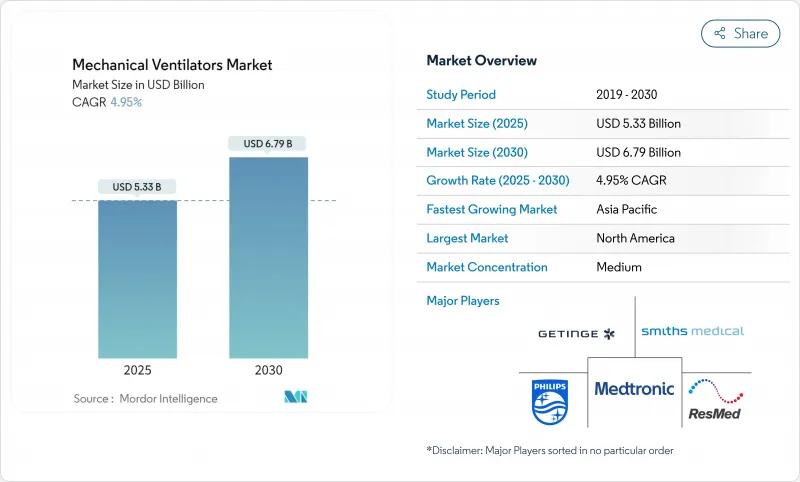

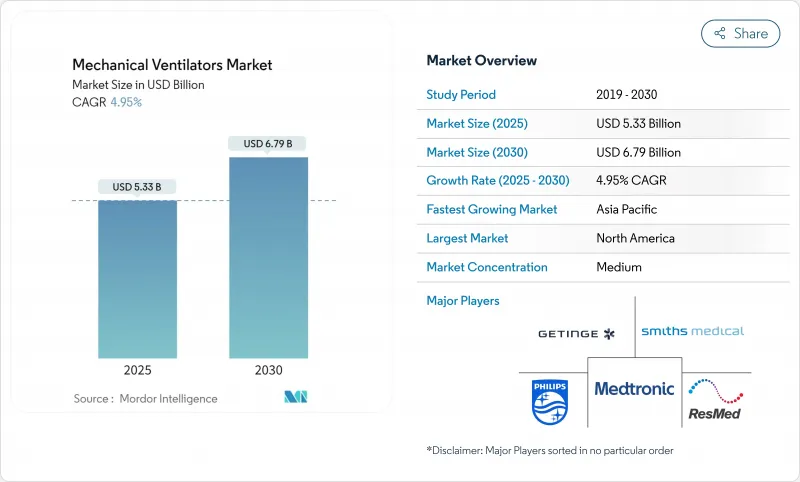

기계식 인공호흡기 시장의 2025년 시장 규모는 53억 3,000만 달러로 추정되고, 2030년에는 67억 9,000만 달러에 이를 것으로 예측되며, CAGR 4.95%로 추이할 전망입니다.

성장은 팬데믹 의한 급증으로부터, ICU에서의 장기 체류를 필요로 하는 고령화나 COPD 등의 만성 호흡기 질환 증가에 지지된 꾸준한 확대로 이행되고 있습니다. 인공지능이 폐쇄 루프의 인공호흡을 자동화하고, 임상의의 부담을 줄이며, 합병증을 줄이기 때문에 자본 예산이 엄격하더라도 병원은 의료기기를 업데이트하는 경향이 있습니다. 메디케어의 규칙이 업데이트되어 만성 호흡 부전에 대한 비침습적 인공호흡이 커버되어 환자가 재입원을 회피할 수 있게 되었기 때문에 재택 치료가 병행해 성장 엔진으로서 대두해 왔습니다. 특히 아시아태평양에서는 중증 환자를 위한 의료 인프라가 지역적으로 불균형하기 때문에 낮은 급성기 요구에 대응하는 비용 효과적인 장비의 백색 공간이 될 수 있습니다.

세계의 COPD 환자 수가 증가하고 있으며 침습적 및 비침습적 장치에 대한 수요가 강화되고 있습니다. 메디케어 및 메디케이드 서비스 센터(Medicaid Services, Centers for Medicare)는 2025년까지 PaCO2가 52mmHg 이상인 경우 재택 인공호흡 적용 범위를 확대하여 COPD 치료 대상자를 확대했습니다. 재택 요법은 낮 동안 호흡 곤란이 남아있는 반면, 재입원을 줄이고 혈액가스 교환을 개선합니다. 이러한 결과는 지급자에게 받아들여져, 제조자가 컴팩트하고 유지 보수가 적은 비침습적 모델을 조정하는 원동력이 되었습니다. 질병 부담이 고령화됨에 따라 만성 합병증 관리로의 폭넓은 인구통계학적 시프트에 동반하여 수요도 수렴해 나갈 것입니다.

노인은 이미 호주 인구의 22%를 차지하고 있으며, 비슷한 경향이 서양에서도 발견됩니다. 만성 질환이 증가함에 따라 미국에서는 2030년까지 1억 7,000만 일의 입원 일수가 발생한다고 병원협회는 예측했습니다. 환기 과정의 장기화가 장비 교체를 촉진하고 집중 치료 전문의 부족이 계속되면 병원은 손으로 조정을 줄이는 것보다 더 스마트한 모드에 투자하게 됩니다. 프랑스에서는 현재 ICU의 3분의 2가 적어도 한 명의 의사를 결원으로 삼아 자동화의 가치를 높이고 있습니다. 중국과 같은 국가들은 금세기 중반까지 1인당 의료비를 10배 이상 늘릴 수 있는 대규모 지출 증가를 계획하고 있으며, 이는 지속적인 능력 증진을 시사합니다. COVID-19의 팬데믹은 지리적 불균형을 드러냈지만, 기술 공급업체는 모듈식으로 신속한 배치가 가능한 유닛을 통해 그 시정을 지원할 수 있습니다.

지정학적 충격으로 인한 부품 가격 상승으로 공급망 비용 총액은 장비 수익의 최대 20%를 흡수합니다. 인공호흡기는 메디케어의 '빈번하고 실질적인 유지보수 점검' 범주로 분류되며 정기적인 유지보수 점검이 의무화되어 소유 비용이 증가하고 있습니다. FDA의 2026년 품질규칙에 대한 대응은 특히 AI 소프트웨어 업데이트를 위한 문서화 및 검증 비용을 더욱 증가시킵니다. ICU의 병상 수가 평균 이하인 신흥 병원은 프리미엄 모델의 자금 조달에 고전해, 재생품이나 현지 조립의 유닛에 조타를 끊고 있습니다. 공급업체는 물류의 오버헤드를 억제하기 위해 급성기 병상 계층간에 부품을 공유하는 모듈식 설계로 대응합니다.

집중 치료실이 기계식 인공호흡기 시장 점유율의 54.91%를 차지하고 있습니다. 집중 치료실의 구매 결정은 공급업체의 연구 개발 주도권을 잡고 적응성이 높은 폐쇄 루프 모드와 저소음 터빈을 생산하여 이송 변종으로 전환하고 있습니다. ICU 모델의 기계식 인공호흡기 시장 규모는 여전히 전체 매출을 초과할 것으로 예측됩니다. 이는 소프트웨어의 진보로 측정 가능한 품질 향상이 촉진되면 병원이 저시설보다 빨리 함대 업데이트를 수행하기 때문입니다. 휴대용 장치는 보다 작은 베이스에서 시작하는 반면, 응급 서비스 및 재해 대응 팀이 배터리 구동 시간과 견고한 하우징을 우선하기 때문에 CAGR 5.34%로 가속합니다. HAMILTON-C6은 ICU 등급 알고리즘을 10kg 이하의 이동식 인클로저에 패키징하여 부문을 넘어서는 기술 이전을 실현하고 있습니다. 특히 북미에서는 진료 보수 코드로 시설 간 이동시 청구가 가능해지면 반송의 채용도 늘어납니다.

아급성기 병동을 위한 하이브리드 제품 클래스가 등장해, 이상 툴과 중간 정도의 플로우 기능을 융합시키는 것으로, 풀 프라이스의 ICU 하드웨어를 회피하고 있습니다. 함대 관리자는 섀시 제품군에 공통된 소모품을 높이 평가하고 재고를 줄입니다. 모빌리티 클래스간에 공통 사용자 인터페이스를 설계하는 공급업체는 교육을 단순화하고 사용자 오류를 줄입니다. 이러한 가치 제안은 공공 입찰이 최저 비용 준수 입찰을 중시하는 중에서도 비싼 가격 설정을 보호하는 데 도움이 됩니다.

침습적 인공호흡은 2024년 매출의 64.25%를 차지했습니다. 이는 심각한 ARDS와 수술은 여전히 기관 내 접근이 필요하기 때문입니다. 침습적 시스템과 관련된 기계식 인공호흡기 시장 규모는 소폭 확대되는 반면, 비침습적 라인은 가정 내로의 보급과 조기 개입 프로토콜 덕분에 CAGR 5.71%를 기록합니다. IntelliTrig와 같은 누출을 보상하는 소프트웨어는 환자의 동조성을 높이고 삽관으로의 에스컬레이션을 줄입니다. 병원에서는 임상의가 하드웨어를 교체하지 않고 전환할 수 있도록 듀얼 모드 장비의 도입이 진행되고 있습니다.

비침습적인 장점은 소아 및 신생아 용도 증가로 인해 발생합니다. 작은 기도와 얼굴 구조에 맞는 인터페이스는 장기간의 치료를 가능하게 하는 동시에 피부 손상을 줄입니다. 헬멧과 마우스 피스형 인공 호흡기는 마스크가 폐소 공포증의 트리거가 될 때 대안을 제공합니다. 고 유량 비강 캐뉼라의 규제 승인은 경미한 저산소 혈증의 경우를 커버함으로써 기존의 NIV에 경쟁자를 추가합니다. 제조업체는 모듈형 매니폴드 커넥터 및 센서 어레이를 통해 포트폴리오 폭과 재고 복잡성의 균형을 맞추고 있습니다.

기계식 인공호흡기 시장 점유율의 42.91%를 차지하는 북미는 광범위한 ICU 인프라, 연방 정부의 비축, 지원적인 상환의 틀에서 이익을 얻고 있습니다. 공공 조달 정책은 현재 집중적인 예비구입과 병원 설비의 갱신 보조를 조합하고 있어 2020-2022년 수요 급증 후의 주문 패턴을 원활하게 하고 있습니다. FDA(미국 식품의약국)의 사이버 보안 가이던스 준수도 유효한 소프트웨어 라이프 사이클을 가진 국내 공급업체에게 유리합니다.

유럽은 성숙하면서도 혁신적인 구매자로 계속됩니다. 이 지역에서는 에너지 효율적인 터빈과 암호화된 클라우드 커넥터에 공급업체를 향하게 하는 엄격한 환경 설계 및 데이터 보호 규칙이 시행되고 있습니다. 여러 국가가 치명타 관리를 위한 AI 로드맵을 수립하고 시험 도입에 자금을 제공합니다. 평균 판매 가격과 소프트웨어 구독 상승으로 수익이 증가했습니다.

아시아태평양은 CAGR 가장 빠른 6.71%를 기록했습니다. 중소득국의 인구 10만 명당 중증 환자 침대수를 5층 이상으로 끌어올리는 것을 목표로 하는 의료 인프라 구상이 원동력이 되고 있습니다. 지역 내의 편차는 큽니다. 일본과 같은 고소득국가는 5년마다 업그레이드 주기를 유지하고 있는 반면, 저소득국은 조성금에 의한 자금조달에 의존하고 있습니다. 공급업체는 벽걸이식 및 압축기식 산소원을 모두 수용하는 확장 가능한 플랫폼을 제공함으로써 성공을 거두고 있습니다.

2009년 중국이 집중 치료를 전문 분야로 인정한 것으로 프로토콜을 표준화하고 기기 입찰을 가속시키는 전문학회 네트워크에 불이 붙었습니다. 현지 기업은 수입 관세를 피하기 위해 서유럽 터빈 기술을 공동 라이선스하고 다국적 기업에 가격 압력을 가하고 있습니다. 인도와 인도네시아는 국내에서의 부가가치 향상을 30% 이상 촉진하는 Make-in-Country 제도를 우선하고 있습니다.

라틴아메리카에서는 COVID-19 사이에 긴급 제조 붐이 일어났습니다. 각국 정부는 현재 일부 팝업 시설을 상설 중증 환자용 병동으로 전환하여 중견급 인공호흡기에 대한 기본 수요를 유지하고 있습니다. 그럼에도 불구하고 통화 변동이 자본 수입을 복잡하게 하기 때문에 임대 모델이 인기를 끌고 있습니다.

중동 및 아프리카는 보급이 늦었지만 장기적인 잠재력을 가지고 있습니다. 석유 자원이 풍부한 걸프 국가들은 높은 사양의 ICU에 자금을 제공하고 일산화질소 공급 기능을 내장한 고급기를 요구하고 있습니다. 자원이 부족한 국가는 기증자로부터의 자금 지원에 의존하고 있으며, 먼지가 많은 환경과 가변 전원에 대응할 수 있는 견고한 유닛이 필요합니다. 공급업체는 NGO와 제휴하여 교육을 번들로 채택을 용이하게 합니다.

미국은 북미의 기계식 인공호흡기 시장을 독점하고 2024년 인공호흡기 시장 점유율의 약 45%를 차지했습니다. 이 나라 시장 리더십은 고급 집중 치료 시설을 갖춘 5,000개 이상의 병원으로 구성된 광범위한 헬스케어 네트워크에 의해 지원됩니다. 선도적인 제조업체의 존재, 견고한 헬스케어 인프라 및 높은 의료비 지출로 인해 일본 시장 지위가 더욱 강화되고 있습니다. 미국 시장은 만성 호흡기 질환의 이환율 증가와 장기적인 환기 지원을 필요로 하는 노화로 인해 집중 치료용 인공호흡기 및 휴대용 환기 솔루션 모두에 대한 왕성한 수요가 특징입니다.

캐나다는 북미에서 가장 급성장하고 있는 시장으로, 2024-2029년의 성장률은 약 7%로 예측되고 있습니다. 이 나라 시장 성장의 원동력은 헬스케어 지출 증가, 재택 헬스케어 솔루션 채택 확대, 호흡 관리 관리에 대한 의식 증가입니다. 캐나다의 의료시설에서는 환자의 예후를 개선하기 위해 고급 환기 기술에 대한 투자가 증가하고 있습니다. 정부의 지원적인 헬스케어 정책과 치명타 케어 인프라의 강화에 주력하는 자세가 시장 확대에 기여하고 있습니다. 이 나라에서는 특히 원격지의 헬스케어 환경이나 재택 케어 용도로, 휴대용 환기 장치 수요도 높습니다.

유럽의 기계식 인공호흡기 시장은 독일, 영국, 프랑스, 이탈리아, 스페인의 확립된 헬스케어 시스템에 지원되어 큰 힘을 보여줍니다. 이 지역 시장은 선진 의료 기술의 채용률이 높고, 대기업 인공 호흡기 제조업체가 강한 존재감을 나타내고 있는 것이 특징입니다. 유럽 국가들은 의료기기에 대한 엄격한 규제 기준을 유지하면서 헬스케어 인프라 개선에 지속적으로 투자하고 있습니다. 이 시장은 재택 헬스케어 솔루션에 대한 관심과 모바일 인공 호흡기에 대한 수요 증가로 혜택을 누리고 있습니다.

독일은 유럽의 기계식 인공호흡기 시장을 선도하고 있으며, 2024년에는 이 지역의 인공호흡기 시장 점유율의 약 20%를 차지했습니다. 이 나라가 시장을 선도하는 이유는 견고한 헬스케어 시스템, 상당한 의료비, 강력한 국내 제조 능력에 있습니다. 독일 병원은 높은 수준의 집중 치료 시설을 유지하고 있으며 고급 인공 호흡 솔루션에 대한 일관된 수요를 보여줍니다. 선도적인 제조업체와 연구 기관의 존재가 환기 기술의 끊임없는 기술 혁신에 기여하는 반면, 고령화는 시장의 지속적인 성장을 뒷받침하고 있습니다.

영국은 유럽 중에서도 중요한 시장이며, 2024-2029년의 성장률은 약 7%로 예측되고 있습니다. 영국의 헬스케어 시스템은 치명타 케어 인프라의 현대화와 고급 호흡 케어 솔루션에 대한 액세스 확대에 계속 투자하고 있습니다. 이 나라에서는 가정용 의료 서비스의 중요성이 높아짐에 따라 휴대용 환기 솔루션과 홈 환기 솔루션의 채택이 증가하고 있습니다. 영국의 헬스케어 시설은 환자 관리의 결과와 업무 효율성을 개선하기 위해 새로운 환기 기술을 적극적으로 도입하고 있습니다.

아시아태평양 시장은 중국, 일본, 인도, 한국, 호주의 다양한 건강 관리 시장을 포함하여 강력한 성장 가능성을 보여줍니다. 이 지역에서는 헬스케어 인프라의 정비가 진행되고, 헬스케어 지출이 증가하며, 호흡 케어에 대한 의식이 높아지고 있습니다. 급속한 도시화, 오염 수준의 상승, 호흡기 질환의 이환율의 상승이 이들 국가에서 시장 확대의 원동력이 되고 있습니다. 이 지역은 또한 국내 생산 능력의 향상과 선진 의료 기술의 채용 증가로부터 이익을 얻고 있습니다.

중국은 아시아태평양 최대의 기계식 인공호흡기 시장으로서의 지위를 유지하고 있습니다. 이 나라의 광범위한 헬스케어 시스템의 현대화, 환자 수가 많음, 국내 제조 능력의 향상이 시장 성장의 원동력이 되고 있습니다. 중국의 의료 시설은 치명타 케어 능력을 계속 확대하고 있는 한편, 재택 헬스케어 솔루션에 대한 주목이 높아지고 있는 것이 새로운 시장 기회를 창출하고 있습니다. 헬스케어 인프라에 대한 투자와 의료기기 제조의 자급자족을 중시하는 자세가 이 나라 시장 포지션을 강화하고 있습니다.

한국은 아시아태평양에서 가장 빠르게 성장하는 시장입니다. 이 나라의 첨단 헬스케어 시스템, 강력한 기술력, 헬스케어 이노베이션에 대한 주력의 고조가 시장 확대의 원동력이 되고 있습니다. 한국의 의료시설은 고도의 환기 기술의 채용률이 높고, 고령화가 진행되는 이 나라에서는 지속적인 수요가 창출되고 있습니다. 이 시장은 강력한 국내 제조 능력 및 헬스케어 인프라 개척에 대한 지속적인 투자로 이익을 얻고 있습니다.

중동 및 아프리카 기계식 인공호흡기 시장은 유망한 성장 잠재력을 보이지만 지역에 따라 큰 변동이 있습니다. GCC 국가들은 대규모 헬스케어 투자와 현대 의료시설의 혜택을 받아 지역 시장을 선도하고 있습니다. 남아프리카도 주요 시장의 하나이며 의료 인프라의 정비와 선진 의료 기술의 도입이 진행되고 있습니다. 이 지역에서는 구명 응급 시설 개선과 고급 호흡 관리 솔루션에 대한 접근성 확대에 점점 초점이 맞추어지고 있으며, GCC 국가들은 이 지역에서 가장 크고 가장 빠르게 성장하는 시장으로 부상하고 있습니다.

남미의 기계식 인공호흡기 시장은 진화를 계속하고 있으며, 브라질과 아르헨티나가 이 지역의 주요 시장이 되고 있습니다. 이 시장은 지속적인 헬스케어 인프라 개척, 의료비 증가, 호흡 관리에 대한 의식 증가 등의 혜택을 누리고 있습니다. 브라질은 이 지역에서 가장 큰 시장으로 자리잡고 있으며 아르헨티나는 가장 빠른 성장 가능성을 보여줍니다. 이 지역에서는 의료투자 확대와 첨단 의료기술 접근성 확대로 집중 치료용 및 휴대용 환기 솔루션의 채용이 증가하고 있습니다.

The mechanical ventilator market is valued at USD 5.33 billion in 2025 and is forecast to reach USD 6.79 billion by 2030, advancing at a 4.95% CAGR.

Growth is shifting from pandemic-driven surges to steady expansion supported by aging populations that demand longer ICU stays and by rising chronic respiratory conditions such as COPD. Artificial-intelligence features now automate closed-loop ventilation, cut clinician workload, and reduce complications, encouraging hospitals to refresh fleets despite tighter capital budgets. Home care is emerging as a parallel growth engine because updated Medicare rules cover non-invasive ventilation for chronic respiratory failure, enabling patients to avoid repeat admissions. Regional imbalances in critical-care infrastructure, especially in Asia-Pacific, create white-space opportunities for cost-effective devices that meet lower-acuity needs.

Global COPD cases continue climbing, reinforcing baseline demand across invasive and non-invasive devices. The Centers for Medicare & Medicaid Services broadened 2025 coverage for home ventilation when PaCO2 remains at or above 52 mmHg, which expands the treated COPD population.Overlap with obesity hypoventilation syndrome and obstructive sleep apnea has produced a 1.560% prevalence pool that often requires domiciliary ventilatory support. Home therapy lowers readmissions and improves blood-gas exchange, even though daytime dyspnea persists. These outcomes underpin payer acceptance and spur manufacturers to tailor compact, low-maintenance non-invasive models. As the disease burden skews older, demand also converges with the broader demographic shift toward chronic comorbidity management.

Older adults already make up 22% of Australia's population and similar trajectories exist across Europe and North America. Hospital associations project 170 million inpatient days in the United States by 2030 as chronic conditions rise. Longer ventilation courses drive equipment turnover, while persistent intensivist shortages prompt hospitals to invest in smarter modes that reduce hands-on adjustments. In France, two-thirds of ICUs now report at least one physician vacancy, magnifying the value of automation. Nations such as China plan large expenditure increases that could lift per-capita health spending more than 10-fold by mid-century, signaling sustained capacity buildouts. The COVID-19 pandemic exposed geographic imbalances that technology suppliers can help correct through modular, rapidly deployable units.

Total supply-chain expenses absorb up to 20% of device revenue as geopolitical shocks raise component prices. Ventilators fall under Medicare's Frequent and Substantial Servicing category, obligating regular upkeep that inflates ownership costs. Compliance with the FDA's 2026 quality rule will further increase documentation and validation spending, particularly for AI software updates. Emerging hospitals with below-average ICU bed density struggle to finance premium models, steering them toward refurbished or locally assembled units. Suppliers respond with modular designs that share parts across acuity tiers to curb logistics overhead.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Intensive care units dominate with 54.91% mechanical ventilator market share. Their purchasing decisions steer supplier R&D, producing adaptive closed-loop modes and low-noise turbines that then migrate into transport variants. The mechanical ventilator market size for ICU models is projected to continue outpacing overall revenue because hospitals refresh fleets faster than lower-acuity sites when software advances push measurable quality gains. Portable devices, though starting from a smaller base, accelerate on 5.34% CAGR as emergency services and disaster-response teams prioritize battery runtime and rugged housings. The HAMILTON-C6 illustrates cross-segment technology transfer by packaging ICU-grade algorithms in a moveable chassis that weighs under 10 kg. Transport adoption also rises when reimbursement codes permit billing during inter-facility transfers, particularly in North America.

A hybrid product class for sub-acute wards has emerged, blending weaning tools with moderate flow capabilities to avoid full-price ICU hardware. Fleet managers appreciate common consumables across chassis families, which lowers inventory. Suppliers that design shared user interfaces across mobility classes simplify training and cut user error. These value propositions help defend premium pricing even as public tenders emphasize lowest cost compliant bids.

Invasive ventilation accounts for 64.25% of revenue in 2024 because severe ARDS and surgical procedures still require endotracheal access. The mechanical ventilator market size linked to invasive systems will expand modestly, while non-invasive lines post 5.71% CAGR thanks to domiciliary uptake and early intervention protocols. Leakage-compensation software such as IntelliTrig enhances patient synchrony, reducing escalation to intubation. Hospitals increasingly deploy dual-mode devices so clinicians can switch without swapping hardware, which lowers capital intensity.

Non-invasive gains also stem from growing pediatric and neonatal applications. Interfaces tailored to small airways and facial structures reduce skin injuries while enabling prolonged therapy. Helmets and mouthpiece ventilation deliver alternatives where masks trigger claustrophobia. Regulatory approvals for high-flow nasal cannula add competitors to conventional NIV by covering mild hypoxemia cases. Manufacturers balance portfolio breadth with inventory complexity through modular manifold connectors and sensor arrays.

The Mechanical Ventilators Market Report is Segmented by Mobility (Intensive Care Ventilators, Portable Ventilators, and More), Interface (Invasive Ventilation and Non-Invasive Ventilation), Patient (Adult, Pediatric, and Neonatal) End User (Hospitals, Home Healthcare, and Ambulatory Surgical Centers), and Geography. The Market Size and Forecasts are Provided in Terms of Value (USD) for the Above Segments.

North America, with 42.91% mechanical ventilator market share, benefits from extensive ICU infrastructure, federal stockpiles, and supportive reimbursement frameworks . Public procurement policy now blends centralized reserve purchases with hospital fleet refresh subsidies, smoothing order patterns after the 2020-2022 demand spike. Adherence to FDA cybersecurity guidance also favors domestic suppliers with validated software lifecycles.

Europe follows as a mature yet innovative buyer. The region enforces strict eco-design and data-protection rules that push vendors toward energy-efficient turbines and encrypted cloud connectors. Several countries roll out national AI roadmaps for critical care, making funding available for pilot deployments. Market volume remains steady; revenue growth arises from higher average selling prices and software subscriptions.

Asia-Pacific records the fastest 6.71% CAGR, powered by health infrastructure initiatives that aim to lift critical-care bed density above 5 per 100,000 population in middle-income nations . Variance within the region is high. High-income economies such as Japan sustain upgrade cycles every five years, whereas low-income countries rely on grant financing. Suppliers succeed by offering scalable platforms that accept both wall and compressor oxygen sources.

China's recognition of intensive care as a specialty in 2009 ignited a network of professional societies that standardize protocols and accelerate equipment tendering. Local firms co-licensed western turbine technology to bypass import tariffs, putting price pressure on multinationals. India and Indonesia prioritize Make-in-Country schemes that favor domestic value addition above 30%.

Latin America saw emergency manufacturing booms during COVID-19. Governments now convert some pop-up facilities into permanent critical-care wards, sustaining baseline demand for mid-tier ventilators. Currency volatility nevertheless complicates capital imports, so lease models gain popularity.

The Middle East and Africa trail in penetration yet hold long run potential. Oil-rich Gulf states fund high-spec ICUs, demanding premium devices with integrated nitric oxide delivery. Resource-poorer nations depend on donor funding and require rugged units capable of dusty environments and variable power supply. Suppliers partner with NGOs to bundle training, easing adoption.

The United States dominates the North American mechanical ventilators market, accounting for approximately 45% of the regional ventilator market share in 2024. The country's market leadership is supported by its extensive healthcare network comprising over 5,000 hospitals with advanced intensive care facilities. The presence of leading manufacturers, robust healthcare infrastructure, and high healthcare expenditure further strengthen its market position. The US market is characterized by strong demand for both intensive care ventilators and portable ventilation solutions, driven by the rising incidence of chronic respiratory diseases and an aging population requiring long-term ventilation support.

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 7% during 2024-2029. The country's market growth is driven by increasing healthcare expenditure, growing adoption of home healthcare solutions, and rising awareness about respiratory care management. Canadian healthcare facilities are increasingly investing in advanced ventilation technologies to improve patient outcomes. The government's supportive healthcare policies and focus on enhancing critical care infrastructure contribute to market expansion. The country also shows strong demand for portable ventilators, particularly in remote healthcare settings and home care applications.

The European mechanical ventilators market demonstrates significant strength, supported by well-established healthcare systems across Germany, the United Kingdom, France, Italy, and Spain. The region's market is characterized by high adoption rates of advanced medical technologies and a strong presence of major ventilator manufacturers. European countries maintain strict regulatory standards for medical devices while continuously investing in healthcare infrastructure improvement. The market benefits from an increasing focus on home healthcare solutions and rising demand for portable ventilation devices.

Germany leads the European mechanical ventilators market, holding approximately 20% of the regional ventilator market share in 2024. The country's market leadership is attributed to its robust healthcare system, substantial healthcare spending, and strong domestic manufacturing capabilities. German hospitals maintain high standards of intensive care facilities and demonstrate consistent demand for advanced ventilation solutions. The presence of major manufacturers and research institutions contributes to continuous innovation in ventilation technologies, while the country's aging population drives sustained market growth.

The United Kingdom represents a significant market in Europe, with a projected growth rate of approximately 7% during 2024-2029. The UK's healthcare system continues to invest in modernizing its critical care infrastructure and expanding access to advanced respiratory care solutions. The country shows increasing adoption of portable and home ventilation solutions, driven by a growing emphasis on home healthcare services. British healthcare facilities are actively incorporating new ventilation technologies to improve patient care outcomes and operational efficiency.

The Asia-Pacific mechanical ventilators market demonstrates robust growth potential, encompassing diverse healthcare markets across China, Japan, India, South Korea, and Australia. The region experiences increasing healthcare infrastructure development, rising healthcare expenditure, and growing awareness about respiratory care. Rapid urbanization, increasing pollution levels, and rising incidence of respiratory diseases drive market expansion across these countries. The region also benefits from growing domestic manufacturing capabilities and increasing adoption of advanced medical technologies.

China maintains its position as the largest market for mechanical ventilators in the Asia-Pacific region. The country's extensive healthcare system modernization, large patient population, and growing domestic manufacturing capabilities drive market growth. Chinese healthcare facilities continue to expand their critical care capabilities, while increasing focus on home healthcare solutions creates new market opportunities. The country's investment in healthcare infrastructure and emphasis on medical device manufacturing self-sufficiency strengthens its market position.

South Korea emerges as the fastest-growing market in the Asia-Pacific region. The country's advanced healthcare system, strong technological capabilities, and increasing focus on healthcare innovation drive market expansion. Korean healthcare facilities demonstrate high adoption rates of advanced ventilation technologies, while the country's aging population creates sustained demand. The market benefits from strong domestic manufacturing capabilities and continuous investment in healthcare infrastructure development.

The Middle East & Africa mechanical ventilators market shows promising growth potential, with significant variations across different regions. The GCC countries lead the regional market, benefiting from substantial healthcare investments and modern medical facilities. South Africa represents another key market, with growing healthcare infrastructure development and increasing adoption of advanced medical technologies. The region demonstrates an increasing focus on improving critical care facilities and expanding access to advanced respiratory care solutions, with the GCC emerging as both the largest and fastest-growing market in the region.

The South American mechanical ventilators market continues to evolve, with Brazil and Argentina representing key markets in the region. The market benefits from ongoing healthcare infrastructure development, increasing healthcare expenditure, and rising awareness about respiratory care. Brazil maintains its position as the largest market in the region, while Argentina shows the fastest growth potential. The region demonstrates increasing adoption of both intensive care and portable ventilation solutions, supported by growing healthcare investments and expanding access to advanced medical technologies.