV battery pack market. Toyota RAV4 plug-in hybrid is one of the popular cars and witnessed good sales in 2023. A good service network, lower prices than other brands, and a reliable brand image are reasons for the growing sales of Toyota cars. Another good-selling car by Toyota in the US EV battery pack market is the Sienna, offered with a hybrid powertrain; consumers with big families looking for 7-seater cars have positively responded to the Toyota Sienna. Other vehicles competing in the US EV battery pack market include the Toyota Highlander, Jeep Wrangler, Toyota Camry, Honda Accord, and Ford Mustang Mach-E.

US EV Battery Pack Industry Overview

The US EV Battery Pack Market is fairly consolidated, with the top five companies occupying 93.29%. The major players in this market are Contemporary Amperex Technology Co. Ltd. (CATL), Envision AESC Japan Co. Ltd., LG Energy Solution Ltd., Panasonic Holdings Corporation and SK Innovation Co. Ltd. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Electric Vehicle Sales

4.2 Electric Vehicle Sales By OEMs

4.3 Best-selling EV Models

4.4 OEMs With Preferable Battery Chemistry

4.5 Battery Pack Price

4.6 Battery Material Cost

4.7 Price Chart Of Different Battery Chemistry

4.8 Who Supply Whom

4.9 EV Battery Capacity And Efficiency

4.10 Number Of EV Models Launched

4.11 Regulatory Framework

4.11.1 US

4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)