ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

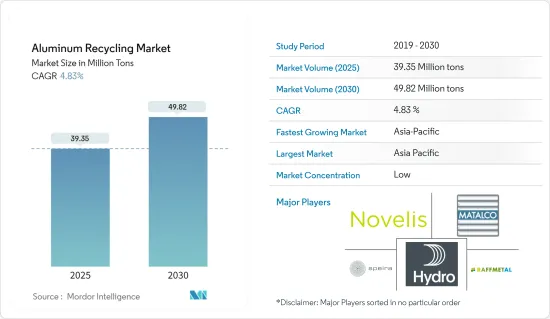

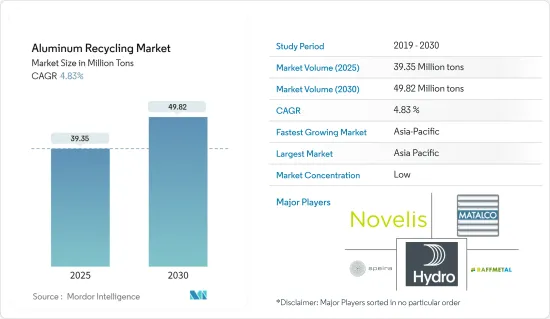

알루미늄 재활용 시장 규모는 2025년에는 3,935만 톤으로 추정되며, 2030년에는 4,982만 톤에 달할 것으로 예측되고, 예측기간(2025-2030년)의 CAGR은 4.83%를 나타낼 전망입니다.

COVID-19의 유행은 알루미늄 재활용 시장에 상당한 영향을 미쳤습니다. 특히 주택 등록이 중단되고 주택 대출 지급이 둔화되는 등 주거용 부동산이 위축되면서 알루미늄의 주요 수요처인 건축 및 건설업이 큰 타격을 입었습니다. 그러나 제한이 해제된 이후 이 부문은 회복세를 보이고 있습니다. 2021-2022년 알루미늄 시장은 다양한 최종 사용자 산업의 소비 증가로 인해 크게 회복되었습니다.

주요 하이라이트

단기적으로는 자동차 및 건설 산업에서 재활용 알루미늄의 활용도가 증가하면서 시장 수요를 견인할 것으로 예상됩니다.

반대로 철과 같은 바람직하지 않은 불순물의 존재는 시장의 성장을 방해 할 가능성이 높습니다.

전기 자동차 부문의 성장과 탄소 발자국 감소에 대한 관심이 높아지면서 시장에 새로운 성장 기회를 제공할 것으로 보입니다.

아시아태평양은 시장을 지배 할 것으로 예상되며 예측 기간 동안 가장 높은 CAGR을 목격 할 가능성이 높습니다.

알루미늄 주기 시장 동향

건축 및 건설 산업의 수요 증가

알루미늄은 건축 및 건설 산업에서 두 번째로 널리 사용되는 금속입니다. 건물에 사용되는 알루미늄의 약 60%는 재활용 재료로 구성되어 있습니다.

재활용 알루미늄 주조 합금, 압출 시트 및 기타 제품은 천정, 창문, 문, 계단, 벽 패널, 지붕 시트 및 기타 다양한 용도로 사용되었습니다.

재활용 알루미늄을 사용하면 에너지 절약에도 상당한 이점이 있습니다. 사용한 알루미늄을 재용융하는 데는 1차 금속 생산에 필요한 에너지의 5%만 필요합니다. 따라서 알루미늄을 재용융 및 개질하여 새로운 세대의 건축 부품을 생산함으로써 사회의 폐기물 문제에 기여하는 대신 새로운 세대의 건축 부품을 생산할 수 있습니다.

2차 알루미늄 및 재활용 알루미늄 제품은 건물 외관, 커튼월, 지붕 및 클래딩, 태양열 차양, 태양광 패널, 난간, 계단, 선반 및 기타 가설 구조물에 광범위하게 사용됩니다. 또한 고층 건물, 고층 빌딩 및 교량 건설에도 사용됩니다.

옥스포드 이코노믹스의 보고서에 따르면 2030년까지 전 세계 건설 생산량은 아시아태평양 지역에서 약 40%로 가장 많이 증가할 것으로 예상되며, 북미 지역이 약 16%로 그 뒤를 이을 것으로 전망됩니다

세계 건설 활동이 증가하는 것이 최근 연구된 시장을 이끄는 주요 요인 중 하나입니다. 특히 아시아태평양, 북미, 중동 지역은 건축 및 건설 산업에서 긍정적인 성장률을 보이고 있습니다. 따라서 재활용 알루미늄 시장에 대한 수요는 예측 기간 동안

아시아태평양에서는 중국이 건설 메가붐을 일으키고 있습니다. 전 세계적으로 중국은 전 세계 건설 투자의 약 20%를 차지하는 가장 중요한 건축 시장을 보유하고 있습니다. 중국에서만 2030년까지 약 13조 달러가 건물에 투자될 것으로 예상됩니다.

건설 산업은 인도에서 두 번째로 큰 규모입니다. 2022년에는 10.7%의 성장률을 기록했습니다. 예측 기간이 끝날 무렵 인도의 건설 산업은 약 1조 달러 규모로 전 세계에서 세 번째로 큰 시장으로 부상할 것으로 예상됩니다.

캐나다 건설 협회 데이터에 따르면, 건설 부문은 캐나다에서 가장 큰 고용주 중 하나이며 캐나다의 경제적 성공에 크게 기여하고 있습니다. 이 산업은 캐나다 GDP의 7%를 차지합니다.

캐나다 정부는 '캐나다 투자 계획'의 일환으로 2028년까지 캐나다의 주요 인프라 개발을 위해 약 1,400억 달러를 투자할 계획을 발표했습니다. 2019-2020년에는 캐나다의 새로운 인프라 프로젝트에 56억 달러 규모의 투자를 승인할 계획입니다.

사우디는 비전 2030과 국가혁신계획(NTP)을 발표하면서 교육, 의료 등 다양한 분야에 대한 투자를 늘려 경제 성장을 지원하고 있습니다. 사우디 정부는 사우디의 사회 인프라 개발을 위한 광범위한 계획을 가지고 있습니다. 국가의 다양한 부문에 대한 정부 및 민간 투자는 상업용 건물 건설 활동의 증가로 이어질 가능성이 높습니다.

따라서 위에서 언급한 요인으로 인해 재활용 알루미늄에 대한 수요는 예측 기간 동안 긍정적인 영향을받을 것입니다.

아시아태평양이 시장을 독점

아시아태평양은 예측 기간 동안 재활용 알루미늄의 가장 큰 성장 시장이 될 것으로 예상됩니다. 특히 중국, 인도, 일본 등의 국가에서 전자, 자동차, 건축 및 건설, 항공우주 및 방위산업 등의 산업이 성장하고 있습니다.

중국은 1970년대부터 국내에서 알루미늄을 재활용하고 있습니다. 또한 최근 몇 년 동안 2차 알루미늄에 대한 관심을 높이고 있습니다. 이와 관련하여 2030년까지 1차 알루미늄 제련 용량을 약 4,500만 톤으로 제한할 계획입니다.

국제무역관리국(ITA) 데이터에 따르면 중국은 연간 판매량과 생산량에서 여전히 세계 최대 자동차 시장입니다. 국내 생산량은 2025년까지 약 3,500만 대에 달할 것으로 예상됩니다. 중국 정부는 코로나19 팬데믹 이후 자동차 소비를 늘리고 있습니다. 중국은 전 세계에서 판매되는 모든 신형 전기자동차의 절반 이상(58%)을 차지합니다. 국제에너지기구(IEA)에 따르면 2022년에는 전국적으로 590만 대의 신형 전기자동차가 판매될 것이며, 이는 2021년 대비 80% 이상 증가한 수치입니다.

국제무역기구의 보고서에 따르면 중국은 전 세계에서 가장 큰 건설 시장이며 전 세계적으로 도시화율이 가장 높습니다. 미국 건축가 협회(AIA) 상하이의 데이터에 따르면 2025년까지 중국은 1990년대 이후 뉴욕에 10개에 해당하는 도시를 건설할 것이라고 합니다.

인도 브랜드 에퀴티 재단(IBEF)에 따르면, 민간 항공 산업은 최근 몇 년동안 인도에서 가장 빠르게 성장하는 산업 중 하나입니다. 2023년(2022년 4월-12월)의 항공 수송량은 2억 3,671만명으로, 전년 동기가 1억 3,161만명이었던 것으로부터 알 수 있듯이, 인도의 항공 산업은 신형 코로나 바이러스의 영향을 받을 것으로 예상되고 있습니다. 또한 2023년 6월 인도의 에어 인디아사는 에어버스사와 보잉사와 추정 700억 달러로 470대를 구매하는 계약을 체결했습니다.

일본의 가전 산업은 세계 최고의 산업 중 하나입니다. 일본은 컴퓨터, 게임기, 휴대폰 및 기타 주요 부품을 생산하는 세계적인 선도국입니다. 또한 가전 제품은 일본 경제 생산량의 약 3분의 1을 차지합니다. 일본의 전체 전자제품 생산량은 인도, 중국, 한국 등의 국가와의 치열한 경쟁으로 인해 감소하고 있습니다.

일본전자정보기술산업협회(JEITA)에 따르면 2023년 1월 일본 소비자용 전자기기의 생산액은 234억 2,500만 엔(1억 6,500만 달러)으로 전년 동기 대비 79.8%의 대폭 증가했습니다. 한편, 전자기기의 생산액은 2023년 1월에 2,903억 900만 엔(20억 4,200만 달러)이 되어, 전년 동기 대비 89.6% 증가했습니다.

따라서 위의 요인은 예측 기간 동안 연구된 시장 수요에 영향을 미칠 가능성이 높습니다.

알루미늄 재활용 산업 개요

알루미늄 재활용 시장은 세분화되어 있습니다. 주요 기업으로는 Novelis Inc., Speira GmbH, Norsk Hydro ASA, Matalco Inc., Raffmetal 등을 들 수 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건설 산업에서 재활용 알루미늄의 활용도 증가

자동차 산업에서 재활용 알루미늄에 대한 수요 증가

억제요인

철과 같은 바람직하지 않은 불순물의 존재

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

제품 유형

주조 합금

압출

시트

기타 제품 유형

최종 사용자 산업

자동차

항공우주 및 방위

건축 및 건설

전기 및 전자

포장

기타 최종 사용자 산업

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율 랭킹 분석

주요 기업의 전략

기업 프로파일

Alcoa Corporation

Amag Austria Metall AG

Constellium

Kuusakoski OY

Matalco Inc.

Norsk Hydro Asa

노벨리스

Raffmetal Spa

Real Alloy

Speira Gmbh

Stena Metall AB

Ye Chiu Group

제7장 시장 기회와 앞으로의 동향

전기자동차 부문의 성장

탄소 발자국 감소에 대한 관심 증가

HBR

영문 목차

영문목차

The Aluminum Recycling Market size is estimated at 39.35 million tons in 2025, and is expected to reach 49.82 million tons by 2030, at a CAGR of 4.83% during the forecast period (2025-2030).

The COVID-19 pandemic had a substantial impact on the aluminum recycling market. Building and construction, a major sink for aluminum, was badly hit, especially due to curtailment in residential real estate resulting in the suspension of home registrations and slow home loan disbursements. However, the sector has been recovering well since restrictions were lifted. The aluminum market recovered significantly in the 2021-22 period, owing to rising consumption from various end-user industries.

Key Highlights

Over the short term, the growing utilization of recycled aluminum in the automotive and construction industry is expected to drive demand for the market.

On the contrary, the presence of undesirable impurities like iron is likely to hamper the market's growth.

Growth in the electric vehicles segment and growing focus on the reduction of carbon footprint are likely to provide new growth opportunities for the market.

The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Aluminum Recycling Market Trends

Increasing Demand from the Building and Construction Industry

Aluminum is the second most widely used metal in the building and construction industry. Around 60% of the aluminum used in the buildings consists of recycled material.

Recycled aluminum casting alloys, extruded sheets, and other products were used in floating ceilings, windows, doors, stairs, wall panels, roof sheets, and a variety of other applications.

The use of recycled aluminum also offers substantial energy benefits. Remelting used aluminum requires only 5 percent of the energy needed to produce primary metal. Thus, rather than contributing to society's growing waste problem, aluminum can be remelted and reformed to produce a new generation of building parts.

Secondary aluminum/recycled aluminum products are extensively used in building facades, curtain walls, roofing and cladding, solar shading, solar panels, railings, staircases, shelves, and other temporary structures. They are also used in the construction of high-rise buildings, skyscrapers, and bridges.

According to the Oxford Economics report, global construction output is expected to grow the most in the Asia-Pacific region by around 40% by 2030, followed by the North American region by nearly 16%.

Increasing construction activity worldwide is one of the key factors driving the market studied in recent times. Asia-Pacific, North America, and the Middle East, among others, are witnessing a positive growth rate in the building and construction industry. Hence, the demand for the recycling aluminum market is likely to increase over the forecast period.

In Asia-Pacific, China is amid a construction mega-boom. Globally, China has the most significant building market, making up around 20% of all construction investments across the world. The country alone is likely to spend about USD 13 trillion on buildings by 2030.

The construction industry is the second-largest in India. It grew at 10.7% in 2022. By the end of the forecast period, India's construction industry may emerge as the third-largest market across the world, with a size of around USD 1 trillion.

As per the Canadian Construction Association data, the construction sector is one of largest employers in Canada and a significant contributor to the country's economic success. The industry contributes to 7% of the country's GDP.

As part of the 'Investing in Canada Plan,' the Canadian government has announced plans to invest around USD 140 billion for significant infrastructure developments in the country by 2028. In 2019-20, the government plans to approve investments valuing USD 5.6 billion for new infrastructure projects in the country.

The announcement of Vision 2030 and the National Transformation Plan (NTP) in Saudi Arabia have increased investments in different sectors, such as education and healthcare, to support the economic growth of the country. The government has expansive plans for the development of social infrastructure in the country. Government and private investments in various sectors of the country are likely to lead to a rise in commercial building construction activities.

Therefore, owing to the factors mentioned above, the demand for recycled aluminum will be positively impacted during the forecasted period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region is expected to be the largest growing market for recycled aluminum during the forecast period. Industries such as electronics, automotive, building and construction, aerospace and defense, etc., are growing in countries such as China, India, and Japan, among others.

China has been recycling aluminum domestically since the 1970s. Additionally, It has increased its focus on secondary Aluminum in recent years. In this regard, It is planning to cap the primary aluminum smelting capacity at around 45 million tons by 2030.

As per the International Trade Administration (ITA) data, China remains the largest auto market globally in annual sales and production. Domestic production is anticipated to reach nearly 35 million units by 2025. The Chinese government is boosting car consumption following the COVID-19 pandemic. China accounts for over half (58%) of all new electric vehicles sold worldwide. According to the International Energy Agency (IEA), 5.9 million new electric cars will be sold nationwide in 2022, an increase of more than 80% compared to 2021.

According to the report of the International Trade Organization, China is the largest construction market across the world and has the highest rate of urbanization globally. According to data from the American Institute of Architects (AIA) Shanghai, by 2025, China will have built a city equivalent to 10 in New York since the 1990s.

According to the Indian Brand Equity Foundation (IBEF), the civil aviation industry has become one of India's fastest-growing industries in recent years. The aviation industry in India is expected to be affected by the new coronavirus, as can be seen from the fact that the air traffic volume in 2023 (April to December 2022) was 236.71 million, compared to 131.61 million in the same period of the previous year. Furthermore, In June 2023, the Indian company Air India signed agreements with Airbus and Boeing to purchase 470 planes for an estimated cost of USD 70 billion.

The consumer electronics industry in Japan is one of the world's leading industries. The country is a world leader in producing computers, gaming stations, cell phones, and other vital components. Further, consumer electronics account for around one-third of the Japanese economic output. Japan's overall electronics production has declined due to stiff competition from countries such as India, China, and South Korea.

According to the Japanese Electronics and Information Technology Industries (JEITA), the production value of consumer electronic equipment in the country stood at JPY 23,425 million (USD 165 million) in January 2023, increasing by a significant 79.8% during the same period last year. Meanwhile, the production value of electronic devices stood at JPY 290,309 million (USD 2,042 million) in January 2023, increasing by 89.6% annually.

Thus, the factors above will likely affect the market demand studied during the forecast period.

Aluminum Recycling Industry Overview

The aluminum recycling market is fragmented in nature. Some major players include Novelis Inc., Speira GmbH, Norsk Hydro ASA, Matalco Inc., and Raffmetal, among others (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Utilization of Recycled Aluminum in the Construction Industry

4.1.2 Growing Demand for Recycled Aluminum from the Automotive Industry

4.2 Restraints

4.2.1 Presence of Undesirable Impurities Like Iron

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Casting Alloys

5.1.2 Extrusion

5.1.3 Sheets

5.1.4 Other Product Types

5.2 End-user Industry

5.2.1 Automotive

5.2.2 Aerospace and Defense

5.2.3 Building and Construction

5.2.4 Electrical and Electronics

5.2.5 Packaging

5.2.6 Other End-user Industries

5.3 Geography

5.3.1 Asia Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Nordic Countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Alcoa Corporation

6.4.2 Amag Austria Metall AG

6.4.3 Constellium

6.4.4 Kuusakoski OY

6.4.5 Matalco Inc.

6.4.6 Norsk Hydro Asa

6.4.7 Novelis

6.4.8 Raffmetal Spa

6.4.9 Real Alloy

6.4.10 Speira Gmbh

6.4.11 Stena Metall AB

6.4.12 Ye Chiu Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growth in the Electric Vehicles Segment

7.2 Growing Focus on Reduction of Carbon Footprint