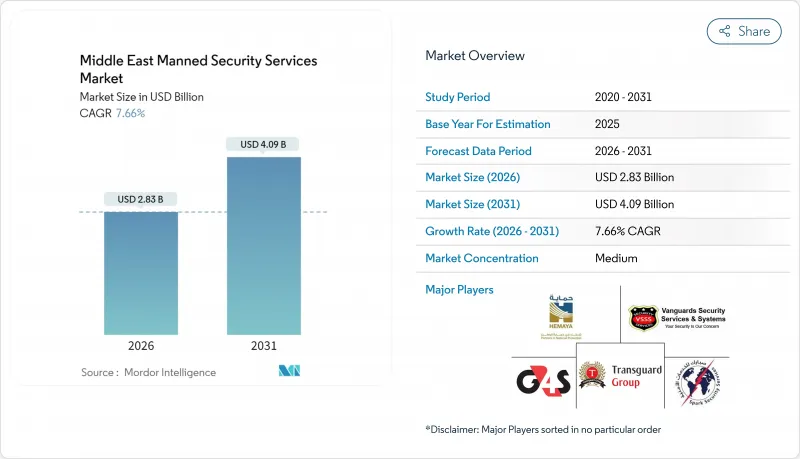

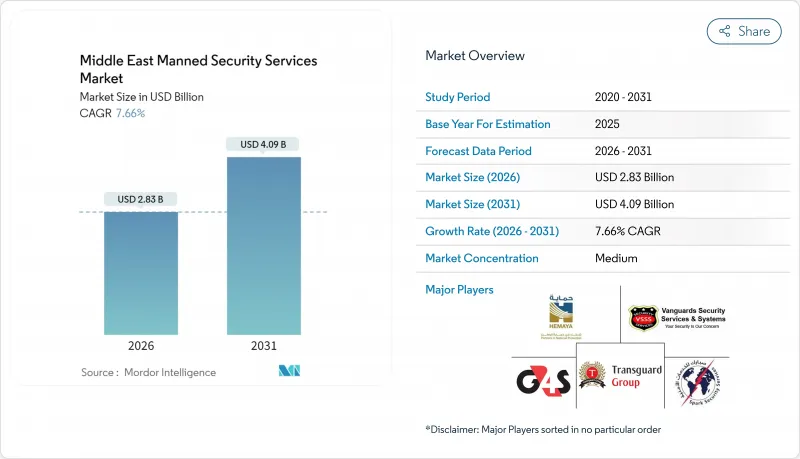

중동의 유인 경비 서비스 시장은 2025년 26억 3,000만 달러로 평가되었으며, 2026년 28억 3,000만 달러, 2031년까지 40억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)에 CAGR은 7.66%를 나타낼 전망입니다.

사우디아라비아의 '비전 2030', 아랍에미리트(UAE)의 에티하드 철도, 카타르의 고주파 이벤트 계획에 따른 인프라 투자의 급증이 지출을 계속 지원하는 한편, 규제 강화에 의해 고품질의 라이선싱 경비 요원에 대한 수요가 높아지고, 고단가화가 진행되고 있습니다. 기업 및 정부기관의 구매 부문은 물리적 경비와 AI 탑재 영상 분석, 드론 순회, 생체 인증 액세스를 조합함으로써 경비 범위를 손상시키지 않고 인원 삭감을 도모하고 있습니다. 새로운 에미레이트화 및 사우디화 할당량제도에 의한 임금압력과 연간 35%의 경비원 이직률이 결합되어 기술과 소규모로 고임금 팀을 조합한 통합계약으로의 이행이 공급자에게 요구되고 있습니다. 얼라이드 유니버설과 같은 세계의 통합 기업에 의한 월경 투자의 활성화는 지속적인 수익성에서 규모와 자본이 필수적인 요소가 되었음을 보여줍니다.

사우디아라비아는 2030년까지 1억 1,600만 명의 관광객 유치를 목표로 하고 있으며, 2027년 AFC 아시아컵과 2034년 FIFA 월드컵 등 메가 이벤트가 그 기둥이 됩니다. 이 모든 것에서 스마트 군중 분석 기술을 기반으로 한 다층적 인적 보안이 요구됩니다. 카타르에서 개최된 2022년 FIFA 월드컵은 3,000명의 외국인 기동대원 외에 대 드론 시스템을 전개하는 등 필요한 규모와 전문성을 보여주었습니다. 지역 주최자는 현재 VIP 호위 및 실시간 사고 보고를 교육받은 다국어 대응 경비원을 찾고 있으며 경비원 시간당 수익을 끌어올리는 서비스 프리미엄을 창출하고 있습니다. 경기장 고유의 훈련을 받은 공인 팀을 파견할 수 있는 공급자는 새로운 장소가 가동됨에 따라 반복 계약을 받았습니다. 두바이, 리야드, 도하가 컨퍼런스 포트폴리오를 확대하는 가운데, 이벤트 경비는 임시 인력 배치에서 연중 틀의 계약으로 성숙하고 있습니다.

비전 2030의 1조 달러 규모의 건설 계획(NEOM의 170km에 이르는 선형 도시, 키디아의 엔터테인먼트 클러스터, 에티하드 철도의 1,200km 네트워크 포함)에서는 상시 경비 구역의 보호, 드론 모니터링, 사이버 모니터링 센터의 설치가 요구되고 있습니다. 우드사 등의 계약자는 2024년 지역계약에서 9억 2,000만 달러를 획득하여 원격지의 탄화수소 및 재생에너지 시설을 위해 500명의 추가 인원을 고용했습니다. 보안 범위는 현재 위험 평가, 액세스 제어 설계, 장기 지령 센터 운영을 포괄하고 여러 공급업체를 수년간 수익원에 연결합니다. 중동의 유인 경비 서비스 시장에서는 계약 금액 증가와 고객의 탈락이 보이며 규모를 확대하는 사업자의 수익성이 향상되고 있습니다.

사우디아라비아의 니터컷 제도에서는 컨설팅과 사이버 보안 업무에서 자국민 비율 40%가 의무화되었으며, 아랍에미리트(UAE)에서는 에미라티화 시책 하에서 직종별 목표가 확대되고 있습니다. 사우디 국민은 할당 대상이 되기 위해 월액 최소 4,000 사우디 리얄(1,067 USD)을 벌어야 하기 때문에 기업이 인원 구성을 재조정할 때 경비원의 급여 지출은 15-25% 증가합니다. 규제 위반은 비자 발행 제한이나 입찰 금지를 초래하기 때문에 서비스 제공 기업은 증가한 인건비를 고객에게 전가할 수밖에 없어 기술 대체 수단에 대한 가격 경쟁력이 저하되고 있습니다.

상업 부문은 2025년 중동 유인 경비 서비스 시장 점유율의 45.12%를 유지하면서 아랍에미리트(UAE)과 사우디아라비아에서 소매, 접객 및 복합 용도 건설에 대한 지속적인 수요를 배경으로 했습니다. 고층 빌딩 개발업체는 상주 경비원을 줄이면서 24시간 체제의 영상 분석을 도입하는 '경비+기술' 통합 포장을 선호합니다. 정부·기관 고객은 규모가 작지만 리야드와 도하가 거대 프로젝트와 국가 행사 개최를 위한 보안을 앞당겨 강화하고 있기 때문에 8.42%의 연평균 복합 성장률(CAGR)로 가장 급속히 확대하고 있습니다. 이 계층의 계약 규모는 더 크고 여러 해에 걸쳐 엄격한 현지화 조항을 포함하기 때문에 외국 기업의 진입 장벽이 높아지고 있습니다. 따라서 사우디화(사우디 인재 우선 고용) 준수 및 무기 허가 취득을 실증하는 공급업체에서 중동 정부용 유인 경비 서비스 시장 규모는 2031년까지 두배로 될 것으로 예측됩니다.

상업계약은 여전히 정부 입찰을 능가하지만 가격 경쟁은 더욱 심화되고 있습니다. 개발업체는 총소유비용(TCO)을 중시하고 분석기술을 통합하여 인력을 20-30% 삭감할 수 있는 경비회사에 우대조치를 줍니다. 한편 정부부처는 엄격한 심사를 거친 아랍어 대응팀과 안전한 지령센터를 중시하고 할증요금을 결제합니다. 에너지부문을 필두로 하는 산업구매자는 위험환경 대응 인증을 요구하기 때문에 소매경비에 비해 평균 일당이 최대 40% 높아집니다. 두바이와 아부다비의 주거 단지에서는 SIRA 모니터링 허브와 협력하는 커뮤니티 전체의 액세스 관리 앱을 채택하여 기술에 익숙한 공급자로의 가치 변화가 진행되고 있습니다.

2025년 시점에서 중동 유인 경비 서비스 시장의 고정 경비 점유율은 58.10%를 차지하고 있습니다. 이는 건물 사용 시간 동안 항상 인정을 받은 인원을 현장에 배치할 것을 의무화하는 건축 기준법에 의해 뒷받침됩니다. 중동의 상주 경비 서비스 시장 규모는 그 점유율이 감소하는 한편, 기가 프로젝트 전체에서 경비 대상 면적이 확대되고 있기 때문에 절대치로서는 계속 증가할 전망입니다. 한편, 이벤트 경비와 군중 관리 업무는 경기장 건설 프로젝트, 국제 박람회, 다언어 대응 및 군중 분석 훈련을 받은 요원을 필요로 하는 문화제의 급증을 계기로 CAGR 8.74%로 성장하고 있습니다.

이동 경비 서비스는 GPS에 의한 배치와 바디 카메라를 융합시켜, 한 세트의 경비원이 1 시프트로 최대 8개소의 저위험 시설을 커버할 수 있게 됩니다. 현금 수송 업무는 틈새면서 고수익을 유지. 브링크스와 같은 사업자들은 스마트 금고와 실시간 차량 텔레메트리를 통합하여 리스크 프리미엄을 줄이고 있습니다. 공항 및 수입 폭발 볼트를 보관하는 대규모 건설 현장에서는 K9 폭발물 감지 장치 수요가 안정적입니다. 모든 카테고리에서 기술의 융합은 멈추지 않습니다. 두바이에서는 신규 고정 경비 계약의 40%가 내장형 열화상 카메라와 AI 침입 경보를 지정해 하드웨어 상각비를 월액 경비 요금에 포함하고 있습니다.

The Middle East manned security services market was valued at USD 2.63 billion in 2025 and estimated to grow from USD 2.83 billion in 2026 to reach USD 4.09 billion by 2031, at a CAGR of 7.66% during the forecast period (2026-2031).

Spiraling infrastructure outlays linked to Saudi Arabia's Vision 2030, the UAE's Etihad Rail, and Qatar's high-frequency events pipeline continue to anchor spending, while tightening regulatory regimes mandate higher-quality, licensed guard forces that command premium rates. Corporate and sovereign buyers are increasingly bundling physical guarding with AI-enabled video analytics, drone patrols, and biometric access to cut headcount without compromising coverage. Wage pressures triggered by new Emiratization and Saudization quotas and a 35% annual guard turnover rate are pushing providers toward integrated contracts that mix technology with smaller, better-paid teams. Intensifying cross-border investments by global consolidators such as Allied Universal underscore how scale and capital are now prerequisites for sustained profitability.

Saudi Arabia aims to attract 116 million visitors by 2030, anchored by mega-events such as the 2027 AFC Asian Cup and the FIFA World Cup 2034, all of which require layered human security backed by smart crowd analytics. Qatar's FIFA World Cup 2022 illustrated the volume and specialization needed, deploying 3,000 foreign riot police plus anti-drone systems. Regional organizers now demand multilingual guards trained in VIP escort and real-time incident reporting, creating a service premium that boosts revenue per guard hour. Providers able to field certified teams with stadium-specific training win repeat contracts as new venues come online. As Dubai, Riyadh, and Doha expand their conference portfolios, event guarding has matured from ad-hoc staffing to year-round, framework-style agreements.

Vision 2030's USD 1 trillion construction docket, spanning NEOM's 170-km linear city, Qiddiya's entertainment cluster, and Etihad Rail's 1,200-km network, requires constant perimeter protection, drone surveillance, and cyberwatch centers. Contractors like Wood plc secured USD 920 million in regional awards during 2024, hiring 500 additional personnel to service remote hydrocarbons and renewables sites. Guarding scopes now bundle risk assessments, access control design, and long-term command-center operations, locking providers into multi-year revenue streams. The Middle East manned security services market thus sees higher contract values and lower churn, improving profitability for scale players.

Saudi Arabia's Nitaqat system now mandates 40% nationals in consulting and cybersecurity functions, while the UAE expands job-classification targets under Emiratization. Because Saudi nationals earn at least SAR 4,000 (USD 1,067) monthly to count toward quotas, guard payroll outlays rise 15-25% when firms rebalance headcount. Non-compliance triggers visa caps and tender bans, so providers pass higher labor costs to clients, eroding price competitiveness against technology alternatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The commercial segment retained 45.12% of Middle East manned security services market share in 2025, leveraging sustained retail, hospitality, and mixed-use construction in the UAE and Saudi Arabia. High-rise developers favor integrated guarding-plus-tech packages with fewer on-site guards but round-the-clock video analytics. Government and institutional customers, though smaller today, are expanding fastest at an 8.42% CAGR as Riyadh and Doha front-load security for giga-projects and sovereign event hosting. Contract values in this tier are larger, multi-year, and include stringent localization clauses, raising barriers for foreign entrants. The Middle East manned security services market size for government work is therefore expected to double by 2031 among suppliers that demonstrate Saudization compliance and secure weapons permits.

Commercial contracts still outnumber government tenders, but pricing pressure is higher; developers award on total cost of ownership, rewarding guard firms that embed analytics to trim rosters by 20-30%. In contrast, ministries pay premiums for vetted, Arabic-speaking teams supported by secure command centers. Industrial buyers, led by the energy sector, require hazardous-environment certification, boosting average daily rates by up to 40% compared with retail guarding. Residential compounds in Dubai and Abu Dhabi adopt community-wide access apps that integrate with SIRA's monitoring hub, shifting value toward tech-savvy providers.

Static guarding held 58.10% of the Middle East manned security services market in 2025, underpinned by building codes that require certified on-site personnel during all occupancy hours. The Middle East manned security services market size tied to static posts will continue to rise in absolute terms even as its share declines, because total guarded square footage expands across giga-projects. Event and crowd-control assignments, however, grow at an 8.74% CAGR, catalyzed by stadium projects, international expos, and a surge in cultural festivals that necessitate multi-lingual, crowd-analytics-trained personnel.

Mobile patrol services merge GPS dispatch with body-worn cameras, allowing one crew to cover up to eight low-risk sites during a shift. Cash-in-Transit remains niche but high margin; providers such as Brink's integrate smart safes and real-time fleet telemetry to cut risk premiums. K9 explosive-detection units enjoy steady demand at airports and large construction sites that house imported explosive bolts. Across categories, technology convergence is relentless: 40% of new static contracts in Dubai now specify built-in thermal cameras and AI intrusion alerts, embedding hardware amortization into monthly guard fees.

The Middle East Manned Security Services Market Report is Segmented by End-User (Commercial, Industrial, Government and Institutional, and More), Service Type (Static Guarding, Mobile Patrol, and More), Guard Classification (Unarmed Guards and Armed Guards), Contract Duration (Long-Term Above 12 Months, and Short-term/Event-based), and Country. The Market Forecasts are Provided in Terms of Value (USD).