ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

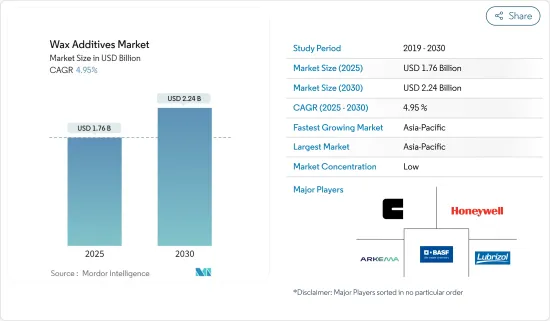

왁스 첨가제 시장 규모는 2025년에 17억 6,000만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 4.95%로, 2030년에는 22억 4,000만 달러에 달할 것으로 예측되고 있습니다.

COVID-19의 발생으로 건설 활동에 지장이 발생했습니다. 게다가 반도체 칩 부족과 기타 공급망의 혼란으로 인해 자동차 제조도 큰 영향을 받았습니다. 그러나 왁스 첨가제 시장은 팬데믹에서 회복하고 크게 성장하고 있습니다.

주요 하이라이트

가정 장식이나 보건소에서의 촛불의 소비 확대가 시장 수요를 증가 시킬 것으로 보입니다. 또한, 왁스 첨가제에 의해 코팅제와 잉크에 부여되는 특성도 시장 성장을 뒷받침할 것으로 예상됩니다.

그러나 원유가격 변동이 시장 성장을 방해할 가능성이 높습니다.

그럼에도 불구하고 바이오의 왁스 첨가제 응용 분야가 세계적으로 상승하고 있기 때문에 향후 시장에 유리한 기회가 생길 가능성이 높습니다.

아시아태평양은 중국, 일본, 인도 등 국가에서 엄청난 소비로 시장을 독점할 것으로 예상됩니다.

왁스 첨가제 시장 동향

왁스 첨가제는 페인트 분야에서 높은 수요가 예상된다.

왁스 첨가제는 최종 제품의 외관을 향상시키고 제품 출하 및 취급시 타박상이나 긁힘으로부터 보호하며 활성 화합물의 담체로 작용하기 때문에 코팅제에 널리 사용됩니다.

유연하고 많은 제형에 긍정적인 영향을 미치기 때문에 코팅제에 널리 사용됩니다. 일반적인 내구성, 내 스크래치성, 내마모성, 심지어 미끄럼 방지 효과도 기대할 수 있습니다.

세계도료공업회에 따르면 2022년 페인트 및 코팅의 세계 판매량은 약 1,799억 달러로 연간 성장률은 3.1%였습니다.

2022년 북미 시장 규모는 339억 2,000만 달러, 유럽 시장 규모는 423억 7,000만 달러로 평가되었습니다. 이러한 각 지역의 성장은 캐나다, 독일, 미국에서 주택 개혁 증가로 인한 것입니다.

아시아태평양의 페인트 및 코팅 시장은 2022년에 630억 달러에 달했습니다. 동아시아 지역은 세계의 페인트 및 코팅 시장에서 가장 유리한 시장입니다. 중국 시장은 2022년에 추가로 5.7% 증가했습니다. 현재의 추세에 따르면, 2022년에는 중국의 페인트 및 코팅의 총 매출액은 450억 달러를 넘어섰습니다.

페인트 및 코팅 산업은 자동차, 건축 및 건설 부문 수요 증가로 인해 해마다 성장해 왔습니다. 이러한 수요 증가는 수요 및 공급의 격차를 줄이기 위해 세계 및 국내 선수들에 의한 여러 국가의 확장 프로젝트로 이어졌습니다. 예를 들어, 악조노벨은 2023년 6월 미국 노스캐롤라이나주 하이포인트 남부에 있는 목공용 페인트 제조 캠퍼스의 5,500만 달러 확장을 발표했습니다.

따라서, 상기와 같은 요인이 코팅 용도를 촉진하고 예측 기간 동안 왁스 첨가제 수요를 높일 것으로 예상됩니다.

아시아태평양이 세계 시장을 선도할 전망

아시아태평양에서는 왁스 첨가제 시장이 크게 성장하여 중국과 인도 등 국가들이 코팅제와 인쇄 잉크의 대량 소비를 차지하고 있습니다.

중국에서는 코팅제, 인쇄 잉크, 촛불, 가죽 마감 등의 용도가 왁스 첨가제의 주요 수요를 견인하고 있습니다.

세계 페인트 코팅 산업회에 따르면 중국은 현재 이 지역 시장을 독점하고 있으며 CAGR 5.8%로 성장하고 있습니다. 중국의 페인트 및 코팅 시장은 2022년에 5.7% 증가했습니다.

현재의 추세에 따르면 2022년에는 중국의 페인트 및 코팅의 총 매출은 450억 달러를 넘었습니다. 이는 동아시아에서 가장 큰 시장 점유율(78%)을 가진 중국의 지배력을 보여줍니다.

인도의 페인트 및 코팅 산업은 약 80억 달러를 차지하고 있습니다. 인도 경제는 세계적으로 가장 빠르게 성장하는 국가 중 하나입니다. 인도에는 약 3,000개의 페인트 제조업체가 있습니다. 건축용 페인트의 점유율은 75%, 산업용 페인트의 점유율은 25%입니다.

또한 중국에서는 특히 휴일 시즌에 촛불을 사용하는 것이 인기입니다. 중국의 전통적인 공휴일 중 가장 중요한 것은 춘절이라고도 불리는 설날입니다.

무역지도에 따르면 2023년 6월, 7월, 8월 3개월 동안 각 각 7만 7,583달러, 9만 1,034달러, 9만 8,438달러 초가 수출되었습니다.

한편 일본은 2023년 8월에 전 세계에서 2,495달러 상당의 초를 수입했습니다. 특히 인기 있는 디자인은 꽃무늬 초로, 일본에서는 불교도들 사이에서 일상적인 제물로 인기를 끌었습니다. 또한 칠한 왁스 양초는 촛불을 좋아하는 사람에게 애용되고 있습니다.

또한, 국제 잉크 제조 업체도 중국에서 큰 존재감을 보여줍니다. T&K 동화와의 합작회사인 항주 동화묵과 동양잉크와의 합작회사인 천진동양묵은 중국의 2대 잉크 제조업체입니다. DIC, Flint Group, Sakata INX, Siegwerk 및 기타 잉크 산업의 리더 기업도 중국에서 큰 존재감을 보여줍니다.

위의 요인은 정부의 지원과 함께 예측 기간 동안 왁스 첨가제 시장 수요 증가에 기여하고 있습니다.

왁스 첨가제 산업 개요

왁스 첨가제 시장은 세분화됩니다. 이 시장의 주요 기업으로는 Lubrizol Corporation, Honeywell International Inc., BASF SE, Arkema, and Clariant 등이 있습니다(특정 순서 없이).

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 및 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

홈 데콜과 헬스 센터에서의 촛불의 소비 확대

코팅제나 잉크에 있어서의 왁스 첨가제의 특전

억제요인

원유 가격 변동

업계 밸류체인 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

재료

천연

반합성

합성

유형

디스퍼전

에멀젼

마이크로나이즈드

용도

코팅

가죽 마무리

인쇄 잉크

촛불

기타 용도(플라스틱 가공, 접착제, 고무 첨가제)

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Arkema

BASF SE

BYK-CHEMIE GmbH

Clariant

Concentrol

Evonik Industries AG

Honeywell International Inc.

Innospec

Munzing Corporation

Paramold Manufacturing LLC

Shamrock Technologies, Inc.

The Lubrizol Corporation

Tianshi Wax

제7장 시장 기회와 앞으로의 동향

바이오베이스 왁스 첨가제의 새로운 용도

SHW

영문 목차

영문목차

The Wax Additives Market size is estimated at USD 1.76 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 4.95% during the forecast period (2025-2030).

The outbreak of COVID-19 resulted in hindrances in construction activities. Furthermore, due to semiconductor chip shortage and other supply chain disruptions, automotive manufacturing was also affected severely. However, the wax additives market recovered from the pandemic and is growing significantly.

Key Highlights

The growing consumption of candles in home decor and health centers is likely to drive the demand for the market forward. Furthermore, the properties imparted by the wax additives in coatings and inks are also expected to fuel the market growth.

However, the volatility in crude oil prices is likely to hamper the market growth.

Nevertheless, emerging bio-based wax additive applications on a worldwide scale are likely to present lucrative opportunities for the market in the future.

The Asia-Pacific region is expected to dominate the market with enormous consumption from countries such as China, Japan, and India.

Wax Additives Market Trends

Wax Additives Expected to find High Demand in Coatings Segment

Wax additives are widely used in coatings to improve the appearance of finished products, help protect from bruising or scratching during the shipping and handling of goods, and act as a carrier for active compounds.

They are used extensively in coatings because of their flexibility and significant positive impact on many formulation types. They can provide general durability, scratch and abrasion resistance, and even anti-slip properties.

According to the World Paint and Coatings Industry Association, in 2022, the global sales volume of paints and coatings stood at around USD 179.9 billion, with an annual growth rate of 3.1%.

The North American market value stood at USD 33.92 billion, while Europe was valued at USD 42.37 billion in 2022, respectively. The growth of these respective regions is attributed to an increase in the number of house renovation activities in Canada, Germany, and the United States.

The Asia-Pacific paints and coatings market stood at USD 63 billion in 2022. The East Asian region is the most lucrative market for paints and coatings worldwide. The Chinese market further increased by 5.7 % in 2022. From the current trend, in 2022, China's total sales of paints and coatings exceeded USD 45 billion.

The paint and coatings industry grew over the years due to increased demand from the automotive, building, and construction sectors. Such increased demand led to several expansion projects by global and domestic players in several countries to reduce the demand and supply gap. For instance, in June 2023, AkzoNobel unveiled the USD 55 million expansion of its wood coatings manufacturing campus in south High Point in North Carolina, United States.

Therefore, all the above factors are expected to drive the coatings application, enhancing the demand for wax additives during the forecast period.

Asia-Pacific Region Expected to Lead the Global Market

The Asia-Pacific region saw significant growth in the wax additives market, with countries such as China and India accounting for significant consumption of coatings and printing inks.

In China, the major demand for wax additives is driven majorly by applications such as coatings, printing inks, candles, leather finishing, and others.

According to the World Paint & Coatings Industry Association, China presently dominates the region market, which is growing at a CAGR of 5.8%. The Chinese paints and coatings market increased by 5.7% in 2022.

From the current trend, in 2022, China's total sales of paints and coatings exceeded USD 45 billion. It is, thereby, depicting the country's dominance with the largest market share (78%) in East Asia.

The Indian Paint and Coating Industry accounts for around USD 8 billion. It is considered one of the fastest-growing economies globally. India comprises around 3,000 paint manufacturers. The country exhibits a 75% share of architectural and a 25% share of industrial paints.

Further, the usage of candles in China is very popular, particularly during the holiday season. The most important of all traditional Chinese holidays is Chinese New Year, also known as Spring Festival.

As per the trade map, the country exported candles with a value of USD 77,583, 91,034, and 98,438 in the June, July, and August months of 2023.

Japan, on the other hand, imported USD 2,495 worth of candles from all around the world in August 2023. A particularly popular design is a candle with flower patterns that became popular amongst Buddhists as a daily offering in the country. Moreover, painted wax candles are used by people who love candles.

Furthermore, international ink manufacturers also hold a major presence in China. Hangzhou Toka Ink, a joint venture with T&K Toka, and Tianjin Toyo Ink Co. Ltd, a joint venture with Toyo Ink, are China's two largest ink manufacturers. DIC, Flint Group, Sakata INX, Siegwerk, and other ink industry leaders also include a sizable presence in China.

The factors above, coupled with government support, are contributing to the increasing demand for the wax additives market during the forecast period.

Wax Additives Industry Overview

The market for wax additives is fragmented in nature. Some of the major players in the market include The Lubrizol Corporation, Honeywell International Inc., BASF SE, Arkema, and Clariant (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Consumption of Candles in Home Decor and Health Centers

4.1.2 Wax Additives Benefits in Coatings and Inks

4.2 Restraints

4.2.1 Volatility in Crude Oil Price

4.3 Industry Value Chain Analysis

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Material

5.1.1 Natural

5.1.2 Semi-synthetic

5.1.3 Synthetic

5.2 Type

5.2.1 Dispersion

5.2.2 Emulsion

5.2.3 Micronized

5.3 Application

5.3.1 Coatings

5.3.2 Leather Finishing

5.3.3 Printing Ink

5.3.4 Candles

5.3.5 Other Applications (Plastic Processing, Adhesives, and Rubber Additive)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements