ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

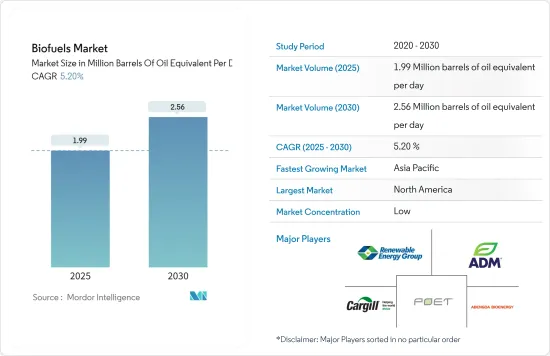

바이오연료 시장 규모는 2025년 석유 환산일량 199만 배럴로 추정되고, 예측기간(2025-2030년)의 CAGR은 5.2%로 전망되며, 2030년에는 석유 환산일량 256만 배럴에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 안전하고 지속 가능한 청정에너지에 대한 수요가 증가하고 자동차 연료에 대한 혼합비율을 높이는 정부의 의무화가 함께 세계 바이오연료 수요가 촉진될 것으로 예상됩니다.

반면에, 바이오연료와 관련된 모든 이점이 있음에도 불구하고, 바이오연료의 생산 비용이 높아 시장 성장을 억제할 가능성이 높습니다.

최근의 기술 진보에 따라 바이오연료의 생산량이 증가하고 있으며, 이는 시장 확대의 호기가 될 것 같습니다.

북미는 시장을 독점하고 있으며 예측 기간 동안 가장 높은 CAGR로 추이할 가능성이 높습니다. 이 지역에서는 바이오연료 수요 증가와 함께 생산 설비가 급증하고 있는 것이 성장의 요인이 되고 있습니다.

바이오연료 시장 동향

상당한 성장이 예상되는 에탄올

세계적으로 보면, 운수부문은 내연기관에서 화석연료의 연소에 의해 온실가스를 가장 많이 배출하고 있습니다. 온실가스 배출을 제한하기 위해 세계 각국은 신재생 에너지 자원의 이용을 촉진하는 기준을 채택하고 있습니다. 에탄올과 같은 바이오연료는 운송부문에 보다 깨끗한 에너지원이며, 향후 바이오연료 시장의 개척으로 이어질 수 있습니다.

재생가능연료협회(RFA)에 따르면 2022년 미국은 1,540억 갤런의 연료용 에탄올을 생산하여 세계 최고의 바이오연료 생산국이 되었습니다.

바이오연료의 세계 수요를 견인하고 있는 것은 북미, 인도, 브라질, 유럽, 인도네시아, 말레이시아 등에서 정해진 1차 혼합 의무입니다. 예를 들어 인도에서는 2025년까지 에탄올을 20% 혼합해야 합니다. 인도네시아에서는 바이오디젤 35% 혼합이 2023년에 시작될 예정이며, 브라질에서는 에탄올 혼합에 대한 기존 지령은 27%입니다. 이러한 조치는 바이오연료의 이용이 각국에서 증가하고 있음을 돋보이게 합니다.

또한 2022년 3월 브라질 경제부는 인플레이션 압력을 완화하기 위해 다른 제품을 포함한 에탄올 수입 관세 철폐를 발표했습니다. 이는 가솔린으로의 에탄올 혼합을 촉진하고 시장이 활성화될 것으로 예상했습니다.

2022년에는 SGP BioEnergy가 파나마 정부와 공동으로 세계에서 가장 대규모 바이오연료의 유통 및 생산 허브를 파나마에 개발할 것이라고 발표했으며, 닛산 18만 배럴의 바이오연료 생산이 전망되고 있습니다. 마찬가지로 미국 에너지부는 2023년 미국의 운송 및 제조 요구를 충족시키기 위해 에탄올 및 기타 바이오연료를 확대하는 17개 프로젝트에 1억 1,800만 달러를 기부했습니다. 이러한 동향은 바이오연료 시장을 활성화시킬 가능성이 높습니다.

따라서 위의 관점에서 에탄올 부문은 예측 기간 동안 바이오연료 시장에서 큰 성장을 이룰 것으로 예상됩니다.

북미가 시장을 독점할 전망

북미에는 화석연료를 중심으로 하는 최대급의 항공시장이 있으며, 교통 인프라도 정비되어 있습니다. 북미는 온실 효과를 억제하기 위해 배출량 감소의 최전선에 서 왔습니다.

미국 에너지정보국에 따르면 미국의 바이오디젤 총 생산량은 2022년까지 16억 갤런에 달할 전망입니다.

2022년 1월 미국 환경보호청은 온실가스 배출량이 많은 화석연료를 대폭 대체할 수 있는 바이오연료와 화학제품의 심사를 합리화하는 새로운 구상을 발표하고 바이오연료 시장을 크게 뒷받침했습니다. 마찬가지로 미국 에너지부는 2022년 12월 이후에 설치되는 천연가스, 프로판, 액화수소, 전기, E85 또는 바이오디젤 20% 이상을 포함한 디젤 혼합연료의 급유설비에 대해 30%의 대체연료 인프라 세액공제를 실시한다고 발표했습니다. 이러한 우대 조치는 바이오연료 시장을 촉진하는 것으로 간주됩니다.

마찬가지로 캐나다 정부는 2022년 4월부터 탄소세를 배출량 1톤당 10캐나다 달러에서 50캐나다 달러로 끌어올려 온실가스 배출량이 적은 바이오연료의 보급을 촉진하는 것을 목표로 하고 있습니다.

이상으로부터, 정부의 시책과 생산 능력에 의해 북미가 바이오연료 시장을 독점할 가능성이 높습니다.

바이오연료 산업 개요

바이오연료 시장은 세분화되어 있습니다. 주요 기업으로는 Archer Daniels Midland Company, Abengoa Bioenergy SA, Renewable Energy Group Inc., Cargill Incorporated, POET LLC 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

바이오연료 생산의 역사와 예측(-2028년)

바이오연료 소비의 역사적 추이 및 예측(-2028년)

최근 동향 및 개발

정부의 규제 및 시책

시장 역학

성장 촉진요인

안전하고 지속 가능한 청정 에너지에 대한 수요 증가

억제요인

바이오연료의 높은 생산 비용

공급망 분석

산업의 매력-Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

연료 유형별

에탄올

바이오디젤

기타 연료 유형

원료별

팜유

자트로파

설탕 작물

거친 곡물

기타 원료

지역별

북미

미국

캐나다

기타 북미

유럽

독일

영국

덴마크

기타 유럽

아시아태평양

중국

인도

인도네시아

기타 아시아태평양

남미

브라질

아르헨티나

칠레

기타 남미

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

주요 기업의 전략

기업 프로파일

Abengoa Bioenergy SA

Cargill Incorporated

Shell PLC

Wilmar International Ltd.

Renewable Energy Group Inc.

Archer Daniels Midland Company

BP PLC

POET LLC

Neste Oyj

Verbio Vereinigte BioEnergie AG

제7장 시장 기회 및 향후 동향

바이오연료 생산에 있어서 기술의 진보

AJY

영문 목차

영문목차

The Biofuels Market size is estimated at 1.99 million barrels of oil equivalent per day in 2025, and is expected to reach 2.56 million barrels of oil equivalent per day by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing demand for secure, sustainable, and clean energy coupled with government mandates for increasing blending in automotive fuels is expected to propel the demand for biofuels across the globe.

On the other hand, the high cost of production of biofuels, even with all the benefits associated with them, is likely to restrain the growth of the market.

Nevertheless, with the recent technological advancements, the production of biofuels has increased, which is going to act as an opportunity for the market's expansion.

North America dominates the market, and it is likely to witness the highest CAGR during the forecast period. The growth is attributed to the rapid increase in production facilities coupled with the increase in demand for biofuels in the region.

Biofuels Market Trends

Ethanol Likely to Experience a Significant Growth

Globally, the transportation sector is the biggest emitter of greenhouse gases due to the combustion of fossil fuels in its internal combustion engines. To limit the emission of greenhouse gases, countries worldwide have adopted norms to promote the use of renewable energy resources. Biofuels such as ethanol affirm themselves as a cleaner energy source for the transportation sector, which could lead to a developed biofuel market in the future.

According to the Renewable Fuels Association (RFA), in 2022, the United States produced 15,4 billion gallons of fuel ethanol, making it the leading producer of biofuel in the world.

Primary blending mandates that drive the global demand for biofuels are set in North America, India, Brazil, Europe, Indonesia, Malaysia, etc. For instance, in India, there is a mandate to begin 20% ethanol blending by 2025. In Indonesia, a commission of 35% biodiesel blending is expected to start in 2023, whereas in Brazil, the existing order for ethanol blending is 27%. Such measures highlight the increase in the use of biofuels across countries.

Furthermore, in March 2022, Brazil's Ministry of Economy announced the withdrawal of import tariffs on ethanol, including other products, to alleviate inflationary pressures. This is expected to boost the ethanol blend in gasoline and drive the market.

In 2022, SGP BioEnergy announced the development of the world's most extensive biofuel distribution and production hub in Panama, in association with the country's government, which is estimated to produce 180,000 barrels per day of biofuel. Similarly, in 2023, the US Department of Energy awarded USD 118 million for 17 projects to scale up ethanol and other biofuels to help America's transportation and manufacturing needs. Such trends are likely to ramp up the biofuel market.

Therefore, owing to the above points, the ethanol segment is expected to experience significant growth in the biofuels market during the forecast period.

North America is Expected to Dominate the Market

The North American region houses one of the biggest aviation markets, primarily fossil fuels, and a well-established transportation infrastructure. The North American region has been at the forefront of lowering emissions to limit the greenhouse effect.

According to the U.S. Energy Information Administration, the total production volume of biodiesel production in the United States was 1.6 billion gallons by 2022

In January 2022, the US Environmental Protection Agency announced a new initiative for streamlining the review of biofuels and chemicals that can significantly replace higher GHG-emitting fossil fuels, providing a significant push to the biofuels market. Similarly, the US Department of Energy announced an Alternative Fuel Infrastructure Tax Credit of 30% for the fueling equipment for natural gas, propane, liquefied hydrogen, electricity, E85, or diesel fuel blends containing a minimum of 20% biodiesel installed on or after December 2022. Such incentive measures would likely promote the biofuel market.

Similarly, in Canada, the government aimed to increase carbon taxes by CAD 10 to CAD 50 per ton of emissions from April 2022, thereby pushing for wider adoption of biofuels that emit less GHG.

Hence, owing to the above points, the North American region is likely to dominate the biofuels market due to government policies and production capacity.

Biofuels Industry Overview

The biofuels market is fragmented. Some of the major players include (in no particular order) Archer Daniels Midland Company, Abengoa Bioenergy SA, Renewable Energy Group Inc., Cargill Incorporated, and POET LLC., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Biofuel Production Historic and Forecast, till 2028

4.3 Biofuel Consumption Historic and Forecast, till 2028

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.1.1 Increasing Demand for Secure, Sustainable, and Clean Energy

4.6.2 Restraints

4.6.2.1 High Cost of Production of Biofuels

4.7 Supply Chain Analysis

4.8 Industry Attractiveness - Porter's Five Forces Analysis

4.8.1 Bargaining Power of Suppliers

4.8.2 Bargaining Power of Consumers

4.8.3 Threat of New Entrants

4.8.4 Threat of Substitute Products and Services

4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Fuel Type

5.1.1 Ethanol

5.1.2 Biodiesel

5.1.3 Other Fuel Types

5.2 Feedstock

5.2.1 Palm Oil

5.2.2 Jatropha

5.2.3 Sugar Crop

5.2.4 Coarse Grain

5.2.5 Other Feedstock

5.3 Geography

5.3.1 North America

5.3.1.1 United States of America

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 Denmark

5.3.2.4 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Indonesia

5.3.3.4 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Chile

5.3.4.4 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 United Arab Emirates

5.3.5.2 Saudi Arabia

5.3.5.3 South Africa

5.3.5.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Abengoa Bioenergy SA

6.3.2 Cargill Incorporated

6.3.3 Shell PLC

6.3.4 Wilmar International Ltd.

6.3.5 Renewable Energy Group Inc.

6.3.6 Archer Daniels Midland Company

6.3.7 BP PLC

6.3.8 POET LLC

6.3.9 Neste Oyj

6.3.10 Verbio Vereinigte BioEnergie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Advancements in Production of Biofuels