풍력발전 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Global Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1642031

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

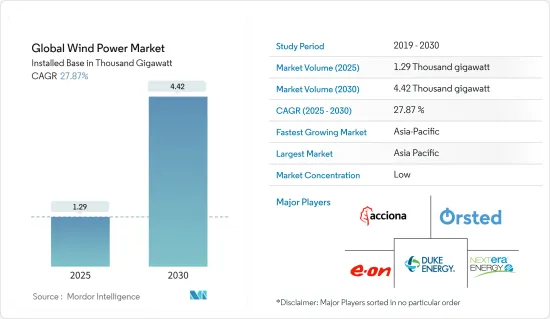

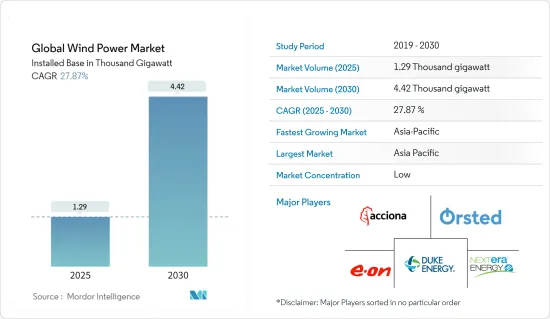

세계의 풍력발전 시장 규모는 2025년 1,290기가와트에서 2030년에는 4,420기가와트로 확대될 전망이며, 예측기간(2025-2030년)의 CAGR은 27.87%가 될 것으로 예측됩니다.

주요 하이라이트

중기적으로는 유리한 정부 시책, 향후 풍력발전 프로젝트에 대한 투자 증가, 풍력에너지 비용 절감 등의 요인이 풍력에너지 도입 증가로 이어져 2024년부터 2029년까지 시장을 견인할 것으로 예상됩니다.

가스 기반 및 태양광 발전과 같은 대체 에너지원의 채용이 증가하고 있다는 것은 시장 성장을 방해할 것으로 예상됩니다.

해상 풍력 터빈의 효율성과 생산 비용 절감의 기술적 진보는 세계 시장에 충분한 기회를 창출할 것으로 예상됩니다.

아시아태평양은 에너지 수요가 증가함에 따라 가장 빠르게 성장하는 시장입니다. 이 성장은 인도, 중국 및 호주를 포함한 이 지역 국가의 정부 지원 조치와 함께 투자가 증가하고 있기 때문입니다.

세계의 풍력발전 시장 동향

해상 풍력발전 부문은 대폭적인 성장이 예상됩니다.

유럽은 해상 풍력발전의 주요 대륙이며 세계에서 가장 큰 해상 풍력발전소가 운영되고 있습니다. 이 지역의 해상 풍력발전 용량은 유럽의 전력 수요를 충족하기에 충분한 규모이며, 앞으로도 증가의 길을 따라갈 것으로 예상됩니다.

해상 풍력은 육상 풍력보다 훨씬 빠르기 때문에 해상 풍력발전소의 설치는 유리한 시장이되고 있습니다. 또한 해상 풍력발전소는 육상 풍력발전소보다 풍속이 빠르고 육지 장애물이 적기 때문에 편리합니다.

해상 풍력발전은 지난 5년간 세계적으로 크게 증가하고 있습니다. 국제 신재생 에너지기구(IRENA)에 따르면 2023년 해상 풍력 에너지는 72.66GW로 2019년에 비해 1.57배로 증가했습니다. 앞으로 많은 풍력발전 프로젝트가 가동될 것으로 예상되기 때문에 예측 기간 동안 크게 증가할 것으로 예상됩니다.

2024년 3월 영국 정부는 신재생 에너지 프로젝트에 10억 파운드(12억 5,000만 달러)라는 가장 중요한 예산을 발표했지만, 그 중에는 해상 풍력발전에 8억 파운드(10억 달러), 부체식 해상 풍력발전과 지열 기술에 1억 500만 파운드(1억 3100만 달러)가 포함되어 있습니다.

마찬가지로 영국 정부는 2023년 9월 95개 신재생 에너지 이니셔티브에 차금결제계약(CFD)을 배분하여 370만kW의 청정에너지 용량을 확보할 것이라고 발표했습니다. 이 프로젝트에는 육상 풍력, 햇빛, 조력 에너지 개발이 포함됩니다. 또한 영국에 본사를 둔 Octopus Energy는 2030년까지 해상 풍력발전에 전 세계 200억 달러를 투자할 계획입니다. Octopus Energy Group의 자회사인 이 회사는 이 투자에 의해 연간 12기가 톤(GW)의 신재생 에너지 발전이 이루어지며, 이는 1,000만 가구분의 전력에 상당한다고 말하고 있습니다.

게다가 2024년 4월, 미국 에너지부의 풍력에너지 기술국(WETO)은 해상 풍력 플랫폼의 연구 개발 강화를 포함한 해상 풍력에 대한 4,800만 달러의 투자를 발표했습니다. 이러한 프로젝트를 통해 2024년부터 2029년까지 세계에서 풍력발전이 가속될 것으로 예상됩니다.

따라서 이러한 시나리오로 인해 해상 풍력발전 시장은 2024년부터 2029년까지 크게 성장할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 세계에서 가장 중요한 풍력발전 시장이며, 중국, 인도, 호주 등이 최고 시장입니다. 2024년부터 2029년까지 특히 중국에서의 성장이 눈부시고, 아시아태평양이 선두 자리에 뛰어날 가능성이 높습니다.

국제 신재생 에너지기구(IRENA)에 따르면 2023년 아시아 전체의 풍력에너지는 508.45GW로 2019년에 비해 97.32% 증가했습니다. 2023년 풍력발전량은 중국이 441.89GW로 선두가 되었고 인도가 44.74GW로 이어졌습니다. 향후 수년간 많은 풍력발전 프로젝트가 가동될 것으로 예상되기 때문에 이 숫자는 2024년부터 2029년까지 크게 증가할 것으로 예상됩니다.

이 지역 전체의 정부는 에너지 생산을 촉진하기 위해 복수의 신재생 에너지 프로젝트를 주요 조직에 제공합니다. 예를 들어, 2023년 12월, Apraava Energy는 인도의 카르나타카 주에 300MW의 풍력발전소를 건설하기 위해 Energy Corporation of India(SECI)가 실시하는 주간 송전(ISTS)의 1,200MW 경매 용량 프로젝트를 수주했습니다. 프로젝트의 건설은 전력구매계약(PPA)에 의한 것으로, 25년간 INR 3.24/kWh의 경쟁요금으로 이루어집니다.

또한 신재생 에너지 수요는 지난 수년간 아시아태평양 전역에서 급격히 증가하고 있으며, 기업은 아시아태평양 전역에서 대규모 투자를 하고 있습니다. 예를 들어 영국에 본사를 둔 Octopus Energy는 2023년 5월 아시아태평양 전역의 풍력발전 프로젝트를 포함한 신재생 에너지 프로젝트에 18억 달러를 투자한다고 발표했습니다. 이 회사는 2027년까지 풍력, 태양광 및 기타 청정 에너지 프로젝트에 투자하는 것 같습니다. 이 투자는 2030년까지 해상 풍력발전 용량을 150GW 증가시키는 일본의 풍력에너지 목표에도 초점을 맞추었습니다. 이러한 목표와 투자는 모두 2024년부터 2029년까지 시장을 견인할 가능성이 높습니다.

따라서 대규모 풍력발전의 설치, 향후 프로젝트, 해상 풍력 부문의 확대계획은 2024년부터 2029년까지 아시아태평양시장을 견인할 것으로 예상됩니다.

세계의 풍력발전 산업 개요

풍력발전 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 Acciona Energia SA, Duke Energy Corporation, Electricite de France(EDF) SA, Orsted AS, NextEra Energy Inc., E.ON SE 등을 들 수 있습니다.

The Global Wind Power Market size in terms of installed base is expected to grow from 1.29 thousand gigawatt in 2025 to 4.42 thousand gigawatt by 2030, at a CAGR of 27.87% during the forecast period (2025-2030).

Key Highlights

In the medium term, factors such as favorable government policies, the increasing investment in upcoming wind power projects, and the reduced cost of wind energy have led to increased adoption of wind energy and are expected to drive the market between 2024 and 2029.

The increasing adoption of alternative energy sources, such as gas-based and solar power, is expected to hinder the growth of the market.

Nevertheless, technological advancements in efficiency and decreased production costs of offshore wind turbines are expected to create ample opportunity for the global market.

Asia-Pacific is the fastest-growing market due to the rising energy demand. This growth is attributed to increasing investments, coupled with supportive government policies in the countries of this region, including India, China, and Australia.

Global Wind Power Market Trends

The Offshore Wind Power Sector is Expected to Witness Significant Growth

Europe is the leading continent in offshore wind and is home to the most significant operational wind farms globally. The region's offshore wind capacity is large enough to meet Europe's electricity needs, which will only continue to grow in the upcoming years.

Installing wind farms in offshore areas is becoming a lucrative market because offshore winds are much faster than onshore winds. Also, offshore wind farms are more convenient than onshore wind farms, given that offshore areas have more wind speed and less land obstruction.

Offshore wind energy has increased significantly over the last five years worldwide. According to the International Renewable Energy Agency (IRENA), in 2023, offshore wind energy was 72.66 GW, an increase of 1.57 times compared to 2019. The number is expected to rise significantly during the forecast period as many wind projects are expected to be operational in the upcoming years.

In March 2024, the government of the United Kingdom announced the most significant budget of GBP 1 billion (USD 1.25 billion) for renewable energy projects, which includes GBP 800 million (USD 1 billion) for offshore wind and GBP 105 million (USD 131 million) for floating offshore wind and geothermal technologies.

Similarly, in September 2023, the United Kingdom's Government announced the distribution of Contract for Difference (CFDs) to 95 new renewable energy initiatives, ensuring 3.7 GW of clean energy capacity. These projects include onshore wind, solar, and tidal energy developments. Furthermore, Octopus Energy, based in the United Kingdom, plans to invest USD 20 billion globally in offshore wind by 2030. The company, which is a subsidiary of Octopus Energy Group, stated that the investment will generate 12 gigatonnes (GW) of renewable electricity per year, enough to power 10 million homes.

Furthermore, in April 2024, the United States Department of Energy's Wind Energy Technologies Office (WETO) announced an investment of USD 48 million in offshore wind, including enhancing the research and development of offshore wind platforms. These types of projects are expected to accelerate wind energy generation across the world between 2024 and 2029.

Hence, with such a scenario, the offshore wind power market is expected to grow significantly from 2024 to 2029.

Asia-Pacific is Expected to Dominate the Market

Asia-Pacific is the world's most significant wind power market, with top markets including China, India, and Australia. Encouraging growth, particularly in China, is likely to propel it to the top spot between 2024 and 2029.

According to the International Renewable Energy Agency (IRENA), in 2023, wind energy across Asia was 508.45 GW, an increase of 97.32% compared to 2019. China generated 441.89 GW of wind energy in 2023 and became the leader, followed by India, which generated 44.74 GW. The number is expected to rise significantly between 2024 and 2029 as many wind projects are expected to be operational in the upcoming years.

The government across the region offers multiple renewable energy projects to the leading organizations to boost energy production. For instance, in December 2023, Apraava Energy received the 1200 MW auction capacity project of the Inter-State Transmission System (ISTS) conducted by the Energy Corporation of India (SECI) to construct a 300 MW Wind farm in Karnataka, India. The project's construction is as per the Power Purchase Agreement (PPA), which is for 25 years at a competitive tariff of INR 3.24/kWh.

Furthermore, the demand for renewable energy has been rising exponentially across the region for the past few years, and companies are investing significantly across Asia-Pacific. For instance, in May 2023, octopus Energy, a United Kingdom-based company, announced an investment of USD 1.8 billion for renewable energy projects, including wind energy projects across Asia-Pacific. The company is likely to invest in wind, solar, and other clean energy projects by 2027. The investment also focused on Japan's wind energy target to increase offshore wind energy capacity by 150 GW by 2030. All these types of targets and investments are likely to drive the market between 2024 and 2029.

Therefore, large-scale wind power installations, upcoming projects, and plans to expand the offshore wind segment are expected to drive the Asia-Pacific market between 2024 and 2029.

Global Wind Power Industry Overview

The wind power market is fragmented. Some of the key players in this market are Acciona Energia SA, Duke Energy Corporation, Electricite de France (EDF) SA, Orsted AS, NextEra Energy Inc., and E.ON SE.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Renewable Energy Mix, 2023

4.3 Wind Power Installed Capacity and Forecast in GW, till 2029

4.4 Recent Trends and Developments

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing Investments in Offshore Wind Power Projects

4.5.1.2 Supportive Government Policies

4.5.2 Restraints

4.5.2.1 Increasing Adopting of Alternative Clean Energy Sources (Ex: Solar, Hydro)

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Location

5.1.1 Onshore

5.1.2 Offshore

5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)})

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 United Kingdom

5.2.2.2 France

5.2.2.3 Norway

5.2.2.4 Germany

5.2.2.5 Spain

5.2.2.6 Turkey

5.2.2.7 Russia

5.2.2.8 NORDIC

5.2.2.9 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Japan

5.2.3.4 Malaysia

5.2.3.5 Thailand

5.2.3.6 Indonesia

5.2.3.7 Vietnam

5.2.3.8 Rest of Asia-Pacific

5.2.4 Middle East and Africa

5.2.4.1 United Arab Emirates

5.2.4.2 Egypt

5.2.4.3 Saudi Arabia

5.2.4.4 Nigeria

5.2.4.5 Qatar

5.2.4.6 Rest of Middle East and Africa

5.2.5 South America

5.2.5.1 Brazil

5.2.5.2 Chile

5.2.5.3 Argentina

5.2.5.4 Colombia

5.2.5.5 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements