ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

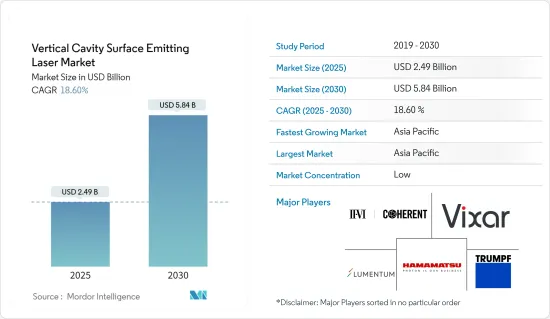

수직 공진기 면발광 레이저 시장 규모는 2025년에 24억 9,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR은 18.6%로 전망되며, 2030년에는 58억 4,000만 달러에 달할 것으로 예측되고 있습니다.

출하 대수에서는 2025년 51억 4,000만대에서 2030년에는 160억 6,000만대로 성장할 것으로 예측되며, 예측 기간 2025년부터 2030년까지 CAGR은 25.60%로 전망됩니다.

수직 공진기 면발광 레이저(VCSEL)는 레이저가 상면에 수직으로 방사되는 반도체입니다. 가장자리에서 레이저를 방출하는 끝면 발광 레이저와 다릅니다. VCSEL은 비용 효율적인 솔루션으로 고정밀도, 고효율, 고신뢰성 및 고속성을 제공하며 레이저 물리학에서 가장 유망한 신기술 개발입니다. VCSEL은 저전력, 빔 품질, 변조 속도, 제조 비용 등 다양한 이점을 제공합니다.

주요 하이라이트

VCSEL 시장은 고속 및 고효율로 장거리 데이터 전송에 대한 요구가 높아지고, 차량 탑재 LiDAR 용도나 산업용도에 있어서의 VCSEL 레이저 수요 증가 등, 여러 요인들로부터 예측 기간 중에 강력한 성장이 예상됩니다. 2023년 8월 Innoviz Technologies와 BMW 그룹은 차세대 LiDAR의 B-샘플 개발 단계를 시작하여 협력을 확대하고 있습니다.

최근 몇 년동안 데이터센터의 광 상호 연결 인프라는 100Gbit/s에서 차세대 400Gbit/s의 데이터 속도로 발전하고 있습니다. 이는 주로 AI, VR/AR, 사물인터넷(IoT) 등 신기술의 급속한 시장 성장과 5G 모바일 네트워크 시스템의 도입으로 데이터센터 내의 데이터 트래픽이 계속 증가하고 있기 때문입니다.

스마트폰 제조업체에 의한 3D 센싱 및 근접 센싱 용도에서 스마트폰에 대한 VCSEL 채용 증가는 시장 성장을 가속하는 주요 요인 중 하나입니다. 3D 센싱의 성장은 iPhone에 페이스 ID 모듈이 도입됨으로써 추진되었습니다. 그 이후로 3D 감지에는 큰 진전이 있었습니다. 점차적으로 3D 센싱은 프론트 측의 얼굴 인증 모듈에서 사진 촬영 용도의 리어 측으로 이행해 갔습니다.

InP 기반 VCSEL은 분산이 적고 광섬유 손실이 적기 때문에 일반적으로 광통신과 같은 용도에 선호됩니다. 그러나 InP 기반 VSCEL은 높은 반사율과 낮은 투과 깊이로 인해 큰 굴절률 대비 DBR 미러를 제공할 수 없습니다. 유효 공진기 길이는 튜닝 범위와 구속 계수를 제한합니다.

COVID-19의 유행은 조사한 시장에 현저한 영향을 미쳤고, VCSEL을 도입하는 몇몇 최종 사용자 산업은 몇몇 어려움에 직면했습니다. 각 산업은 전국적인 조업정지에 휩쓸려 발걸음 상태에 빠졌지만 2020년 2분기 이후 서서히 조업을 시작했습니다. 원료는 중국에서 구입하기 때문에 미국이 부과한 관세의 영향을 받습니다.

세계의 지정학적 긴장과 분쟁이 군사비 수요를 견인하고 있습니다. 스톡홀름 국제평화랩(SIPRI)에 따르면 미국은 2022년 군사비가 가장 많은 나라의 순위에서 선두에 서서 군사비에 8,770억 달러를 투입했습니다. 이는 같은 해 세계 군사비 총액 2조 2,000억 달러의 40% 가까이를 차지했습니다. 이는 미국 국내총생산의 3.5%에 해당합니다.

수직 공진기 면발광 레이저 시장 동향

ADAS와 LiDAR이 급성장 용도로

자동차 산업은 VCSEL 제조업체의 주요 신흥 시장 중 하나이며 자율 주행 차량 및 자동차의 하이 엔드 내장 기능과 같은 동향에 기인합니다. 최근, 자동차 산업은 불황에 휩쓸리고 있지만, 자동차 1대당 센서수 증가가 주로 벤더를 움직이고 있습니다. 시장 벤더의 대부분은 자동차 시장(내장 및 외장 용도)의 범위를 확대하고 있습니다.

LiDAR은 ADAS의 중요한 구성 요소이며 고효율 VCSEL은 작은 풋 프린트, 매력적인 가격 설정, 탁월한 신뢰성 및 성능으로 ADAS LiDAR에 적합합니다. VCSEL은 물체 감지 및 거리 매핑을 위한 LiDAR 시스템, ADAS 및 자율 주행을 위한 차량 외부 감지 기술, 차량 내부 및 차량 외부용 차량 탑재 3D 감지 등에 사용됩니다.

LEVEL 4의 자율성을 실현하기 위해, 선진국과 신흥국 지역의 대부분이 신차에 ADAS 탑재를 의무화하거나 의무화할 예정이며, 시장 벤더에게 큰 성장 기회를 가져올 것으로 기대되고 있습니다. 예를 들어, 미국에서는 신차의 80-90%가 적어도 하나의 ADAS 기능을 탑재하고 있습니다.

National Safety Council에 따르면 2026년까지 등록 차량의 약 71%에 리어 카메라가 탑재되어 60%에 리어 파킹 센서가 탑재된다고 합니다. 이러한 ADAS의 채용 증가는 조사 대상 시장의 성장을 가속할 것으로 예상됩니다.

자동운전차와 자율주행차의 채용 증가는 ADAS 시장의 주요 성장 요인입니다. 예를 들어 인텔사에 따르면 세계 자동차 판매 대수는 2030년에 1억 140만대 이상에 이를 것으로 예상되고 있으며, 자율주행차는 2030년까지 자동차 등록 대수의 약 12%를 차지할 것으로 예상되고 있습니다.

아시아태평양은 중국이 시장을 독점하고 큰 성장이 예상됩니다.

아시아태평양에서는 자동차, 의료, 소비자 일렉트로닉스 산업에서 VCSEL 채용이 증가하고 있기 때문에 중국의 대폭적인 성장이 전망되고 있습니다.

중국은 세계에서 가장 유명한 소비자용 전자 기기 제조업체입니다. 이 지역에서는 제조업이 급성장하고 있으며 다양한 제조 기술과 통신 기술이 도입되고 있습니다.

세계의 다양한 전자기기가 중국에 계속 유입되고 있기 때문에 중국의 반도체 소비는 기타 국가보다 빠르게 성장하고 있습니다. 세계의 유명한 휴대전화 회사 상위 5개 중 3개사가 이 나라에 거점을 두고 있어 반도체를 채용하는 절호의 기회가 되고 있습니다.

중국 정부는 또한 시민을 추적하고 모니터링하기 위한 인공지능과 센서를 동력원으로 하는 테크노 오솔리티 국가의 창설에 임하고 있습니다. 이러한 프로그램은 이 나라에서 연구되는 시장 수요가 확대될 것으로 예상됩니다. 중국 정부의 '메이드 인 차이나 2025' 구상은 2030년까지 반도체 산업의 생산고를 3,050억 달러에 도달시켜 국내 수요의 80%를 충족하는 것을 목표로 하고 있습니다. 이러한 움직임은 일본 시장의 성장을 뒷받침할 것으로 추정됩니다.

대기업은 시장에서의 지위를 강화하기 위해 혁신적인 제품 개발에 주력하고 있습니다. 예를 들어, VCSEL 반도체 연구 개발의 선구자이자 고속 광통신용 VCSEL 및 3D 심도 카메라 제조업체인 Berxel Photonics는 2023년 9월 중국 심천에서 개최된 China International Optoelectronic Exposition에서 106Gbps VCSEL 탑재 800G 트랜시버의 라이브 데모를 발표했습니다.

VCSEL의 성장에 기여하는 또 다른 요인은 전기자동차 채택이 확대되고 있다는 것입니다. 예를 들어, 제스처 인식, 운전자 모니터링, 자율주행 센서 등의 용도로 자동차 산업에서 이 기술이 사용될 것으로 예상되고 있습니다. 이 지역에서는 자동차 산업이 훌륭한 속도로 성장하고 있습니다. 이 지역에서는 맞춤형 반도체 및 센서에 대한 수요가 증가하고 있습니다. 따라서 VCSEL 기술은 이 지역에서 중요한 역할을 할 것으로 기대됩니다. CAAM에 따르면 2023년 8월 중국에서 생산된 배터리 전기차는 58만 9,000대로, 그 중 승용 BEV가 55만 1,000대, 비즈니스 BEV가 3만 8,000대였습니다. 같은 달 중국에서는 25만 4,000대의 PHEV가 생산되었으며, 그 중 25만 3,000대가 승용 PHEV, 1,000대가 상용 PHEV였습니다.

중국 정부는 자동차 부품 부문을 포함한 자동차 산업을 기간 산업의 하나로 자리 매김하고 있습니다. 정부는 중국의 자동차 생산량이 2025년까지 3,500만 대에 달할 것으로 전망하고 있습니다. 이러한 사례는 시장이 예측 기간 동안 성장할 것으로 예상을 보여줍니다.

수직 공진기 면발광 레이저 산업 개요

VCSEL 시장은 Coherent Corporation, Lumentum Operations LLC, Vixar Inc(OSRAM AG), Hamamatsu Photonics KK, TRUMPF Group 등의 대기업이 존재하고 세분화되고 있습니다. 시장 진출기업은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 얻기 위해 제휴 및 인수와 같은 전략을 채택하고 있습니다.

2023년 10월-데이터 통신용 고속 VCSEL과 포토다이오드 솔루션의 세계 참가 기업인 트럼프 포토닉 컴포넌트사와 스페인에 본사를 둔 고속 광 네트워킹 솔루션의 전문가인 KDPOF는 글래스고에서 개최된 유럽 광통신 회의(ECOC)로 자동차 시스템을 위한 최초의 980nm 멀티 기가비트 상호 접속 시스템을 전시했습니다..

2023년 6월-세계 최고의 광학 솔루션 공급업체인 AMS Osram은 수직 공진기 면발광 레이저(VCSEL)의 TARA2,000-AUT-SAFE 제품군 출시를 발표했습니다. 자동차 실내 센싱용 적외선 레이저 모듈의 포트폴리오를 강화하면서 신뢰성이 높고 보다 견고한 아이 안전 기능을 기재하고 있습니다. 새로운 TARA2,000-AUT-SAFE는 940nm의 피크 파장에서 엄격하게 제어된 적외선 빔을 생성합니다. 드라이버 모니터링, 제스처 센싱, 차내 모니터링 등 기존의 TARA2,000-AUT 시리즈와 같은 용도 시나리오에 대응합니다. 이 컴팩트한 모듈에는 ams의 오스람 VCSEL 칩과 마이크로 렌즈 어레이(MLA)가 장착되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

시장 개요

산업의 매력-Porter's Five Forces 분석

공급기업의 협상력

구매자 및 소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

특허 상황

COVID-19의 부작용 및 기타 거시 경제 요인이 시장에 미치는 영향

제4장 시장 역학

시장 성장 촉진요인

데이터센터에서 VCSEL 채용 증가

스마트폰에서 3D 센싱 용도 수요 증가

시장 성장 억제요인

InP 기반 VCSEL의 보급률이 낮고 데이터 전송 범위가 좁음

제5장 재료 동향 분석

질화갈륨

갈륨비소

기타 재료 유형

제6장 시장 세분화

파장별

적색(650-750 nm)

근적외선(750-1,400 nm)

단파장 적외선(1,400-3,000 nm)

다이 사이즈별

0.02-0.06 mm2

0.06-0.4 mm2

0.4-1.3 mm2

10-75 mm2

최종 사용자 산업별

텔레콤

모바일 및 소비자

자동차

의료

산업

항공우주 및 방위

용도별

데이터콤

광학식 마우스

얼굴 인식 및 심도 카메라

제스처 인식

레이저 자동 초점

근접 센서

홍채 스캔

의료용

ADAS LiDAR

산업 용도

기타

지역별

북미

유럽

대만

중국

한국

일본

기타

제7장 경쟁 구도

기업 프로파일

Coherent Corporation

Lumentum Operations LLC

Vixar Inc(OSRAM AG)

Hamamatsu Photonics KK

TRUMPF Group

ams OSRAM AG

HLJ Technology Co. Ltd

Teledyne FLIR Systems Inc.

Vertilite Inc.

Leanardo Electronics US(Lasertel)

Broadcom Inc.

Santec Corporation

제8장 투자 분석

제9장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

The Vertical Cavity Surface Emitting Laser Market size is estimated at USD 2.49 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 18.6% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 5.14 billion units in 2025 to 16.06 billion units by 2030, at a CAGR of 25.60% during the forecast period (2025-2030).

The vertical-cavity surface-emitting laser (VCSEL) is a semiconductor whose laser is emitted perpendicular to the top surface. It differs from an edge-fired laser, which emits the laser from the edge. VCSELs offer precision, high efficiency, reliability, and high speed with a cost-effective solution, and these are the most promising new technological developments in laser physics. VCSELs offer various advantages, such as lower power consumption, beam quality, modulation speeds, and manufacturing costs.

Key Highlights

The VCSEL market is anticipated to witness robust growth during the forecast period owing to several factors like increasing requirements for transmitting data over long distances with high speed and efficiency, rising demand for these lasers in automotive LiDAR applications, and industrial applications. In August 2023, Innoviz Technologies and the BMW Group are expanding their collaboration by starting a B-sample development phase on a new generation of LiDAR.

Over the past few years, optical interconnect infrastructures in the data centers have advanced to the next-generation 400 Gbit/s data rate from 100 Gbit/s. This is primarily driven by the ever-increasing data traffic in data centers due to the rapid market growth of emerging technologies, such as AI, VR/AR, and the Internet of Things (IoT), and the introduction of 5G mobile network systems.

The increasing adoption of VCSELs in smartphones by smartphone manufacturers for 3D sensing or proximity sensing applications is one of the primary factors driving the market growth. The growth of 3D sensing was propelled by the introduction of face ID modules in iPhones. Since then, there have been significant developments in 3D sensing. Slowly, there was a transition of 3D sensing from front-side face ID modules to the rear side for photography applications.

InP-based VCSELs are typically preferred for applications such as optical communication due to their low dispersion and low fiber loss. However, InP-based VSCELs cannot provide large refractive index contrast DBR mirrors, owing to the high reflectivity and low penetration depth. The effective cavity length limits the tuning range and the confinement factor.

The COVID-19 pandemic had a remarkable impact on the market studied, with several end-user industries that deploy VCSEL facing several difficulties. The industries were stuck with nationwide lockdowns, which brought them to a standstill, but after Q2 of 2020, they gradually started their operation. Since the raw materials are bought in China, the sourcing has been affected by the tariffs imposed by the United States.

Geopolitical tensions and conflicts worldwide drive the demand for military spending. According to the Stockholm International Peace Research Institute (SIPRI), the United States led the ranking of countries with the highest military expenditure in 2022, with USD 877 billion dedicated to the military. That constituted nearly 40 percent of the total military spending worldwide that year, which amounted to USD 2.2 trillion. This amounted to 3.5 percent of the US gross domestic product.

ADAS and LiDAR to be the Fastest-growing Application

The automotive industry is one of the major emerging markets for the VCSEL manufacturers, owing to trends like autonomous vehicles and high-end interior features in vehicles. Although the automotive industry has been witnessing a recession in recent years, the growing number of sensors per vehicle is mainly motivating the market vendors. Most of the market vendors are expanding their scope for the automotive market (interior and exterior applications).

LiDAR is a critical component of ADAS, and highly efficient VCSELs, with their tiny footprint, attractive pricing, and remarkable reliability and performance, are making them suitable for ADAS LIDAR. VCSELs are used in LiDAR systems for object detection and mapping distances, exterior sensing technologies for ADAS and autonomous driving, and automotive 3D sensing for in-cabin and outside the vehicle, among others.

In order to achieve LEVEL 4 autonomy, most of the developed and developing regions have mandated or are planning to mandate ADAS in new vehicles, which is expected to create massive growth opportunities for the market vendors. For instance, 80-90% of new vehicles in the United States have at least one ADAS feature.

According to the National Safety Council, by 2026, approximately 71% of registered vehicles will be equipped with rear cameras, while 60% will have rear parking sensors. Such increasing adoption of ADAS would aid the growth of the market studied.

The increasing adoption of self-driving or autonomous vehicles is a primary growth factor for the ADAS market. For instance, according to Intel, global car sales are expected to reach over 101.4 million units in 2030, and autonomous vehicles are expected to account for about 12% of car registrations by 2030.

Asia-Pacific Expected to Witness Significant Growth with China Dominating the Market

China is expected to grow substantially in the Asia-Pacific region due to the increasing adoption of VCSEL in the automotive, healthcare, and consumer electronics industries.

China is one of the prominent consumer electronics producers across the world. The manufacturing industry is rapidly growing in the region and is witnessing the deployment of various manufacturing and telecommunications technologies, which is expected to aid in the market's growth.

Due to the continued flow of global, diversified electronics equipment into China, the consumption of semiconductors in China is growing faster than in others. Three of the world's top five most prominent mobile phone companies are based in this country, which presents enormous opportunities for adopting semiconductors.

The Chinese government is also working to create a techno-authoritarian state powered by artificial intelligence and sensors to track and monitor its citizens. The demand for market studied in the country is expected to grow with such programs. The Chinese government's "Made in China 2025" initiative aims to make its semiconductor industry reach USD 305 billion in output by 2030 and meet 80% of domestic demand. Such instances are estimated to boost the market's growth in the country.

Major players focus on developing innovative products to strengthen their market positions. For instance, in September 2023, Berxel Photonics, a pioneer in VCSEL semiconductor R&D and manufacturer of high-speed optical communications VCSELs and 3D depth cameras, announced a live demo of its 106 Gbps VCSEL-powered 800G transceiver in China International Optoelectronic Exposition in Shenzhen, China.

Another factor contributing to the growth of VCSEL is the growing adoption of electric vehicles. For example, this technology is anticipated to be used in the vehicle industry for applications like recognition of gestures, driver monitoring, and autonomous driving sensors. In this region, the auto industry is growing at an excellent rate. The demand for custom semiconductors and sensors is increasing in the area. Therefore, VCSEL technology is expected to play a significant role in the region. As per CAAM, 589,000 battery-electric vehicles were made in China in August 2023, with 551,000 passenger BEVs and 38,000 business BEVs. In the same month, 254,000 PHEVs were produced in China, of which 253,000 were passenger PHEVs, and 1,000 were commercial PHEVs.

The Chinese government views its automotive industry, including the auto parts sector, as one of its pillar industries. The government expects China's automobile output to reach 35 million units by 2025. Such instances show that the market is anticipated to grow over the forecast period.

Vertical Cavity Surface Emitting Laser Industry Overview

The VCSEL market is fragmented with the presence of major players like Coherent Corporation, Lumentum Operations LLC, Vixar Inc (OSRAM AG), Hamamatsu Photonics KK, and TRUMPF Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

October 2023 - TRUMPF Photonic Components, a global player in high-speed VCSEL and photodiode solutions for data communication, and KDPOF, an expert in high-speed optical networking solutions based in Spain, showcased its first 980nm multi-gigabit interconnect system for automotive systems at the European Conference for Optical Communication (ECOC), held in Glasgow.

June 2023 - AMS Osram, the world's significant supplier of optical solutions, announced the launch of the TARA2000-AUT-SAFE family of vertical cavity surface emitting lasers (VCSELs), Reliable and more robust eye safety features while enhancing the portfolio of infrared laser modules for automotive in-cabin sensing. The new TARA2000-AUT-SAFE generates a tightly controlled beam of infrared light at a peak wavelength of 940nm. It suits the same application scenarios as the existing TARA2000-AUT series: driver monitoring, gesture sensing, and in-cabin monitoring. The compact module contains an ams Osram VCSEL chip and a microlens array (MLA).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

3.1 Market Overview

3.2 Industry Attractiveness - Porter's Five Forces Analysis

3.2.1 Bargaining Power of Suppliers

3.2.2 Bargaining Power of Buyers/Consumers

3.2.3 Threat of New Entrants

3.2.4 Threat of Substitute Products and Services

3.2.5 Intensity of Competitive Rivalry

3.3 Patent Landscape

3.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Increasing Adoption of VCSEL in Data Centers

4.1.2 Growing Demand for 3D Sensing Applications in Smartphones

4.2 Market Restraints

4.2.1 Low Penetration of InP-based VCSELs and Limited Data Transmission Range