전략적 광물 재료 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Strategic Mineral Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683181

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

전략적 광물 재료 시장은 예측기간 동안 5% 이상의 CAGR로 추이할 전망

주요 하이라이트

이에 반해 COVID-19 팬데믹의 영향과 채굴 작업에 대한 환경문제 증가가 시장 성장을 방해할 것으로 예측됩니다.

다양한 전략적 광물의 용도 기반이 증가하고 있는 것은 미래에 호기로서 작용할 것으로 예측됩니다.

아시아태평양이 시장을 독점하고 가장 큰 소비국은 중국, 이어 인도, 한국, 일본입니다.

전략적 광물 재료 시장 동향

철강 용도가 니오븀 부문을 지배합니다.

일반적으로, 철강의 특성은 탄소, 망간, 인, 실리콘, 합금 원소, 미세 합금 원소에 관한 화학 조성 및 가공 조건에 의해 결정됩니다. 일반적으로 강철의 강도를 높이는 가장 쉬운 방법은 탄소 함량을 높이는 것입니다. 그러나 이것은 용접성, 인성, 성형성 등 다른 필요한 특성에 부정적인 영향을 미칩니다.

그러나, 니오븀은 탄소와 친화성이 높고, 탄화물이나 탄질화물을 형성하기 때문에 철강이나 스테인리스에 페로니오븀이라고 하는 형태로 첨가해, 균형 잡힌 특성을 유지하는 경우가 많습니다. 그 결과 마이크로 합금 강 제품으로 알려져 있으며 일반적으로 약 0.1 중량%의 니오븀을 포함하며 종종 티타늄과 바나듐과 함께 사용됩니다.

HSLA강의 경우, 니오븀은 합금 전체의 0.1% 이하인 경우가 많지만, 결정립 미세화제로서의 역할은 강의 강도, 용접성, 연성, 인성을 향상시켜 큰 차이를 가져옵니다. 저급강의 강도는 결정립의 미세화에 의해 생성되고, 고급강의 강도는 결정립의 미세화와 석출 경화의 조합에 의해 만들어집니다.

저급강의 강도는 결정립의 미세화에 의해 고급강의 강도는 결정립의 미세화와 석출 경화의 조합에 의해 만들어집니다. 니오븀과 티타늄은 탄소나 질소와 같은 개재 원소를 고정하기 때문에 이들 강은 개재 원소 프리로 표현됩니다.

그러나 최상의 결과는 일반적으로 시너지 이점을 이용한 미세 합금의 조합에 의해 달성됩니다. 이 예는 우수한 표면 품질이 필수적인 '노출된' 무기질 강철 자동차 부품에 니오븀과 티타늄을 병용하는 것을 포함합니다.

최신 HSLA 강철의 대부분은 이 '저탄소' 범주에 속합니다. 전 세계적으로 니오븀 제품의 90%가 철강 산업에서 사용되고 있습니다.

고강도 저합금(HSLA) 강에서 니오븀의 가장 큰 용도는 자동차, 석유 파이프라인, 건설용입니다. HSLA강은 원자로(지르코늄과 합금화하여 노심 엘리먼트를 만든다), 풍력 터빈, 철도 선로, 조선에도 사용되고 있습니다. HSLA 스틸은 연간 니오븀 생산량의 약 90%를 소비합니다.

니오븀 철은 철강 산업에서 가장 널리 사용되는 제품이며 주로 파이프라인, 자동차, 구조물 및 스테인레스 스틸의 4 부문으로 사용됩니다. 파이프라인 산업에 관해서는 중국에서의 용도는 세계 기타 지역과 거의 동일하지만, 자동차 강재, 구조 강재, 스테인리스재 산업에서의 용도에는 큰 차이가 있습니다.

아시아태평양이 시장을 독점

아시아태평양은 세계 시장을 독점하고 있습니다. 중국, 인도, 한국, 일본 등의 국가에서는 다양한 용도로 다양한 광물의 이용이 가속화되고 있으며, 예측 기간 동안 이 시장은 큰 성장을 이룰 가능성이 높습니다. 아시아태평양의 전기 및 전자산업(반도체와 통신 포함)은 인도나 중국과 같은 국가들로부터 높은 수요 덕분에 최근 급속히 성장했습니다. 전자 산업에서의 기술 혁신의 급속한 속도, 기술 진보 및 연구 개발 활동은 최신 전자 제품에 대한 수요가 높습니다. 고급 제품에 특화된 제조 공장 및 개발 센터의 수가 증가하고 있습니다. 항공우주는 전략적 광물 재료의 또 다른 주요 최종 사용자 산업입니다. 항공기 수요는 세계적으로 증가하고 있으며, 항공우주 산업은 제조시간 개선과 비용 절감을 위한 혁신적인 솔루션의 도입을 목표로 하고 있습니다. 따라서 앞서 언급한 요인은 예측 기간 동안 다양한 용도로부터 전략적 광물 재료의 사용을 가속화하고 있습니다. 하지만 2020년에도 경제적 성과와 수요는 이 지역의 현재 COVID-19 팬데믹의 영향을 받을 가능성이 높기 때문에 수요는 영향을 받을 가능성이 높습니다.

전략적 광물 재료 산업 개요

세계의 전략적 광물 재료 시장은 다양한 광물을 다루는 수많은 기업들이 존재하기 때문에 그 특성상 세분화되고 있습니다. 시장의 유명한 기업으로는 Intercontinental Mining, Vale, Anglo American plc, Glencore, CBMM, Materion Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

다양한 최종 사용자 산업에서 수요 증가

기타 촉진요인

성장 억제요인

COVID-19 팬데믹의 영향

채굴 작업에 대한 환경 문제 증가

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

미네랄별

안티몬

난연제

배터리

세라믹 및 유리

촉매

합금

발라이트

석유 및 가스

기타 용도(도료, 화학제조, 기타)

베릴륨

일렉트로닉스

항공우주

자동차

에너지

기타

코발트

배터리

초합금

초경합금 및 다이아몬드 공구

촉매

기타

형석

화학제품

철강

알루미늄

시멘트

기타

갈륨

집적회로

레이저 다이오드

수광소자

태양전지

기타

게르마늄

섬유 광학

적외선 광학 부품

촉매

전기 및 솔러 기기

기타

인듐

플랫 패널 디스플레이 화면 및 터치스크린

저융점 합금 및 땜납

반도체

투명 열반사판

기타

망간

주조 합금

포장

수송

건축

기타

니오븀

철강

초합금

초전도 마그넷

커패시터

유리

기타

백금족 원소

자가촉매

보석 장식

전기 및 전자

화학

기타

희토류

촉매

배터리

자성 합금

야금

기타

탄탈

일렉트로닉스

의료

항공우주

자동차

기타

지역별

아시아태평양

중국

인도

일본

한국

ASEAN 국가

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Anglo American plc

CBMM

Glencore

Indium Corporation

Intercontinental Mining

Materion Corporation

South32

Vale

WARRIOR GOLD INC.

제7장 시장 기회 및 향후 동향

각종 광물의 용도 확대

AJY

영문 목차

영문목차

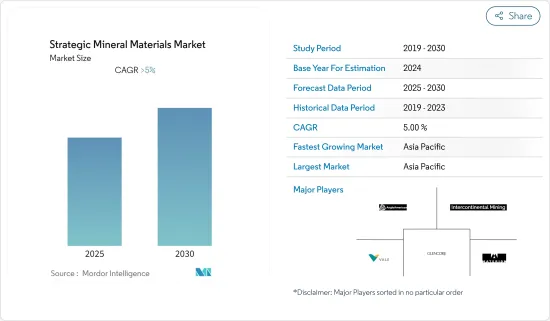

The Strategic Mineral Materials Market is expected to register a CAGR of greater than 5% during the forecast period.

Key Highlights

On the flipside, the impact of COVID-19 pandemic and increasing environmental concerns regarding mining operations is expected to hinder the growth of the market.

Increasing application base for various strategic minerals is projected to act as an opportunity in the future.

Asia-Pacific dominated the market with the largest consumption coming from China, followed by India, South Korea, and Japan.

Strategic Mineral Materials Market Trends

Steel Application to Dominate the Niobium Segment

In general, the properties of steel depend on its chemical composition concerning carbon, manganese, phosphorus, silicon, alloying and micro-alloying elements, and processing conditions. Generally, the easiest way to increase the strength of steel is improving its carbon content. But this adversely affects other necessary properties, such as weldability, toughness, and formability.

However, niobium has a high affinity for carbon, forming carbides and carbon nitrides, therefore, it is often added to steel and stainless steel in the form of ferro-niobium to maintain a balanced package of properties, the carbon and niobium levels being carefully matched with processing conditions to achieve the desired properties. The result, known as a micro-alloyed steel product, typically contains around 0.1% niobium by weight, often in conjunction with titanium and vanadium.

In HSLA steel niobium is often less than 0.1% of the total alloy, but its role as a grain refiner makes a significant difference by increasing strength, weldability, ductility, and toughness of the steel. Strength is generated by grain refinement for the lower grades and a combination of grain refinement and precipitation hardening for the higher grades.

Strength is generated by grain refinement for the lower grades and a combination of grain refinement and precipitation hardening for the higher grades. These steels are described as interstitial-free, since niobium and titanium fix interstitial elements, like carbon and nitrogen.

However, the best results are usually achieved with a combination of micro alloys that exploit synergistic benefits. An example of this is the use of niobium and titanium together in 'exposed' interstitial-free steel automobile parts where superior surface quality is essential.

Most modern HSLA steels fall into this 'low carbon' category. Globally, 90% of the niobium products are used in the steel industry.

The largest use for niobium in high-strength and low-alloy (HSLA) steel is for automobiles, oil pipelines, and construction. HSLA steels are also used in nuclear reactors (alloyed with zirconium to make core elements), wind turbines, railroad tracks, and in ship building. HSLA steels consume approximately 90% of the annual niobium production.

Ferro niobium is the most widely used product in the steel industry, which is mainly applied in four fields of the pipeline, automobile, structure, and stainless steel. As for the pipeline industry, the application in China is in line with that in the other parts of the world, but the difference is significant in the application in automotive steel, structural steel, and stainless steel industries.

Asia-Pacific to Dominate the Market

Asia-Pacific dominated the global market. With accelerating usage of various minerals in different applications in countries, such as China, India, South Korea, and Japan, the market studied is likley to witness significant growth during the forecast period. The Asia-Pacific electrical and electronics industry (including semiconductors and telecommunications) grew rapidly in the recent past, owing to the high demand from countries, like India and China. There is a high demand for modern electronic products, due to the rapid pace of innovation, the advancement of technology, and R&D activities in the electronics industry. There is a growth in the number of manufacturing plants and development centers, focusing on high-end products. Aerospace is the another major end-user industry for strategic mineral materials. The demand for aircraft is increasing across the world, and the aerospace industry is aiming to introduce innovative solutions to improve the manufacturing time and save costs. Therefore, the aforementioned factors are accelerating the usage of strategic mineral materials from various applications during the forecast period. However, the demand is likely to be affected during 2020 as well, as economic performance and demand are likely to remain affected by the current COVID-19 pandemic in the region.

Strategic Mineral Materials Industry Overview

The global strategic mineral materials market is fragmented in nature with the presence of numerous players for different minerals. The prominent companies in the market includes Intercontinental Mining, Vale, Anglo American plc, Glencore, CBMM, and Materion Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from Various End-user Industries

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Impact of COVID-19 Pandemic

4.2.2 Growing Environmental Concerns over Mining Operations

4.3 Industry Value-chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION

5.1 Mineral

5.1.1 Antimony

5.1.1.1 Flame Retardants

5.1.1.2 Batteries

5.1.1.3 Ceramics and Glass

5.1.1.4 Catalyst

5.1.1.5 Alloys

5.1.2 Barite

5.1.2.1 Oil and Gas

5.1.2.2 Other Applications (paints, chemical manufacturing and others)

5.1.3 Beryllium

5.1.3.1 Electronics

5.1.3.2 Aerospace

5.1.3.3 Automotive

5.1.3.4 Energy

5.1.3.5 Other Applications

5.1.4 Cobalt

5.1.4.1 Batteries

5.1.4.2 Superalloys

5.1.4.3 Cemented Carbides and Diamond Tools

5.1.4.4 Catalysts

5.1.4.5 Other Applications

5.1.5 Fluorspar

5.1.5.1 Chemicals

5.1.5.2 Steel

5.1.5.3 Aluminum

5.1.5.4 Cement

5.1.5.5 Other Applications

5.1.6 Gallium

5.1.6.1 Integrated Circuits

5.1.6.2 Laser diodes

5.1.6.3 Photodetectors

5.1.6.4 Solar Cells

5.1.6.5 Other Applications

5.1.7 Germanium

5.1.7.1 Fiber Optics

5.1.7.2 Infrared Optics

5.1.7.3 Catalyst

5.1.7.4 Electrical and Solar Equipment

5.1.7.5 Other Applications

5.1.8 Indium

5.1.8.1 Flat-Panel Display Screens and Touchscreens

5.1.8.2 Low Melting Alloys and Solders

5.1.8.3 Semiconductors

5.1.8.4 Transparent Heat Reflectors

5.1.8.5 Other Applications

5.1.9 Manganese

5.1.9.1 Casting Alloys

5.1.9.2 Packaging

5.1.9.3 Transportation

5.1.9.4 Construction

5.1.9.5 Other Applications

5.1.10 Niobium

5.1.10.1 Steel

5.1.10.2 Super Alloys

5.1.10.3 Superconducting Magnets

5.1.10.4 Capacitors

5.1.10.5 Glass

5.1.10.6 Other Applications

5.1.11 Platinum Group Elements

5.1.11.1 Autocatalyst

5.1.11.2 Jewelry

5.1.11.3 Electrical & Electronics

5.1.11.4 Chemical

5.1.11.5 Other Applications

5.1.12 Rare Earth Elements

5.1.12.1 Catalyst

5.1.12.2 Batteries

5.1.12.3 Magnetic Alloys

5.1.12.4 Metallurgy

5.1.12.5 Other Applications

5.1.13 Tantalum

5.1.13.1 Electronics

5.1.13.2 Medical

5.1.13.3 Aerospace

5.1.13.4 Automotive

5.1.13.5 Other Applications

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 ASEAN Countries

5.2.1.6 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Spain

5.2.3.6 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers & Acquisitions, Joint Ventures, Collaborations and Agreements

6.2 Market Share/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Anglo American plc

6.4.2 CBMM

6.4.3 Glencore

6.4.4 Indium Corporation

6.4.5 Intercontinental Mining

6.4.6 Materion Corporation

6.4.7 South32

6.4.8 Vale

6.4.9 WARRIOR GOLD INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Application base of Various Minerals