아프리카의 작물 보호 화학제품 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Africa Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683131

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

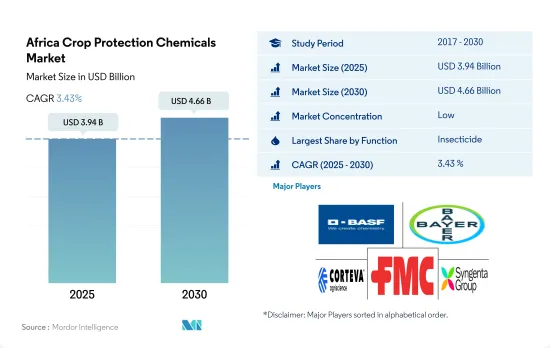

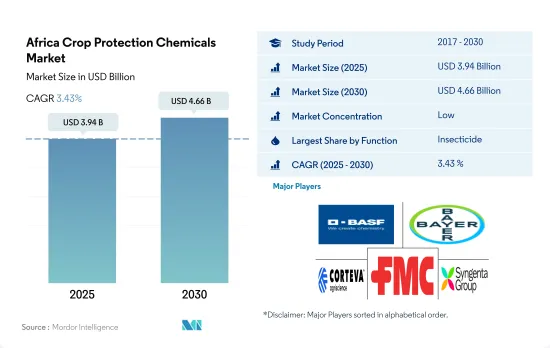

아프리카의 작물 보호 화학제품 시장 규모는 2025년에 39억 4,000만 달러로 추정되고, 2030년에는 46억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR은 3.43%로 성장할 전망입니다.

살충제가 아프리카 작물 보호 화학 시장을 독점

농업은 아프리카의 주요 부문 중 하나입니다. 이 부문은 증가하는 인구의 식량 안보 요구를 충족시키고 지역 경제 성장에 기여합니다. 이 지역의 다양한 기후 조건은 밀, 옥수수, 쌀, 콩, 해바라기, 콩류, 담배, 커피, 코코아, 차 등 다양한 작물에 유리합니다.

살충제는 아프리카의 작물 보호 화학제품 시장을 독점했으며 2022년에는 41.7%의 점유율을 차지했습니다. Centre for Agriculture and Biosciences International에 따르면, 아프리카 국가에서 곤충에 의한 작물 손실은 매년 예상되는 작물 총 수율의 49.0%로 추정됩니다. 그러나 농작물의 손실은 더욱 악화될 수 있으며 기후 변화의 영향으로 곤충에 의한 피해가 확대될 것으로 예상됩니다. 줄기류, 엽식 벌레, 참새 귀리, 진딧물, 엉겅퀴, 요코바이, 코나지라미, 카이가람시는 이 지역에서 경제적인 수율 손실을 초래하는 주요 해충입니다.

제초제는 아프리카에서 두 번째로 많이 사용되는 작물 보호제로 2022년 시장 점유율은 30.7%였습니다. 이 지역에서는 잡초의 만연으로 매년 평균 25-100%의 작물 손실이 발생하고 있습니다. 동시에, 이 지역은 증가하는 인구의 식량 수요를 충족시키기 위해 집약적인 농법을 실시하고 있으며, 이는 다양한 잡초 종의 만연을 조장하고 있습니다. 과거 기간 동안 제초제 소비량은 상당한 성장을 보였으며 2017년부터 2022년까지 사용량은 8,264톤 증가했습니다.

인구 증가, 경지 면적 감소, 식량 안보 향상이 이 지역 시장 성장 촉진요인이며 예측 기간 중 CAGR은 3.6%로 예측됩니다.

해충 및 잡초로부터 작물을 보호하기 위한 농약 소비 증가로 시장은 성장

아프리카에서는 해충, 질병, 잡초로부터 작물을 보호하기 위해 농약에 대한 수요가 증가하고 있습니다. 이 지역의 농업 종사자들은 해충과 병해충의 만연이 작물에 상당한 손해와 손실을 초래할 수 있기 때문에 이러한 화학 물질에 크게 의존합니다.

추잠의 확산은 약 50억 달러에 해당하는 1,600만 톤의 옥수수 부족으로 이어질 수 있습니다. 국제농업생물과학센터에 따르면 이 추잠이 제대로 방제되지 않으면 아프리카의 주요 옥수수 생산국 중 12개국에서 연간 830만 톤에서 2060만 톤의 손실을 일으킬 수 있다고 합니다.

아프리카에서는 카사바, 고구마, 감자, 야마이모 등의 근채류가 2,300만 헥타르의 땅에서 재배되고 있습니다. 카사바는 5억 명에서 10억 명의 아프리카인들이 소비하고 있지만 해충과 질병에 약합니다. 카사바 모자이크 바이러스와 카사바 갈조병은 이 작물에 영향을 미치는 가장 중요한 질병입니다. 아프리카 동부와 중부 아프리카의 연간 경제 손실은 19억-27억 달러로 추정됩니다.

이 나라에서 재배되는 가장 중요한 식용 작물은 옥수수, 쌀, 밀, 설탕입니다. 그 중에서도 옥수수는 가장 널리 재배되는 곡물입니다. 옥수수는 Chilo partellus Swinhoe와 같은 해충에 매우 약하며 연간 15%에서 100%까지 상당한 수율 감소를 일으킬 수 있습니다. 사실 아프리카 동부의 농업 종사자들은 칠로 파르테루스만이 최대 4억 5,000만 달러의 생산 손실을 보고했습니다. 이러한 요인은 농약 소비를 촉진하고 작물 보호 화학 시장은 예측 기간 동안 CAGR 3.6%를 나타낼 것으로 예상됩니다.

아프리카 작물 보호 화학제품 시장 동향

IPM 전략이나 윤작과 같은 다른 대체 방법의 채택으로 헥타르 당 농약 소비량이 크게 감소

과거 기간 동안 아프리카에서는 헥타르 당 농약 소비량이 현저히 감소했습니다. 2017년 농약 소비량은 1ha 당 1,175G였습니다. 그러나, 그 후의 노력에 의해 1헥타르당 96g의 삭감에 성공해, 현재의 1헥타르당 1,079g이 되고 있습니다. 이 농약 사용량의 대폭적인 삭감은 지속가능하고 친환경적 방법을 우선한 개량형 농업의 실시 등 다양한 요인이 겹쳤기 때문입니다. 농업 종사자들은 종합적 병해충 관리, 윤작, 생물학적 해충 방제 등의 혁신적인 기술을 점차 채용하고 있으며, 헥타르당 화학농약 사용량을 최소화하고 있습니다.

제초제는 이 지역에서 주로 이용되고 있는 농약 제품이지만, 최근, 1헥타르당의 제초제 소비량은 2017년에 비해 2022년에는 34g으로 대폭 감소하고 있습니다. 이 제초제 소비량의 상당한 감소는 종합적인 잡초 관리(IWM) 기술의 성공으로 인한 것입니다. 이 방법에서 농업 종사자는 다양한 작제 체계, 기계적 제초, 윤작, 피복 작물의 이용 등 다양한 혁신적 전략을 채택하고 있습니다. 이러한 친환경 기술은 제초제에 대한 의존도를 낮추고 지속 가능한 농업을 촉진하고 토양의 건전성을 높이고 생물 다양성을 보전하는 데 기여하고 있습니다.

농업 종사자는 IPM 전략, 내병성 작물, 병해충 방제의 대체 수단을 채용해, 농약의 악영향에 대한 의식을 높이는 것으로, 2017년에 비해 2022년에는 1헥타르당의 살균제 사용량을 38g, 살충제 사용량을 23g 삭감했습니다.

수요 증가와 제한된 가용성은 유효 성분 가격을 크게 변동시킵니다.

시펠메트린은 벼, 면화, 콩, 야채 등의 작물에 영향을 미치는 해충을 제거하기 위해 이 지역에서 주로 사용되는 살충제입니다. 높은 수요로 인해 시펠메트린 가격은 2017년에 비해 2022년 미터톤당 3,186.2달러 상승했습니다. 이 상승은 지역 내 생산이 제한되어 수요를 충족시키기 위해 수입에 크게 의존하기 때문입니다.

아트라진은 남아프리카나 나이지리아와 같은 옥수수 생산국에서 사용되는 주요 제초제이며, 옥수수 면적의 88%가 잡초 방제에 사용되고 있습니다. 아트라진의 사용 범위는 다양한 육상 식용 작물, 비식용 작물, 숲, 주택 잔디, 골프 코스, 레크리에이션 지역, 방목지까지 퍼져 있으며, 농장에서 널리 채용되고 있는 잡초 대책이 되고 있습니다. 다양한 작물 적용이 확대됨에 따라 아틀라진 가격은 전년 대비 꾸준히 상승했으며, 2017년에 비해 2022년에는 1톤당 3,292.7달러의 성장을 기록했습니다.

글리포세이트는 이 지역에서 두 번째로 많이 사용되는 제초제로 널리 받아들여지고 있지만, 그 주요 이유는 저렴합니다. 많은 농업 종사자들은 글리포세이트를 주요 잡초 방제 솔루션으로 선택합니다. 2022년, 글리포세이트의 유효 성분의 가격은 1톤당 1,143.2달러였습니다.

과거 기간 동안 이 지역의 농약 활성 성분의 가격은 크게 상승했고, 미터당 1,580.9달러의 상승이 되었습니다. 이 상승은 주로 이 지역의 생산 능력이 제한되어 있기 때문입니다. 지난 5년간 아프리카로의 농약 수입이 현저하게 증가하여 수입 제품에 대한 의존도가 높아지면서 이 지역의 가격이 상승했습니다.

아프리카의 작물 보호 화학제품 산업 개요

아프리카의 작물 보호 화학제품 시장은 세분화되어 상위 5개사에서 24.91%를 차지하고 있습니다. 이 시장의 주요 기업은 BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

남아프리카

밸류체인 및 유통채널 분석

제5장 시장 세분화(시장 규모(단위 : 달러, 수량), 예측, 성장 전망 분석 포함)(-2030년)

기능별

살균제

제초제

살충제

살연체 동물제

살선충제

적용 모드별

약제 살포

잎면 살포

훈증

종자 처리

토양처리

작물 유형별

상업 작물

과일 및 야채

곡물

콩류 및 지방종자

잔디 및 관상용

생산국별

남아프리카

기타 아프리카

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

ADAMA Agricultural Solutions Ltd.

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Nufarm Ltd

Sumitomo Chemical Co. Ltd

Syngenta Group

UPL Limited

Wynca Group(Wynca Chemicals)

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The Africa Crop Protection Chemicals Market size is estimated at 3.94 billion USD in 2025, and is expected to reach 4.66 billion USD by 2030, growing at a CAGR of 3.43% during the forecast period (2025-2030).

Insecticides dominate the African crop protection chemicals market

Agriculture is one of the major sectors in Africa. This sector fulfills the growing population's food security needs and helps the region to grow economically. The region's diverse climate conditions are favorable to the various crops, including wheat, maize, rice, soybeans, sunflower, beans, tobacco, coffee, cocoa, and tea.

Insecticides dominated the African crop protection chemicals market, accounting for a share of 41.7% in 2022. Crop losses in African countries due to insects are estimated at 49.0% of the expected total crop yield each year, according to the Centre for Agriculture and Biosciences International. However, some crop losses may be even worse, and the effects of the changing climate are expected to increase the damage done by insects. Stem borers, leaf-eating caterpillars, bean flies, aphids, thrips, leafhoppers, whiteflies, and beetles are major pests that cause economic yield losses in the region.

Herbicides are the second most used crop protection chemicals in Africa, accounting for a market share of 30.7% in 2022. On average, the region is losing up to 25-100% crop losses to weed infestations every year. At the same time, the region is implementing intensive agricultural practices to meet the food needs of a growing population, which favors the infestation of various weed species. During the historical period, the consumption of herbicides witnessed significant growth, and the usage increased by 8,264 metric tons between 2017 and 2022.

Growing population, a decrease in arable land, and a rise in food security are some driving factors of the market in the region, and the market is anticipated to witness a CAGR of 3.6% during the forecast period.

The market is growing due to the rising consumption of pesticides to protect crops from pests and weeds

The demand for pesticides in Africa is increasing to protect crops from pests, diseases, and weeds. Farmers in the region depend heavily on these chemicals as pest and disease infestations can result in substantial crop damage and loss.

The fall armyworm infestation can lead to a shortage of 16 million metric tons of maize worth almost USD 5 billion. According to the Centre for Agriculture and Biosciences International, if this moth is not properly controlled, it has the potential to cause annual losses of 8.3 to 20.6 million tons in 12 of Africa's major maize-producing nations.

Africa cultivates root and tuber crops such as cassava, sweet potato, potato, and yam on 23 million hectares of land. Cassava is consumed by 500 million to 1 billion Africans, but it is susceptible to insect pests and disease. The cassava mosaic virus and cassava brown streak disease are the most significant diseases affecting the crop. The annual economic losses in eastern Africa and central Africa are estimated to be between USD 1.90-2.70 billion.

Maize, rice, wheat, and sorghum are the most important food crops grown in the country. Among these, maize is the most widely grown cereal crop. It is highly susceptible to pests, like Chilo partellus Swinhoe (Crambidae), which can cause significant yield losses ranging from 15% to 100% annually. In fact, farmers in eastern Africa have reported production losses of up to USD 450 million due to Chilo partellus alone. These factors are expected to drive the consumption of pesticides, and the crop protection chemicals market is expected to register a CAGR of 3.6% during the forecast period.

Africa Crop Protection Chemicals Market Trends

Adoption of IPM strategies and other alternative methods like crop rotations significantly reduces pesticide consumption per hectare

During the historical period, there has been a remarkable decline in pesticide consumption per hectare within Africa. In 2017, the pesticide consumption rate stood at 1,175 g per ha. However, subsequent efforts have successfully reduced it by 96 g per ha, resulting in a current rate of 1,079 g per ha. This significant reduction in pesticide usage was due to a combination of various factors, which include the implementation of improved agricultural practices that prioritize sustainable and eco-friendly methods. Farmers have increasingly adopted innovative techniques such as integrated pest management, crop rotation, and biological pest control, which have minimized the need for chemical pesticide usage per hectare.

Herbicides are majorly utilized pesticide products in the region, but in recent years, the herbicide consumption per hectare is significantly reduced by 34 g in 2022, as compared to 2017. This substantial decrease in herbicide consumption was due to the successful implementation of integrated weed management (IWM) practices. Under this approach, farmers have adopted a range of innovative strategies such as diversified cropping systems, mechanical weed control, crop rotation, and the use of cover crops. These environment-friendly techniques have contributed to reducing herbicide reliance and also promoted sustainable agriculture, enhancing soil health and conserving biodiversity.

Farmers adopt IPM strategies, disease-resistant crops, and alternatives to control pests and diseases, raising awareness of pesticide's negative effects, thus reducing fungicide and insecticide use per hectare by 38 and 23 g per ha in 2022, compared to 2017.

Increasing demand and limited availability majorly fluctuate the active ingredient prices

Cypermethrin is the predominant insecticide utilized in the region to control pests affecting crops such as rice, cotton, soybeans, and vegetables. Due to its high demand, the price of Cypermethrin rose by USD 3,186.2 per metric ton in 2022 compared to 2017. This increase was due to its limited production within the region, leading to a significant dependence on imports to meet the demand.

Atrazine stands as the primary herbicide utilized in maize-producing countries like South Africa and Nigeria, with 88% of the maize area employed for weed control. Its usage extends to various terrestrial food crops, non-food crops, forests, residential turf, golf courses, recreational areas, and rangelands, making it a widely adopted weed control measure on farms. Due to its expanding application across various crops, the price of Atrazine has been steadily increasing Y-o-Y, with a growth recorded at USD 3,292.7 per metric ton in 2022 compared to 2017.

Glyphosate is widely embraced as the second most used herbicide in the region, primarily due to its affordability. Many farmers opt for glyphosate as their primary weed control solution. In 2022, glyphosate's active ingredient was priced at USD 1,143.2 per metric ton.

During the historical period, prices of pesticide-active ingredients in the region experienced a substantial increase, amounting to an increase of USD 1,580.9 per metric ton. This surge may be mainly attributed to the region's limited production capacity. Over the past five years, there has been a notable rise in pesticide imports into Africa, leading to heightened dependence on imported products and consequent price escalation in the region.

Africa Crop Protection Chemicals Industry Overview

The Africa Crop Protection Chemicals Market is fragmented, with the top five companies occupying 24.91%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 South Africa

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Function

5.1.1 Fungicide

5.1.2 Herbicide

5.1.3 Insecticide

5.1.4 Molluscicide

5.1.5 Nematicide

5.2 Application Mode

5.2.1 Chemigation

5.2.2 Foliar

5.2.3 Fumigation

5.2.4 Seed Treatment

5.2.5 Soil Treatment

5.3 Crop Type

5.3.1 Commercial Crops

5.3.2 Fruits & Vegetables

5.3.3 Grains & Cereals

5.3.4 Pulses & Oilseeds

5.3.5 Turf & Ornamental

5.4 Country

5.4.1 South Africa

5.4.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 ADAMA Agricultural Solutions Ltd.

6.4.2 BASF SE

6.4.3 Bayer AG

6.4.4 Corteva Agriscience

6.4.5 FMC Corporation

6.4.6 Nufarm Ltd

6.4.7 Sumitomo Chemical Co. Ltd

6.4.8 Syngenta Group

6.4.9 UPL Limited

6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS