아시아태평양의 연체동물 살충제 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Asia Pacific Molluscicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1683092

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

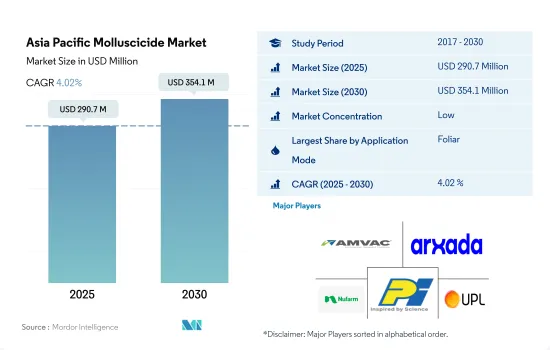

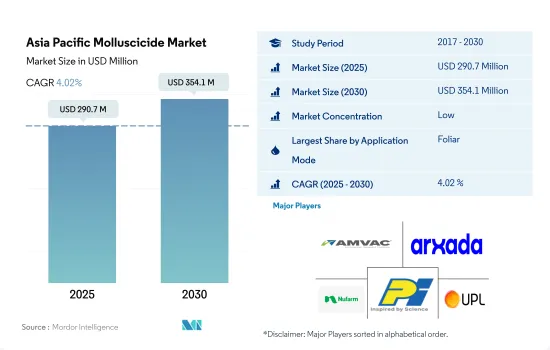

아시아태평양 연체동물 살충제 시장 규모는 2025년에는 2억 9,070만 달러로 추정되고, 2030년에는 3억 5,410만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR은 4.02%로 성장할 전망입니다.

엽면 살포는 즉각적이기 때문에 연체동물 살충제의 용도에서 우위를 차지합니다.

민달팽이와 달팽이는 대부분의 작물과 많은 잡초를 포함한 넓은 잎 식물과 잔디를 폭넓게 먹습니다. 묘목을 시들게 하거나 묘목을 악화시키거나 어린 식물의 잎을 손상시켜 작물에 해를 끼칩니다. 그러므로 민달팽이의 관리는 영향을 받기 쉬운 작물의 수율을 향상시키는 데 가장 중요합니다. 아시아태평양의 연체동물 살충제 시장은 2022년 2억 5,630만 달러로 평가되었으며, 예측 기간이 끝날 때 3억 4,360만 달러에 이를 것으로 예상됩니다.

갈색 정원 달팽이, 거대한 아프리카 달팽이, 논민달팽이, 중국 민달팽이, 킬백 민달팽이는 아시아태평양 작물 생산에 심각한 과제를 초래할 수 있는 주요 민달팽이 및 달팽이 종의 일부입니다. 메타알데히드, 인산철, 메티오카르브, 제2철 EDTA나트륨이 일반적으로 사용되는 연체동물 살충제입니다.

연체동물 살충제는 다양한 방법으로 살포될 수 있습니다. 아시아태평양에서는 엽면 살포가 연체동물 살충제 살포에서 우위를 차지하고 있으며, 2022년에는 54.8%의 최대 시장 점유율을 차지했습니다. 엽면 살포 연체동물 살충제는 연체동물의 개체 수를 신속하게 제어할 수 있습니다. 연체동물 살충제를 잎에 살포하면 해충이 연체동물 살충제와 접촉하여 쉽게 흡수됩니다. 이렇게 하면 빠르게 사멸시킬 수 있습니다.

2022년 아시아태평양의 연체동물 살충제 시장에서는 토양처리가 30.4%로 2위 시장 점유율을 차지했습니다. 달팽이 및 민달팽이에 대한 안정성, 부착성, 유인성을 향상시킨 습윤성이 높은 분말, 과립, 미끼제 개발의 최근 동향이 토양처리를 견인합니다. 시장은 예측기간 2023년부터 2029년까지 CAGR 4.1%를 나타낼 것으로 예측됩니다.

벼와 같은 주요 작물에서 연체동물 살충제의 요구 증가가 시장을 견인

아시아태평양의 연체동물 살충제 시장은 과거 기간 동안 꾸준한 성장을 이루었고, 2022년에는 세계의 연체동물 살충제 시장에서 금액 기준으로 26.0%로 두 번째로 높은 점유율을 차지했습니다.

아시아에서는 달팽이가 생육 중인 벼농사를 파괴하고 벼농사가 이 지역의 주요 식량과 수입원이라는 점에서 심각한 경제적 손실을 야기했기 때문에 달팽이 양식이 실패했습니다. 왕우렁이(Pomacea canaliculata)는 아시아 국가에 도입되어 의외로 벼 해충으로 발전했습니다. 대부분의 농업 종사자들은 연체동물 살충제의 사용을 포함한 화학적 방제에 의존하고 달팽이의 종합적인 관리 방법을 채택하고 있습니다.

벼는 아시아 전역에서 압도적으로 중요한 작물이며, 세계의 생산과 소비의 90%가 이 지역에서 이루어지고 있습니다. 아시아태평양은 쌀과 같은 주식용 곡물의 최대 수출국 및 생산국이기 때문에 연체동물 살충제는 아시아태평양의 곡물 및 곡류에 많이 사용되고 있습니다. 이 부문은 2022년 금액 기준으로 55.5%의 점유율을 차지했습니다.

마찬가지로 과일 작물에 대한 연체 동물의 공격도 이 지역에서 증가하고 있으며, 농업 종사자가 작물을 보호하기 위해 화학적 방제 방법을 채택하기 시작했습니다. 과일 및 야채는 2022년에 금액 기준으로 17.5%의 점유율을 차지했습니다.

이 지역에서는 방제 전략이 시급하지만, 연구자들은 농업 종사자가 연체동물 살충제의 적절한 살포 전략을 채택하기 위해서는 달팽이의 생태에 대한 올바른 지식을 가질 필요가 있다고 지적합니다. 동시에, 각국 정부에 의한 대처나 제조업체에 의한 기술 혁신에 의해 동지역의 연체동물 살충제 시장은 예측 기간중 2023년부터 2029년까지 CAGR 4.2%로 성장할 것으로 전망되고 있습니다.

아시아태평양 연체동물 살충제 시장 동향

연체 동물의 개체 수가 증가하면 헥타르 당 살포량이 증가합니다.

연체동물 살충제의 헥타르당 소비량은 일본이 최대이며, 2022년에는 100.0그램이 되었습니다. 달팽이는 일본에서는 폭넓은 작물을 식해하는 일반적인 해충입니다. 그러나 외래종인 왕우렁이는 일본, 특히 규슈의 벼농사에 큰 위협을 가져왔습니다. 왕우렁이는 벼농사에서 직파 재배의 도입에 큰 장애가 되고 있다고 여겨집니다. 이 문제를 해결하기 위해 농업 종사자의 연체동물 살충제와 기피제의 사용이 증가하고 있으며, 왕우렁이의 침입으로 인한 영향을 줄이는 효과적인 전략임이 입증되었습니다.

호주는 아시아태평양에서 1헥타르당 연체동물 살충제의 사용량이 압도적으로 많아 2022년에는 1헥타르당 13.2그램을 사용했습니다. 아프리카 왕달팽이(Lissachatina fulica)는 급속하게 번식하고 농작물, 관상용 식물 및 자생 식물을 포함한 다양한 식물을 먹기 때문에 호주에서 주요 해충으로 간주됩니다. 식욕이왕성하고 정원과 농작물, 자연 서식지에 큰 피해를 주어 심각한 경제적 손실로 이어집니다.

2022년 연체동물 살충제를 사용한 국가는 필리핀, 베트남, 중국이 각각 1헥타르당 9.9그램, 8.4그램, 7.1그램으로 돌출했습니다. 국제 벼 실험실에 따르면 왕우렁이는 벼 줄기를 뿌리에서 절단하고 주식 전체를 파괴하기 때문에 이들 국가에서는 벼 생산에 큰 위협이 되고 있으며, 특히 관개 논에서는 연간 수율이 최대 50% 감소한다고 합니다.

왕우렁이 같은 달팽이 종류는 성장이 빠르고 번식도 빠르기 때문에 방제가 매우 어렵고 아시아태평양 국가에서는 연체동물 살충제의 사용량이 증가하고 있습니다.

이 시장의 주요 촉진요인으로는 농약의 채용이 증가하고 있는 것, 아시아의 논에서 왕우렁이가 만연하고 있는 것 등을 들 수 있습니다.

민달팽이는 일반적으로 토양 표면의 위아래로 먹고 씨앗, 새싹, 뿌리에 손상을 줍니다. 작물에 따라서는 파종시에 주요 문제가 발생하는 것도 있고, 생육기나 수확시에 문제가 발생하는 것도 있습니다. 이러한 연체동물 유형은 농업에 막대한 손실을 초래하는 큰 위협 중 하나입니다. 이 종은 주로 밀, 보리, 귀리와 같은 곡물과 원예 작물에서 발견됩니다. Deroceras, Milax, Tandonia, Limax, Arion은 농작물에 경제적 손실을 초래하는 중요한 연체동물로 인정받고 있습니다.

금속 알데히드는 연체동물 살충제로서 밭, 정원, 온실에서 다양한 야채와 작물에 사용됩니다. 민달팽이 및 달팽이를 죽이기 위해 액체, 과립, 살포, 먼지, 펠릿 및 미립자 먹이의 형태로 살포됩니다. 메탈알데히드는 2022년 1톤당 52,500달러로 평가되었습니다.

인산철은 곡물, 유채, 감자 및 광범위한 원예 작물에 사용되는 연체동물 살충제로 2022년에는 1톤당 5만 2,000달러로 평가되었습니다. 인산철은 목장의 칼슘 대사를 억제하고 궁극적으로 녹말의 작물과 간췌장에서 세포 병리학적 변화를 일으킵니다. 이 섭식부터 사멸까지의 과정은 보통 약 3-6일 걸립니다.

이 시장의 주요 촉진요인으로는 농약 채용 증가, 고부가가치 원예작물에 대한 수요의 고조, 아시아의 논에서의 왕우렁이의 만연 등을 들 수 있습니다. 게다가, 농업 종사자의 연체동물 제거에 대한 의식이 증가하고 혁신적인 연체동물 살충제의 도입은 예측 기간 동안 이 시장에 성장 기회를 가져올 것으로 기대됩니다.

아시아태평양 연체동물 살충제 산업 개요

아시아태평양 연체동물 살충제 시장은 세분화되어 상위 5개사에서 14.89%를 차지하고 있습니다. 이 시장의 주요 기업은 American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries, UPL Limited입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

1헥타르당 농약 소비량

유효성분의 가격 분석

규제 프레임워크

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

밸류체인 및 유통채널 분석

제5장 시장 세분화

용도 모드별

화학 관개

잎면 살포

훈증

토양처리

작물 유형별

상업 작물

과일 및 야채

곡물

콩류 및 지방종자

잔디 및 관상용

생산국

호주

중국

인도

인도네시아

일본

미얀마

파키스탄

필리핀

태국

베트남

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

American Vanguard Corporation

Arxada

Nufarm Ltd

PI Industries

UPL Limited

Zagro

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The Asia Pacific Molluscicide Market size is estimated at 290.7 million USD in 2025, and is expected to reach 354.1 million USD by 2030, growing at a CAGR of 4.02% during the forecast period (2025-2030).

Foliar application dominates molluscicide applications owing to its quick action

Slugs and snails eat a wide array of broadleaf plants and grasses, including most crops and many weeds. They harm crops by killing seedlings, causing poor stands, and damaging leaves on young plants. Hence, the management of slugs is of utmost importance to get better yields in the susceptible crops. The Asia-Pacific molluscicide market was valued at USD 256.3 million in 2022 and is anticipated to reach USD 343.6 million by the end of the forecast period.

Brown garden snails, giant African snails, rice field slugs, Chinese slugs, and keelback slugs are some of the major slug and snail species that can pose significant challenges to crop production in Asia-Pacific. Metaldehyde, iron phosphate, methiocarb, and sodium ferric EDTA are commonly used molluscicides.

Molluscicides can be applied through different methods. In Asia-Pacific, foliar application dominated in molluscicide application, accounting for the largest market share of 54.8% in 2022. Foliar-applied molluscicides can provide quick control of mollusk populations. When sprayed onto the foliage, the molluscicides can be readily absorbed by the pests as they come into contact with it. This can lead to rapid mortality.

Soil treatment accounted for the second largest market share of 30.4% of the Asia-Pacific molluscicide market in 2022. Recent advances in the development of enhanced wettable powders, granules, and bait formulations with improved stability, adherence, and attractiveness to snails and slugs will drive the soil treatment. The market is anticipated to register a CAGR of 4.1% during the forecast period (2023-2029).

Increased need for molluscicides in major crops like rice is driving the market

The molluscicides market in Asia-Pacific witnessed steady growth during the historical period, with the region occupying the second-highest share of 26.0% by value of the global molluscicide market in 2022.

Snail farming failed in Asia as snails destroyed the growing rice crops, causing severe economic losses as rice farms are the region's major source of food and income. The golden apple snail, Pomacea canaliculata, has been introduced to several Asian countries, where it has unexpectedly developed into a rice pest. Most farmers have resorted to chemical control, including the use of molluscicides, and have adopted integrated snail management practices.

Rice is by far the most important crop throughout Asia, where 90% of the world's production and consumption occurs in this region. Molluscicides are mostly used in grains and cereals in Asia-Pacific as the region is the largest exporter and producer of staple grains such as rice. The segment occupied a share of 55.5% by value in 2022.

Similarly, mollusk attacks on fruit crops have also been on the rise in the region, leading to farmers adopting chemical control methods to protect their crops. Fruits and vegetables occupied a share of 17.5% by value in 2022.

Although control strategies are urgently needed in the region, researchers have suggested that farmers must have a sound knowledge of the ecology of snails to adopt the right application strategy for molluscicides. At the same time, initiatives by governments of various countries and innovations by manufacturers are expected to drive the molluscicide market in the region at a CAGR of 4.2% during the forecast period (2023-2029).

Asia Pacific Molluscicide Market Trends

The increasing mollusk population is leading to higher application per hectare

Japan is the largest per hectare consumer of molluscicides, with 100.0 grams in 2022. Snails are common pests that feed on a wide range of crops in Japan. However, the apple snail, an invasive species, poses a significant threat to rice cultivation in Japan, particularly in Kyushu. It is considered a major hindrance to the adoption of direct-sowing practices in rice farming. To address this problem, the use of molluscicides and repellents by farmers has increased and proven to be an effective strategy in mitigating the impact caused by the apple snail invasion.

Australia is by far the second-highest per hectare consumer of molluscicides in Asia-Pacific, with 13.2 grams per hectare in 2022. African giant snail (Lissachatina fulica) is considered a major pest in Australia due to its ability to reproduce rapidly and feed on a wide range of plants, including crops, ornamental plants, and native vegetation. It has a voracious appetite and can cause significant damage to gardens, crops, and natural habitats, leading to severe economic losses.

The Philippines, Vietnam, and China were other prominent countries using molluscicides at the rate of 9.9 grams, 8.4 grams, and 7.1 grams per hectare, respectively, in 2022. Golden apple snails are the major threat to rice production in these countries as they cut the rice stem at the base, destroying the whole plant and leading to annual yield losses of up to 50%, especially in irrigated rice fields, according to the International Rice Research Institute.

Few of the snail species like golden apple snails can grow and reproduce quickly, making it very difficult to control, leading to higher usage of molluscicides in the countries of Asia-Pacific.

The major drivers for this market include the increasing adoption of agrochemicals and the infestation of golden apple snails in the rice fields of Asia

Slugs usually feed above and below the soil surface, damaging seeds, shoots, and roots. In some crops, the main problem time is at planting, while in others, problems occur during the growing season or harvest. These mollusk species have become one of the major threats causing huge agricultural losses. These species are majorly seen in cereal crops such as wheat, barley, oats, and horticultural crops. Deroceras, Milax, Tandonia, Limax, and Arion are recognized as important mollusks causing economic losses in the crops.

Metaldehyde is a molluscicide used in a variety of vegetables and crops in fields, gardens, and greenhouses. It is applied in the form of liquid, granules, sprays, dust, or pelleted/grain bait to kill slugs and snails. Metaldehyde was valued at USD 52.5 thousand per metric ton in 2022.

Ferric phosphate is a molluscicide for use in cereals, oilseed rape, potatoes, and a wide range of horticultural crops and was valued at USD 52.0 thousand per metric ton in 2022. Iron phosphate interferes with the calcium metabolism within the slug and eventually causes cellular pathological changes in the slug's crop and hepatopancreas. This process from feeding to dying normally takes about three to six days.

The major drivers for this market include increasing adoption of agrochemicals, rising demand for high-value horticulture crops, and infestation of golden apple snails in the rice fields of Asia. Further, increasing awareness of mollusk control among farmers and the introduction of innovative molluscicide products are expected to create growth opportunities for this market during the forecast period.

Asia Pacific Molluscicide Industry Overview

The Asia Pacific Molluscicide Market is fragmented, with the top five companies occupying 14.89%. The major players in this market are American Vanguard Corporation, Arxada, Nufarm Ltd, PI Industries and UPL Limited (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Consumption Of Pesticide Per Hectare

4.2 Pricing Analysis For Active Ingredients

4.3 Regulatory Framework

4.3.1 Australia

4.3.2 China

4.3.3 India

4.3.4 Indonesia

4.3.5 Japan

4.3.6 Myanmar

4.3.7 Pakistan

4.3.8 Philippines

4.3.9 Thailand

4.3.10 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application Mode

5.1.1 Chemigation

5.1.2 Foliar

5.1.3 Fumigation

5.1.4 Soil Treatment

5.2 Crop Type

5.2.1 Commercial Crops

5.2.2 Fruits & Vegetables

5.2.3 Grains & Cereals

5.2.4 Pulses & Oilseeds

5.2.5 Turf & Ornamental

5.3 Country

5.3.1 Australia

5.3.2 China

5.3.3 India

5.3.4 Indonesia

5.3.5 Japan

5.3.6 Myanmar

5.3.7 Pakistan

5.3.8 Philippines

5.3.9 Thailand

5.3.10 Vietnam

5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

6.4.1 American Vanguard Corporation

6.4.2 Arxada

6.4.3 Nufarm Ltd

6.4.4 PI Industries

6.4.5 UPL Limited

6.4.6 Zagro

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS