High Speed Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1641887

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

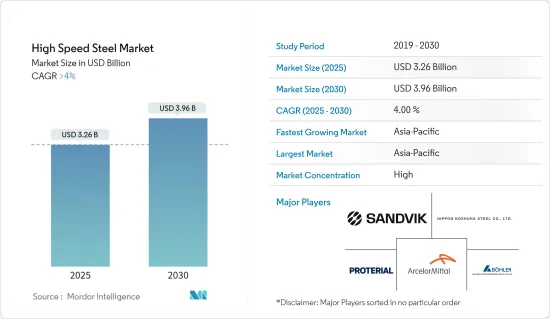

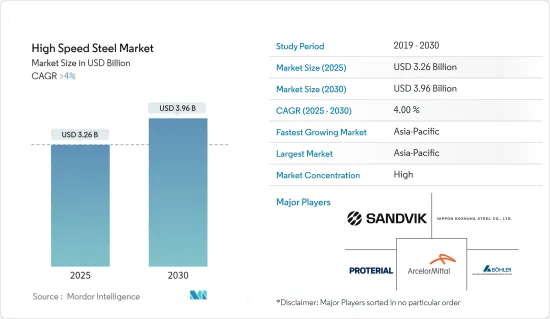

고속도강 시장 규모는 2025년에 32억 6,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 4%를 넘어, 2030년에는 39억 6,000만 달러에 달할 것으로 예측됩니다.

COVID-19의 대유행은 세계의 고속도강(HSS) 시장에 큰 영향을 주었으며 공급망 혼란과 수요 감소를 일으켰습니다. 그러나 2021년 이후 경제가 재개되고 산업활동이 재개됨에 따라 시장은 점차 회복되고 있습니다. 공급망의 회복력에 다시 주목을 받고 있습니다. 자동차나 항공우주 등의 산업이 기세를 되찾으면서 HSS 수요가 증가하고 시장의 추가 회복이 예상됩니다.

주요 하이라이트

시장 성장의 주요 요인은 산업용도 증가와 항공우주 산업 수요 증가입니다.

다양한 최종 용도 부문에서 탄화물 기반 절삭 공구의 사용이 증가하는 것은 시장 성장을 둔화시킬 가능성이 높습니다.

향후 수년간 기술의 급속한 변화로 인해 고속도강 시장의 성장이 예상됩니다.

예측 기간 동안 아시아태평양은 고속도강 시장을 독점할 것으로 예상됩니다.

고속 도강 시장 동향

자동차산업이 시장을 독점할 전망

고속도강은 자동차의 경량화, 고강성화, 장소에 따라서는 에너지 흡수가 뛰어난 등 자동차 산업에서 다양한 형태로 사용되고 있습니다.

고속도강은 기계적 특성과 범위, 두께와 폭의 능력, 열간 및 냉간 압연의 가용성, 코팅 사양, 화학 조성 사양 등 자동차 산업 수요를 높이는 다양한 특성을 가지고 있습니다.

자동차 산업에서 강재의 강도는 일반적으로 화학 조성, 열 이력 및 생산 일정 동안 통과하는 변형 공정에 따라 변화하는 미세 구조에 의해 결정됩니다.

고속도강은 특히 무게가 연료 사용률에 크게 영향을 미치는 자동차 산업의 경우 일반 스틸보다 많은 장점이 있습니다. 용접성, 피로, 정적 강도, 음극 보호, 내수소 취화성 등의 기계적 특성은 자동차 산업에 유용합니다.

고속도강은 캠 샤프트와 크랭크 샤프트 스프로킷, 커넥팅로드, 싱크로 나이저 링, 베어링 캡, 오일 펌프 기어 등의 구조 용도에 사용됩니다. 이러한 용도에 사용되는 스테인레스 스틸에는 엔진 밸브 시트도 포함됩니다. Fe-Cr-Mn-Si계 재료 등의 철계 합금은 쇼크 업소버 부품, 유압 시스템용 필터, 매니폴드 플랜지, 배기 컨버터 출구 플랜지, 배기 가스 재순환 시스템 등에 사용됩니다.

자동차 산업은 유행 이후 기존 자동차와 전기자동차 모두에 대한 수요가 급증하고 있습니다.

국제자동차공업회(OICA)에 따르면 2022년에는 세계 약 8,501만대의 자동차가 생산되었으며, 2021년 8,020만대에 비해 5.99%의 성장률을 보였습니다.

OICA에 따르면 북미에서는 2022년 자동차 생산 대수는 1,479만 8,146대로 2021년 1,346만 7,065대에 비해 9.88% 증가했습니다. 또한 북미에서는 2022년 전기자동차 판매 대수가 110만 8,000대가 되었으며 2021년 74만 8,000대에 비해 크게 증가했습니다.

유럽에서는 독일이 주요 자동차 제조업체 중 하나입니다. 독일 자동차 제조업은 유럽 자동차 생산 전체의 상당 부분을 차지합니다. 이 나라에는 Volkswagen, Mercedes-Benz, Audi, BMW, Porsche 등 주요 자동차 제조 브랜드가 있습니다.

국제자동차제조자기구(OICA)에 따르면 2022년 동국의 자동차 생산 대수는 367만 7,820대로 2021년 330만 8,692대에 비해 11% 증가했습니다.

전반적으로, 연비 향상과 자동차 경량화를 위한 고속도강의 사용 증가는 자동차 산업의 성장을 뒷받침할것입니다.

아시아태평양이 시장을 독점할 전망

앞으로 수년간 아시아태평양이 고속도강의 최대 시장이 될 것으로 예상됩니다. 중국과 인도 등 국가에서는 자동차, 항공우주 등의 산업이 성장하여 고속도강 수요가 급증하고 있습니다.

아시아태평양의 생산과 판매는 주로 중국, 인도, 일본 등의 국가들이 독점하고 있으며, 이들 국가는 대기업 자동차 제조업체와 방대한 수의 생산 거점으로 구성되어 있습니다.

중국 기차공업협회(CAAM)에 따르면 2022년 자동차 총생산 대수는 2,700만대로 2021년 대비 3.4% 증가했으며 중국은 세계적으로 가장 중요한 자동차 생산 거점이 되었습니다.

중국에서는 전기차 생산과 판매 확대에 주안을 두고 있습니다. 이 나라는 2025년까지 연간 700만대의 전기차를 생산하는 목표를 내걸고 있습니다. 2025년까지 중국의 신차 생산 대수의 20%를 전기자동차로 하는 것을 목표로 하고 있습니다.

인도는 이 지역에서 2위의 자동차 제조업체가 되었습니다. 인도자동차공업회(SIAM)에 따르면 2022-23년에는 2021-2022년도 대비 약 12.55% 증가하여 2,593만 1,867대를 기록했습니다.

일본 자동차 공업회에 따르면 2023년도 국내 자동차 생산 대수는 14.84% 증가한 899만 8,538대를 기록했습니다.

예측 기간 동안 이러한 변화는 고속도강의 요구를 높일 가능성이 높습니다.

고속 도강 산업 개요

고속 도강 시장은 그 특성상 부분적으로 통합되어 있습니다. 시장의 주요 기업으로는 Sandvik AB, voestalpine BOHLER Edelstahl GmbH & Co.KG, NIPPON KOSHUHA STEEL, PROTERIAL Ltd, ArcelorMittal 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

다양한 산업용도에서의 용도 확대

항공우주산업에서의 수요 증가

기타 촉진요인

억제요인

다양한 최종 용도 부문에서 탄화물 기반 절삭 공구 사용 증가

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

유형

텅스텐 고속 도강

몰리브덴 고속 도강

기타 유형(코발트 고속 도강, 크롬 고속 도강, 바나듐 고속 도강)

제품 유형

금속 절삭 공구

냉간 공구

기타 제품 유형(밀링 공구, 드릴 공구 등)

최종 사용자 산업

자동차산업

항공우주

플라스틱

기타 최종 사용자 산업(광업, 제조, 공구 제조 등)

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

노르딕

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동?아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%) 분석**/랭킹 분석

주요 기업의 전략

기업 프로파일

ArcelorMittal

CRS Holdings LLC

ERASTEEL

Friedr. Lohmann GmbH

NACHI-FUJIKOSHI CORP.

NIPPON KOSHUHA STEEL CO. LTD

PROTERIAL Ltd

Sandvik AB

thyssenkrupp AG

VILLARES METALS SA

voestalpine BOHLER Edelstahl GmbH & Co. KG

제7장 시장 기회와 앞으로의 동향

급속한 기술 향상

기타 기회

SHW

영문 목차

영문목차

The High Speed Steel Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 3.96 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The COVID-19 pandemic significantly impacted the global high-speed steel (HSS) market, causing disruptions in supply chains and reducing demand. However, since 2021, the market has been gradually recovering as economies reopened and industrial activities resumed. There is a renewed focus on supply chain resilience. As industries like automotive and aerospace regain momentum, the demand for HSS is expected to increase, driving further recovery in the market.

Key Highlights

The major factors driving the market's growth are the growing number of industrial uses and the increasing demand from the aerospace industry.

The growing use of carbide-based cutting tools in different end-use sectors is likely to slow the market's growth.

In the coming years, the high-speed steel market is expected to grow due to the rapid changes in technology.

Asia-Pacific is expected to dominate the high-speed steel market over the forecast period.

High Speed Steel Market Trends

The Automotive Industry is Expected to Dominate the Market

High-speed steel is used in many ways in the automotive industry to make vehicles lighter, stiffer, and better at absorbing energy in some places.

High-speed steel has various properties that enhance its demand in the automotive industry, such as mechanical properties and ranges, thickness and width capabilities, hot- and cold-rolled availability, coating specifications, and chemical composition specifications.

In the automotive industry, steel's strength is usually determined by its microstructure, which varies based on its chemical makeup, its history with heat, and the deformation processes it goes through during its production schedule.

High-speed steel has a lot of advantages over regular steel, especially in the automotive industry, where weight is a significant factor in how well fuel is used. The mechanical properties, such as weldability, fatigue, static strength, cathodic protection, and resistance to hydrogen embrittlement, are useful to the auto industry.

High-speed steel is used in structural applications such as camshaft and crankshaft sprockets, connecting rods, synchronizer rings, bearing caps, oil pump gears, etc. The stainless steel used in these applications includes engine valve seats. Ferrous-based alloys, such as Fe-Cr-Mn-Si materials, are used in shock absorber parts, filters for hydraulic systems, manifold flanges, exhaust converter outlet flanges, and exhaust gas recirculation systems.

The automotive industry has been witnessing an upsurge in demand for both conventional and electric vehicles post-pandemic, primarily due to the increased traveling activities of people across the globe.

According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, around 85.01 million vehicles were produced worldwide, showcasing a growth rate of 5.99% compared to 80.20 million vehicles in 2021.

In North America, according to the OICA, automotive production in 2022 accounted for 14,798,146 units, an increase of 9.88% compared to the show in 2021, which was reportedly 13,467,065 units. Additionally, in North America, the sales of electric vehicles in 2022 accounted for 1,108 thousand units, compared to 748 thousand unit sales in 2021.

In Europe, Germany is among the key manufacturers of vehicles. The automobile manufacturing industry in Germany is a prominent shareholder of the overall automotive production in the European region. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, Porsche, etc.

According to the Organization Internationale des Constructeurs d'Automobiles (OICA), in 2022, the country produced 3,677,820 vehicles, which increased by 11% compared to 3,308,692 cars in 2021.

Overall, the increasing usage of high-speed steel for better fuel efficiency and lighter vehicles will boost the growth of the automotive industry.

Asia-Pacific is Expected to Dominate the Market

During the next few years, the Asia-Pacific region is expected to be the largest market for high-speed steel. In countries like China and India, the growth of industries like automotive, aerospace, and others has caused the demand for high-speed steel to surge.

The production and sales in the Asia-Pacific region are primarily dominated by countries like China, India, and Japan, which consist of large automotive manufacturers and a vast number of production bases within the countries.

According to the China Association of Automobile Manufacturers (CAAM), China had the most significant automotive production base globally, with a total vehicle production of 27 million units in 2022, an increase of 3.4% compared to 2021.

In China, the main focus is to increase production and sales of electric vehicles. The country has set a target to produce 7 million electric vehicles per year by 2025. By 2025, the goal is to have electric vehicles comprise 20% of total new vehicle production in China.

India has become the second-largest automotive vehicle manufacturer in the region. According to the Society of Indian Automobile Manufacturers (SIAM), in FY 2022-23, the total number of automobile manufacturers in the country grew by about 12.55% compared to FY 2021-2022, recording 25,931,867 units.

According to the Japan Automobile Manufacturers Association (JAMA), motor vehicle production in the country in 2023 grew by 14.84%, recording 8,998,538 units.

During the forecast period, these changes are likely to increase the need for high-speed steel.

High Speed Steel Industry Overview

The high-speed steel market is partially consolidated in nature. Some of the major players in the market include Sandvik AB, voestalpine BOHLER Edelstahl GmbH & Co. KG, NIPPON KOSHUHA STEEL CO. LTD, PROTERIAL Ltd, and ArcelorMittal.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Usage in Different Industrial Applications

4.1.2 Increasing Demand from Aerospace industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 The Rising Use of Carbide-based Cutting Tools Across Various End-use Sectors

4.2.2 Other Restraints

4.3 Industry Value-Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Tungsten High Speed Steel

5.1.2 Molybdenum High Speed Steel

5.1.3 Other Types (Cobalt High-Speed Steel, Chromium High-Speed Steel, and Vanadium High-Speed Steel)

5.2 Product Type

5.2.1 Metal Cutting Tools

5.2.2 Cold Working Tools

5.2.3 Other Product Types (Milling Tools, Drilling Tools, etc.)

5.3 End-user Industry

5.3.1 Automotive

5.3.2 Aerospace

5.3.3 Plastics

5.3.4 Other End-user Industries (Mining, Manufacturing, Tool Making, etc)

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Spain

5.4.3.6 NORDIC

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Nigeria

5.4.5.4 Qatar

5.4.5.5 Egypt

5.4.5.6 United Arab Emirates

5.4.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements