중국의 유기질 비료 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

China Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683191

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

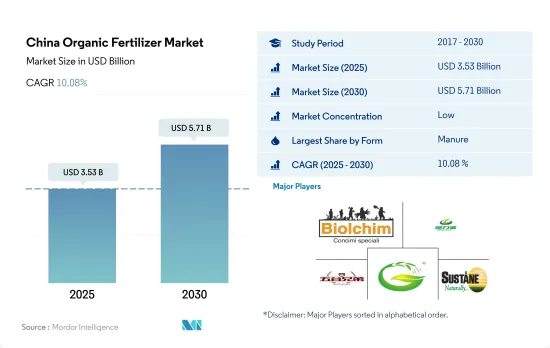

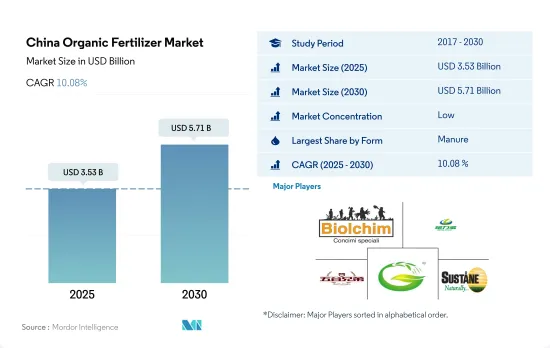

중국의 유기질 비료 시장 규모는 2025년에 35억 3,000만 달러, 2030년에는 57억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 10.08%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

2022년 중국 전체 농업 생물학적 제제 시장에서 유기질 비료가 70.6%로 가장 큰 점유율을 차지했습니다. 유기질 비료의 우위는 주로 유기농업과 관행농업 모두에 대량으로 적용되기 때문입니다.

중국 전체 유기농 재배 면적은 2017년 190만 헥타르에서 2022년 250만 헥타르로 증가했습니다. 이러한 전체 유기농 작물 재배면적 증가 추세는 시장을 견인할 가능성이 있습니다. 시장 가치는 약 75.6% 증가하여 2029년에는 51억 9,000만 달러에 달할 것으로 예상됩니다.

중국의 유기질 비료 시장은 퇴비가 지배적이며, 2022년 시장 규모는 14억 2,000만 달러에 달했습니다. 퇴비는 전통적으로 유기 재배와 비유기 재배 모두에서 기초 비료로 사용되며, 토양 내 유기물과 탄소 함량을 증가시키는 것으로 알려져 있습니다. 그 뒤를 이어 피쉬 구아노, 박쥐 구아노, 피쉬 에멀젼, 버미컴포스트, 당밀, 기타 퇴비 등 기타 유기질 비료가 뒤를 잇고 있습니다. 기타 유기질 비료는 2022년 약 8억 3,220만 달러로 평가되었습니다.

중국 정부는 생태문명 건설, 공급측 구조개혁, 농촌 활성화 전략 등 다양한 규제와 정책을 도입했습니다. 이러한 규제는 유기농업의 기본적 사고와 개념과 매우 일치합니다.

지역 유기농업의 발전도 각급 지자체에서 계획하고 있습니다. 또한, 생산자들이 유기농업으로 전환하도록 장려하는 인센티브도 도입되고 있습니다. 이러한 요인들은 2023년부터 2029년까지 중국의 유기질 비료 시장을 더욱 견인할 것으로 보입니다.

중국 유기질 비료 시장 동향

농약 사용량 제로 성장과 유기농 제품 수출 증가로 유기농 재배 촉진

FiBL과 IFOAM의 최신 보고서에 따르면 중국의 유기농 식품 시장은 연간 25.0%의 성장률을 보이고 있습니다. 관행농법에서 유기농법으로의 전환은 중국에서 매년 29억 1,000만 달러의 농산식품이 수출되는 것을 감안할 때, 중국 내에서 보다 지속 가능한 식품 시스템으로의 전환입니다.

중국에서 유기농 농지 면적이 급증한 것은 소득 증가와 식품 안전에 대한 중요성이 높아지면서 더 많은 사람들이 유기농 제품을 구매하게 되었기 때문입니다. 지난 3년 동안 중국의 유기농 재배 면적은 10% 증가하여 2020년에는 240만 헥타르에 달했습니다. 유기농 생산을 촉진하기 위해 국가 정책이 채택되었고, "맑은 물과 푸른 산은 대체할 수 없는 자산이다", "녹색 발전"이라는 슬로건을 내세웠습니다.

중국의 유기농업은 주로 수출 지향적입니다. 수출과 수입을 모두 하는 것은 곡물, 콩, 과일, 과일, 그리고 일부 채소입니다. 중국의 동북 3성인 랴오닝성, 지린성, 헤이룽장성은 생산량, 수량, 면적 면에서 전국 최대의 유기농 생산을 뒷받침하고 있습니다. 중국 북부(산둥성, 랴오닝성 등)에 위치한 대부분의 유기농 농장은 유기농 야채와 과일을 인근 도시에 공급하고 있습니다. 또한 일본, 한국, 유럽, 미국으로 수출하는 제품도 있습니다.

화학 합성 비료와 농약의 과다 사용으로 인한 토양 독성에 대한 우려가 커지면서 중국에서는 지속 가능한 농업 관행과 유기농 식품 생산에 대한 수요가 증가하고 있습니다. 이는 재배 방법의 전환을 서서히 둔화시키면서 증가시킬 것으로 보입니다. 또한, 작물 영양 및 보호 제품에 대한 수요도 증가할 것입니다.

유기농 제품에 대한 수요가 증가함에 따라 중국 소비자의 약 73%가 유기농 식품을 먹기를 원하고 있습니다.

중국의 유기농 식품 시장은 빠르게 발전하고 있으며, 중국 소비자의 유기농 식품에 대한 잠재적 수요는 엄청나다. 그 배경에는 부유한 중산층 증가와 건강에 미치는 영향에 대한 인식이 높아지면서 2021년 중국 유기농 식품 매출은 약 775억 4,000만 달러에 달했습니다.

식품의 안전성보다 유기농 식품을 우대하는 정부의 각종 법규와 기존 식품보다 유기농 식품을 선호하는 소비자들의 기호로 인해 유기농 식품에 대한 수요가 크게 확대되었습니다. 중국 내 유기농 채소 가격은 관행 농산물의 3-15배인 반면, 유기농 채소의 가격은 일반적으로 관행 농산물의 5-10배에 달할 전망입니다. 그러나 가격적 요인에도 불구하고 부유한 가정과 건강 문제가 있는 개인은 예산을 늘리고 싶어하며, 중국 소비자의 약 73%는 유기농 식품에 대한 추가 비용을 지불할 의향이 있습니다.

중국 정부는 점차 유기농 식품 분야의 자립을 목표로 하고 있습니다. 예를 들어, 농부들이 화학비료 사용을 줄이고 바이오 대체품으로 전환하도록 장려함으로써 경제는 점차 친환경 농업으로 전환하고 있으며, 2020년 중국 체인점 프랜차이즈 협회(CCFA)의 조사에 따르면, 지속 가능한 식품 생산의 개념을 이해하는 선진 도시 중국인의 유기농에 대한 인식이 83%에 달한다고 발표했습니다. 중국의 유기농 식품 부문은 아직 규모가 매우 작아 국내외 소비자 수요를 충족시키기에는 아직 멀었지만 2021년 국내 매출이 4.01% 증가할 것이라는 점을 감안할 때 중국 유기농 식품은 국내 시장과 해외 시장에서 엄청난 잠재력을 가지고 있다고 할 수 있습니다.

중국 유기질 비료 산업 개요

중국 유기질 비료 시장은 세분화되어 있으며, 상위 5개 기업이 0.20%를 차지하고 있습니다. 이 시장의 주요 기업은 다음과 같습니다. Biolchim SPA, Genliduo Bio-tech Corporation Ltd, Hebei Woze Wufeng Biological Technology, Qingdao Future Group, Sustane Natural Fertilizer Inc. 알파벳순으로 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

유기재배 면적

1인당 오가닉 제품에 대한 지출

규제 프레임워크

중국

밸류체인과 유통 채널 분석

제5장 시장 세분화

형태별

비료

밀(Meal) 기반 비료

오일 케이크

기타 유기질 비료

작물 유형별

환금 작물

원예 작물

밭작물

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 개요(세계 레벨 개요, 시장 레벨 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 랭크, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함).

The China Organic Fertilizer Market size is estimated at 3.53 billion USD in 2025, and is expected to reach 5.71 billion USD by 2030, growing at a CAGR of 10.08% during the forecast period (2025-2030).

Organic fertilizers held the maximum market share of 70.6% of the total Chinese agricultural biologicals market in 2022. The dominance of organic fertilizers is mainly due to their application in bulk quantities both in organic and conventional farming.

The overall organic area in the country increased from 1.9 million hectares in 2017 to 2.5 million hectares in 2022. This increasing trend in the overall organic crop area may drive the market. The market value is anticipated to increase by about 75.6% and reach USD 5.19 billion by 2029.

Manures dominate the organic fertilizer market in the country, which was valued at USD 1.42 billion in 2022. Manure is conventionally used as a basic fertilizer both in organic and non-organic cultivation and is known to increase organic matter and carbon content in the soil, which would increase the nutrient uptake of the crop and, thus, the grain yield. This is followed by other organic fertilizers, which include fertilizers like Fish Guano, Bat Guano, fish emulsion, vermicompost, molasses, and other composted fertilizers. Other organic fertilizers were valued at about USD 832.2 million in 2022.

The Chinese government introduced a variety of regulations and policies to the construction of ecological civilization, supply-side structural reform, rural revitalization strategy, etc. These regulations are very much in line with the fundamental ideas and concepts of organic farming.

The development of local organic agriculture has also been planned by municipal governments at all levels. They have also introduced incentives to encourage producers to switch to organic farming. These factors may further drive the organic fertilizer market in the country between 2023 and 2029.

China Organic Fertilizer Market Trends

Country's zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

According to the latest reports by FiBL and IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million hectares in 2020. National policies have been adopted to promote organic production, advocating the slogans that state, "lucid waters and lush mountains are invaluable assets" and "green development".

Organic farming in China is majorly export-oriented. The products that are both exported and imported are cereals, soybeans, and fruits, followed by some vegetables. Liaoning, Jilin, and Heilongjiang, China's three northeastern provinces, support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in northern China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides, which lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This would moderately slow down yet increase the shift in cultivation practices. It also subsequently increases the demand for crop nutrition and protection products.

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China were about USD 77.54 billion.

Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 to 10 times the prices of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

China Organic Fertilizer Industry Overview

The China Organic Fertilizer Market is fragmented, with the top five companies occupying 0.20%. The major players in this market are Biolchim SPA, Genliduo Bio-tech Corporation Ltd, Hebei Woze Wufeng Biological Technology Co. Ltd, Qingdao Future Group and Sustane Natural Fertilizer Inc. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Area Under Organic Cultivation

4.2 Per Capita Spending On Organic Products

4.3 Regulatory Framework

4.3.1 China

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Form

5.1.1 Manure

5.1.2 Meal Based Fertilizers

5.1.3 Oilcakes

5.1.4 Other Organic Fertilizers

5.2 Crop Type

5.2.1 Cash Crops

5.2.2 Horticultural Crops

5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).