위험구역용 장비 : 시장 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)

Hazardous Area Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683856

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

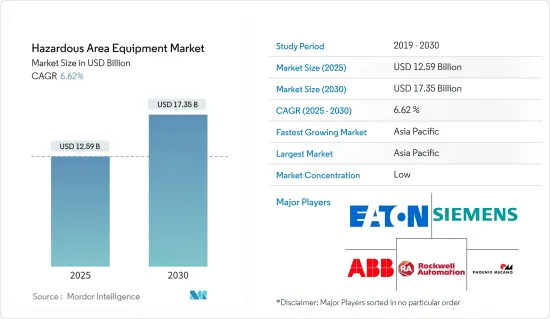

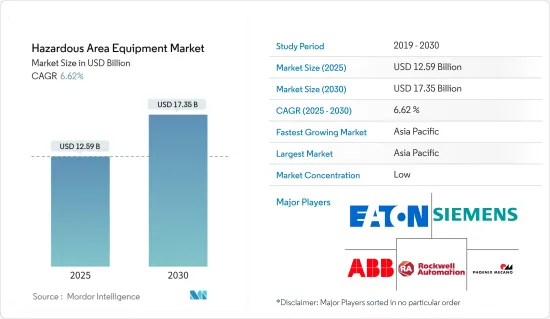

위험구역용 장비 시장 규모는 2025년에 125억 9,000만 달러에 이를 것으로 추정됩니다. 예측기간(2025-2030년)의 CAGR은 6.62%를 나타내고, 2030년에는 173억 5,000만 달러에 달할 것으로 추정되고 있습니다.

위험구역용 장비는 가연성 공기 가연성 가스 또는 미립자 조합이 존재하기 때문에 폭발성이 높은 환경에서 사용하도록 특별히 설계되었습니다. 이러한 장비의 안전한 설계, 기능 및 관리를 위한 기준을 설명하는 여러 시스템이 있습니다. 위험과 보호 조치를 설명하는 데 사용되는 용어도 다양합니다. 이러한 분위기가 존재하는 것은 많은 산업, 상업, 과학적 환경에서 일반적이거나 적어도 그 가능성이 있음을 주목하는 것이 중요합니다. 방화·방폭의 확보는 종업원의 안전과 조업의 신뢰성에 있어 매우 중요합니다.

주요 하이라이트

위험구역용 장비 수요는 다양한 정부에 의한 안전 규제의 실시와 위험 환경에서의 사고와 폭발을 방지할 필요성에 의해 견인되고 있습니다. 또한 장비 설계의 기술적 진보와 에너지 효율의 중요성이 커짐에 따라 시장 성장을 뒷받침하고 있습니다.

위험구역용 장비 산업은 성장하고 있지만, 추가 개발을 방해하는 요인도 몇 가지 있습니다. 장비와 관련된 많은 비용과 장비 운영에 자격을 갖춘 전문가가 필요하다는 것은 시장 확대에 영향을 미치는 주요 장애물입니다.

위험구역용 장비의 통일 규격이나 인증이 없는 것, 원격지에서는 이러한 제품에 대한 액세스가 제한되어 있는 것도, 시장의 성장에 큰 과제를 가져오고 있습니다.

또한 공정산업 및 냉각산업 등의 분야에서 안전대책이 중시되게 되었기 때문에 산업용 컨트롤러, 케이블 그랜드, 모터, 센서, 스트로보 비콘, 조명, 기타 관련 품목 등의 방염·방폭 위험 구역 기기에 대한 수요가 높아지고 있습니다. 또한 다양한 산업, 특히 공정 및 냉각 분야에서의 안전 대책 강화에 대한 주목의 고조가 위험구역용 장비 수요 증가로 이어지고 있으며, 예측 기간 중에 대폭적인 성장이 예상되고 있습니다.

위험구역에서 사용되는 장비는 잠재적인 위험을 방지하기 위해 단단히 밀폐되어 있습니다. 이 장비는 일반적으로 다이 캐스팅 스틸과 때로는 플라스틱과 같은 견고한 소재로 만들어집니다. 밀폐는 열과 불꽃을 발생시키는 장비의 결함으로 인한 폭발을 효과적으로 방지합니다.

또한 위험구역에서 사용되는 장비의 안전을 보장하는 방법은 국가마다 다릅니다. 이러한 장비는 장점이 있는 반면, 도입에는 상당한 비용이 들고 무게도 상당히 무거워집니다. 그 결과 위험구역용 장비를 도입하는 데 드는 초기 비용이 높아 시장 성장을 방해하고 있습니다.

위험구역용 장비 시장 동향

석유 및 가스 최종사용자 산업분야가 큰 시장 점유율을 차지할 전망

석유 및 가스 산업에서 방폭에는 두 가지 요구 사항이 있습니다. 즉, 기기가 적절한 규격으로 제조되어 추가 규격에 따라 설치·보수될 필요가 있습니다. 또한 석유 및 가스 직원은 위험한 환경에서 작업해야 합니다. 가연성 액체, 가스, 증기 또는 가연성 분진이 상당한 양 존재하는 경우 안전성이 중요합니다. 이러한 요구사항은 향후 몇 년 동안 위험구역용 장비 수요를 증가시킬 것입니다.

이 시장에서는 고객의 일상적인 건설, 운영, 최적화, 자산 강화를 지원하고 보다 위험한 상황에서 대체 전기 솔루션을 제공하기 위한 다양한 혁신을 볼 수 있습니다. 게다가 석유 매장량의 발견과 탐사 과정에 대한 향후 투자는 위험구역용 장비 수요를 촉진할 것으로 예상됩니다. 예를 들어 국제에너지기구(IEA)에 따르면 2040년까지 세계 석유 수요는 21% 증가하고, 전체 에너지의 35%를 석유가 차지하며 천연가스 수요는 31% 증가할 것으로 전망됩니다. 전체 에너지의 17%를 천연가스가 차지할 것으로 예측됩니다.

게다가 자동차, 에너지, 기계제조, 전력, 화학, 야금의 각 분야에 있어서, 난방유나 디젤 연료를 포함한 원유·완성유 수요 증가가 석유 및 가스 탐사 프로세스의 필요성을 한층 더 높여, 위험 구역용 장치 수요를 간접적으로 밀어 올리고 있습니다. 2022년 세계의 원유(바이오연료 포함) 수요는 일량 약 9,957만 배럴에 이르렀고, 2023년에는 1억189만 배럴로 증가했습니다.

위험한 장소는 주로 석유 및 가스 산업에서 볼 수 있으며, 가연성 가스의 존재가 한정적인 지역이 높습니다. GECF에 따르면 2022년 12월 중국의 천연가스 소비량은 335억 입방미터(bcm)에 달했습니다. 또한 IEA에 따르면 2040년까지 세계 천연가스 수요의 2,800억 입방미터를 차지할 것으로 예상됩니다. 또한 2040년까지 일량 1,300만 배럴을 순수입하고, 2030년까지 미국을 제치고 궁극의 석유 소비국이 될 가능성도 있습니다. 이러한 석유 및 가스 산업의 확대는 시장 성장을 더욱 촉진할 수 있습니다.

정부의 석유성은 이전, 향후 수년간 인도에 있어서의 석유 및 가스 탐사와 천연 가스·인프라의 정비에 약 1,180억 달러를 투입한다고 발표했습니다. 2023년까지 580억 달러가 석유 및 가스 탐사와 전시에 충당되었고, 2024년까지 600억 달러가 파이프라인, 수입 터미널, 도시가스 공급망 등 천연가스 인프라 개발에 투입되었습니다. 이와 같이, 이 시장은 현저한 성장을 이룰 것으로 예상됩니다.

아시아태평양이 큰 시장 점유율을 차지할 것으로 예상

중국은 제조 장비 및 공작기계의 세계 주요 생산 국가 및 수출국 중 하나입니다. 지난 10년간의 제조 활동이 급증함에 따라 장비 및 공구 생산이 증가하고 있습니다. 따라서 이 성장은 방폭기기의 채용률에 영향을 미치고 있습니다. Semiconductor Equipment and Materials International에 따르면 2022년 중국의 반도체 장치 매출은 거의 1조 3,800억 위안(1,900억 달러)에 달했습니다.

제조 절차에서 자동화의 도입이 진행됨에 따라 방폭 솔루션 수요가 높아질 것으로 예상됩니다. 많은 산업공장과 제조공장에서는 담당자가 정기적으로 정해진 루트를 순회하여 현장검사를 실시하고, 특정 지점에서 현장장치를 점검하여 시설 및 장치의 안전성과 양호한 작동상태를 유지하고 있습니다.

인도에서는 산업화의 진전과 광산업 시장개척에 의해 조사된 시장성장에 대한 투자가 빈번히 이루어지고 있습니다. 또한 인도의 광업 부문은 부모산업인 신정부를 위해 확대되고 있습니다. MOSPI에 따르면 2022년 말 인도 전역의 광업 생산량은 약 12% 증가했습니다.

또한 IBEF에 따르면 정부는 2022년부터 2025년까지 광업 부문에서 28,727캐롤 루피(36억 8,000만 달러) 상당의 자산을 수익화할 계획입니다. 또한 JSW 그룹은 2023년 2월 안도라 프라데시 주 YSR 카다파 지역에 8,800캐롤 루피(10억 달러)를 투자하여 제철소를 건설할 것이라고 발표했습니다. 이러한 금속·광산 플랜트의 개발은 연구 시장 수요를 더욱 창출할 가능성이 있습니다.

일본은 자동차 및 전자 기기의 주요 제조업체 중 하나이며, 이러한 제품에 대한 수요는 세계적으로 급증하고 있습니다. 이로 인해 세계 수요를 충족하고 새롭고 혁신적인 제품을 제공하기 위해 제조 설비 건설 및 업그레이드가 증가하고 있습니다. 이를 촉진하기 위해서는 활동을 실시하기 위한 기계가 필요하며, 제조 분야에서의 방폭 기기의 성장을 높이고 있습니다.

위험구역용 장비 시장 개요

위험구역용 장비 시장은 매우 경쟁이 치열하여 여러 전통 기업들이 시장 점유율을 겨루고 있습니다. 이 업계의 유명한 기업으로는 ABB Ltd, Eaton Corporation, Honeywell International Inc., Siemens AG, Rockwell Automation Inc. 등이 있습니다.

이러한 기업들은 강력한 국제적 영향력을 갖고 있으며, 방폭 조명, 통신 툴, 제어 시스템, 센서 등 다양한 위험구역용 장비를 제공합니다. 시장 내 지위를 유지하기 위해 이러한 기업들은 혁신, 제품 진보, 전략적 파트너십을 선호합니다.

이러한 노포 기업 외에도 위험 구역 기기 업계에는 신규 참가 기업과 신흥 기업도 몇 가지 나타납니다. 이러한 기업들은 안전성과 효율성을 향상시키는 혁신적이고 고급 제품으로 시장에 혁명을 일으키려는 야심을 가지고 있습니다. 하지만 이미 확고한 브랜드 평가와 충실한 고객 기반을 구축하고 있는 전통 기업과의 치열한 경쟁에 노출되어 있습니다.

2023년 5월-ABB는 차세대 전동화 솔루션 개발을 가속화하기 위해 테네시주 멤피스에 300만 달러를 투자하여 로버트 M. 토마스 혁신 센터를 개설한다고 발표했습니다.

2023년 8월 - Eaton Corporation PLC가 Automation Expo 2023에서 위험구역을 위한 새로운 산업 솔루션을 전시한다고 발표했습니다. Ethernet over Coax(EoC) CCTV 솔루션, Zone 2, 21 및 22 위험구역에서 사용되는 nHLL 선형 LED 기구, 석유 및 가스, 화학 처리 및 폐수 처리와 같은 산업용 스마트 범용 마샬링(MTL SUM5)을 소개합니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

경쟁 기업간 경쟁 관계

대체품의 위협

업계 밸류체인 분석

매크로 동향의 업계에 대한 영향 평가

제5장 시장 역학

시장 성장 촉진요인

위험구역과 물질의 취급에 관한 규제 강화

에너지 수요 증가, 신규 광산 탐사 수요 촉진

시장의 과제/억제요인

장비에 대한 높은 투자 및 높은 설치 비용

제6장 시장 세분화

장비별

전원 공급 시스템

전기 모터

감시 시스템

케이블 글랜드 및 커넥터

자동화 및 제어 제품

인클로저

조명 제품

푸시 버튼 및 시그널링 장치

최종 사용자 산업별

석유 및 가스

에너지 및 발전

화학

식음료

제약

기타 최종 사용자 산업

지역별

북미

미국

캐나다

유럽

영국

독일

제품 카테고리별, 최종 사용자 산업별 점유율

위험 장비 제조업체 일람

프랑스

스페인

이탈리아

베네룩스

아시아

중국

인도

일본

한국

호주 및 뉴질랜드

라틴아메리카

멕시코

브라질

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

제7장 지역 등급 - 시장 시나리오

존 0/20, 클래스 I/II/III 디비전 1

존 1/21, 클래스 I/II/III 디비전 2

존 2/22, 클래스 I/II/III 디비전 2

제8장 경쟁 구도

기업 프로파일

ABB Ltd

Eaton Corporation PLC

Siemens AG

Rockwell Automation Inc.

Phoenix Mecano

R. Stahl AG

CZ Electric Co. Ltd

Pepperl Fuchs GmbH

Cordex Instruments Ltd

Marechal Electric Group

Adalet Inc.(Scott Fetzer Company)

Bartec GmbH

Alloy Industry Co. Ltd

GM International Srl

Spina Group SRL

Supermec Pte. Ltd

Wago GmbH & Co. KG

Warom Technology Inc. Co.

Honeywell HBT

Hangzhou Hikvision Digital Technology Co. Ltd

제9장 시장 전망

KTH

영문 목차

영문목차

The Hazardous Area Equipment Market size is estimated at USD 12.59 billion in 2025, and is expected to reach USD 17.35 billion by 2030, at a CAGR of 6.62% during the forecast period (2025-2030).

Equipment for hazardous areas is specifically designed for use in environments that are highly explosive due to the presence of combustible air-flammable gases or particulate combinations. There are multiple schemes that outline the standards for the safe design, functioning, and management of such equipment. The terminology used to describe hazards and protective measures can also vary. It is important to note that the presence of such an atmosphere is common or at least possible in numerous industrial, commercial, and scientific settings. Ensuring fire and explosion protection is crucial for the safety of employees and the reliability of operations.

Key Highlights

The demand for hazardous area equipment is being driven by the implementation of safety regulations by various governments and the need to prevent accidents and explosions in hazardous environments. The market growth is also being propelled by technological advancements in equipment design and the growing emphasis on energy efficiency.

Although the hazardous area equipment industry has experienced growth, there are several factors that impede its further development. The significant expenses associated with the equipment and the necessity for qualified professionals to operate them are the primary obstacles affecting market expansion.

The absence of uniform standards and certification for hazardous area equipment, along with the limited accessibility of these products in remote areas, pose substantial challenges to the market's growth.

There is also a growing demand for flame- and explosion-proof hazardous area equipment, such as industrial controllers, cable glands, motors, sensors, strobe beacons, lighting, and other related items, due to the heightened emphasis on safety measures in sectors like process and cooling industries. Also, the increasing focus on enhancing safety measures in various industries, specifically in process and cooling sectors, is leading to a rise in demand for hazardous area equipment and is expected to experience substantial growth in the forecast period.

The equipment used in the hazardous area is securely enclosed to prevent any potential hazards. These equipment are typically made of sturdy materials such as die-cast steel and sometimes plastic. The enclosure effectively prevents explosions in case of faulty equipment generating heat or sparks.

Additionally, different countries have their own methods of ensuring the safety of equipment used in hazardous areas. While these equipment offers benefits, their deployment can be quite costly, and they can become quite heavy. As a result, the high initial cost of implementing hazardous area equipment is hindering market growth.

Hazardous Area Equipment Market Trends

Oil and Gas End-user Industry Segment is Expected to Hold Significant Market Share

In the oil and gas industry, explosion proofing has two requirements: equipment must be manufactured to the appropriate standards and installed and maintained in accordance with additional standards. Also, oil and gas employees are frequently required to work in dangerous environments. Safety is significant when flammable liquids, gases, vapors, or combustible dust are present in substantial amounts. Such requirements are creating increasing demand for hazardous area equipment in the coming years.

The market is witnessing various innovations to assist customers in the daily construction, operation, optimization, and enhancement of their assets and provide alternative electrical solutions in more hazardous situations. Moreover, the discovery of oil reserves and upcoming investments in the exploration processes is expected to drive the demand for hazardous area equipment. For instance, the International Energy Agency said that by 2040, the world's demand for oil will go up by 21%, making it the source of 35% of all energy, and the demand for natural gas will go up by 31%, making it the source of 17% of all energy.

Additionally, the increasing demand for crude oil and finished oils, including heating oil and diesel fuel in the automobile, energy, machinery manufacturing, electricity, chemicals, and metallurgy sectors has further boosted the need for more oil and gas exploration processes, indirectly driving the demand for hazardous area equipment. The demand for crude oil (including biofuels) in 2022 globally amounted to approximately 99.57 million barrels per day, and it is forecasted to increase to 101.89 million barrels per day in 2023.

Hazardous locations are primarily found in the oil and gas industry, as areas with limited presence of combustible gas are high. According to GECF, in December 2022, natural gas consumption in China amounted to 33.5 billion cubic meters (bcm). In addition, according to the IEA, the country is expected to account for 280 billion cubic meters of global natural gas demand by 2040. It also has the potential to overtake the United States as the ultimate oil consumer by 2030, with 13 million barrels per day net imports by 2040. Such expansion in the oil and gas industries may further propel the market's growth.

The government's Oil Ministry's earlier announcement related to the spending of around USD 118 billion in the oil and gas exploration and setting up of natural gas infrastructure in India over the next few years, which USD 58 billion would be funded in oil and gas exploration and exhibition, by 2023 while USD 60 billion will be put in the development of natural gas infrastructure, such as pipelines, import terminals, and city gas distribution networks by 2024. Thus, the market is anticipated to witness significant growth.

Asia-Pacific is Expected to Hold Significant Market Share

China is one of the significant producers and exporters of manufacturing equipment and machine tools worldwide. The surge in manufacturing activities over the last decade has increased the production of equipment and tools. Therefore, this growth is impacting the rate of adoption of explosion-proof equipment. According to Semiconductor Equipment and Materials International, in 2022, the sales revenue from semiconductor equipment in China reached almost CNY 1.38 trillion (USD 0.19 trillion).

The increasing adoption of automation in manufacturing procedures is expected to propel the demand for explosion-proof solutions. At many industrial and manufacturing plants, personnel periodically perform field inspections by patrolling along defined routes and checking field devices at specific points to keep facilities and equipment safe and in good working order.

India is frequently investing in the studied market growth due to the increase of industrialization and the development of Mining industries in the country. Additionally, India's mining sector has expanded due to a new government that is pro-industry. According to MOSPI, at the end of fiscal year 2022, production of the mining industry across India increased by about 12%.

Further, according to IBEF, the government plans to monetize assets worth INR 28,727 crore (USD 3.68 billion) in the mining sector over 2022-25. Additionally, in February 2023, JSW Group announced the construction of a steel plant in Andhra Pradesh's YSR Kadapa district with an investment of INR 8,800 crore (USD 1 billion). Such developments in the metals and mines plants may further create demand in the studied market.

Japan is one of the significant manufacturers of automobiles and electronic equipment, and the demand for these products is increasing rapidly worldwide. This factor has led to the rise in construction and upgrading manufacturing facilities to meet global demand and provide new and innovative products. To facilitate this, machinery is required to carry out the activities, thus increasing the growth of explosion-proof equipment in the manufacturing sector.

Hazardous Area Equipment Market Overview

The hazardous area equipment market is quite competitive, with several well-established players competing for market share. Among the prominent companies in this industry are ABB Ltd, Eaton Corporation, Honeywell International Inc., Siemens AG, and Rockwell Automation Inc.

These companies possess a robust international influence and provide a diverse array of hazardous area equipment, including explosion-proof lighting, communication tools, control systems, and sensors. To uphold their standing within the market, these companies prioritize innovation, product advancement, and strategic partnerships.

In addition to these established players, there are several new entrants and startups emerging in the hazardous area equipment industry. These companies have the ambition to revolutionize the market with their innovative and advanced products, which bring enhanced safety and efficiency. Nevertheless, they encounter strong competition from well-established players who have already built a solid brand reputation and loyal customer base.

May 2023 - ABB Ltd announced the opening of its USD 3 million Robert M. Thomas Innovation Center in Memphis, Tennessee, to accelerate the development of next-generation electrification solutions.

August 2023 - Eaton Corporation PLC company announced to showcase its new industrial solutions for hazardous areas at Automation Expo 2023. It will introduce Ethernet over Coax (EoC) CCTV solution, nHLL linear LED fixture used in Zone 2 and 21 and 22 hazardous areas, and Smart Universal Marshalling (MTL SUM5) for industries such as oil & gas, chemical processing, and wastewater treatment.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitutes

4.3 Industry Value Chain Analysis

4.4 An Assessment of Macro Trends Impact on the Industry

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Stricter Regulations for Handling Hazardous Areas and Substances

5.1.2 Increasing Energy Requirements, Driving the Demand for Exploration of New Mines

5.2 Market Challenges/Restraints

5.2.1 High Investments and High Installation Cost of the Equipment

6 MARKET SEGMENTATION

6.1 By Equipment

6.1.1 Power Supply Systems

6.1.2 Electric Motors

6.1.3 Surveillance Systems

6.1.4 Cable Glands and Connectors

6.1.5 Automation and Control Products

6.1.6 Enclosures

6.1.7 Lighting Products

6.1.8 Push Buttons and Signaling Devices

6.2 By End-user Industry

6.2.1 Oil and Gas

6.2.2 Energy and Power Generation

6.2.3 Chemical

6.2.4 Food and Beverage

6.2.5 Pharmaceuticals

6.2.6 Other End-user Industries

6.3 By Geography

6.3.1 North America

6.3.1.1 United States

6.3.1.2 Canada

6.3.2 Europe

6.3.2.1 United Kingdom

6.3.2.2 Germany

6.3.2.2.1 Market Share by Product Category and End-user Industry

6.3.2.2.2 List of Manufacturers of Hazardous Equipment

6.3.2.3 France

6.3.2.4 Spain

6.3.2.5 Italy

6.3.2.6 Benelux

6.3.3 Asia

6.3.3.1 China

6.3.3.2 India

6.3.3.3 Japan

6.3.3.4 South Korea

6.3.3.5 Australia and New Zealand

6.3.4 Latin America

6.3.4.1 Mexico

6.3.4.2 Brazil

6.3.5 Middle East and Africa

6.3.5.1 United Arab Emirates

6.3.5.2 Saudi Arabia

6.3.5.3 South Africa

7 AREA RATING - MARKET SCENARIO

7.1 Zone 0 / 20, Class I / II / III Division 1

7.2 Zone 1 / 21, Class I / II / III Division 2

7.3 Zone 2 / 22, Class I / II / III Division 2

8 COMPETITIVE LANDSCAPE

8.1 Company Profiles

8.1.1 ABB Ltd

8.1.2 Eaton Corporation PLC

8.1.3 Siemens AG

8.1.4 Rockwell Automation Inc.

8.1.5 Phoenix Mecano

8.1.6 R. Stahl AG

8.1.7 CZ Electric Co. Ltd

8.1.8 Pepperl+Fuchs GmbH

8.1.9 Cordex Instruments Ltd

8.1.10 Marechal Electric Group

8.1.11 Adalet Inc. (Scott Fetzer Company)

8.1.12 Bartec GmbH

8.1.13 Alloy Industry Co. Ltd

8.1.14 G.M. International Srl

8.1.15 Spina Group SRL

8.1.16 Supermec Pte. Ltd

8.1.17 Wago GmbH & Co. KG

8.1.18 Warom Technology Inc. Co.

8.1.19 Honeywell HBT

8.1.20 Hangzhou Hikvision Digital Technology Co. Ltd